Abstract

The aim of this paper is to examine the causal relationship between CO2 emissions, real GDP, energy consumption, financial development, trade openness, and urbanization in Tunisia over the period of 1971–2012. The long-run relationship is investigated by the auto-regressive distributed lag (ARDL) bounds testing approach to cointegration and error correction method (ECM). The results of the analysis reveal a positive sign for the coefficient of financial development, suggesting that the financial development in Tunisia has taken place at the expense of environmental pollution. The Tunisian case also shows a positive monotonic relationship between real GDP and CO2 emissions. This means that the results do not support the validity of environmental Kuznets curve (EKC) hypothesis. In addition, the paper explores causal relationship between the variables by using Granger causality models and it concludes that financial development plays a vital role in the Tunisian economy.

Similar content being viewed by others

Explore related subjects

Discover the latest articles, news and stories from top researchers in related subjects.Avoid common mistakes on your manuscript.

Introduction

In general, the original form of environmental function related to the statement of the environmental Kuznets curve (EKC) hypothesis makes no explicit reference to the possible relationship between level of environmental degradation and income distribution. The first point of view suggested by Coondoo and Dinda (2008) indicates that the environmental damage–income relationship may be viewed as a quadratic form based on the Engel curve for environmental damage.

Although there had been an issue of the EKC studies in the last decade, a lot of researches are still needed to be discovered in the field of omitted variable bias in the relationship between emissions and income. At this level, some works such as Akhmat et al. (2014) have proved that environmental pollutants are significantly related to energy consumption, while others (e.g., Ang 2007; Apergis and Payne 2009, 2010; Lean and Smyth 2010; Arouri et al. 2012) have introduced energy into the relationship between emissions and income as a method to circumvent omitted variable bias. This method is deemed relevant in light of improving the theoretical and empirical results when the energy consumption variable is introduced to the emission–income nexus.

Furthermore, Antweiler et al. (2001), Cole and Elliott (2003), and Ang (2009) have developed the last point and added that it is possible to divide the environmental impact of trade (trade liberalization) into three effects: (i) scale (size of the economy), (ii) technique (production methods), and (iii) composition (specialization).Footnote 1 Thus, the impact of each effect on the environment may present a significant change and may also affect the economy(ies) of the selected country(ies). With respect to this methodology, Halicioglu (2009), Jalil and Mahmud (2009), Jayanthakumaran et al. (2012), and Farhani et al. (2014a) have included trade in the last relationship (i.e., emissions, income, and energy consumption) in order to reduce the problem of omitted variable bias.

Recently, Hossain (2011), Sharma (2011), and Farhani et al. (2013) have emphasized the importance of urbanization in determining the level of emissions. They have suggested that the empirical work of environmental function (i.e., emission is considered as independent “endogenous” variable) should be determined by income, energy consumption, trade, and urbanization.

On the other side, recent studies have incorporated financial development as an important factor that may significantly affect emissions (Tamazian et al. 2009; Sadorsky 2010; Tamazian and Rao 2010; Jalil and Feridun 2011; Zhang 2011; Ozturk and Acaravci 2013; Shahbaz 2013; Shahbaz et al. 2013a, b).

According to the case of Tunisia, Boulila and Trabelsi (2004) have mentioned that financial development presents a relationship with economic growth. This means that financial development may also be further introduced in the environmental function in order (i) to reduce the level of energy consumption, (ii) to control trade, and (iii) to attenuate emissions.

Since there are only a limited number of empirical evidences for the impact of financial development on the environmental performance, this paper proposes to make a contribution to the existing literature by examining the causal relationship between CO2 emissions, real GDP, energy consumption, financial development, trade openness, and urbanization in Tunisia over the period of 1971–2012. Specifically, it contributes in the existing financial development literature by three ways. First, until now, no one has emphasized the importance of this subject for Tunisia. Second, the analysis will be undertaken within an environmental model framework (EKC literature) by including measures of energy consumption, financial development, trade openness, and urbanization at the same time. Third, following the studies of Jalil and Feridun (2011), Ozturk and Acaravci (2013), Shahbaz (2013), and Shahbaz et al. (2013a, b), the sign and magnitude of the respective coefficients will be analyzed and discussed through the various hypotheses of the relationship between variables.

Empirically, we have used the relatively specific unit root tests known as the augmented Dickey–Fuller generalized least squares (ADF-GLS) of Elliot et al. (1996) and the weighted symmetric ADF (ADF-WS) of Park and Fuller (1995) to avoid the low power problem associated with conventional unit root tests, especially in small samples. The auto-regressive distributed lag (ARDL) bounds testing approach for cointegration test is used as an evidence of a long-run relationship between variables before to test the existence of long- and short-run Granger causality relationships. Additionally, we have utilized instability tests of Brown et al. (1975), which are also known as cumulative sum (CUSUM) and cumulative sum of squares (CUSUMSQ) tests based on the recursive regression residuals, to plot against the break points of the model based on strategies of Farhani (2012a) and Farhani (2014b).

The remainder of the paper is organized as follows: Literature review, Data and model specification, and Empirical results. Finally, a summary of policy implications related to the main findings is found in the Conclusion and policy implications section.

