Abstract

This paper provides empirical evidence on the relationship between residential property prices and the business cycle for seven advanced Organisation for Economic Co-operation and Development economies over the period 2002–2015 using quarterly data. To this end, panel data and time series methodologies are adopted as a means of providing a contextual framework on the extant relationship. The panel methodological framework explores the interaction between economic fundamentals and financial variables while the use of time series methodologies developed by Phillips et al. (2011 and 2015) provide novel evidence on the detection of property price bubbles that have been manifested in each individual country of the sample. In particular, the short-run dynamic panel framework provides a robust exploratory platform thus, shedding light on the determinants of property prices (i.e. real gross domestic product, bank credit growth, long-term bond yields and real effective exchange rate) whilst the bubble detection methodologies provide evidence of the impact of credit-driven economies on the propagation of housing booms which can serve as warning signals of the potential formation of housing bubbles.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

Introduction

Activity in the residential property market has been regarded as a potential indicator of economic performance. At the same time, the fact that housing booms and busts have been detrimental to both financial stability and real economic activity has strengthened the perception that irrational exuberance, as much as fundamentals to a great extent, explains housing price fluctuations (Shiller 2009; Mikhed and Zemčík 2009; Jordà et al. 2016).

Over the course of past decades, emerging evidence points towards a significant relationship between key macroeconomic indicators and fluctuations in the property market. Leamer (2007, 2015) provides evidence that residential investment has a larger impact on output than any other sector and is by far the best leading indicator of economic activity. By virtue of its prominence as the best early warning sign of an imminent recession, the housing market assumes a prominent role in the conduct of monetary policy. According to Leung (2004) the significant cyclical movements and volatility observed in the housing market are closely related to macroeconomic movements in the business cycles.

On the empirical front, various studies have been conducted in an attempt to shed additional light on the inherent relationship between macroeconomic indicators and housing price fluctuations. In this context, both cross-country and country-specific studies have generated strong evidence of dynamic interactions between housing prices and bank lending (Davis and Zhu 2011; Goodhart and Hofmann 2008). Recently, a growing interest in the detection of bubbles in the housing market has spawned new empirical as well as theoretical research on the validity and further development of the current methodological approaches. (see for instance Yiu et al. 2013; Caspi 2016; Engsted et al. 2016; Bourassa et al. 2016).

Motivated by Mayer’s (2011) suggestion that without firm evidence about what causes bubbles, it is hard to develop policy, in this study, we initially explore the housing–business cycle relationship by looking at the determinants of residential property prices for a small panel of seven advanced Organization for Economic Coordination and Development (OECD) economies (Australia, Belgium, Canada, Denmark, Great Britain, Norway and Sweden). In our study the impact of the real effective exchange rate appears to be playing an instrumental role in determining housing price fluctuations in so far as a potential depreciation or devaluation affects competitiveness which in turn galvanizes demand in the housing market. Given the relatively under-researched area, the yielding evidence presented in this study contributes further to the literature on housing prices and exchange rates in the context of advanced economies.

A salient feature of the data on housing prices is the presence of booms and busts (Burnside et al. 2011) that may be driven by fundamentals, but can be compounded by market expectations or speculation (Agnello and Schuknecht 2011). For this reason, subsequently, we engage in the detection of potential property price bubbles that have been present in the respective property markets of the sample countries by utilizing times series methodologies. Recent reports indicate that in the sample countries housing prices have increased steadily after a brief correction during the Great Recession stressing the fears of housing bubbles fuelled by record-low real interest rates and foreign demand from safe haven seekers (Financial Times 2015; International Monetary Fund [IMF] 2014). In our study, we employ the recently developed recursive procedures developed by Phillips et al. (2011) and Phillips et al. (2015) to identify and date residential housing price bubbles. These procedures have proved to be useful as warning signals in surveillance strategies developed by central banks with real-time data (Phillips et al. 2015). We depart from the studies of Engsted et al. (2016) and Caspi (2016) by applying the bubble detection tests in the residential real housing price index and the ratio of credit to gross domestic product (GDP). This is because the prospect of capital gains appears to remain a key driver for investors even in the face of declining rental yields. The declining affordability of housing and increasing investor presence have seen a downward trend in the share of households owning their own home in a number of OECD countries. For this reason, we consider the application of bubble detection tests to the housing index for each country as more relevant.

