Abstract

Many advanced economies have experienced significant job polarization in the last decades, with an increase in the employment share and relative wage of both low-wage and high-wage workers at the expense of middle-wage workers. This polarization has probably been spurred by the substitution of routine-intensive labour with automation and information and communication technologies. This paper explores whether the Italian labour market has experienced similar patterns and, if so, whether they are the consequence of a pure technology-driven shock. The evidence is mixed. While the share of low-wage manual occupations has increased markedly, that of high-wage professional occupations has fallen slightly. The share of middle-wage jobs has declined significantly but, unlike the case of the US, the wages have not. Regression analyses based on occupational task characteristics (Goos et al. in Am Econ Rev 104(8): 2509–2526, 2014) do not fully align with the routine-biased technical change hypothesis either, consistently with the limited adoption of automation technology in Italy. Among the most likely factors, cross-sector reallocation, which favoured the low value added service sector, and the rise of low skilled migrant and college graduate labour supply explain most of the observed occupational changes.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

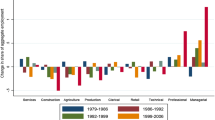

The 2017 OECD Employment Outlook (OECD 2017) analyzes the evolution of the occupational structure in Europe in the period 1995–2015 and shows that the most industrialized economies’ labour market became increasingly polarized. The OECD observes an increase in the share of low-pay (e.g., manual services) and high-pay occupations (e.g., managerial and professional positions), and a drop of middle-pay occupations as share of total employment (Fig. 1). These latter tend to intensively perform tasks that “can be accomplished by following explicit rules”, i.e., routine-intensive tasks (Autor et al. 2003), and usually employ middle-skilled workers (e.g., white collar, secretarial, archival and cashier occupations). Automating and information and communication technologies (ICT), which substitutes for routine-intensive labour and complement manual-intensive (through demand) and analytical-intensive (through production complementarities), are considered the main determinant of job polarization (Autor et al. 2003, 2006; Autor and Dorn 2013; Goos et al. 2014; Cirillo 2016; OECD 2017). Such hypothesis goes under the name of routine-biased technical change (RBTC). Alternative hypotheses hinge on the demand growth for goods produced by industries which employ workers at the two extremes of the skill distribution (Comin et al. 2018), and on secular declines of the manufacturing sector (Bárány and Siegel 2018).

Percentage point change in share of total employment, 1995–2015; selected countries from OECD (2017). Source: OECD Employment Outlook (2017), Fig. 3.A1.1 (selected countries). OECD calculations based on the European Labour Force Survey, Canada, Japan, and Switzerland labour force surveys and the United States CPS MORG. Notes: According to the OECD Employment Outlook (2017), high-paying (and high-skill) occupations include jobs classified under the ISCO-88 major groups 1, 2, and 3. That is, legislators, senior officials, and managers (group 1), professionals (group 2), and technicians and associate professionals (group 3). Middle-paying (middle-skill) occupations include jobs classified under the ISCO-88 major groups 4, 7, and 8. That is, clerks (group 4), craft and related trades workers (group 7), and plant and machine operators and assemblers (group 8). Low-paying (low-skill) occupations include jobs classified under the ISCO-88 major groups 5 and 9. That is, service workers and shop and market sales workers (group 5), and elementary occupations (group 9). As agricultural, fishery and mining industries were not included in the analysis, those occupations within ISCO-88 group 6 (agricultural and fisheries workers) were likewise excluded

The OECD analysis leaves, however, many unanswered questions: do low- and high-end polarization occurs simultaneously in the two decades analyzed, as the RBTC hypothesis would suggest? Is polarization the consequence of a pure demand shock or workers and industrial composition matter too?Footnote 1 In addition, what is the role of occupational classification, task indexes and wage-based rankings in shaping the results given the differential technological adoption and institutional features (e.g., wage bargaining) across countries?

