Abstract

Standard Phillips curve models of price inflation suggest that the United States should have experienced an episode of deflation during the Great Recession and the subsequent sluggish recovery. Although inflation reached very low levels, prices continued to rise rather than fall. More recently, many observers have argued that inflation should have increased as the unemployment rate declined and labor markets tightened, but inflation has remained below the Federal Reserve’s policy target. This paper confirms that the slope of the Phillips curve has declined over the past 50 years and is very close to zero today. The Phillips curve was modified to allow its slope to vary over time consistent with theories of price-setting behavior by firms when prices are costly to adjust and when information is costly to obtain or process. Adapting the Phillips curve to allow for time-variation in its slope helps explain the pattern of inflation, not only during and after the Great Recession, but also over the previous four decades.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

Introduction

Standard models relating price inflation to measures of slack in the economy suggest that the United States should have experienced an episode of deflation during the Great Recession of 2007–2009 and the subsequent sluggish economic recovery. Although inflation reached very low levels, prices continued to rise rather than fall. More recently, many observers have argued that inflation should have increased quickly as the unemployment rate declined and labor markets tightened, but inflation has remained persistently below the Federal Reserve’s policy target. These standard Phillips curve models, which incorporate expectations about future inflation, have in the past performed reasonably well in tracking inflation. The failure of these models during the last decade presents a troubling finding both for economists’ understanding of inflation and for policymakers’ ability to ensure steady growth and low (but positive) inflation.

These short-run models of inflation build upon the work of Friedman (1968) and relate inflation to expected inflation and slack in the economy, where slack is often measured by the gap between unemployment and its natural rate. Most versions of these models employ past inflation as a proxy for expected inflation, so that the change in inflation is determined by the gap variable. Many authors have used this accelerationist Phillips curve, e.g. Fuhrer (1995), Gordon (1982, 1990), and Staiger et al. (1997).

Recently, a number of authors have proposed modifications to the standard Phillips curve to account for the behavior of inflation during and after the Great Recession, while still maintaining a stable relationship between inflation and the unemployment gap. One type of modification, employed by Watson (2014) and Ball and Mazumder (2019), assumes that the Federal Reserve is credibly committed to a positive inflation target and that this commitment anchors expectations about future inflation. These anchored expectations cause actual inflation to exhibit greater inertia in the face of economic slack. Another type of modification uses alternative measures of slack in the economy, such as the short-term unemployment rate, rather than the overall unemployment rate. As shown by Gordon (2013) and Krueger et al. (2014), short-term unemployment moved up proportionately less during the Great Recession compared with earlier downturns and declined rapidly thereafter. Thus, a Phillips curve using short-term unemployment for its activity variable predicts less of a decline in inflation. A third type of modification, presented by Coibion and Gorodnichenko (2015), uses survey measures rather than past values of inflation as a proxy for expected inflation. Because these survey measures typically exhibit a subdued response to past inflation, they lead to more inertia in inflation. Although these modified versions of the Phillips curve based on anchoring, alternative measures of activity, and/or survey measures of expected inflation perform well in tracking inflation during recent years, they represent a significant departure from the traditional accelerationist Phillips curve.

In contrast with these approaches, Murphy (2014) considered time variation in the relationship between inflation and the unemployment gap in an otherwise standard accelerationist Phillips curve. He described how changes in regional dispersion of economic conditions influence the pricing decisions of firms, and found that the resulting time variation in the slope of the Phillips curve could account for the behavior of inflation during and immediately following the Great Recession.

This paper extends the work of Murphy (2014), assessing whether a time-varying Phillips curve model can explain inflation not only since the Great Recession but also over the previous four decades. The Phillips curve is modified to allow its slope to vary continuously through time consistent with theories of price-setting behavior when prices are costly to adjust and when information is costly to obtain or process. By adapting the Phillips curve to allow for time-variation in its slope, the behavior of inflation is explained without resorting to anchored expectations, alternative measures of slack or survey measures of expected inflation.

