Abstract

This study aims to examine the stochastic convergence of per capita carbon dioxide (CO2) emissions in 21 OECD countries and 19 emerging market economies. After approximating both sharp and smooth breaks, the panel unit root tests are performed to test the convergence. The empirical results suggest stochastic convergence for the two groups of countries. However, the results are different when tests for individual countries are conducted separately. Specifically, CO2 emissions of only four OECD countries and four emerging market economies show evidence of convergence if smooth breaks are not considered. With the inclusion of both sharp and smooth breaks, convergence is observed for 11 OECD countries and 10 emerging market economies. These findings may have implications for climate change policy making in selected economies.

Similar content being viewed by others

Explore related subjects

Discover the latest articles, news and stories from top researchers in related subjects.Avoid common mistakes on your manuscript.

Introduction

The Kyoto Protocol requests that signatory countries cut emissions of CO2 and five other greenhouse gases. According to Paris Climate Agreement, the OECD countries commit to keep carbon concentration in the atmosphere at 450 ppm and to restrict the increasing trend of global mean temperature. Thus, CO2 emission has been viewed as the main threat to environmental pollution. Cutting CO2 emission has been listed in many countries’ development strategies. To achieve this goal, a good understanding of the convergence and divergence of CO2 emission is important (Lee and Chang, 2008). In fact, more and more studies pay attention to the convergence and divergence of CO2 emission through various research methods (Aldy, 2006; Criado and Grether, 2011; Cheong et al., 2016; Wu et al., 2016; Lee and Chang, 2008; Lee et al., 2008; Romero-Ávila, 2008; Westerlund and Basher, 2008 and Lee and Lee, 2009). However, no consistent conclusions about the convergence of CO2 emission have been reached. To gain further insights into this issue, more advanced research methods are needed (Lee et al., 2008 and Cheong et al., 2016).

In this paper, we first use a more powerful panel unit root test with smooth and sharp breaks to test the classical convergence hypothesis. Specifically, if CO2 emission series is nonstationary, an external shock on CO2 emission would have permanent effects and hence affect macroeconomic performance. In contrast, if the null hypothesis is rejected, the CO2 emission is stationary and exhibits the I(0) process, a shock on CO2 emission would only have temporary effects. In other words, if CO2 emission follows the I(0) process, the CO2 emission series will return to its mean or trend over time. The environmental protection action would be slightly mandatory (Lee and Chang, 2008) and CO2 emission would be convergent over time. In contrast, if CO2 emission is nonstationary, the environmental protection policy could significantly affect the path of CO2 emission.

The contribution of this study can be listed as follows. It is commonly accepted that the development of an economy will be accompanied by structural changes, from agriculture-led to industry-led and eventually to service-led growth. Obviously, the industrial sector will likely generate more CO2 emission because of its burning of fossil fuels such as oil, coal and natural gas. The changes in economic structure would significantly affect the CO2 emission. In other words, CO2 emission must have structural breaks in the development process (Lee and Chang, 2008). To capture the structural breaks, most previous studies are inclined to use dummies. However, dummies could only approximate sharp breaks, while the smooth breaks in most cases cannot be captured. The failure to capture smooth breaks would result in the failure of traditional tests of stochastic convergence. To fill this gap in the existing studies, we use both dummies and the Fourier function to generate time-varying intercepts which are fitted to the path of CO2 emission.

The empirical findings show stochastic convergence for the two groups of countries, namely OECD and emerging market countries. Specifically, the CO2 emissions per capita are not converging for Australia, Belgium, Finland, Ireland, Japan, Netherlands, New Zealand, Portugal, Sweden and the UK in OECD group and Brazil, South Africa, Hungary, Peru, the Philippines, Poland, Thailand, the United Arab Emirates and Qatar in emerging market economies, respectively. External shocks like oil shocks, financial crisis and environmental protection policies have profound impacts on the path. For the rest of the countries, CO2 emission per capita is converging.

The remainder of the paper is organized as follows. The “Literature review” section reviews research methods in existing studies. The “Econometric models” section presents the datasets and descriptive statistics. The “Datasets and descriptive statistics” section introduces the econometric methods. The “Empirical results” section discusses the empirical results and economic implications. The last section concludes the paper.

Literature review

Pettersson et al. (2014) suggest that the existing empirical studies related to carbon convergence could be divided into four strands in terms of their research methods. They can be called nonparametric tests, the stochastic approach (our paper could be categorized into this strand) and the distributional analyses and index decomposition analyses.

Non-parametric test

Menegaki and Tiwari (2019) provide a detailed review of this strand of literature. Strazicich and List (2003) use cross-sectional regression to test the σ and β convergence for 21 OECD countries.Footnote 1 They find the per capita carbon emission converges conditional on the gasoline price and winter temperature. Besides, Strazicich and List (2003) suggest that due to the sizes of different countries some caution should be exercised when the effects of winter temperature are considered. Van (2005) examines the CO2 emission for 100 countries, including 26 high-emission countries. They find evidence of convergence for high-emission countries, but evidence of divergence for the whole sample. Stegman and McKibbin (2005) test the σ and β convergence for 26 OECD countries and 97 global countries. They find convergence only for OECD countries. Aldy (2006) also considers the OECD group and global economies together. The conclusions are similar to those obtained by Stegman and McKibbin (2005). Panopoulou and Pantelidis (2009) test σ convergence for 128 countries and divergence for the sample as a whole. Brock and Taylor (2010) cover the 21 OECD countries and find unconditional and conditional β convergence by employing a cross-sectional approach. Jobert et al. (2010) focus on testing the convergence of 22 European countries and further indicate both conditional and absolute convergence for the group. Conversely, Camarero et al. (2013) examine the σ convergence of carbon dioxide intensity. A more recent piece of work by Ulucak and Apergis (2018) uses a club clustering approach and finds the presence of a small number of convergence clubs.