This paper aims at answering these questions in the context of the Italian labour market and describes the most evolution of its occupational structure since the onset of the Great Recession.Footnote 2 The existing literature points to an upgrading of the Italian occupational structure in the 1990s until the mid-2000s (Goos et al. 2009; Fernandez-Macias 2012; Olivieri 2012). The empirical evidence presented herein, which is novel for Italy, indicates that a strong growth in the share of low-skilled manual occupations and a mild drop in the share of high-pay professional occupations have characterized the last 10 years. The share of middle-pay occupational decreased sharply. Regression analyses based on occupational task characteristics, similar to those run by Goos et al. (2014), do not confirm that RBTC is the main driver of the Italian occupational structure, at least in the most recent period. Other factors, such as changes in the composition of the workforce and the growth of low value added services, are uncovered by means of simple Oaxaca–Blinder decompositions. In this sense, the paper contributes to the international literature by providing a more complete set of empirical analyses that uncover different channels that together may shape the occupational distribution. In fact, existing papers often take a stand on a specific channel (such as, for instance, RBTC and ITC diffusion) and neglect others (such as, for instance, structural transformation and the shrinking of the manufacturing sector or the role of labour supply forces). This paper shows that is important to test empirically for all possible explanations: changes in the composition of the workforce and the growth of low value added services seem to have contributed significantly to occupational changes in the Italian case.

Finally, the paper combines analyses on the employment margin with a thorough analysis of occupational wage dynamics that also account for compositional changes. Studying together quantities and prices is important to try to disentangle demand from supply determinants, although most of the existing literature mainly focuses on employment only. In this regard, as an ancillary result, I highlight how the characteristics of the Italian occupations, especially their wages and the relationship with the task contents, are not fully comparable with those of their European counterparts. In this sense, the paper warns about the use of off-the-shelf task measures in contexts where technology adoption and institutional factors (mainly wage setting) differ.

The paper proceeds as follows. Section 2 summarizes the existing evidence on job polarization in Italy. Section 3 describes the data used and the classification of occupations. Section 4 presents descriptive evidence on the change of the Italian occupational structure in the last decade and discusses some possible determinants. Section 5 concludes.

2 Changes of the Occupational Structure in Italy Over Two Decades: Existing Evidence

As reported in Fig. 1, the OECD shows that the Italian labour market polarized as much as the OECD average and in line with those of Germany and the US. This evidence confirms a recent analysis by Goos et al. (2014). Goos and coauthors show that between 1993 and 2010 the decline in middle-pay occupational share in Italy was large (− 10.6 percentage points). At the polar ends, the share of the eight highest paying occupations increased by 4.5 percentage points, that of low-pay occupations by 6.1 percentage points. Overall, job polarization in Italy fostered the specialization of low-skilled service jobs such as construction and transport labourers, personal service workers and other sales and service elementary positions much more than in other advanced economies. It is worth noting that their employment share was already high in 1993, at 27% versus a European average of 21.6 (Goos et al. 2014).

A previous contribution by Goos et al. (2009) analyzes data until 2006. Interestingly, they find a shift towards high-skilled occupations in Italy, rather than an increase of both low and high-skilled occupational shares (Fernandez-Macias (2012) finds similar patterns). This result is consistent with work by Olivieri (2012) and Olivieri and Nellas (2012) who show that Italy experienced substantial occupational upgrading in the 1990s and 2000s. The share of hours worked in high-qualification occupations, defined as occupations with the highest educational requirement (rather than the highest paying ones), increased while the share of hours in low-qualified positions dropped between 1993 and 2000 and slightly increased until the late 2000s (see Figs. 4.1 and 4.2 in Olivieri 2012).

The existing evidence thus points to some interesting, but puzzling, facts. The Italian labour market polarized in the last two decades, but the dynamics differs substantially if we look at the two sub-periods separately. The occupations whose share increased the most before mid-2000s were highly qualified and paying higher wages. Low skilled occupations grew only in the more recent period, thus not contemporaneously to highly qualified occupations, as the demand channel of the RBTC theory would suggest (Autor and Dorn 2013). The share of the middle-pay occupations, instead, declined substantially throughout the last 25 years.

Given the conflicting results in terms of occupational evolution across decades, it is not clear whether routine-biased technical change can be considered the only driver for such changes. Moreover, the lack of evidence on occupational wage growth, which under a demand shock follows the same direction of the changes in occupational shares, cannot fully exclude the possibility that changes in supply also drive part of the results. Rosolia (2010) and Olivieri (2012) are the only papers that look at the evolution of wages: they observe a strong wage growth at the polar ends of the wage distribution between 1985 and 2004 using administrative data from INPS. However, they cannot link such wage changes to employment changes at the occupation level because of data limitations.Footnote 3

The rest of the paper focuses on the last decade trying to study in depth the changes in the occupational structure that occurred from just before the Great Recession until the most recent recovery possibly shedding some light on the puzzle. Moreover, I investigate and discuss possible causes of the recent shift towards low skilled jobs, whether due to structural transformation in production processes (for instance, related to globalization) or to changes in labor supply. However, pinning down the exact determinant of such a profound structural change goes beyond the scope of this paper.