The paper estimates a standard accelerationist Phillips curve and documents a statistically significant weakening in the responsiveness of inflation to economic activity over the past 50 years. To account for this weakening in the response of inflation to economic activity, a version of the Phillips curve is estimated that allows the slope to vary over time, linking this variation to the inflation environment and uncertainty about regional economic conditions, as suggested by the sticky-price and sticky-information approaches to price adjustment. This modified Phillips curve best explains the path of inflation, both since the Great Recession and over earlier decades.

Phillips Curve Models of Inflation

The standard Phillips curve model expresses inflation as a linear function of expected inflation and the gap between the unemployment rate and its natural (or full-employment) value:

where π is the inflation rate, u is the unemployment rate, un is the natural rate, β < 0, and ε is an error term. In this standard formulation, the error term captures cost-push shocks that are assumed to be uncorrelated with the gap between unemployment and its natural rate. Relationships similar to Eq. (1) can be derived from microfounded models based on sticky prices or imperfect information, as shown by Calvo (1983), Lucas (1973), Mankiw and Reis (2002), and Roberts (1995).Footnote 1

A common approach to estimating Eq. (1) uses several lags of past inflation as a proxy for expected inflation, e.g., Gordon (1982) and Stock and Watson (2008). This study adopts this approach, using four lags, and assuming that the coefficients are equal in magnitude and sum to one:

This specification of the Phillips curve captures the accelerationist feature emphasized by Friedman (1968) whereby a reduction in unemployment below its natural rate leads to a long-run increase in the rate of inflation.Footnote 2 This formulation implies that a sustained increase in actual inflation will take one year to be fully incorporated into expected inflation.Footnote 3 Estimation of Eq. (2) also requires a measure of the natural rate of unemployment. As in many previous studies, estimates of the natural rate are produced by the Congressional Budget Office (2017).

Equation (2) is estimated over various sample periods, beginning in 1960. Table 1 presents estimates using quarterly data for inflation measured by the price index for personal consumption expenditures (PCE).Footnote 4 Estimates are reported for both total inflation and inflation less food and energy prices (denoted “core”), with Newey-West standard errors in parentheses.Footnote 5 In all cases, the coefficient on the unemployment gap variable is of the correct sign (negative), is statistically different from zero at high levels of confidence, and the restriction that the coefficients on lagged inflation sum to one cannot be rejected.

Comparing results for the time periods shown in the top panel of Table 1, it is apparent that the sensitivity of inflation to slack in the economy is much lower when the post 2007 data are included in the sample than when they are not, with the coefficient dropping by about two standard errors for both overall and core inflation. The hypothesis that the coefficient is equal across these two samples can be rejected at the 1% level.

The bottom panel of Table 1 shows results for time periods ending in 1990 and in 2000. The point estimates of the coefficient on the unemployment gap are larger for these samples compared with the sample ending in 2007. The hypothesis that the coefficients are equal can be rejected at the 5% level of significance, except for total PCE when the time period ends in 2000, where it can be rejected only at the 10% level. Also, the hypothesis that the coefficients are equal to those obtained when the time period ends in 2016 can be overwhelmingly rejected. This suggests that Eq. (2) is not stable across the full sample period of 1960–2016.

A possible explanation for the failure of standard Phillips curve models to explain the recent behavior of inflation is that its slope varies through time and has become much flatter in recent years. Figure 1 shows estimates of the slope parameter β from Eq. (2) using rolling regressions with 10-year windows over the period 1960–2016, centering estimates at the mid-point of each window.Footnote 6 The slope parameter is negative and roughly constant for most of the 1960s, declines and then rises during the 1970s, plateaus in the 1980s and first half of the 1990s, and then trends upward through the late 1990s, approaching zero over the last 15 years. This pattern is similar to the time variation in Phillips curve coefficients estimated using time-series techniques in Stock and Watson (2010a) and Ball and Mazumder (2011).