Literature Review

The interlinkages between housing prices, credit and real economic activity are well documented in both the theoretical and the empirical literature. Equally, a number of studies focused on financial instability risks inherent in the growing housing market imbalances. Especially, housing price busts can severely hurt economies. Analysing housing prices in 14 countries during 1970–2001, IMF (2003) identified 20 examples of busts, when real prices fell by almost 30% on average, which led to a recession to all countries except one. America was the only country to avoid the boom and bust during that period. Subsequently, we focus on cross-country studies that analyse the determinants of housing prices.

In a sample of 15 countries, Adams and Füss (2010) find that housing prices tend to increase in the long-run by 0.6% in response to a 1% increase in economic activity while the long-term interest rate shows average long-term effects of approximately 0.6% and −0.3%, respectively. The evidence suggests that property price busts, even though found to be less frequent than equity price busts, were twice as large in duration hence, resulting in significant output losses (Helbing and Terrones 2003). At the same time, the time to full recovery or long-term equilibrium may take up to 14 years, suggesting a slow adjustment process between macroeconomic variables on international housing prices (Adams and Füss 2010).

Using a reduced-form theoretical model which relates bank lending to property prices, Davis and Zhu (2011) find that macroeconomic shocks (GDP, interest rates) cause changes in property prices and bank lending, in a sample of 17 developed economies. Goodhart and Hofmann (2008) provide evidence of a significant multidirectional link between housing prices, credit and the macro-economy while the effects of shocks to money and credit are found to be stronger when housing prices are booming. In a panel of 49 U.S. states over the period 1975–2003, Holly et al. (2010) document a cointegrating relationship between housing prices and real incomes and identify a small role for real interest rates. In a study of 14 OECD countries, Hott and Jokipii (2012) find that short-term interest rates that are set too low for too long have a significant impact on the creation of housing bubbles.

Recently, the literature has been enriched by studies that investigate the rapidly growing economies of the Asian region. More specifically, Jianhua and Huidian’s (2013) evidence for the Chinese economy points towards a significant but nevertheless weak long-term equilibrium relationship as well as a bidirectional causality between the macroeconomic factors and the property markets. Additional evidence for the Turkish economy indicates that housing prices are affected by innovations in CPI whereas the role of wages is insignificant (Ucal and Gőkkent 2009). Beltratti and Morana (2010) find a bidirectional linkage between real housing prices and macroeconomic developments are an important source of global fluctuations for real housing prices in the G-7 area.

Punzi (2016) finds that the correlations between real GDP per capita and real housing prices and between lending and real housing prices have increased over time, more evidently if we compare periods of the Great Recession with the Great Depression. In line with Igan et al. (2011), Punzi (2016) finds that asset prices tend to lead real activity. Igan et al. (2011) provide evidence that housing price cycles lead credit and real activity in the long run, while in the short- to medium-run the relationship varies across countries. In contrast, Cerutti et al. (2015) find that the presence of a household-credit boom increases the probability of a real-estate boom to 57% from an unconditional probability of 29%, suggesting that household-credit booms are better predictors of housing-price booms than private credit booms. But as Burnside et al. (2011) point out, it remains difficult to find observable fundamentals that are correlated with price movements. In studying booms and busts in housing prices for 18 industrialised countries over the period 1980–2007, Agnello and Schuknecht (2011) found that domestic credit and interest rates had a significant influence on the probability of booms and busts. Moreover, global liquidity plays a significant role for the occurrence of housing booms and in conjunction with banking crises for busts. Potentially, global liquidity shocks affect housing prices, consumption, and the current account in emerging economies much more than fully blown market economies (Bianchi et al. 2015). The impact of real exchange rates is also envisaged to have global liquidity and balance sheet effects (Bruno and Shin 2015; Cespedes et al. 2004; Cespedes et al. 2012; Gabaix and Maggiori 2014). Furthermore, in general equilibrium models where the interaction of housing and macroeconomic factors are explored, apart from the collateral constraints that amplify the response of consumption and investment to business cycle shocks, shocks are thought to also affect the value of collateral and in turn determine the borrowing capacity of households and firms (Iacoviello 2005; Monacelli 2009; Liu et al. 2013). Sá et al. (2014), in a study exploring the impact of capital inflows, monetary policy and financial innovation find that both capital inflows and monetary policy shocks have a significant and positive effect on real housing prices, real credit to the private sector and residential investment. Thereby, the presence of a financial accelerator mechanism is more pronounced in economies where the housing market is more developed and where securitization is more prevalent. Against this backdrop, households can make available a larger fraction of their house as collateral, hence, making them more vulnerable to changes in the value of collateral.