Stochastic convergence test

Strazicich and List (2003) use the panel unit root test proposed by Im et al. (2003) to examine the stochastic convergence of per capita carbon dioxide emission in 21 OECD countries. They find stochastic convergence of CO2 emission for the group. Barassi et al. (2008) employ a set of unit root tests to check the convergence of carbon dioxide emission, including the methods proposed by Hadri (2000) and Im et al. (2003). They find divergence in per capita CO2 emission in OECD countries. Romero-Ávila (2008) applies the panel unit root test with multiple structural breaks proposed by Carrion-i-Silvestre et al. (2005) to examine the stochastic convergence of CO2 emission. The empirical results support the conclusions of Strazicich and List (2003) and reconfirm the converging behaviour of CO2 emission. They compare the results obtained with and without considering structural breaks. Under the condition of no structural breaks, the null hypothesis is rejected for 18 out of 23 countries. However, the null is rejected for 3 out of 23 countries when structural breaks are considered. In other words, the structural breaks significantly affect the estimation. Westerlund and Basher (2008) apply panel unit root tests proposed by Bai and Ng (2004), Phillips and Sul (2003) and Moon and Perron (2004) to re-examine the convergence of CO2 emission. Their empirical results exhibit convergence for the panel as a whole. Lee and Chang (2008) use a panel Augmented Dickey-Fuller (ADF) test to check the convergence of per capita CO2 emission. Their findings show that 14 out of 21 OECD countries exhibit divergence. Additionally, they suggest that traditional panel unit root tests would result in misleading estimation results. Lee and Chang (2008) also use the panel unit root test proposed by Carrion-i-Silvestre et al. (2005) to check the stationarity of CO2 emission for the OECD countries. Similar to the results of Strazicich and List (2003) and Westerlund and Basher (2008), the stochastic convergence is verified for OECD countries. Camarero et al. (2008) use the SURADF unit root test proposed by Breuer et al. (2002) to examine convergence and they find divergence for most of the OECD countries. Barassi et al. (2011) test the convergence of CO2 emission with a long memory approach and show that 13 out of 18 countries are divergent. Christidou et al. (2013) use both linear and nonlinear unit root tests to check the stationarity of per capita CO2 emission for 36 countries. The empirical results suggest that per capita CO2 emission is stationary by implementing a nonlinear method. Presno et al. (2018) test the stochastic convergence for 28 OECD countries through a nonlinear stationarity test with quadratic trends. Most of the countries are nonstationary. Tiwari et al. (2016) use Fourier function to approximate the structural breaks, by implementing the method proposed by Becker et al. (2006). They find stationarity for 27 countries in Sub-Saharan Africa. Furthermore, when using a panel unit root test with a SPSM procedure, the stationarity holds in 15 of the countries in Sub-Saharan Africa. Lastly, when a Fourier function is added into the panel unit root test with a Sequential Panel Selection Model (SPSM) procedure, Tiwari et al.(2016) find that the CO2 emission for all of the 35 Sub-African countries is stationary. Ahmed et al. (2017) use unit root tests with wavelet analysis proposed by Fan and Gençay (2010) and further reveal that stationarity holds in 38 countries and non-stationarity is observed in the rest of 124 countries.

Distributional dynamics approach

The distributional dynamics method mainly contains two approaches, namely the traditional Markov transition matrix approach and stochastic Kernel approach. Stegman (2005) uses the stochastic kernels method to check the convergence of CO2 emission for 97 countries and they find no convergence for the whole sample. Nguyen (2005) implements a nonparametric Epanechnikov kernel with Silverman bandwidth choice to determine the convergence of CO2 emission. The empirical findings offer little evidence of convergence. Aldy (2006) employs the traditional Markov transition matrix approach and finds divergence of CO2 emission. This conclusion is questioned by Lee and Chang (2008) due to the lower testing power of the Markov transition matrix. Ezcurra (2007) uses the method of nonparametric Gaussian adaptive kernel with Silverman bandwith choice to test 87 countries. The empirical results show convergence among industrial economies and the top emitters, and divergence for the rest of the countries. Herrerias (2011) also uses a nonparametric distributional approach, but only focuses on EU countries, covering the period from 1920 to 2007. Her results show faster convergence for the group after 1970. Recently, Cheong et al. (2016) employ a stochastic kernel approach to investigate the convergence of CO2 emission in Chinese prefectural level cities. Furthermore, Wu et al. (2016) use a continuous distributional dynamics approach to examine the convergence of CO2 in Chinese cities. They believe the convergence of CO2 emission among Chinese cities is largely decided by geographical, income and environmental policy factors. Their conclusions are similar to those by Criado and Grether (2011).