Literature review

We can divide this section into four sub-sections as follows: First, we mention that the treatment of the emission–GDP (or income) nexus is determined by the energy use, where all quantities of energy used for consumption may improve the level of income and also manage socio-economic inequalities (Ang 2007). Second, we show that the environmental damage may be affected by the associated pattern of energy consumption and trade openness (Liu 2005; Coondoo and Dinda 2008). Third, we suggest that the inclusion of urbanization in the relationship that is related CO2 emissions, GDP, energy consumption, and trade may give interesting results (Hossain 2011; Sharma 2011; Farhani et al. 2013). Finally, we propose the financial development as a new factor that can play a vital role in the EKC approach when CO2 emissions, GDP, energy consumption, trade, and urbanization are found in the same model (Jalil and Feridun 2011; Ozturk and Acaravci 2013; Shahbaz 2013).

Emissions, GDP, and energy

Pollution is strongly related to the quantities of energy consumed, since more energy consumption leads to produce not only a higher economic development but also higher pollutant gases (e.g., Ang 2007; Apergis and Payne 2009, 2010; Acaravcı and Ozturk 2010; Lean and Smyth 2010; Arouri et al. 2012).

Ang (2007) examined the causal relationships between emissions, energy consumption, and real GDP for France over the period of 1960–2000. The empirical results provided evidence for a strongly long-run relationship between these variables. In terms of causality, the findings indicated that GDP causes both energy use and emissions in the long-run, while a unidirectional causality running from energy use to GDP is detected in the short-run.

The studies of Apergis and Payne (2009, 2010) followed the work of Ang (2007) and explored the causal relationship between CO2 emissions, energy consumption, and GDP for two panel vector error-correction model (VECM): (i) six Central American countries over the period of 1971–2004 and (ii) eleven countries of the Commonwealth of Independent States over the period of 1992–2004. The finding estimates showed that real GDP exhibits the inverted U-shape pattern associated with the EKC hypothesis, and energy consumption showed a positive and statistically significant impact on emissions. In terms of causality, there are unidirectional causality from energy consumption and real GDP to emissions and bidirectional causality between energy consumption and real GDP in the short-run, while there is a strong bidirectional causality between energy consumption and emissions in the long-run.

Acaravci and Ozturk (2010) explored the causal relationship between CO2 emissions, real GDP, and energy consumption for selected European (19) countries over the period of 1960–2005. Using the ARDL bounds testing approach to cointegration, there is an evidence of a long-run relationship between variables only for Denmark, Germany, Greece, Iceland, Italy, Portugal, and Switzerland. More precisely, there is a positive long-run elasticity estimate of emissions with respect to energy consumption only for Denmark, Germany, Greece, Italy, and Portugal. In addition, there is a positive long-run elasticity estimate of carbon emissions with respect to real GDP and a negative long-run elasticity estimate of carbon emissions with respect to the square of real GDP in both Denmark and Italy. This means that the findings support the validity of EKC hypothesis only for Denmark and Italy.

In the same way, Lean and Smyth (2010) examined the causal relationship between CO2 emissions, real GDP, and electricity consumption for five ASEAN countries over the period of 1980–2006. The findings concluded a significant positive long-run elasticity estimate of emissions with respect to electricity consumption and supported the validity of EKC hypothesis. In terms of causality, the findings suggested that there is a unidirectional causality running from emissions and electricity consumption and to real GDP in the long-run and also suggested a unidirectional causality running from emissions to electricity consumption in the short-run.

By extending the works of Liu (2005), Ang (2007), Apergis and Payne (2009), and Payne (2010), Arouri et al. (2012) have recently proposed bootstrap panel unit root tests and cointegration techniques to examine the causal relationship between CO2 emissions, energy consumption, and real GDP for 12 Middle East and North African (MENA) countries over the period of 1981–2005. The findings support the results of Lean and Smyth (2010) in terms of long-run elasticity estimates of emissions with respect to electricity consumption and the validity of EKC hypothesis.

Emissions, GDP, energy, and trade

In the literature history, there are little efforts attempting to examine environmental pollution (emissions) with including the impact of trade (e.g., Ang 2009; Halicioglu 2009; Jalil and Mahmud 2009; Jayanthakumaran et al. 2012; Farhani et al. 2014a).

Ang (2009) explored the estimation of the Chinese pollution function using CO2 emissions (as endogenous variable), GDP, energy use, and trade openness (as regressors) over the annual period of 1953–2006. The findings indicated that more energy use, GDP, and trade openness lead to more CO2 emissions.

In the same way, Halicioglu (2009) have suggested the dynamic causal relationships between CO2 emissions, GDP, energy consumption, and foreign trade in Turkey over the period of 1960–2005. Using the ARDL bounds testing approach to cointegration, the findings indicated that there are two forms of long-run relationships running from GDP, energy consumption, and foreign trade to CO2 emissions as well as from CO2 emissions, energy consumption, and foreign trade to GDP. The Granger causality results suggested that the CO2 emissions are very well explained by GDP, energy consumption, and foreign trade with given more attention to the vital role of GDP in reducing emissions.

Jalil and Mahmud (2009) have extended the methodology of Halicioglu (2009) for China over the period of 1975–2005. Using a quadratic relationship between GDP and CO2 emission, the finding results support the validity of EKC hypothesis. The findings also indicated that CO2 emissions can be determined by GDP and energy consumption, while trade has insignificant impact on CO2 emissions in the long-run. In terms of causality, the results of Granger causality tests indicated one causal relationship running from GDP to CO2 emissions.

Jayanthakumaran et al. (2012) have tested the long- and short-run relationships between CO2 emissions, growth, energy use, trade, and endogenously determined structural breaks for both China and India over the period of 1971–2007. Using the ARDL bounds testing approach to cointegration, the findings indicated that CO2 emissions in China are determined by real GDP, energy consumption, and structural changes, while no causal relationship is detected for India because (i) the Indian informal economy is much larger than the Chinese case and (ii) India presents a large number of micro-enterprises that are not competitive enough to reach international markets.