Generally, empirical studies indicate that housing markets are influenced by the business cycle. In this setup, Martin et al. (2007) claim that both real and financial variables interact in the boom-bust phases of asset prices. Typically, the macroeconomy is proxied by fundamentals such as unemployment rate, inflation, industrial production and real GDP while financial variables are proxied by monetary conditions (interest rates, money-credit supply). Evidently, the interaction of the real exchange rates and housing prices merits further empirical research.

Data and Panel Methodology

The choice of the countries in this study is determined by the fact that a) real housing prices have increased by more than 50% in 2000–2015 (150% in the period 1985–2015) and b) the supply of housing, especially in the big cities of these countries is highly inelastic. The latter may not hold for Denmark which has been included in the sample because it has one of the highest household-debt ratios in the world, reflecting little incentive to pay off the debt and build house equity (IMF 2015). In determining whether houses in the sample countries are fairly valued, we also looked at the ratios of housing prices against rents or housing prices against average income where a similar trajectory has been observed. In both cases, the ratios moved higher compared to their historical averages, thus indicating an overvaluation. Lastly, the choice of the sample was driven by the fact that these economies are considered to be ‘stable and secure’ environments by foreign investors according to surveys by the Association of Foreign Investors in Real Estate. A dominant feature of the housing market resurgence, recently, has been an increase in investor activity. The inherent homogeneity of these economies is arguably a valid reason why they might be experiencing a cyclical synchronization of housing price fluctuations (Hirata et al. 2013).

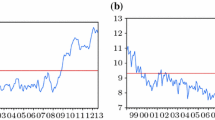

In this context, we formulate and estimate a model for seven advanced OECD economies; Australia, Belgium,Footnote 1 Canada, Denmark, Great Britain, Norway and Sweden by using quarterly data spanning the period 2002q4-2015q2. In particular, the dataset consists of N cross sectional units, denoted i = 1,…, N observed at T time periods, denoted t = 1,…,T. More specifically, y is a (TN × 1) vector of endogenous variables, x is a (TN × k) matrix of exogenous variables, which does not include a column of units for the constant term. In this context, we collated data for a cross section of seven OECD economies (N = 7) over a period of 51 quarters (T = 51). Table 1 provides the definitions of variables and data sources. The online supplemental Appendix table presents the data summary statistics and Fig. 1 the plots of the residential property price index for the sample countries.

Plot of the residential property price index for the sample countries. Source: Bank of International Settlements (2002-2015)

The empirical specification of the housing price regression is a variant of the standard specifications encountered in the literature (for instance Drake 1993; Glindro et al. 2011, Alexiou et al. 2014). Given the dynamic dimension of our model, we opted for the generalised method of moments (GMM) introduced by Holtz-Eakin et al. (1988) and further developed by Arellano and Bond (1991) and Arellano and Bover (1995). The GMM methodological framework is known to be very effective when dealing with estimation issues such as: bi-directional causality between variables; the possible endogeneity of explanatory variables, as well as omitted variable biases; time invariant country characteristics (fixed effects), that may be correlated with the explanatory variables; and the presence of autocorrelation (Anderson and Hsiao 1981; Caselli et al. 1996; Bond 2002). In addition to the two-step system GMM, we also generate estimates using the standard ordinary least squares (OLS) and fixed effects (or within) specifications.