Accounting for Variation in the Phillips Curve’s Slope

This section considers two explanations for why the Phillips curve’s slope may vary through time. One explanation assumes prices are costly to adjust and so firms find it optimal to hold prices constant for some period of time. According to this sticky-price model of price setting, when the level of inflation is low, firms adjust prices less frequently because low inflation means that fixed prices deviate only gradually from their optimal values. Similarly, when uncertainty about overall inflation or market demand conditions is low, the risk that a firm’s fixed price will deviate suddenly from its optimal value also is low, so firms adjust less frequently because they are less concerned that fixed prices will be quickly out of line. Since prices are updated less frequently, inflation will exhibit less responsiveness to shifts in economic slack and the Phillips curve’s slope coefficient will be smaller in absolute value.Footnote 7

A second explanation assumes that firms face costs of acquiring or processing information but are free to adjust prices. Firms set a path for prices and adjust this path only after updating their information about market demand conditions.Footnote 8 According to this sticky-information model of price setting, when uncertainty about market conditions is low, firms will update their information less frequently, leading to less responsiveness of inflation to shifts in economic slack and a smaller absolute value for the Phillips curve’s slope.Footnote 9

Because uncertainty about overall inflation affects the benefit of updating information in addition to the benefit of adjusting prices, inflation variability will influence pricing decisions of sticky-information firms as well as sticky-price firms. But unlike the sticky-price model, the sticky-information model predicts that the average level of inflation has no effect on the sensitivity of prices to aggregate demand. The reason for this is that price paths set by firms fully incorporate the average level of inflation and so inflation has no effect on the frequency of information updates.

To capture uncertainty about market conditions, a measure of dispersion in economic activity across the United States was approximated by the standard deviation of growth in state personal income relative to growth in national personal income. The growth rates are measured as the percent change over the same quarter a year ago. The standard deviation is calculated for each quarter using data for all 50 states. This regional dispersion variable reflects the degree to which economic conditions across the country are different, and so should proxy for the incentive of firms to update information about market conditions in different regions. When firms update their information more (less) frequently, inflation will be more (less) responsive to aggregate economic conditions and the slope of the Phillips curve will be larger (smaller) in absolute value.

To investigate whether changes in the inflation environment and/or the regional dispersion of economic conditions affect the sensitivity of inflation to the unemployment gap, Eq. (2) is modified to allow the slope coefficient to vary over time with these measures.Footnote 10 Specifically, versions of the following equation are estimated:

where \( {\overline{\pi}}_t \) and \( {\sigma}_t^{\pi } \) are four-quarter moving averages of the mean and standard deviation of inflation, and \( {\sigma}_t^y \) is the four-quarter moving average of the standard deviation of quarterly state personal income growth around national personal income growth. Personal income data are from the U.S. Bureau of Economic Analysis (2017b). The interaction terms capture time variation in the slope coefficient.Footnote 11

Table 2 reports estimates of several versions of Eq. (3). Columns labeled A show specifications with inflation interaction terms, \( {\overline{\pi}}_t \) and \( {\sigma}_t^{\pi } \), and columns labeled B and C show estimates for specifications that include the regional dispersion term, \( {\sigma}_t^y \), either alone or in combination with the inflation terms. For the period 1960–2007, as seen in column A, the coefficients on the inflation environment terms (β1 and β2) are not statistically significant either individually or jointly, and the coefficient on the inflation variance term (β2) has an incorrect (positive) sign. For the period 1960–2016, the coefficients are jointly significant, although the coefficient on the inflation variance term again has an incorrect (positive) sign. A high degree of collinearity between \( {\overline{\pi}}_t \) and \( {\sigma}_t^{\pi } \) makes the individual effects hard to distinguish. When the mean of inflation, \( {\overline{\pi}}_t \), is entered alone, its coefficient (β1) is statistically significant and of the correct sign.Footnote 12 These results provide some weak support for the sticky-price model’s prediction that the average level of inflation affects the slope of the Phillips curve, although the positive coefficient on the inflation variance term is at odds with the model’s prediction.