Recently, Farhani et al. (2014a) have developed this literature by investigating the dynamic relationship between CO2 emissions, output (GDP), energy consumption, and trade using the bounds testing approach to cointegration and the ARDL methodology for Tunisia over the period of 1971–2008. The empirical results reveal the existence of two causal long-run relationships between the variables. In the short-run, authors prove the existence of three unidirectional Granger causality relationships, which run from GDP, squared GDP, and energy consumption to CO2 emissions.

Emissions, GDP, energy, trade, and urbanization

According to Martínez-Zarzoso and Maruotti (2011), the inclusion of urbanization in the environmental function presents an intense debate for discussion, especially in terms of environmental and regional development. There are, however, only two works (Hossain 2011; Sharma 2011; Farhani et al. 2013) that have documented the importance of the inclusion of urbanization in the relationship between CO2 emissions, economic growth, energy consumption, and trade.

Hossain (2011) have empirically examined the dynamic causal relationships between these variables for newly industrialized countries (NIC) over the period of 1971–2007. Using time series data, the findings indicated the presence of significant coefficients of CO2 emissions with respect to energy consumption in both long- and short-run. In terms of causality, the finding results showed multiple unidirectional short-run causal relationships running from GDP and trade openness to CO2 emissions, from GDP to energy consumption, from trade openness to GDP, from urbanization to GDP, and from trade openness to urbanization.

Sharma (2011) have investigated the determinants of CO2 emissions for a global panel consisting of 69 countries using a dynamic panel data model over the period of 1985–2005. The findings are that trade openness, per capita GDP, and energy consumption have positive effects on CO2 emissions. Urbanization is found to have a negative impact on CO2 emissions.

According to Farhani et al. (2013), their work is used to combine two approaches: (1) the approach of Halicioglu (2009), Jalil and Mahmud (2009), and Jayanthakumaran et al. (2012) that consists to introduce energy consumption and trade into the environmental function (CO2 emissions as endogenous variable) and [2] the approach of Hossain (2011) that discusses the role of urbanization as a method to circumvent omitted variable bias. The study of Farhani et al. (2013) parallels the two approaches for 11 MENA countries over the period of 1980–2009. The empirical results supported the validity of EKC hypothesis and showed significant impact of variables on CO2 emissions with mentioning a more attention to the role of the urbanization inclusion in the environmental function.

Emissions, GDP, energy, financial development, trade, and urbanization

The financial development factor was recently included in the environmental function through the works of Jalil and Feridun (2011), Ozturk and Acaravci (2013), and Shahbaz (2013).

The study of Jalil and Feridun (2011) discussed the impact of economic growth energy consumption, trade openness, and financial development on carbon emissions in China from 1953 to 2006. Using an ARDL bounds testing procedure, the findings showed that financial development did not present a significant impact on carbon emissions in the long-run, while economic growth, energy consumption, and trade openness presented a significant impact on carbon emissions. Moreover, their findings confirmed the EKC hypothesis.

Recently, Ozturk and Acaravci (2013) have investigated the causal relationship between carbon emissions, GDP, energy consumption, trade openness, and financial development in Turkey over the period of 1960–2007. The bounds F‐test for cointegration test yields evidence of a long-run relationship showed that an increase in trade openness leads to increase carbon emissions, while financial development had no significant effect on carbon emissions in the long-run. The findings also supported the validity of EKC hypothesis.

Finally, we mention the study of Shahbaz (2013). This study has examined the relationship between financial instability and the environmental degradation within the presence of GDP, energy consumption, and trade openness in Pakistan over the period of 1971–2009. Using ARDL bounds testing approach to cointegration and ECM to examine the long-run and short-run dynamics, respectively, the empirical findings indicated that a long-run relationship between variables can be detected as well as financial instability may increase the environmental degradation.

Data and model specification

Data

The study covers annual frequency data over the period of 1971–2012 for the case of Tunisia. The data on CO2 emissions (CO2, in metric tons per capita), real GDP per capita (GDP, in constant 2005 US$), energy consumption (EC, in kg of oil equivalent per capita), financial development indicator (FD, measured using domestic credit to private sector as share of GDP), trade openness (TO, measured using exports and imports as share of GDP), and urbanization (URB, measured using urban population as share of total population) are taken from the World Development Indicators (WDI) online database (see Fig. 1).Footnote 2

Plots in natural logarithm of per capita CO2 emissions, per capita real GDP, per capita energy consumption, financial development, trade openness, and urbanization for case of Tunisia, 1971−2012

Table 1 provides the descriptive statistics of these series for the Tunisian economy. It indicates that all series are normally distributed as shown by statistics of Jarque–Bera test. Pair-wise correlation analysis reveals that real GDP per capita, energy consumption, financial development, trade openness, and urbanization are positively associated with CO2 emissions. There is a positive correlation of energy consumption, financial development, trade openness, and urbanization, with real GDP per capita. There is also a positive correlation of financial development, trade openness, and urbanization, with energy consumption. The correlation analysis also reveals that trade openness and urbanization are positively associated with financial development. A positive correlation is also found between trade openness and urbanization.