We estimate the following regression specification:

where HP is the residential real price index; GDP is the real GDP growth that has been used as a proxy to measure the state of the business cycle and household income; CR can be either bank credit to private sector (BCR) expressed as a percentage of GDP or credit to households (HCR), and expected to positively affect demand for property thus exerting an upward pressure on property prices; RER is the real effective exchange rate which following an depreciation or depreciation is expected to negatively or negatively affect property market prices, particularly in markets where there is substantial demand from non-residents for investment purposes, UN stands for unemployment rate; and LTBY is the long-term bond yield, a proxy for long-term rates. This is a one-way error component regression model, where v i ~ IIN (0, σ2) and independent of e it ~ IIN (0, σ2).

We apply the model specification in the first differences (growth rates) of the variables. The evidence from the panel unit root testsFootnote 2 indicates that almost all variables were I(1). The focal point of the analysis that will follow pertains to the GMM-SYS specification, the generated evidence of which yields more reliable estimates. It is worth noting that whenever there is considerable difference between the FE and the GMM estimates (mostly in terms of the significance of the coefficients), the Hausman test is applied to determine which model is the most consistent one. The robustness of our estimated coefficient for the GMM-SYS specification is confirmed by the AR(2) and Sargan tests on the basis of which the null hypothesis of no serial correlation and instrument validity could not be rejected. As a robustness test for the validity of the chosen independent variables, we also employed the ratio of credit to the household sector and the real interest rates as prolonged periods of low real rates tend to be associated with property hikes. As a robustness test for the results yielded by the GMM-SYS specification, we applied the two stage least squares (TSLS) framework and obtained relatively consistent estimators. Also, the results remained robust in the presence of alternative proxies for credit (i.e. credit to households) and interest rates (i.e. money market rates).

Results and Discussion of the Panel Framework

The results reported in Table 2 suggest that credit expansion is strongly associated with property price hikes, hence supporting the evidence of a strong housing price-credit nexus. In this context, the use of real estate as a means of collateral might act as a conduit through which housing price movements feed back into the credit market which in turn drives property prices (Davis and Zhu 2011). The real economic growth (GDP) and the proxy used for the competitiveness of the economy (RER) are found to positively affect housing prices. While the linkage between economic growth and housing prices is well-documented in the literature (Cerutti et al. 2015; Martin et al. 2007), the respective significant effect of RER in the case of developed economies constitutes a novel aspect in the time period of our study which captures both booms and busts for almost all countries in the sample. An appreciating RER might be the result of strong inflows of foreign capital in the advanced economies of our sample countries where investment in housing properties is perceived to be a ‘safe haven’ in periods of uncertainty. Still, an appreciating RER which signals a loss in competitiveness could well indicate risks of housing busts or at least, can help explain the occurrence of boom and busts (Martin et al. 2007).

We also find that in the short-run, housing price-inflation is sensitive to the long-term government bond yield which is aligned with the evidence provided by Tsatsaronis and Zhu (2004) and Hirata et al. (2013). In an economic environment with unprecedented low interest rates, households’ appetite for housing loans increases to a point where irrational behaviour is likely to set in. The implication of the latter is of great significance for household mortgage repayment as a potential future increase in the interest rates or a housing price collapse may destabilize the financial sector. In general, low rates are perceived as a source of risk as they drive lending and risk-taking. Our results suggest that increasing long-term bond yields negatively affect housing prices in the sample countries. In the same spirit, Hott and Jokipii (2012) find that low interest rates drive housing prices higher while a number of studies document that an increase in domestic credit growth increases the probability of a housing boom. The effect of unemployment, although insignificant, is positive which is puzzling. This could be attributed to the time period of our study which encompasses both booms and busts for the sample countries implying possible sign switches (Agnello and Schuknecht 2011).

Generally speaking, there is no widely accepted definition as to what constitutes housing or credit booms and busts. These episodes are generally defined as large and persistent deviations of these variables from some historical norm (Cerutti et al. 2015), or sharp increases in prices followed by collapsing ones (Lind 2009). Strictly speaking, the term bubble may insinuate a predominant role of non-fundamentals which is not always the case for booms. In the following section, use both terms interchangeably.