When the dispersion term either alone or in combination with the inflation environment terms (columns B and C) is included, its coefficient (β3) is always statistically significant and of the correct sign for both sample periods. But the inflation environment terms are never statistically significant either individually or jointly, and the coefficient on the inflation variance term again has an incorrect (positive) sign. When only the mean of inflation with the regional dispersion term is included, the coefficient on the mean of inflation is not statistically significant and has an incorrect (positive) sign. The coefficient on the dispersion term always has the correct (negative) sign, is statistically significant, and is stable across specifications.Footnote 13

The results in Table 2 suggest that variation over time in the slope of the Phillips curve is more closely related to regional dispersion of income growth than to characteristics of inflation. As mentioned above, the average level of inflation should affect the slope of the Phillips curve in the sticky-price model but not the sticky-information model. Because the interaction term for the mean of inflation is not statistically significant when combined with the regional dispersion term, and assuming that uncertainty about regional economic conditions is appropriately captured by the regional dispersion of income growth, these results provide some support for the sticky-information model of price setting.

Table 3 presents root mean square error (RMSE) and \( {\overline{\mathrm{R}}}^2 \) statistics to evaluate the performance of Eq. (3) over several earlier subsamples. These statistics are provided for versions where the slope varies with the inflation environment or regional dispersion of income growth. For all sample periods, the RMSE statistic is smaller and the \( {\overline{\mathrm{R}}}^2 \) statistic is larger when the regional dispersion term is included in the regression. These results are consistent with those presented for the longer sample periods used in Table 2, and support the conclusion that accounting for time variation in the Phillips curve helps improve its performance during earlier periods.

As a check on the structural stability of Eq. (3), the top panel of Fig. 2 presents results of a Quandt likelihood ratio (QLR) test for the version in which the slope varies with the regional dispersion term.Footnote 14 We cannot reject the hypothesis of no structural break. But for the version of Eq. (3) where the slope varies with mean inflation, the QLR test in the bottom panel of Fig. 2 finds evidence of a structural break.Footnote 15

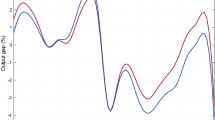

Figure 3 shows in-sample one-step-ahead predictions of inflation starting in 1961 using parameters estimated over the full 1960 to 2016 sample. Results are presented for the model that allows the slope to vary with the regional dispersion term and for the model with a constant slope. The task here is to observe whether the modified Phillips curve can accurately track inflation in decades prior to the Great Recession.

As seen in Fig. 3, the model with the regional dispersion term matches inflation closely over the late 1970s, 1980s, and 1990s, similar to the model with a constant slope. But for recent years, the model with the regional dispersion term performs better than the model with a constant slope. This in-sample simulation confirms that a traditional Phillips curve modified to allow its slope to vary with the regional dispersion of economic activity tracks inflation reasonably well over the past 50 years.

Summary

This paper has explored the ability of a standard Phillips curve to explain the pattern of U.S. inflation. A reduced sensitivity of inflation to economic activity over the past several decades was documented and the failure of the traditional constant-slope specification to predict inflation accurately during and after the Great Recession was illustrated. Although modifications of the Phillips curve based on anchoring and/or alternative measures of activity perform reasonably well in explaining inflation for recent years, they represent a significant break from the traditional Phillips curve.

This paper instead shows that directly accounting for time variation in the slope of an otherwise traditional Phillips curve can help explain the behavior of inflation. The sticky-price and sticky-information approaches to price adjustment together imply that the level and variability of inflation and uncertainty about market conditions should influence the slope of the Phillips curve. The Phillips curve is modified to include these effects and finds that uncertainty about market conditions, as captured by the regional dispersion of economic activity, explains time-variation in the slope. This modified Phillips curve is consistent with the behavior of inflation not only since the Great Recession but also over the prior four decades.

The results of this paper suggest that central bankers should consider additional factors such as the regional dispersion of economic activity when setting monetary policy. In particular, assessing the degree to which market conditions vary or are similar across regions is an important consideration for determining how responsive inflation will be to changes in unemployment brought about by policy adjustments. Hence, monetary policy should be calibrated to account for the regional dispersion of economic activity in order to avoid overshooting (or undershooting) target inflation when responding to changes in overall economic activity.

Notes

By contrast, the New Keynesian Phillips curve predicts that inflation is expected to decline when unemployment falls below its natural rate as Roberts (1995) illustrated, an implication rejected by historical data.