Index decomposition analysis

There is also a large body of studies focusing on the decomposition of CO2 emissions through various index approaches such as the Theil decomposition analysis, Divisia decomposition analysis and Fisher index decomposition analysis. Duro and Padilla (2006) utilize Theil decomposition analysis to examine the inequalities in per capita CO2 emissions. They find that the inequalities in CO2 emissions are mainly caused by income inequality. Hatzigeorgiou et al. (2008) utilize the Divisia decomposition analysis to decompose CO2 emissions into four components including income effect, energy intensity effect, fuel share effect and population effect. Similar to the findings in Duro and Padilla (2006), Hatzigeorgiou et al. suggest the main contributor to increasing CO2 emissions is the income effect. In contrast, energy intensity effect mainly causes the decrease in CO2 emissions. By using the Fisher index decomposition analysis, Su and Ang (2014) propose a generalized Fisher index in the context of structural decomposition analysis (SDA) and use this method to analyse the carbon emissions embodied in China’s export with sectoral evidence. They find the equipment and machinery manufacturing and raw material manufacturing are main contributors to CO2 emissions change. One recent study by Ang and Goh (2019) presents a detailed literature review of the CO2 emissions decomposition.

After the review of the abovementioned studies, we conclude that there are still no consistent conclusions about to the convergence of CO2 emission. With the increasing power of the tests, more accurate empirical findings could be obtained. This paper aims to provide evidence of stochastic convergence of per capita CO2 emissions through a newly proposed econometric method which approximates both sharp and smooth breaks in the data series.

Econometric models

This study employs the KPSS test with sharp and smooth breaks. The test was proposed by Bahmani-Oskooee et al. (2014) to examine the convergence of CO2 emissions per capita. It combines the techniques by Carrion-i-Silvestre et al. (2005) and Enders and Lee (2012), and is also utilized in Cai and Menegaki (2019a).Footnote 2 Consider a data generation process (DGP), yi, t, which includes a deterministic trend di, t and stationary error term εi, t:

where, i = 1, 2, …, N in the panel. ai, t, T, m and ki represent intercept, trend, number of observations, the maximum number of breaks and flexible frequency, respectively. DUi, l, t and DTi, l, t are dummy variables in the intercept and trend of lth break TBi, l of ith individual, respectively. DUi, l, t and DTi, l, t are used to approximate sharp breaks. Further, \( \sin \left(\frac{2\pi {k}_it}{T}\right) \) and \( \cos \left(\frac{2\pi {k}_it}{T}\right) \) are Flexible Fourier Function to approximate the smooth breaks in the ith individual. Specifically, DUi, l, t and DTi, l, t are defined as follows:

To locate the breaking dates TBi, l, the procedure proposed by Bai and Perron (1998) is utilized. This method is also employed in the study of Carrion-i-Silvestre et al. (2005). The method of Bai and Perron (1998) minimizes the sum of squared residuals (SSR) in Eq. 1:

Moreover, to select the optimal frequency \( {k}_i^{\ast } \), Becker et al. (2006), Enders and Lee (2012) and Bahmani-Oskooee et al. (2014) use a F test which can be expressed as:

where, \( {SSR}_0\left({k}_i^{\ast}\right) \) and \( {SSR}_1\left({k}_i^{\ast}\right) \) denote the SSR from Eq. 1 with and without nonlinear components. q is the number of the regressors. Due to the nuisance parameters, we use Monte Carlo simulation to generate critical values for \( F\left({k}_i^{\ast}\right) \) with 10,000 replications. After determining both sharp and smooth breaks in Eq. 1, we compute the following univariate KPSS test based on Kwiatkowski et al. (1992):

where \( {\hat{S}}_{i,t} \) denotes the partial sum process which can be estimated through OLS in Eq. 1. \( {\hat{w}}_i \) is a consistent estimate of the long-run variance of εi, t in Eq. 1. As suggested by Carrion-i-Silvestre et al. (2005), the LMi test highly depends on the location of break TBi, l in Eq. 3. To test the null of a stationary panel with sharp and smooth breaks, Bahmani-Oskooee et al. (2014) utilize the following test:

where μ and σ are the mean and standard deviation of LMi, respectively. To compute the finite sample critical values, bootstrap procedure is utilized with 20,000 replications.

Datasets and descriptive statistics

Per capita CO2 emission (metric tons) is drawn from the World Development Indicators which cover the period from 1960 to 2014. For consistent and comparative purposes, we use the same OECD countries as those used by Strazicich and List (2003), including Australia, Austria, Belgium, Canada, Denmark, Finland, France, Greece, Iceland, Ireland, Italy, Japan, Netherlands, New Zealand, Norway, Portugal, Spain, Sweden, Switzerland, the UK and the USA. For emerging market countries, we select the BRICS countries (excluding Russia due to its limited data span) and 15 other countries. The emerging market countries are classified by Morgan Stanley Capital International. In this paper, similar to Paramati et al. (2016), the emerging market countries includes Brazil, Chile, China, India, South Africa, Colombia, Egypt, Arab Rep., Hungary, Indonesia, Korea, Rep., Mexico, Peru, the Philippines, Poland, Thailand, Turkey, Pakistan, the United Arab Emirates and Qatar.