Detection of Housing Price Bubbles

Property booms can be partly explained by fundamentals as bubble-like symptoms abound in the sample countries. This is because, the property bubble tends to replace a stock market bubble but also because of behavioural factors, such as the deeply ingrained perception that property is by far the safest and most rewarding investment one can make in their lifetime. Still, housing prices are just as prone to irrational exuberance as the stock markets.

In detecting residential price bubbles, we employ three tests: a rolling window ADF test and the more recent tests developed by Phillips et al. (2011, hereafter PWY or SADF test) and Phillips et al. (2015, hereafter PSY or GSADF test) which constitute a supplemental augmented ADF test based on a sequence of forward recursive right-tailed ADF tests (PWY) and a more generalised version of it, which allows for flexible window widths in the recursive regressions on which the test procedure is based (PSY). Especially, the PSY test utilises a recursive flexible window method that is better suited for practical implementation with time series delivering a consistent real-time stamping strategy for the origination and termination of multiple bubbles. In all three tests, the null hypothesis of a unit root is applied and the alternative hypothesis is of a mildly explosive process (Phillips and Magdalinos 2007).

In developing these tests, we utilise longer time-series (individually for each country) compared to the panel framework, thanks to the data availability in the database of the Bank of International Settlements (BIS). Phillips et al. (2015) suggest that the use of these methods over long historical periods presents a serious econometric challenge due to the complexity of the nonlinear structure and break mechanisms that are inherent in multiple-bubble phenomena within the same sample period. Equally, Hamilton (1986) suggests that the interpretation of tests for speculative price bubbles depends on the nature of any non-stationarity in the fundamentals. Thus, rejection of the ‘no-bubble’ null that implies the acceptance of the presence of a bubble is only possible within the specified model.

Notably, the tests were successful in identifying episodes of exuberance without necessary leading to collapses in the sample countries. Overall, the results presented in Table 3 and the respective plots of the PSY tests as shown in the supplementary appendix, broadly confirm existing empirical evidence (Helbing and Terrones 2003; Goodhart and Hofmann 2008; Agnello and Schuknecht 2011; Engsted et al. 2016) as well as anecdotal information such as real estate surveys or other market reports. For instance, the results for Canada, Great Britain, Norway and Sweden (countries where longer time series were available), are in line with Helbing and Terrones (2003). The same applies for the results for Canada, Norway and Great Britain which are broadly in line with Agnello and Schuknecht (2011).

Equally, Denmark’s results are in consensus with Dam et al. (2011) suggesting that the country has experienced a housing price cycle with a run-up in housing prices in 2005–2007. Dam et al. (2011) refer to a Danish housing bubble that begun to unfold in 2006–2007 and contributed strongly to the overheating of the economy.

In the case of Belgium, the hypothesis of a mildly explosive process (housing bubble) cannot be accepted in all three tests performed, which is in line with IMF (2014) and Agnello and Schuknecht (2011) but in contrast to Engsted et al. (2016). A second observation from the results is that housing prices in the sample countries moved largely in tandem during 2000–2015.

More importantly, the bust (bubble-bursting) occurred at around the same time in these countries. Firstly, housing prices increased significantly prior to the global financial crisis and then, with the exception of Great Britain, housing prices collapsed over the period 2006–2008, and in 2014–2015 started to rebound in most of the countries in the sample. The finding of the synchronized fluctuations in the sample housing markets is in line with Hirata et al. (2013) suggesting co-movement of housing prices in the developed world as a result of a high degree of integration over the past two decades, and ultimately synchronized business cycles. Certainly, housing booms have different characteristics across (even within) countries and time periods. However, our tests reveal that most of the sample countries move in sync especially in the aftermath of the Global Financial Crisis. Noteworthy, a number of countries (Australia, Canada, Denmark and Sweden) are spotted as candidates for potential housing market “exuberance” in 2015. At the same time, central banks in a number of countries in our sample that present bubble-risk in 2014–2015 maintained interest rates at ultra-low levels. Certainly, the tests applied in this paper serve merely as primary indicators of potential formation of housing bubbles that need to be co-estimated with other economic fundamentals and demand-supply factors. As Burnside et al. (2011) assert, not all booms in housing prices are followed by busts and the interpretation of booms and busts in housing markets requires a considerable degree of judgement, hence a subjective element as well as the stylised facts in the countries under analysis.