Model specification

Until now, only the three papers of Hossain (2011), Sharma (2011), and Farhani et al. (2013) have explored the importance of urbanization in regulating the level of emissions. Suggested that emissions should be determined by income, energy consumption, trade, and urbanization, these authors have used the following model:

By taking the natural logarithm (ln) of Eq. (1), we obtain the following equation:

In order to test whether the EKC hypothesis exists when energy consumption, trade openness, and urbanization are incorporated in the environmental function, the used model can be specified as follows:

Following the original theories of Koop and Tole (2008), Tamazian et al. (2009), and Tamazian and Rao (2010), a recent empirical idea proposed by Jalil and Feridun (2011),Ozturk and Acaravci Ozturk and Acaravci (2013), and Shahbaz (2013) leads to introduce financial development in the EKC approach. The above discussion motivates us to formulate our final model as follows:

where t, β 0, and ε denote, respectively, the time, the fixed country effect, and the white noise stochastic disturbance term. In addition, β 0 = ln A, β 1, β 2, β 3, β 4, β 5, and β 6 are, respectively, the long-run elasticities of GDP, squared GDP, energy consumption, financial development, trade openness, and urbanization. As for the expected signs in Eq. (4), it is expected that the coefficients β 1 and β 2 should be, respectively, positive and negative when the EKC hypothesis is true. The sign β 3 is expected to be positive because a significant increase in energy consumption may increase economic activity and stimulate CO2 emissions (Kohler 2013; Farhani et al. 2014a). The sign β 4 is expected to be positive (Ozturk and Acaravci 2013; Shahbaz 2013; Shahbaz et al. 2013a, b), and it will be discussed with more details in the present paper. The expected sign of β 5 is mixed because it depends on the level of economic development stage of a country (Halicioglu 2009). For most developed countries, this sign is expected to be negative because these countries follow a strategy of producing a few quantities of national importing pollution intensive goods, while the basic strategy consists to import these types of goods from other countries with less restrictive environmental protection laws. Per contra, for most developing countries, this sign is reversed for the reason that they tend to produce without having tools or means of environment protection. Thus, they result dirty industries with heavy share of pollutants (Grossman and Krueger 1995; Farhani et al. 2014a). This also means that due to a dirty production under weaker environmental regulations of developing countries, a higher level in trade openness will increase pollution (Jayanthakumaran et al. 2012). Finally, the sign β 6 is suggested by Hossain (2011) and Sharma (2011) who mentioned that relatively low- and middle-income countries are less urbanized than high income countries. This means that the expected sign of urbanization is mixed depending on the level of economic development of a concerned country or a panel of countries.

Econometrical methodology

ARDL cointegration analysis

Since the developed works of Pesaran and Shin (1999) and Pesaran et al. (2001), the ARDL bounds testing approach to cointegration has become the most widely used methodology. This is due to the fact that this approach has numerous advantages compared with other cointegration methods such as Engle and Granger (1987), Johansen (1988), and Johansen and Juselius (1990) procedures: (i) no need to have the same order of integration or to have the same optimal lags for all variables in the system, (ii) no need to have large samples or absence of endogeneity between regressors to obtain an efficient estimator, and (iii) no need to have multiple equations because a single reduced-form equation may result the same findings (Ozturk and Acaravci 2010, 2013). In addition, this approach also presents some disadvantages: (i) the critical bounds provided by Pesaran et al. (2001) and Narayan (2005) will not be valid, if the order of integration for any given variables is greater than one, and (ii) it is necessary to compute on the basis that the variables are I(0) or I(1).

For this purpose, we start by testing the presence of unit root to ensure that all variables satisfy the underlying assumptions of the ARDL bounds testing approach of cointegration methodology before proceeding to the estimation stage. In order to take into account the low power problems associated with conventional unit root tests, especially with smaller sample sizes, we prefer to apply the generalized least squares ADF (ADF-GLS) test of Elliot et al. (1996) and the weighted symmetric ADF (ADF-WS) test of Park and Fuller (1995). These tests may deal with smaller sample sizes than sizes proposed by conventional unit root tests. Ozturk and Acaravci (2013) have recently noted that ADF-GLS and ADF-WS also proposed power properties compared to other tests.

Basically, the ARDL bounds testing approach to cointegration necessitates two steps for estimating long-run relationship.

The first step consists to explore the existence of long-run relationship among all variables in Eq. (4). Thus, the ARDL model will be given by

where Δ denotes the first difference term and μ t is the disturbance term assumed to have a mean value of zero and to be uncorrelated with the independent variables (i.e., regressors). In respect to the joint significance test that considered null hypothesis of no cointegration (H 0 : β i = 0; ∀ i = 8,…,14) against the alternative hypothesis (H 1 : β i ≠ 0; ∀ i = 8,…,14), it should be executed for Eq. (5). The bounds testing approach to cointegration leads to carry out the F-test on the selected ARDL models. This step is based on the selection of appropriate and optimal lag lengths suggested by different criteria such as Akaike information criterion (AIC) and Schwarz information criterion (SIC).

The second step consists to perform the general error-correction representation of the selected ARDL model of Eq. (5) as follows:

where λ is the error-correction parameter and ECT t − 1 is the lagged residuals that are obtained from the estimated long-run cointegration equation, i.e., Eq. (4). At this level, we decide to separate the lagged residuals from Eq. (6) and to define it in Eq. (7) as followsFootnote 3:

The ARDL bounds testing approach to cointegration can be proved and also complemented by Johansen–Juselius maximum likelihood methodology of Johansen and Juselius (1990). This leads to provide a sensitivity check on the results. A brief reminder of this methodology can be summarized by the following vector auto-regression (VAR) model:

where X t = (ln CO2 t , lnGDP t , lnGDP 2 t , ln EC t , ln FD t , ln TO t , lnURB t ) indicates the vector of endogenous I(1) variables, A is a vector of constant terms, Γ presents coefficient matrix, k denotes the lag length, and ξ t is the error matrix.