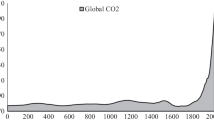

We focus on these two groups of countries as they represent the developed and developing economies in the world, respectively. According to the World Development Indicators, CO2 emissions of OECD and emerging market countries in 1960 account for 51 and 16% of global total emissions, respectively (Fig. 1). The two groups together generated about two thirds of global CO2 emission in that year. By 2014, though this number for the OECD declines to 26%, it dramatically increases to 47% for the emerging economies. Together, the two groups have a share of 73% of global CO2 emission in 2014. Interestingly, CO2 emission shares of the OECD and emerging market countries were about the same in 2005 when the Kyoto Protocol was in force. By 2050, these shares would be 25% for the OECD economies and 60% for the emerging countries. Thus, the two groups of countries covered in this paper are representative due to their substantial shares of CO2 emissions in the world. In addition, their CO2 emissions also tend to follow different trajectories over time. Thus, there may be different policy implications for emission control among the two groups of economies.

CO2 emission shares of OECD and emerging market countries, 1960–2014

The descriptive statistics are listed in Table 1. In the first group of the 21 OECD countries, the USA has the maximum per capita CO2 emission of 22.5 mt, and Portugal has the minimum of 0.9 mt. In addition, the largest standard deviation of 2.8 is observed in Australia. The skewness is positive only for Belgium, France, Portugal and Sweden. The kurtosis is over 3 for Austria, Canada, Finland, Italy, Japan, Netherlands and Switzerland. In terms of the group of 19 emerging market countries, the United Arab Emirates, which is one of the most important oil exporters, has the maximum CO2 emission per capita of 100.7 mt. Thailand has the minimum CO2 emission per capita of 0.1 mt. Unlike the OECD countries, per capita CO2 emission is more likely to be positively skewed for 14 of the other 19 countries. The kurtosis for China, Peru, Qatar and the United Arab Emirates is over 3 and hence exhibits leptokurtosis. We consider these groups of countries because they are the main CO2 emitters in the world. Furthermore, with the growth of emerging market economies, CO2 emissions are more likely to be emitted by these countries. Lastly, due to the changes in economic structure, per capita CO2 emission is more likely to have structural breaks. In other words, traditional panel unit root tests for the stationarity of CO2 emission per capita may be biased.

Empirical results

This section contains the following three parts corresponding to three different research methods, namely panel unit root test without structural breaks, panel unit root test with sharp breaks only and panel unit root test with both sharp and smooth breaks. Step by step, we can show how the testing power increases through the use of different functions in the regression model.

First- and second-generation panel unit root tests

Before we carry out the unit root tests to check the convergence of CO2 emission per capita for the chosen countries, we first take the logarithm of the datasets. We implement the first- and second-generation panel unit root tests for comparative purposes, though their drawbacks are widely known by scholars. The first-generation panel unit root test is notorious for aggregation bias. Specifically, the first-generation panel unit root test does not take cross-sectional dependence into account in the procedure. Here, we implement three panel unit root tests, namely, Levin et al. (2002), Im et al. (2003) and Maddala and Wu (1999).

We test the unit root hypothesis for these two groups of countries. The results are presented in Table 2. The results of the panel unit root test proposed by Levin et al. (2002) show that the null is rejected for both groups at the 1% significance level (with \( {t}_{\rho}^{\ast }=-11.765 \) for 21 OECD countries and − 4.479 for the 19 emerging market countries), indicating CO2 emission per capita is stationary for both groups of countries. Next, the panel unit root test of Im et al. (2003) demonstrates that CO2 emission per capita is stationary for the 21 OECD countries if the statistics Wt _ bar, Zt _ bar and \( {\mathrm{Z}}_{t\_ bar}^{DF} \) are considered. In contrast, these statistics, Wt _ bar, Zt _ bar and \( {Z}_{t\_ bar}^{DF} \), are insignificant for the 19 emerging market countries. Finally, the panel unit root test proposed by Maddala and Wu (1999) suggests stationarity for both groups of economies.

O′ Connell (1998) points out that contemporaneous correlations among the data series will bias the results of panel unit root test towards rejecting the unit root hypothesis. Indeed, the cross-sectional dependence among the datasets is ignored in the first-generation panel unit root test. To improve the efficiency of the first-generation panel unit root test, the second-generation panel unit root tests consider the cross-sectional dependence. Here, we consider the four panel unit root tests by Bai and Ng (2004), Moon and Perron (2004), Choi (2001) and Pesaran (2004). The results are reported in Table 3.

The results of statistics \( {Z}_{\hat{e}}^C \) and \( {P}_{\hat{e}}^C \) in the second-generation panel unit root test proposed by Bai and Ng (2004) indicate that the null hypothesis cannot be rejected at any significant level, implying non-stationarity for CO2 emission per capita for both groups of countries. For the results of the panel unit root test by Moon and Perron (2004), we find that the null hypothesis is rejected at the 1% significance level. The null hypothesis of the panel unit root test of Choi (2001) is also rejected at the 1% significance level for 21 OECD countries when considering the statistics Pm, Z and L∗. Finally, the panel unit root test (CIPS and CIPS∗) proposed by Pesaran (2004) indicates that CO2 emission per capita is nonstationary for both OECD countries and emerging market economies.