Mankiw et al. (2004) found that survey measures of expected inflation were not consistent with either rational expectations or adaptive expectations of the type used here. The traditional approach to estimating Phillips curve models was followed in maintaining that expected inflation depends on lagged values of actual inflation. For analysis that uses survey measures, see Coibion and Gorodnichenko (2015).

All estimates in this paper use data available as of July 2017. The focus is on inflation measured using the PCE price index rather than the CPI because the PCE price index encompasses a broader array of consumer purchases and is the measure that the Federal Reserve emphasizes in its policy discussions. PCE data are from the U.S. Bureau of Economic Analysis (2017a) and unemployment data are from the U.S. Bureau of Labor Statistics (2017).

Results use core PCE inflation here and throughout the remainder of the paper.

See Ball et al. (1988) on the sticky-price model’s implications for the slope of the Phillips curve.

Reis (2006) showed how greater uncertainty about a firm’s market conditions reduced the time between information updates, thereby increasing the responsiveness of prices and inflation to aggregate demand.

The advantage of this approach compared with advanced time-series methodologies is that it links the variation in the slope coefficient directly to movement in variables suggested by economic theory and avoids having to specify in advance a stochastic process for how the slope coefficient evolves through time.

This specification of the Phillips curve permits the slope coefficient to vary over time with the inflation environment and uncertainty about regional economic conditions. The equation is not intended to provide a formal test of the sticky-information or the sticky-price theories, but only to motivate why the slope might vary over time.

When the inflation variance term is entered alone (not shown), its coefficient is not statistically significant.

When the inflation variance term with the regional dispersion term (not shown) is included and the mean inflation term omitted, its coefficient is never statistically significant, while the dispersion term is negative and significant.

An F-statistic is computed for a Chow test of the null hypothesis of no structural break at each observation over the interior 70% of the sample and then the maximum value is chosen as the test statistic. Confidence levels for the QLR statistic shown in Figure 2 are from Stock and Watson (2010b), Table 14.6.

QLR tests for sample periods ending earlier than 2016 (not shown) also find no evidence of a structural break when the slope varies with the regional dispersion term. But for versions of equation (3) where the slope varies with the mean or variance of inflation (not shown), QLR tests always show strong evidence of a structural break.

References

Ball, L., & Mazumder, S. (2011). Inflation dynamics and the great recession. Brookings Papers on Economic Activity, Spring 2011 (pp. 337–381).

Ball, L., & Mazumder, S. (2019). A Phillips curve with anchored expectations and short-term unemployment. Journal of Money Credit and Banking, 51(1).

Ball, L., Mankiw, N., & Romer, D. (1988). The new Keynsesian economics and the output-inflation trade-off. Brookings Papers on Economic Activity, 1988(1), 1–82.

Calvo, G. (1983). Staggered prices in a utility maximizing framework. Journal of Monetary Economics, 12, 383–398.

Coibion, O., & Gorodnichenko, Y. (2015). Is the Phillips curve alive and well after all? Inflation expectations and the missing disinflation. American Economic Journal: Macroeconomics, 7(1), 197–232.

Congressional Budget Office (2017). An update to the budget and economic outlook: 2017 to 2027, June 2017, Washington, DC. Available at: https://www.cbo.gov/publication/52801 (accessed July 25, 2017).

Friedman, M. (1968). The role of monetary policy. American Economic Review, 58, 1–17.

Fuhrer, J. (1995). The Phillips curve is alive and well. New England Economic Review, March/April, 41–56.

Gordon, R. (1982). Inflation, Flexible Exchange Rates, and the Natural Rate of Unemployment. In Workers, Jobs, and Inflation, ed. by M. Baily, Washington, DC: The Brookings Institution Press, 89–158.

Gordon, R. (1990). U.S. inflation, Labor’s share, and the natural rate of unemployment. In Economics of wage determination, ed. by H. Koenig, Berlin: Springer-Verlag, 1–34.

Gordon, R. (2013). The Phillips curve is alive and well: Inflation and the NAIRU during the slow recovery. NBER Working Paper #19390. Available at: (http://www.nber.org/papers/w19390).