It is remarkable that the VAR model presented in Eq. (8) sets all its variables as endogenous. The cointegrating rank can be detected via the maximal eigenvalue and the trace statistics of the Johansen (1988) test. In addition, the lag length of the unrestricted VAR structure, i.e., k, may be obtained through the minimization of final prediction error (FPE), AIC, SIC, Hannan–Quinn (HQ) criteria, and the maximization of the likelihood ratio (LR) criterion.

Granger causality analysis

To apply Granger causality test, Pesaran et al. (2001) often used to estimate a VECM. In other terms, this approach leads to conclude short- and long-run dynamic causal relationships by applying the two steps of Engle and Granger (1987). The first step is based on the estimation of the long-run parameters existed in Eq. (4) in order to result the corresponding residuals related to the deviation from the long-run equilibrium, whereas the second step consists to estimate the parameters related to the short-run adjustment. To do this, we propose the following equation:

where ϕ j (j = 1,…,7) represents the time-invariant constant, k (k = 1,…,m) is the optimal lag length determined by the minimization of SIC, ECT t − 1 is the lagged residual obtained from the long-run relationships presented in Eq. (4) and estimated via Eq. (9), λ j (j = 1,…,7) is the adjustment coefficient, and μ j,t (j = 1,…,7) is the disturbance term assumed to be uncorrelated with zero means.

Opposite to Eq. (4), we propose to estimate all error-correction vectors in Eq. (9) by using the same lag structure (p = q = r = s = v = w = z = m).Footnote 4

Instability analysis

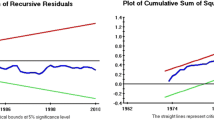

The instability tests of Brown et al. (1975) that are known as cumulative sum (CUSUM) and cumulative sum of squares (CUSUMSQ) tests based on the recursive regression residuals may be used to incorporate the short-run dynamics to the long-run dynamics through residuals. The CUSUM and CUSUMSQ statistics lead to plot and then detect break points of the model. Provided that the plots of these statistics are inside the critical bounds of 5 % significance, thus, we can conclude that the coefficients of a given regression are stable.

Empirical results

Unit root test results

The time series properties of the variables in Eq. (4) are implemented through the generalized least squares ADF (ADF-GLS) test of Elliot et al. (1996) and the weighted symmetric ADF (ADF-WS) test of Park and Fuller (1995). The results presented in Table 2 indicate that all series in Eq. (4) appear to have unit roots in their levels but stationary in their first differences. Thus, we conclude that all series are integrated at order 1, i.e., I(1), at the 5 % level of significance. At this level, we can confidently apply the ARDL methodology to Eqs. (4)–(5).

ARDL cointegration method

Given that ln CO2 t , lnGDP t , lnGDP 2 t , ln EC t , ln FD t , ln TO t , and lnURB t share common integration properties, the ARDL procedure will need to estimate Eq. (5) through two stages. In the first stage, the long-run relationship of Eq. (4) will be given by two steps. Firstly, the order of lag, that may hereafter be used to estimate VAR or VECM models, was obtained from unrestricted VAR model and by maximized likelihood ratio (LR) criterion, minimized final prediction error (FPE), Akaike information criterion (AIC), Schwarz information criterion (SIC), and Hannan–Quinn (HQ) criteria. The results of this stage lead to conserve the optimal lag which is found to be 1, except AIC (Table 3).

Using this lag, Table 4 reports the result of the Johansen maximum eigenvalue test. This test based on the works of Johansen (1988) and Reinsel and Ahn (1992) concludes that there is one cointegrated relationship at the 1 % level of significance.

Secondly, we use the minimization of AIC and SIC (the lag length is used to be 1) to obtain the order of lags (p = q = r = s = v = w = z) for Eq. (5). For both AIC and SIC, the minimization of these criteria leads to choose the same optimal lags: p = 1, q = 0, r = 0, s = 1, v = 0, w = 0, and z = 0 (Table 5).Footnote 5

In the second stage, Eq. (5) will be estimated to show the long- and short-run coefficients for Tunisia using ARDL methodology (Table 6). The results in Table 6 show the lowest value of the 1-year lag in CO2 emission coefficient by (0.2206). In addition, real GDP per capita and the square of real GDP per capita present a long- and short-run positive impact on per capita CO2 emissions. More precisely, a 1 % increase in real GDP per capita may increase CO2 emissions per capita by 3.048 % as well as a 1 % increase in the square of real GDP per capita may increase CO2 emissions per capita by 0.206 %. This concerns the short-run and also mentions that both coefficients are significant at the 10 % level.

Under the EKC hypothesis, the long-run elasticity estimates of carbon emissions per capita with respect to real GDP per capita and the square of real GDP per capita are expected to be positive (β 1 > 0 and β 2 > 0), where a 1 % increase in real GDP per capita may increase CO2 emissions per capita by 6.794 % as well as a 1 % increase in the square of real GDP per capita may increase CO2 emissions per capita by 0.366 %. In other terms, the elasticity of CO2 emissions per capita with respect to real GDP per capita in the long-run is 6.794 + 0.732Y. This means that if real GDP per capita increases, then carbon emissions per capita increase without reaching some threshold level of real GDP per capita. These results do not support the validity of EKC hypothesis in the Tunisian economy and also mean that Tunisia presents a special attention, since it shows a positive monotonic relationship between real GDP and CO2 emissions (Farhani et al. 2013).