Panel unit root test with structural breaks

The panel unit root test with multiple sharp breaks proposed by Carrion-i-Silvestre et al. (2005) provides insights into convergence by focusing on both the whole panel and individual countries in the group. Since the distribution of the LM statistic in Eq. 4 may not be subjected to a specific form, Monte Carlo simulations with 20,000 replications are performed to compute the critical values defined in Eq. 6. Then, the structural breaks are found by the procedure proposed by Bai and Perron (2003). The empirical findings are reported in Table 4. First, panel A summarizes the findings from the stationarity tests by using the whole panel. Both homogeneous and heterogeneous panel KPSS tests are used. Clearly, all of the statistics are smaller than the critical values at the 90% level. In other words, the null of stationarity cannot be rejected at any significance level and CO2 emission for both 21 OECD countries and 19 emerging market countries exhibits stochastic convergence. For individual countries in panel B, the null is rejected for 17 of 21 OECD countries at the 10% significance level. The null is also rejected for 15 of 19 emerging market countries. Table 5 also reports the breaking dates detected by the procedure of Bai and Perron (2003). Most of the breaking dates are located during some political, economic and financial events, such as the Gulf wars, Iraq invasion, Asian financial crisis, and 2008 global financial crisis.

Panel unit root test with both sharp and smooth breaks

Over the past several decades, the economic structure in many countries has significantly changed, which could affect CO2 emission’s path in the economies. Lee and Chang (2008) and Lee et al. (2008) have shown that structural breaks contained in the testing model would significantly relate to the testing efficiency in the field of stationarity of CO2 emission. In fact, previous studies only capture the sharp breaks contained in the CO2 emission series (Lee and Chang, 2008). The structural breaks in the series would be one of the most important features in CO2 emission per capita. However, the breaks contain not only the sharp type, but also the smooth type in most cases. Enders and Lee (2010) verify that smooth breaks in the model could be approximated by the Fourier function. In this study, we focus on not only sharp breaks, but also smooth breaks in the model based on a panel unit root test. Previous studies have not captured both sharp and smooth breaks. A better fit for the path of CO2 emission per capita, the panel unit root test with sharp and smooth breaks, is able to provide more persuasive economic implications.

Before we implement the panel unit root test with both sharp shifts and smooth breaks, we first test the cross-sectional dependence which is suggested by Pesaran (2004). Table 5 reports the empirical results through the panel unit root test with both sharp and smooth breaks. Pesaran (2004) proposes a CD statistic which could be utilized to examine the cross-sectional dependences in the data. The CD statistics (Panel A, Table 5) of 23.602 and 3.017, which are significant at the 1% level, indicate the rejection of the null hypothesis of no cross-sectional dependence of the datasets. To implement the panel unit root test with sharp and smooth breaks, the test requires the individual statistics to be cross-sectionally independent. To solve this problem, Bahmani-Oskooee et al. (2014) suggest using bootstrap techniques proposed by Maddala and Wu (1999) to obtain the empirical distribution of the panel statistics of the panel unit root test based on Carrion-i-Silvestre et al. (2005). We set the iterations to be 20,000 so as to generate the critical values of the statistics. The results are presented in Panel B, Table 5. We find that both versions of panel statistics (homogenous and heterogeneous long-run variances test) are smaller than the critical values at 90% significance level. That is, the null hypothesis of stationarity for the 21 OECD countries cannot be rejected. These results are consistent with those by Lee and Chang (2008). In other words, CO2 emissions for both groups of countries are convergent when the panel is tested as a whole.

To further investigate the stationarity of CO2 emissions among the 21 OECD and 19 emerging market countries, we implement the univariate versions of the unit root test proposed by Bahmani-Oskooee et al. (2014). The results are listed in Panel C Table 5. The critical values for the univariate version of the unit root test are calculated through 20,000 bootstrap iterations. We find that the null hypothesis of stationarity is rejected at the 10% significance level for 10 of 21 OECD countries (Australia, Belgium, Finland, Ireland, Japan, Netherlands, New Zealand, Portugal, Sweden and the UK). Thus, CO2 emissions in these countries are divergent. Policy shocks have profound impacts on CO2 emission per capita. During the period from 2013 to 2015, these OECD countries launched many economic instruments, policy supports and regulatory changes to mitigate CO2 emissions. These policies have profound impacts on CO2 emissions and change the original paths of emissions in these economies. Specifically, there are five climate change policies in force including Clean Energy Finance Corporation (CEFC); National Climate Resilience and Adaptation Strategy; National Wind Farm Commissioner and Independent Scientific Committee on Wind Turbines; Nationally Determined Contribution (NDC) to the Paris Agreement: Australia; Reef 2050 Plan.

In other words, CO2 emission per capita is convergent for the remaining 11 countries. We set the maximum sharp breaks at 7 to capture as many breaks as possible. After a grid search, we find the number of structural breaking dates is 2 breaks for Switzerland; 3 for Norway and Sweden; 4 for Canada, Italy and the Netherlands; 5 for Finland, France, Greece, Iceland and the UK; 6 for Australia, Austria, Denmark and the USA; and 7 for Belgium, Ireland, Japan, New Zealand, Portugal and Spain. Although different structural breaks are detected for individual countries, we find some common breaks in 1973, 1979, 1997, 1998, 2008 and 2009 which correspond to shocks and financial crises. Specifically, we observed structural breaks in 1973 and 1979 when oil crisis occurred. In addition, there are major financial crisis in 1998 and 2008.