3 Data on Occupations and Tasks

3.1 The Italian Labour Force Survey

I use ISTAT Labour Force Survey (LFS) microdata from 2007 to 2017. The universe of reference is the workforce aged 15–64 in the non-agricultural private sector that I collapse into at occupation-industry-year cells. I aggregate industries into five broad categories: manufacturing, energy and mining, construction, retail and wholesale trade, accommodation and food services, other services (health services and education are not included in the analysis as mostly comprised of public sector jobs). Such coarse aggregation is due to structural breaks in the sectoral classification in 2011. I compute the number of employed people in each cell, the share over total employment, as well as the average wage, which is available from Istat only starting in 2009.Footnote 4 In further analyses I also use information on workforce age (above and below 35), gender, nativity status (natives and foreign born) and education (high school or less, some college or more).

3.2 Classifying Occupations

In the absence of detailed technology adoption measures, the literature analyzes job polarization as the changes in occupational employment shares leveraging on different occupational characteristics in order to quantify the impact of routine task-substituting machines on labour demand.

The publicly availably LFS microdata report 130 three-digit occupations that span the entire spectrum of workers’ activities and can be aggregated into one or two-digit occupation groups.Footnote 5 The classification adopted as of 2017, Classificazione delle Professioni 2011 (CP2011), presents a break in 2011 with respect to the previous classification in use since 2001 (CP2001). To overcome the limitations imposed by the change of classification, and to match the Italian occupations to ILO’s International Standard Classification of Occupations (ISCO) classification-based indexes that describe their characteristics, I follow a two-step matching procedure. First, I associate post-2011 LFS three-digit codes to pre-2011 three-digit codes. Then, I similarly match the three-digit pre-2011 to two-digit ISCO-88 occupational codes. Such adjustments do not create an error-free classification of occupations over time, but allow reducing the breaks in the series as shown in panel (a) and (b) of Fig. 2.Footnote 6 Moreover, I provide additional analysis limiting the sample to the period 2011–2017 to test the robustness to the 2011 break. Despite the change of the base year, the results are qualitatively similar (“Appendix B”).

Trends in employment shares and employment growth by broad occupation group, 2007–2017. Notes: Author’s elaboration on Istat Labour Force Survey microdata; private employment excluding agriculture, health services and education. The high-pay/skill group is composed of 1, 2 and 3 one-digit ISCO-88 occupations (managers, professionals, technicians and associate professionals, excluding group 11 “Legislators and senior officials”). The middle-pay/skill group is composed of 4, 7 and 8 one-digit ISCO-88 occupations (clerks, craft and related trades workers, and plant and machine operators and assemblers). The low-pay/skill group is composed of 5 and 9 one-digit ISCO-88 occupations (service workers and shop and market sales workers, and elementary occupations). Occupation groups 11 “Legislators and senior officials”, 23 “Teaching professionals”, 33 “Teaching associate professionals”, 6 “Skilled agricultural and fishery workers” and 92 “Agricultural, fishery and related labourers” are not included in the sample

In the rest of the analyses, I use different groupings of occupations. First, occupations can be ranked by their mean wage following a canonical model of the labour market with three types of labour (low, middle and high skilled) where workers of the same skill level are paid the same wage (Acemoglu and Autor 2011; Autor and Dorn 2013). Such grouping can be done in two ways. Following the OECD (2017), I consider one-digit occupation groups, which I aggregate into three broad categories: low-pay occupations corresponds to ISCO-88 groups 5 and 9 (i.e., service workers and shop and market sales workers, and elementary occupations); middle-pay occupations include jobs classified under the ISCO-88 major groups 4, 7, and 8 (i.e., clerks, craft and related trades workers, and plant and machine operators and assemblers); high-pay occupations include jobs classified under groups 1, 2, and 3 (i.e., managers, professionals, and technicians and associate professionals). As agricultural, fishery, health and education industries and the public sector were not included in the analysis, occupations in ISCO-88 groups 6 and 11 are likewise excluded.Footnote 7

Occupations can also be ranked in a more disaggregated way according to their mean wage. Given that the Italian LFS data do not report wage information before 2009 I rank occupations based on their average wage as measured in the Italian component of the 2006 Eurostat Structure of Earnings Survey, which collects wages for a sample of workers and records their two-digit ISCO-88 occupation code.Footnote 8 Column (a) and (b) of Table 1 report the wage-based rankings of occupations I use in the paper.