The graphical representation (Fig. 2) of CO2 emissions per capita and real GDP per capita supports the positive monotonic relationship.

Plots in natural logarithm of EKC for per capita CO2 emissions and per capita real GDP in Tunisia, 1971–2012

The long-run elasticity estimate of carbon emissions per capita with respect to energy consumption per capita is expected to be positive (β 3 > 0). More precisely, a 1 % increase in energy consumption per capita may increase carbon emissions per capita by 2.355 % (significant at the 1 % level). The long-run elasticity estimate of carbon emissions per capita with respect to financial development is expected to be positive (β 4 > 0). In more details, a 1 % increase in financial development may increase carbon emissions per capita by 0.058 % (significant at the 5 % level). In addition, the coefficient of trade openness variable is also positive (β 5 > 0) and significant at the 10 % level. It shows that a 1 % increase in trade openness leads to increase carbon emissions per capita by about 0.418 %. Finally, the long-run elasticity estimate of carbon emissions per capita with respect to the urbanization is expected to be positive (β 6 > 0) and significant at the 1 % level. According to this result, Table 6 shows that a 1 % increase in urbanization leads to increase carbon emissions per capita by approximately 0.670.

The coefficients of estimated ECTs (italicized values in Table 6), per contra, are negative and statistically significant at 1 % confidence level. These values consist to indicate that any deviation from the long-run equilibrium between variables is corrected for each period and leads to return the long-run equilibrium level.

Following the diagnostic tests, the high value of R² for ECM-ARDL model shows that the adjustment of ARDL model was extremely good (R² = 0987 → 1). The F-statistic which measures the joint significance of all regressors in the models is statistically significant at the 1 % level. The Durbin–Watson statistic is about two; thus, we can conclude the lack of autocorrelation between residuals (prediction errors) from a regression analysis.

Granger causality test results

The present study also explores causal relationship between the variables by using error-correction models based Granger causality tests which mentioned long- and short-run Granger causality models. The results of both Granger causality models are reported in Table 7. These results can be summarized as follows: (i) In the long-run, there is an evidence of two causal relationships: [1] from real GDP per capita, energy consumption per capita, financial development, trade openness, and urbanization to CO2 emissions per capita and [2] from per CO2 emissions capita, real GDP capita, energy consumption capita, trade openness, and urbanization to financial development. At this level, policymakers have to explore the alternative energy policies, for example, decreasing energy intensity, increasing energy efficiency, and increasing the utilization of cleaner energy sources in order to reduce emissions and to improve the financial development factor. (ii) In the short-run, there is an evidence of three short-run unidirectional causal relationships: [1] from real GDP capita, energy consumption capita, and urbanization to CO2 emissions capita, [2] from CO2 emissions capita, real GDP capita, energy consumption capita, and trade openness to financial development, and [3] from CO2 emissions capita, real GDP capita, energy consumption capita, and urbanization to trade openness.

These results call for more attention in the field of environmental protection, since environmental pollution may cause financial development (in the short- and long-run) and trade openness (in the short-run). Thus, Tunisia may impose some pollution control policies such as increasing the environmental taxes (also called pollution taxes), placing restraints on activities that cause environmental degradation, and encouraging academic institutions and environmental projects that may teach how to use and apply the methods of environment protection. In other terms, our findings indicate that the implementation of energy conservation policies has not inversely affected the long-term environmental pollution of Tunisia. In the short-run, the use of more energy consumption, economic growth, and urbanization is required to pollutant emissions. This situation can be managed through more development of energy conservation strategies. We also found a positive impact of CO2 emissions per capita, real GDP per capita, energy consumption per capita, and trade openness on financial sector. Also, a positive impact of CO2 emissions per capita, real GDP per capita, energy consumption per capita, and urbanization on trade openness is detected. Therefore, the policymakers have to include financial development and trade openness factors as dependent variables to manage the level of energy demand and growth and also to mitigate emissions.

Instability test results

Hansen (1992) showed that due to misspecification of model, estimated coefficients may be different in time series data. This instability in estimates may produce prospective biasedness results that may affect the explaining power of the empirical findings. Thus, cumulative sum (CUSUM) and cumulative sum of squares (CUSUMSQ) instability tests based on recursive residuals are applied to observe the constancy of the parameters. These tests are developed by Brown et al. (1975) and mentioned that under null hypothesis, the regression coefficients are constant overtime, while under alternative hypothesis, the regression coefficients are different.

Brown et al. (1975) also argued that if the null hypothesis of parameter constancy is verified, then the recursive residuals have an expected value of zero, per contra, if the parameters present changes, then recursive residuals will not have an expected value of zero (Shahbaz 2013).

The related plots of these tests are presented in the graphs of Fig. 3 at the 5 % level of significance. From these graphs, the plots of CUSUM and CUSUMSQ statistics are strictly within the critical bounds. This means that all coefficients in the error-correction model are stable. Therefore, the selected environmental model (i.e., CO2 emission is considered as endogenous variable) can be used to understand the decision-making policy, such that the impact of instability changes in the explanatory variables’ regression coefficients of CO2 emission model will not be majorly affected by the level of CO2 emissions, since this model presents many variables, and especially if the parameters of these variables seem to follow a stable pattern during the time-estimation period (Halicioglu 2009; Shahbaz 2013; Farhani et al. 2014b).