The optimal frequency is determined by the F tests suggested by Bahmani-Oskooee et al. (2014) with the maximum span of 10. Obviously, the F statistics are significant, indicating choice of a satisfied nonlinear trend. We run the same procedure for the 19 emerging market countries with the same parameters used for testing the 21 OECD countries. We find that the stationary hypothesis is rejected for 9 of the 19 countries (Brazil, South Africa, Hungary, Peru, the Philippines, Poland, Thailand, the United Arab Emirates and Qatar). The number of structural breaks detected is 2 breaks for the United Arab Emirates; 4 for Hungary and Turkey; 5 for China, South Korea, Mexico, the Philippines and South Africa; 6 for Chile, Colombia, India, Indonesia, Pakistan, Poland and Thailand; and 7 for Brazil, Egypt, Peru and Qatar. Finally, the F statistic values are all larger than the critical values at the 90% level, indicating that the choice is reasonable. Similarly, we also summarize the economic instruments, policy supports and regulatory changes of these emerging economies in. The information is drawn from the Addressing Climate Change Policies and Measures Databases which is operated by International Energy Agency. In comparison with the OECD countries, the emerging economies did not actively respond to the climate change problems. Besides, as the main contributors, China and India launched two programs in 2015. In other countries like Brazil and Thailand, there are no policy instruments in force to control CO2 emissions during the period from 2013 to 2015. Thus, we can directly view a significant gap in climate change policies between OECD and emerging market economies. Although achieving fast growth is the main aim for these developing countries, governments in these economies should launch economic policies to cut CO2 emissions.

To verify the accuracy of the estimation, we plot the path of CO2 emission per capita with time-varying intercepts for 21 OECD countries in Fig. 2 and the 19 emerging market countries in Fig. 3. The raw data are plotted in the colour blue and the fitted trend with both sharp and smooth breaks is plotted in red. Clearly, the path of CO2 emission per capita contains both sharp and smooth breaks; however, the specific breaking dates and the optimal frequency to approximate the smooth breaks are unknown to us. Through this technique, we can better model the trend of the CO2 emission and the testing power would be much improved in comparison with classical univariate and panel unit root tests even if only sharp breaks are taken into consideration (Lee and Lee, 2009). A further examination of the path of CO2 emission convinces us that both dummy variables and Fourier approximations could be used to test the stochastic stationarity of CO2 emission for these countries.

CO2 emission per capita for 21 OECD countries with time-varying fitted intercepts

CO2 emission per capita for the 19 emerging market countries with time-varying fitted intercepts

According to the empirical results, CO2 emission per capita for Australia, Belgium, Finland, Ireland, Japan, the Netherlands, New Zealand, Portugal, Sweden, the UK, Brazil, South Africa, Hungary, Peru, the Philippines, Poland, Thailand, the United Arab Emirates and Qatar is not subjected to stochastic convergence. In the past several decades, the governments of Australia, New Zealand, Japan and the United Kingdom made great effort for environmental protection. The path of CO2 emissions for these countries is indeed impacted by those policies. In the meantime, CO2 emission of two oil exporters, the United Arab Emirates and Qatar. Policy makers in these countries should realize the permanent impacts of external shocks on the aggregate economy. Specifically, the environmental protection policy would permanently influence the path of CO2 emission for those countries. In contrast, for the rest of the countries in the sample, the shocks on CO2 emission would only make transitory impacts. Due to the mean-reverting properties of CO2 emission in these countries, the environmental protection policy would only make transitory impacts on the path. Although CO2 emission will return to the mean value, the soaring trend of CO2 emission in these countries cannot be neglected. Exploring clean energy to replace the fossil fuels would be the best way forward for all countries. From the perspective of the estimation, this new method provides persuasive results that CO2 emission of developing countries is more likely to diverge. Thus countries in the development process should be more alert about the pollution from CO2 emission.

Concluding remarks

This is the first paper to utilize a newly proposed panel unit root test with both sharp and smooth breaks to investigate the stochastic convergence of CO2 emission for 21 OECD countries and 19 emerging market countries. This new method provides time-varying intercepts which better model the path of CO2 emission. Both dummies and Fourier function are incorporated into the panel unit root test to approximate two different types of breaks, namely sharp and smooth breaks. Many previous studies only focus on sharp breaks, and neglect the smooth breaks in most cases, especially in studies of transitional economies. By allowing for multiple sharp breaks and a wider search range for optimal frequency, the empirical findings are more robust.