A second approach is that of using off-the-shelves indexes of occupational task characteristics, i.e., routine, manual or analytical task intensity, which aim at capturing the degree of substitutability between labour and technology in performing an activity. For instance, occupations such as office clerks and unskilled production jobs are more likely to be substituted by computers, industrial robots and other automating machines and have higher routine intensity indexes than high skilled managers and scientists, whose activities are instead complementary to such technologies. Services occupations that entail manual and communication activities (e.g., personal services, food preparers, etc.) are also complementary to routine substituting technology through aggregate demand. Autor et al. (2006) and Autor and Dorn (2013)—AD 2013 hereinafter—created a summary index of occupational relative routine intensity (RTI) based on the description of the US occupations in the 1977 Dictionary of Occupational Titles (DOT; US Department of Labor 1977; Autor et al. 2003).Footnote 9 For each occupation, the index measures the relative use of routine intensive tasks, relative to manual and analytical. This index was adapted to the European occupational classification by Goos and Manning (2007) and Goos et al. (2009) aggregating occupations to twenty-one two-digit groups.

Goos et al. (2009)—GMS 2009 hereinafter—also construct the single components of the RTI, i.e., abstract-, routine- and manual-intensive indexes, allocating the main occupational tasks (from O*NET) into three principal components averaging them at the two-digits ISCO level weighted by their US employment in 2005, and rescaled to be interpreted in terms of standard deviation.

Finally, Peri and Sparber (2009) constructed five indexes capturing the relative use of manual, analytical, routine, complex and communication tasks in each US occupation using the 2003 O*Net database.Footnote 10 D’Amuri and Peri (2014)—DP 2014 hereinafter—adapted Peri and Sparber indexes for the European data. Unfortunately, there is no other direct way of classifying occupational task content in Europe.Footnote 11

Table 1 also summarizes task-based indexes for the two-digit private sector occupations ranked accordingly to the OECD highest to lowest-paying criterion of columns (a). All the indexes are highly correlated among each other and with the wage ranking: not surprisingly, occupations that are usually held by high-skilled individuals are better paid and entails less routine and manual tasks and more analytical and complex tasks.

Summing up, these classifications have several pros and cons. On the one hand (i) looking at occupations is a natural way to study the evolution of labour demand, especially because polarization has been observed both within and across industries; (ii) consistent occupational definitions can be mapped into a wage ranking and into routine/manual/analytical-intensive indexes. On the other hand (i) the differences in the average wages of occupations in Italy with respect to other countries may reflect endogenous evolution of labour demand and of technology adoption (further discussed in “Appendix A”), (ii) the unavailability of wage data in the LFSs poses challenges in constructing coherent rakings of occupations in Italy and in the rest of Europe; (iii) the task-intensity indexes likely suffer of measurement error because of the ad-hoc adjustments and judgment calls made when adapting them to the European occupational classification; (iv) the O*NET measures are defined as of late 1990s/early 2000s, and thus reflect characteristics of occupations that are evolving exactly because of the adoption of technology; (v) the indexes are constructed directly on the description of US occupations and reflect the characteristics of US jobs and may misrepresent the characteristics of European occupations. With regard to the latter two arguments, it is worth remarking that there is an implicit assumption in the regression analysis involving these indexes: that is, the degree of substitutability between automating machines and different types of labour is common to all countries and is that given by the US technology adoption. Such assumption is common to all the papers in the literature that use off-the-shelves US occupational characteristics measures in a cross country setting (for instance, Goos et al. 2014).