As a robustness test, we applied where feasible the bubble detection tests in a shorter time period, such as the one utilised in the panel data framework (2002–2015). The results seem to be moderately influenced by the length of time series. However, especially, in the case of PSY (2015) the results were robust to the choice of the minimal window size and the lag length.

According to Jordà et al. (2016) housing bubbles are fueled by credit booms. Similarly, Davis and Zhu (2011) find strong links of credit to property prices in countries that experienced property-linked crises pointing to a positive long-run effect of credit on prices which is suggestive of possible bubbles. For this reason, we apply in the ratio of bank credit to GDP (bcr) the same bubble detection tests we applied in the residential real price index. Preliminary results suggest that credit booms broadly coincide with housing bubbles in most of the sample countries. Future work will enable us to ascertain whether credit booms can help predict housing price booms or the potential direction of the causality between bank credit to the private sector and housing prices.

Conclusions

Housing is a key sector in any economy but also a source of financial crises and vulnerabilities in the banking sector. For this reason, property price fluctuations and detection of housing price bubbles have been a focal point of contemporary macroeconomic research. The results generated in this study have important implications as they provide further insights into the understanding of the dynamics of housing prices as well as in the detection of deviations from fundamentals thresholds. Residential property prices and credit creation, long-term bond yields and the real effective exchange rate are intertwined. Therefore, it is important to include housing prices when studying business cycles. Housing bubbles are broadly synchronized with excessive credit creation, coinciding or even leading the business cycle. In this respect, the bubble detection techniques can provide an early warning signal of an “overheating” housing market that can assist regulators in the countries under analysis. Yet, country-specific demand and supply factors need to be accounted for in the study of housing cycles. For instance, it could be that housing demand from foreign inflows could bypass domestic credit. In this context, any design of macroprudential tools by central banks should be calibrated and adjusted according to the pace of economic growth and credit creation whilst taking into account the role of real effective exchange rates.

Notes

After the collective pre-crisis boom, European housing markets followed two paths. Denmark, Greece, Ireland, Portugal and Spain dropped sharply. Others including Belgium, Great Britain, Norway and Sweden only dipped before rebounding with worrying speed.

For economy of space the panel unit root tests are not reported in this paper but are available upon request.

References

Adams, Z., & Füss, R. (2010). Macroeconomic determinants of international housing markets. Journal of Housing Economics, 19(1), 38–50.

Agnello, L., & Schuknecht, L. (2011). Booms and busts in housing markets: determinants and implications. Journal of Housing Economics, 20, 171–190.

Alexiou, C., Karanikolas, N., & Xifylidou, A. (2014). Determinants of construction activity: Cointegration evidence from the Greek real estate market. The Empirical Economics Letters, 13(6), 675–685.

Anderson, T., & Hsiao, C. (1981). Estimation of dynamic models with error components. Journal of the American Statistical Association, 76(375), 598–606.

Arellano, M., & Bond, S. (1991). Some tests of specification for panel data: Monte Carlo evidence and an application to employment equations. The Review of Economic Studies, 58(2), 277–297.

Arellano, M., & Bover, O. (1995). Another look at instrumental variable estimation of error component models. Journal of Econometrics, 68(1), 29–51.

Bank of International Settlements (2002-2015). About BIS statistics, http://www.bis.org/statistics/index.htm. Accessed 3/3/16.

Beltratti, A., & Morana, C. (2010). International house prices and macroeconomic fluctuations. Journal of Housing Economics, 34(3), 533–545.

Bianchi, A., Cespedes, L.F. and Rebucci, A. (2015). Global liquidity, house prices, and the macroeconomy: evidence from advanced and emerging economies. IMF Working Paper 15/23.