The results in this paper suggest that CO2 emission per capita is convergent when the whole panel is used for testing. However, when individual countries are tested, CO2 emission per capita is divergent for 10 of 21 OECD countries (Australia, Belgium, Finland, Ireland, Japan, Netherlands, New Zealand, Portugal, Sweden and the UK) and 9 of the 19 emerging market countries (Brazil, South Africa, Hungary, Peru, the Philippines, Poland, Thailand, United Arab Emirates and Qatar). CO2 emission reduction policies and international agreements, such as the Kyoto Protocol and Paris Agreement, would permanently affect the path of CO2 emission. However, for the rest of the countries considered in this paper, CO2 emission is convergent. Furthermore, CO2 emission in developing economies is more likely to diverge. The developing economies should pay more attention to reduce CO2 emission. Under the pressure of environmental pollution, more and more developing economies should be encouraged to sign the Kyoto Protocol and Paris Agreement. Due to the heterogeneous convergence and divergence of per capita CO2 emission in the countries, a common energy or environmental policy may not be appropriate. That is, specific environmental policies should be designed for different countries. Developing clean energy with little carbon emission such as solar, wind, nuclear and biomass energy should be encouraged in all nations. Lastly, energy policies aiming to promote the development of new technology should be further implemented. Such policies have been widely verified to be beneficial and increase the energy consumption efficiency for all countries. As Herrerias (2011) suggested, promotion for trade, foreign direct investment and indigenous investment would be beneficial to increase energy efficiency.

Although a panel unit root test with sharp and smooth breaks can effectively approximate the structural breaks contained in the series, to provide more economic implications, CO2 emission for each country should be divided into groups at different quantiles. In other words, CO2 emission per capita at different quantiles may behave differently in terms of convergence and divergence. Thus, to provide more micro insights into the pattern of CO2 emission, it is necessary to introduce quantile regression to test the convergence of CO2 emission.

Notes

As suggested by Strazicich and List (2003), the β convergence test could be obtained through the regression of annual growth rate of per capita CO2 emissions against the initial level of per capita CO2 emissions. The coefficient of the initial level of per capita CO2 emission term denotes β and if β < 0, we infer that the series is convergent. Moreover, the σ convergence denotes a decrease in the cross-sectional variation of the variable in natural log form (Panopoulou and Pantelidis, 2009).

As suggested by Cai and Menegaki (2019b), using Fourier terms can provide better approximate potential unknown smooth breaks in clean energy consumption. In this paper, we follow Cai and Menegaki (2019a) to incorporate both sharp and smooth breaks in unit root tests to examine the CO2 emission per capita.

References

Ahmed M, Khan AM, Bibi S, Zakaria M (2017) Convergence of per capita CO2 emissions across the globe: insights via wavelet analysis. Renew Sust Energ Rev 75:86–97

Aldy JE (2006) Per capita carbon dioxide emissions: convergence or divergence? Environ Resour Econ 33(4):533–555

Ang BW, Goh T (2019) Index decomposition analysis for comparing emission scenarios: applications and challenges. Energy Econ 83:74–87

Bahmani-Oskooee M, Chang T, Wu T (2014) Revisiting purchasing power parity in African countries: panel stationary test with sharp and smooth breaks. Appl Financ Econ 24(22):1429–1438

Bai J, Ng S (2004) A PANIC attack on unit roots and cointegration. Econometrica 72(4):1127–1177

Bai J, Perron P (2003) Computation and analysis of multiple structural change models. J Appl Econ 18(1):1–22

Barassi MR, Cole MA, Elliott RJ (2008) Stochastic divergence or convergence of per capita carbon dioxide emissions: re-examining the evidence. Environ Resour Econ 40(1):121–137

Barassi MR, Cole MA, Elliott RJ (2011) The stochastic convergence of CO 2 emissions: a long memory approach. Environ Resour Econ 49(3):367–385

Becker R, Enders W, Lee J (2006) A stationarity test in the presence of an unknown number of smooth breaks. J Time Ser Anal 27(3):381–409

Brock WA, Taylor MS (2010) The green Solow model. J Econ Growth 15(2):127–153

Cai Y, Menegaki AN (2019a) Convergence of clean energy consumption-panel unit root test with sharp and smooth breaks. Environ Sci Pollut Res 26(18):18790–18803

Cai Y, Menegaki AN (2019b) Fourier quantile unit root test for the integrational properties of clean energy consumption in emerging economies. Energy Econ 78:324–334

Camarero M, Picazo-Tadeo AJ, Tamarit C (2008) Is the environmental performance of industrialized countries converging? A ‘SURE’ approach to testing for convergence. Ecol Econ 66(4):653–661

Camarero M, Picazo-Tadeo AJ, Tamarit C (2013) Are the determinants of CO2 emissions converging among OECD countries? Econ Lett 118:159–162

Carrion-i-Silvestre, Lluís J, Barrio-Castro D, López-Bazo E (2005) Breaking the panels: an application to the GDP per capita. Econ J 8(2):159–175

Cheong TS, Wu Y, Wu J (2016) Evolution of carbon dioxide emissions in Chinese cities: trends and transitional dynamics. J Asia Pac Econ 21(3):357–377

Choi I (2001) Unit root tests for panel data. J Int Money Financ 20(2):249–272

Christidou M, Panagiotidis T, Sharma A (2013) On the stationarity of per capita carbon dioxide emissions over a century. Econ Model 33:918–925

Criado CO, Grether JM (2011) Convergence in per capita CO2 emissions: a robust distributional approach. Resour Energy Econ 33(3):637–665

Duro JA, Padilla E (2006) International inequalities in per capita CO2 emissions: a decomposition methodology by Kaya factors. Energy Econ 28(2):170–187

Enders W, Lee J (2012) A unit root test using a Fourier series to approximate smooth breaks. Oxf Bull Econ Stat 74(4):574–599