Plots of CUSUM and CUSUMSQ of recursive residuals

Conclusion and policy implications

This paper investigates the causal relationship between CO2 emissions per capita, real GDP per capita, the square of real GDP per capita, energy consumption per capita, financial development, trade openness, and urbanization in Tunisia over the period of 1971–2012. The ARDL bounds testing approach for cointegration test yields evidence of a long-run relationship between variables. In the present study, Tunisia presents special attention, since it shows a positive monotonic relationship between CO2 emissions per capita and real GDP per capita. It means that the results do not support the validity of EKC hypothesis in the Tunisia’s economy because the level of CO2 emissions initially increases with real GDP and still increases without reaching a threshold level.

In addition, the long-run elasticity estimates of carbon emissions per capita with respect to energy consumption per capita, financial development, trade openness, and urbanization are expected to be positive. In comparison with given papers for elasticity estimate sign, our results support Jalil and Feridun (2011), Ozturk and Acaravci (2013), Shahbaz (2013), and Shahbaz et al. (2013a, b) except the sign of financial development in the study of Jalil and Feridun (2011).

Concerning long- and short-run Granger causality models, our results present the evidence of two long-run causal relationships where CO2 emissions per capita and financial development are considered as depended variables, and other three short-run unidirectional causal relationships (i) from real GDP per capita, the square of real GDP per capita, energy consumption per capita, and urbanization to CO2 emissions per capita; (ii) from CO2 emissions per capita, real GDP per capita, the square of real GDP per capita, energy consumption per capita, and trade openness to financial development; and (iii) from CO2 emissions per capita, real GDP per capita and the square of real GDP per capita, energy consumption per capita, and urbanization to trade openness.

At this level, process safety and environmental protection must be called, since CO2 emissions as a major factor of environmental pollution are strongly related to energy consumption, financial development, and urbanization.

As a policy implication, the policymakers have to explore the alternative energy policies, such as developing the energy conservation strategies, decreasing the energy intensity, increasing the energy efficiency, and increasing the utilization of cleaner energy sources. This leads to reduce emissions and to improve the financial development factor. In addition, the Tunisian government should implement effective and efficient environmental policies to sustain the economic development, to encourage the import of cleaner technologies for reducing carbon emissions, and to more target the difference between urban and rural areas especially in terms of energy consumption.

Notes

Scale effect means that the increase in the size of the economy leads to increase pollution. Technique effect means that the use of technical production methods consists to improve the environmental conditions through more competitions among the competing firms. Composition effect depends on the country’s comparative advantage (Farhani et al. 2013).

The data values of CO2 emissions for 2 years, 2011 and 2012, and of energy consumption and urbanization for 2012 are given by the World Bank estimation.

This step leads us to estimate the parameters related to the short-run model.

This method is based on the use of an unrestricted VAR model.

It is also important to mention that the presence of a diagnostic divergence in the use of these criteria often arrives in the reality. In this case, it is necessary to understand very well the objective of the study by controlling the autocorrelation of the innovations and by estimating the model that includes the minimum of lags mentioned in the parsimony principle of Raykov and Marcoulides (1999) (see Farhani 2012b; Farhani et al. 2014a).

References

Acaravcı A, Ozturk I (2010) On the relationship between energy consumption, CO2 emissions and economic growth in Europe. Energy 35:5412–5420

Akhmat G, Zaman K, Shukui T, Irfan D, Khan MM (2014) Does energy consumption contribute to environmental pollutants? Evidence from SAARC countries. Environ Sci Pollut Res 21:5940–5951

Ang JB (2007) CO2 emissions, energy consumption, and output in France. Energy Policy 35:4772–4778

Ang JB (2009) CO2 emissions, research and technology transfer in China. Ecol Econ 68:2658–2665

Antweiler W, Copeland BR, Taylor MS (2001) Is free trade good for the environment? Am Econ Rev 91:877–908

Apergis N, Payne JE (2009) CO2 emissions, energy usage, and output in Central America. Energy Policy 37:3282–3286

Apergis N, Payne JE (2010) The emissions, energy consumption, and growth nexus: evidence from the commonwealth of independent states. Energy Policy 38:650–655

Arouri MH, Ben Youssef A, M’Henni H, Rault C (2012) Energy consumption, economic growth and CO2 emissions in Middle East and North African countries. Energy Policy 45:342–349

Boulila G, Trabelsi M (2004) The causality issue in the finance and growth nexus: empirical evidence from Middle East and North African countries. Rev Middle East Econ Fin 2:123–138

Brown RL, Durbin J, Evans JM (1975) Techniques for testing the constancy of regression relationships over time. J Roy Stat Soc 37:149–192

Cole MA, Elliott RJR (2003) Determining the trade-environment composition effect: the role of capital, labor and environmental regulations. J Environ Econ Manag 46:363–383

Coondoo D, Dinda S (2008) Carbon dioxide emission and income: a temporal analysis of cross-country distributional patterns. Ecol Econ 65:375–385

Elliott G, Rothenberg TJ, Stock JH (1996) Efficient tests for an autoregressive unit root. Econometrica 64:813–836

Engle RF, Granger CWJ (1987) Co-integration and error correction: representation, estimation, and testing. Econometrica 55:251–276

Farhani S (2012a) Tests of parameters instability: theoretical study and empirical analysis on two types of models (ARMA model and market model). Int J Econ Financ Issue 2:246–266

Farhani S (2012b) Impact of oil price increases on U.S. economic growth: causality analysis and study of the weakening effects in relationship. Int J Energy Econ Policy 2:108–122

Farhani S., Shahbaz M., Arouri M., (2013) Panel analysis of CO2 emissions, GDP, energy consumption, trade openness and urbanization for MENA countries. MPRA Paper No. 49258