Bond, S. (2002). Dynamic panel data models: a guide to micro data methods and practice. Portuguese Economic Journal, 1(2), 141–162.

Bourassa, S., Hoesli, M., & Oikarinen, E. (2016). Measuring house price bubbles. Journal of Real Estate Economics. doi:10.1111/1540-6229.12154.111.

Bruno, V., & Shin, H. S. (2015). Cross-border banking and global liquidity. Review of Economic Studies, 82, 535–564.

Burnside, C., Eichenbaum, M. and Rebelo, S. (2011). Understanding booms and busts in housing markets. NBER Working Paper 16734.

Caselli, F., Esquivel, G., & Lefort, F. (1996). Reopening the convergence debate: a new look at cross-country growth empirics. Journal of Economic Growth, 1(3), 363–389.

Caspi, I. (2016). Testing for a housing bubble at the national and regional level: the case of Israel. Empirical Economics, 51(2), 483–516.

Cerutti, E., Dagher, J., & Dell'Ariccia, G. (2015). Housing Finance and Real-Estate Booms: A Cross-Country Perspective. IMF Discussion Note, 15/12.

Cespedes, L. F., Chang, R., & Velasco, A. (2004). Balance sheets and exchange rate policy. American Economic Review, 94(4), 1183–1193.

Cespedes, L.F., Chang, R. and Velasco, A. (2012). Financial intermediation, exchange rates, and unconventional policy in an open economy. NBER Working Paper, 18431.

Dam, N.A., Hvolbøl, T.S., Pedersen, E.H., Sørensen, P.B. and Thamsborg, S.H. (2011). The housing bubble that burst: can house prices be explained? and can their fluctuations be dampened. Danmarks Nationalbank, Monetary Review 1st Quarter, 2011.

Davis, P., & Zhu, H. (2011). Bank lending and commercial property cycles: some cross-country evidence. Journal of International Money and Finance, 30(1), 1–21.

Drake, L. (1993). Modelling UK house prices using Cointegration: an application of the Johansen technique. Applied Economics, 25(9), 1225–1228.

Engsted, T., Hviid, S. J., & Pedersen, T. (2016). Explosive bubbles in house prices? Evidence from the OECD countries. Journal of International Financial Markets, Institutions and Money, 40, 14–25.

Financial Times. (2015). Scandinavian housing bubbles spark financial stability fears. August, 2, 2015.

Gabaix, X., and Maggiori, M. (2014). International liquidity and exchange rate dynamics. NBER Working Paper 19854.

Glindro, E., Subhanij, T., Szeto, J., & Zhu, H. (2011). Determinants of house prices in nine Asia-Pacific economies. International Journal of Central Banking, 7(3), 163–204.

Goodhart, C., & Hofmann, B. (2008). House prices, money, credit, and the macroeconomy. Oxford Review of Economic Policy, 24(1), 180–205.

Hamilton, J. D. (1986). On testing for self-fulfilling speculative price bubbles. International Economic Review, 27(3), 545–552.

Helbing, T. and Terrones, M. (2003). When Bubbles Burst. IMF, World Economic Outlook, April 2003.

Hirata, H., Kose, A.M., Otrok, C. and Terrones, M.E. (2013). Global house price fluctuations: synchronization and determinants. IMF Working Paper, 38.

Holly, S., Pesaran, H., & Yamagata, T. (2010). A spatio-temporal model of house prices in the USA. Journal of Econometrics, 158(1), 160–173.

Holtz-Eakin, D., Newey, W., & Rosen, H. S. (1988). Estimating vector Autoregressions with panel data. Econometrica: Journal of the Econometric Society, 56, 1371–1395.

Hott, C. and Jokipii, T. (2012). Housing bubbles and interest rates. Swiss National Bank, Working Paper, 2012–7.

Iacoviello, M. (2005). House prices, borrowing constraints, and monetary policy in the business cycle. American Economic Review, 95(3), 739–764.

Igan, D., Kabundi, A., De Simone, F. N., Pinheiro, M., & Tamirisa, N. (2011). Housing, credit, and real activity cycles: characteristics and comovement. Journal of Housing Economics, 20(3), 210–231.