Ezcurra R (2007) Is there cross-country convergence in carbon dioxide emissions? Energy Policy 35(2):1363–1372

Fan Y, Gençay R (2010) Unit root tests with wavelets. Econ Theory 26(5):1305–1331

Hadri K (2000) Testing for stationarity in heterogeneous panel data. Econ J 3(2):148–161

Hatzigeorgiou E, Polatidis H, Haralambopoulos D (2008) CO2 emissions in Greece for 1990–2002: a decomposition analysis and comparison of results using the Arithmetic Mean Divisia Index and Logarithmic Mean Divisia Index techniques. Energy 33(3):492–499

Herrerias MJ (2011) CO2 weighted convergence across the EU-25 countries (1920–2007). Appl Energy 92:9–16

Im KS, Pesaran MH, Shin Y (2003) Testing for unit roots in heterogeneous panels. J Econ 115(1):53–74

Im KS, Lee J, Tieslau M (2005) Panel LM unit-root tests with level shifts. Oxf Bull Econ Stat 67(3):393–419

Jobert T, Karanfil F, Tykhonenko A (2010) Convergence of per capita carbon dioxide emissions in the EU: legend or reality? Energy Econ 32(6):1364–1373

Lee CC, Chang CP (2008) New evidence on the convergence of per capita carbon dioxide emissions from panel seemingly unrelated regressions augmented Dickey–Fuller tests. Energy 33(9):1468–1475

Lee CC, Lee JD (2009) Income and CO2 emissions: evidence from panel unit root and cointegration tests. Energy Policy 37(2):413–423

Lee CC, Chang CP, Chen PF (2008) Do CO2 emission levels converge among 21 OECD countries? New evidence from unit root structural break tests. Appl Econ Lett 15(7):551–556

Levin A, Lin CF, Chu CSJ (2002) Unit root tests in panel data: asymptotic and finite-sample properties. J Econ 108(1):1–24

Maddala GS, Wu S (1999) A comparative study of unit root tests with panel data and a new simple test. Oxf Bull Econ Stat 61(S1):631–652

Menegaki A, Tiwari AK (2019) Energy efficiency in Europe; Stochastic-Convergent and Non-Convergent Countries, chapter in Energy and Environmental Strategies in the Era of Globalization, Green Energy and Technology series, pp 305–333

Moon HR, Perron B (2004) Testing for a unit root in panels with dynamic factors. J Econ 122(1):81–126

Panopoulou E, Pantelidis T (2009) Club convergence in carbon dioxide emissions. Environ Resour Econ 44(1):47–70

Paramati SR, Ummalla M, Apergis N (2016) The effect of foreign direct investment and stock market growth on clean energy use across a panel of emerging market economies. Energy Econ 56:29–41

Pesaran MH (2004) General diagnostic tests for cross section dependence in panels. CESifo Working Paper Series No. 1229

Pettersson F, Maddison D, Acar S, Söderholm P (2014) Convergence of carbon dioxide emissions: a review of the literature. Int Rev Environ Resour Econ 7(2):141–178

Phillips PC, Sul D (2003) Dynamic panel estimation and homogeneity testing under cross section dependence. Econ J 6(1):217–259

Presno MJ, Landajo M, González PF (2018) Stochastic convergence in per capita CO2 emissions. An approach from nonlinear stationarity analysis. Energy Econ 70:563–581

Romero-Ávila D (2008) Convergence in carbon dioxide emissions among industrialised countries revisited. Energy Econ 30(5):2265–2282

Stegman A (2005) Convergence in carbon emissions per capita. CAMA Working Paper Series, 8/2005

Stegman A and McKibbin WJ (2005) Convergence and per capita carbon emissions. Brookings Discussion Papers in International Economics, No. 167

Strazicich MC, List JA (2003) Are CO 2 emission levels converging among industrial countries? Environ Resour Econ 24(3):263–271

Tiwari AK, Kyophilavong P, Albulescu CT (2016) Testing the stationarity of CO2 emissions series in Sub-Saharan African countries by incorporating nonlinearity and smooth breaks. Res Int Bus Financ 37:527–540

Ulucak R, Apergis N (2018) Does convergence really matter for the environment? An application based on club convergence and on the ecological footprint concept for the EU countries. Environ Sci Pol 80:21–27

Van PN (2005) Distribution dynamics of CO 2 emissions. Environ Resour Econ 32(4):495–508

Westerlund J, Basher SA (2008) Testing for convergence in carbon dioxide emissions using a century of panel data. Environ Resour Econ 40(1):109–120

Wu J, Wu Y, Guo X, Cheong TS (2016) Convergence of carbon dioxide emissions in Chinese cities: a continuous dynamic distribution approach. Energy Policy 91:207–219

Author information

Authors and Affiliations

Corresponding author

Additional information

Responsible editor: Philippe Garrigues

Publisher’s note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendix Climate change policies

Appendix Climate change policies

Rights and permissions

About this article

Cite this article

Cai, Y., Wu, Y. On the convergence of per capita carbon dioxide emission: a panel unit root test with sharp and smooth breaks. Environ Sci Pollut Res 26, 36658–36679 (2019). https://doi.org/10.1007/s11356-019-06786-4

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11356-019-06786-4