Farhani S, Chaibi A, Rault C (2014a) CO2 emissions, output, energy consumption, and trade in Tunisia. Econ Model 38:426–434

Farhani S, Shahbaz M, Arouri M, Teulon F (2014b) The role of natural gas consumption and trade in Tunisia’s output. Energy Policy 66:677–684

Grossman G, Krueger A (1995) Economic growth and the environment. Q J Econ 110:353–377

Halicioglu F (2009) An econometric study of CO2 emissions, energy consumption, income and foreign trade in Turkey. Energy Policy 37:1156–1164

Hansen BE (1992) Tests for parameter instability in regressions with I(1) processes. J Bus Econ Stat 10:321–335

Hossain MS (2011) Panel estimation for CO2 emissions, energy consumption, economic growth, trade openness and urbanization of newly industrialized countries. Energy Policy 39:6991–6999

Jalil A, Feridun M (2011) The impact of growth, energy and financial development on the environment in China: a cointegration analysis. Energy Econ 33:284–291

Jalil A, Mahmud SF (2009) Environment Kuznets curve for CO2 emissions: a cointegration analysis for China. Energy Policy 37:5167–5172

Jayanthakumaran K, Verma R, Liu Y (2012) CO2 emissions, energy consumption, trade and income: a comparative analysis of China and India. Energy Policy 42:450–460

Johansen S (1988) Statistical analysis of cointegrating vectors. J Econ Dyn Control 12:231–254

Johansen S, Juselius K (1990) Maximum likelihood estimation and inference on cointegration—with application to the demand for money. Oxf Bull Econ Stat 52:169–210

Kohler M (2013) CO2 emissions, energy consumption, income and foreign trade: a South African perspective. Energy Policy 63:1042–1050

Koop G, Tole L (2008) What is the environmental performance of firms overseas? An empirical investigation of the global gold mining industry. J Product Anal 30:129–143

Lean HH, Smyth R (2010) CO2 emissions, electricity consumption and output in ASEAN. Appl Energy 87:1858–1864

Liu X (2005) Explaining the relationship between CO2 emissions and national income—the role of energy consumption. Econ Lett 87:325–328

MacKinnon JG, Haug AA, Michelis L (1999) Numerical distribution functions of likelihood ratio tests for cointegration. J Appl Econ 14:563–577

Martínez-Zarzoso I, Maruotti A (2011) The impact of urbanization on CO2 emissions: evidence from developing countries. Ecol Econ 70:1344–1353

Narayan PK (2005) The saving and investment nexus for China: evidence from cointegration tests. Appl Econ 37:1979–1990

Ozturk I, Acaravci A (2010) CO2 emissions, energy consumption and economic growth in Turkey. Renew Sustain Energy Rev 14:3220–3225

Ozturk I, Acaravci A (2013) The long-run and causal analysis of energy, growth, openness and financial development on carbon emissions in Turkey. Energy Econ 36:262–267

Park HJ, Fuller WA (1995) Alternative estimators and unit root tests for the autoregressive process. J Time Ser Anal 16:415–429

Payne JE (2010) Survey of the international evidence on the causal relationship between energy consumption and growth. J Econ Stud 37:53–95

Pesaran HM, Shin Y (1999) Autoregressive distributed lag modelling approach to cointegration analysis. In: Storm S (ed) Econometrics and economic theory in the 20th century: the Ragnar Frisch centennial symposium. Cambridge University Press, Cambridge

Pesaran MH, Shin Y, Smith RJ (2001) Bounds testing approaches to the analysis of level relationships. J Appl Econ 16:289–326

Raykov T, Marcoulides GA (1999) On desirability of parsimony in structural equation model selection. Struct Equ Model 6:292–300

Reinsel GC, Ahn SK (1992) Vector autoregressive models with unit roots and reduced rank structure: estimation, likelihood ratio test, and forecasting. J Time Ser Anal 13:353–375

Sadorsky P (2010) The impact of financial development on energy consumption in emerging economies. Energy Policy 38:2528–2535

Shahbaz M (2013) Does financial instability increase environmental degradation? Fresh evidence from Pakistan. Econ Model 33:537–544

Shahbaz M, Tiwari AK, Nasir M (2013a) The effects of financial development, economic growth, coal consumption and trade openness on CO2 emissions in South Africa. Energy Policy 61:1452–1459

Shahbaz M, Hye QMA, Tiwari AK, Leitão NC (2013b) Economic growth, energy consumption, financial development, international trade and CO2 emissions in Indonesia. Renew Sustain Energy Rev 25:109–121

Sharma SS (2011) Determinants of carbon dioxide emissions: empirical evidence from 69 countries. Appl Energy 88:376–382

Tamazian A, Rao BB (2010) Do economic, financial and institutional developments matter for environmental degradation? Evidence from transitional economies. Energy Econ 32:137–145

Tamazian A, Chousa JP, Vadlamannati KC (2009) Does higher economic and financial development lead to environmental degradation: evidence from BRIC countries. Energy Policy 37:246–253

Zhang Y-J (2011) The impact of financial development on carbon emissions: an empirical analysis in China. Energy Policy 39:2197–2203

Author information

Authors and Affiliations

Corresponding author

Additional information

Responsible editor: Marcus Schulz

Rights and permissions

About this article

Cite this article

Farhani, S., Ozturk, I. Causal relationship between CO2 emissions, real GDP, energy consumption, financial development, trade openness, and urbanization in Tunisia. Environ Sci Pollut Res 22, 15663–15676 (2015). https://doi.org/10.1007/s11356-015-4767-1

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11356-015-4767-1