Krueger, A, J. Cramer, and D. Cho (2014). Are the long-term unemployed on the margins of the labor market? Brookings Papers on Economic Activity, Spring 2014, 229–280.

Lucas, R. (1973). Some international evidence on output-inflation tradeoffs. American Economic Review, 63, 326–334.

Mankiw, N., & Reis, R. (2002). Sticky information versus sticky Price: A proposal to replace the new Keynesian Phillips curve. Quarterly Journal of Economics, 117, 1295–1328.

Mankiw, N., & Reis, R. (2007). Sticky information in general equilibrium. Journal of the European Economic Association, 2, 603–613.

Mankiw, N. and R. Reis (2010). Chapter 5 - Imperfect Information and Aggregate Supply. In Handbook of Monetary Economics, ed. by B. Friedman and M. Woodford, Elsevier, Volume 3, 183–229.

Mankiw, N., Reis, R., & Wolfers, J. (2004). Disagreement about inflation expectations. NBER Macroeconomics Annual, 18, 209–248.

Mazumder, S. (2010). The new Keynesian Phillips curve and the cyclicality of marginal cost. Journal of Macroeconomics, 32, 747–765.

Mazumder, S. (2011). Cost-based Phillips curve forecasts of inflation. Journal of Macroeconomics, 33, 553–567.

Murphy, R. (2014). Explaining inflation in the aftermath of the great recession. Journal of Macroeconomics, 40, 228–244.

Reis, R. (2006). Inattentive producers. Review of Economic Studies, 73, 793–821.

Roberts, J. (1995). New Keynesian economics and the Phillips curve. Journal of Money, Credit, and Banking, 27, 975–984.

Staiger, D., Stock, J., & Watson, M. (1997). How precise are estimates of the natural rate of unemployment? In b. C. Romer & D. Romer (Eds.), Reducing Inflation: Motivation and Strategy, National Bureau of economic research studies in business cycles (pp. 195–246). Chicago, IL: University of Chicago Press.

Stock, J. and M. Watson (2008). Phillips curve inflation forecasts. Federal Reserve Bank of Boston, Conference Series; [Proceedings], volume 53. Available at: https://www.fedinprint.org/series/fedbcp.html.

Stock, J. and M. Watson (2010a). Modeling Inflation After the Crisis. Proceedings - Economic Policy Symposium - Jackson Hole, Federal Reserve Bank of Kansas City, 173–220. Available at https://www.kansascityfed.org/publicat/sympos/2010/Stock-Watson_final.pdf.

Stock, J. and M. Watson (2010b). Introduction to Econometrics, Prentice Hall.

U.S. Bureau of Economic Analysis (2017a). National Income and Product Accounts, Table 2.3.4. Price Indexes for Personal Consumption Expenditures by Major Type of Product. Available at: https://www.bea.gov/data/gdp/gross-domestic-product (accessed July 25, 2017).

U.S. Bureau of Economic Analysis (2017b). Regional Data, Table SQ1 Personal Income Summary. Available at: https://www.bea.gov/data/income-saving/personal-income-by-state (accessed July 25, 2017).

U.S. Bureau of Labor Statistics (2017). Current population survey, table A-1 employment status of the civilian noninstitutional population. Available at: https://www.bls.gov/cps/ (accessed July 25, 2017).

Watson, M. (2014). Inflation persistence, the NAIRU, and the great recession. American Economic Review, 104(5), 31–36.

Acknowledgements

An earlier version of this paper was presented at the Western Economic Association International 93rd Annual Conference, June 26-30, 2018, Vancouver, British Columbia. I thank the editor and referee for their comments and Giridaran Subramaniam for expert research assistance. This research was supported in part by a Boston College Research Incentive Grant.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher’s Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

About this article

Cite this article

Murphy, R.G. Can the Phillips Curve Explain Inflation over the Past Half-Century?. Int Adv Econ Res 25, 137–149 (2019). https://doi.org/10.1007/s11294-019-09730-x

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11294-019-09730-x