International Monetary Fund (2003). World economic outlook, April 2003.

International Monetary Fund (2014). Seven questions on the global housing markets. IMF Research Bulletin, September 2014.

International Monetary Fund (2015). Housing recoveries: cluster report on Denmark, Ireland, the Netherlands, and Spain. Multi-country report, 15/1.

Jianhua, G., & Huidian, L. (2013). Investigation of the linkage among China’s macroeconomy, stock market and real estate market. International Journal of Finance & Banking Studies, 2(2), 1–7.

Jordà, Ò., Schularick, M., & Taylor, A. M. (2016). The great mortgaging: housing finance, crises, and business cycles. Economic Policy, 31(85), 107–152.

Leamer, E.E. (2007). Housing is the business cycle. NBER Working Paper No. 13428.

Leamer, E. E. (2015). Housing really is the business cycle: what survives the lessons of 2008-09? Journal of Money. Credit and Banking, 47(S1), 43–50.

Leung, C. (2004). Macroeconomics and housing: a review of the literature. Journal of Housing Economics, 13, 249–267.

Lind, H. (2009). Price bubbles in housing markets: concept, theory and indicators. International Journal of Housing Markets and Analysis, 2(1), 78–90.

Liu, Z., Wang, P., & Zha, T. (2013). Land and price dynamics and macroeconomic fluctuations. Econometrica, 81(3), 1147–1184.

Martin, R., Schuknecht, L. and Vansteenkiste, I. (2007). The role of the exchange rate for adjustment in boom and bust episodes. ECB Working Paper 813.

Mayer, C. (2011). Housing bubbles: a survey. Annual Review of Economics, 3, 559–577.

Mikhed, V., & Zemčík, P. (2009). Do house prices reflect fundamentals? Aggregate and panel data evidence. Journal of Housing Economics, 18(2), 140–149.

Monacelli, T. (2009). New Keynesian models, durable goods, and collateral constraints. Journal of Monetary Economics, 56(2), 242–254.

Phillips, P., & Magdalinos, T. (2007). Limit theory for moderate deviations from a unit root. Journal of Econometrics, 136(1), 115–130.

Phillips, P., Wu, Y., & Yu, J. (2011). Explosive behaviour in the 1990s NASDAQ: when did exuberance escalate asset values? International Economic Review, 52(1), 201–226.

Phillips, P., Shi, S., & Yu, J. (2015). Testing for multiple bubbles: historical episodes of exuberance and collapse in the S&P 500. International Economic Review, 56(4), 1043–1077.

Punzi, M.T. (2016). Financial cycles and co-movements between the real economy, finance and asset price dynamics in large-scale crises. FinMaP-Working Paper, No. 61. Collaborative EU Project FinMaP, Financial Distortions and Macroeconomic Performance.

Sá, F., Towbin, P., & Wieladek, T. (2014). Capital inflows, financial structure and housing booms. Journal of the European Economic Association, 12(2), 522–546.

Shiller, R. (2009). Irrational Exuberance. New York: Broadway Books, 2nd ed.

Tsatsaronis, K. and Zhu, H. (2004). What drives housing price dynamics: cross country evidence. BIS Quarterly Review, March 2004.

Ucal, M., & Gőkkent, G. (2009). Macroeconomic factors affecting real Estate Markets in Turkey: a VAR analysis approach. Briefing Notes in Economics, 80, 1–13.

Yiu, M. S., Yu, J., & Jin, L. (2013). Detecting bubbles in Hong Kong residential property market. Journal of Asian Economics, 28, 115–124.

Acknowledgements

We wish to thank Professor Henry Pollakowski for providing valuable recommendations and insight in an earlier version of this paper and Itamar Caspi for providing the routines for the bubble detection tests.

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Vogiazas, S., Alexiou, C. Determinants of Housing Prices and Bubble Detection: Evidence from Seven Advanced Economies. Atl Econ J 45, 119–131 (2017). https://doi.org/10.1007/s11293-017-9531-0

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11293-017-9531-0