4 Occupational Employment and Wage Growth in Italy, 2007–2017

4.1 Descriptive Evidence

Figure 2 describes the changes of occupational employment shares (panel (a)) and of employment growth (panel (c)) in the last decade for three broad occupation groups, low-, middle- and high-paying as defined by the OECD. The growth of low-paying occupations and the decline of middle-paying occupations, respectively, determined a downgrading of the Italian occupational structure as the share of high-paying jobs remained substantially stable.Footnote 12 Focusing on the two recent recessionary periods, which are indicated in Fig. 2 by shaded areas, we see that high-paying occupations suffered the most during the Great Recession as their employment share dropped by 2.2 percentage points between 2007 and 2010 (Brandolini et al. 2018, discuss in more details the variation of income across the distribution during the two recent recessions and the 1992 currency crisis). In the second part of the double dip recession, the share of middle-skill jobs decreased sharply (− 3.4 percentage points between 2010 and 2013). During the recent recovery, instead, we observe employment growth in low and high-pay occupations.Footnote 13

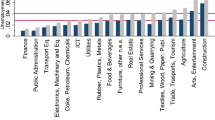

Figure 3 extends the analysis by breaking down the 2007–2017 employment share change (green bars) along the distribution of occupations ranked by their 2006 average. The graph confirms qualitatively the downgrading of the Italian occupational structure (also depicted here by a quadratic fit in Fig. 4a), but it also shows that there is heterogeneity within broad occupational groups. The growth at the low-end is largely concentrated in the lowest decile (+ 4.6 percentage points), while the fourth decile, about in the middle of the distribution, experienced the largest drop (− 4.3 percentage points). Among high paying occupations, there are not significant changes in the occupational employment shares.

Change in employment shares and real wage by occupational mean wage (percentage points). Notes: Author’s elaboration on 2007–2017 Istat Labour Force Survey microdata (2009–2017 for wage growth); private employment excluding agriculture, health services and education. Occupation groups 11 “Legislators and senior officials”, 23 “Teaching professionals”, 33 “Teaching associate professionals”, 6 “Skilled agricultural and fishery workers” and 92 “Agricultural, fishery and related labourers” are not included in the sample. Top coded earnings at 3000 euros are corrected by a 1.25 factor similar to Autor et al. (2008). Robustness checks are provided in the Appendix Fig. A.1. The wage deciles are calculated for the average occupational wage as measured in the 2006 Eurostat Structure of Earnings Survey for Italy

Percentage change in employment shares and in real wage growth by occupational mean wage in Italy and in the US, 2007–2017. Notes: Author’s elaboration on Istat Labour Force Survey microdata and Census Bureau ACS; wage growth is calculated on the period 2009–2017 for Italy and 2007–2017 for the US. Top coded earnings are corrected by a 1.25 factor similar to Autor et al. (2008) for both countries. The hourly deciles are calculated for the average occupational wage as measured in the 2006 Eurostat Structure of Earnings Survey for Italy and the 2006 ACS for the US

The existing literature shows that labour market polarization is also associated with polarized wage growth, as demand factors determine co-movements of quantities and prices (Autor and Dorn 2013). Figure 3 also shows the average occupational hourly wage yearly growth from 2009 to 2017 (orange bars). Wage growth has been heterogeneous across occupations and the overall pattern is not consistent with a demand-driven shock. If anything, middle-pay occupations experienced slightly higher growth, while occupations at the lowest end of the wage distribution and in the middle to top part experienced a slightly milder growth.

To better qualify these changes, I replicate the analysis on US Census ACS data for the period 2007–2015. The US experienced a polarization of the labour market that is reflected both in employment shares and wage growth. Figure 4 compares the shapes of the occupational change and wage growth in Italy and in the US fitting quadratic polynomials. The polarization of the US labour market in the last decade is similar to that observed for the period 1980–2010 by Autor and Dorn (2013) and, differently from Italy, is coherent with a shift of the labour demand curve such that posed by the RBTC hypothesis.

4.2 Regression-Based Evidence on Routine Biased Technical Change

The descriptive analysis suggests that the Italian labour market underwent a downgrading of the occupational structure in the last decade. Such evidence does not seem to square with the hypothesis that the routine-biased technical change is the main responsible for such transformation.

A slightly more formal test of the routine-substituting role of technology is provided by the following regressions. Following Goos et al. (2014), I relate the occupation \(o\), industry \(j\) and year \(t\) log of employment (\(\log empl\)), employment shares (\(empl \,share\)) and log of real hourly wages (\(\log wage\)) to the indexes of occupational characteristics (\(Task\, Index_{o}\)) presented in Sect. 3.2. Similarly to Goos et al., I add in different specifications industry-by-occupation fixed effects (\(\gamma_{oj}\)), which control for differences in occupations across industries, and year-by-industry fixed effects (\(\vartheta_{tj}\)), which capture industry-specific time-varying demand shocks (and thus, business cycle confounders). The underlying framework, which disciplines task demand in each industry, models RBTC as a change in the price of inputs other than domestic labour over time, and is included in the regression analysis as an interaction between occupation indexes and a linear time trend (\(Task \,Index_{o} *t\)). Differently from Goos et al. (2014) and most of the literature, I test whether the results are consistent across different sets of indexes. The variable \(Task\, Index_{o}\) represents in each regression either the RTI summary index of Autor et al. (2003), the abstract, routine and manual indexes derived from O*NET by Goos et al. (2009), or the five-fold occupational characteristics of D’Amuri and Peri (2014). The main regression equations are:

where \(\varepsilon_{ojt}\) are normally distributed zero mean errors (standard errors are clustered at the occupation-industry level).

Table 2 reports the results of Eq. 1. The RTI index (measured in standard deviations and divided by 100) predicts no systematic changes in employment as a function of the relative routine intensity of the occupation-industry cell regardless whether I control for aggregate or industry-specific time effects (columns 1 and 4, respectively). Just based on these regression, we could conclude that either be that RBTC is not the main driver of observed labour market polarization, or that the RTI index is too coarse of a measure to capture structural changes in occupational employment.Footnote 14

Columns 2 and 5 break down the RTI index into the three components (also measured in standard deviations and divided by 100) controlling for aggregate or industry-specific time effects, respectively. The estimated coefficients, which are never statistically significant, suggestively indicate a shift towards manual-intensive jobs away from routine-intensive jobs. The demand for analytical-intensive occupation is instead declining over time: a one standard deviation increase in the abstract task index is associated with a − .58 to − .76 percentage points slower growth in employment each year.

Controlling for the even more disaggregated O*NET-based indexes (D’Amuri and Peri 2014), measured in percentiles divided by 1000, we observe somewhat more robust patterns across specifications that confirm the overall results of the other analyses. Employment in occupations with high content of manual tasks (i.e., low-skilled services) grew significantly—ten percentage points increase in the manual index is associated with around 1 percentage point faster growth in employment each year—while it dropped in occupations with a high level of routine task intensity indexes (− 1.54 to − 1.92 percentage slower growth for ten percentage point higher routine index).

Table 3 replicates the structure of Table 2, but looks at employment shares. Again, the RTI index does not predict systematically changes in employment shares. Consistent with the evidence presented so far, the share of jobs performing routine intensive tasks declined in Italy according to the disaggregated indexes developed by Goos et al. (2009) and D’Amuri and Peri (2014): in columns 3 and 6 we observe an average annual drop of about 4.5 to 6.5 percentage points for a ten percentage points higher level of the routine intensive index. The evidence on analytical and complex tasks is conflicting as the former points to a statistically significant decline and the latter to a statistically significant increase in the shares of occupations with higher values of these task indexes.

Finally, Table 4 provides complementary evidence on wages. I use the log of the average wage in the occupation-industry cell as dependent variable as described in Eq. 3. The results are in line with the qualitative evidence provided in Fig. 4. All disaggregated indexes point to the same direction (columns 2, 3, 5 and 6): wages decreased in low-paying manual and communication-intensive services, and increased at the very top end, in occupation that perform analytical intensive tasks. The effects are however very small, and often not statistically significant at conventional levels once controlling for sector-time fixed effects. The limited evidence on differential wage growth by occupation is also coherent with a high degree of centralized bargaining associated to a compressed wage structure.

From the analyses presented in this section, we can derive two methodological and one factual conclusions. First, one-catch-all indexes of occupational characteristics, such as Autor and Dorn’s (2013) RTI index, are poorly suited to capture changes in the occupational structure that are not coherent with routine-biased technical change. Second, it is important to test for changes in occupational wages, as they are a first indication of whether the dominant force is one of labour demand as it should be in the case technology advancements. Finally, both the descriptive and the regression analyses seem not to support a polarization of the Italian labour market: the Italian occupational structure in the last decade experienced a decline in middle-skill employment, but only in favor of low-skill service jobs. Such conclusion is consistent with empirical evidence on limited adoption by Italian firms of various types of automating technologies, such as industrial robots that could substitute for unskilled production workers (Banca d’Italia 2018) or other ICT practices that would be complemented by high-skill workers (Schivardi and Schmitz 2018). Yet, we have to bear in mind that possibly misclassification of occupations could have generated some measurement error in the analyses.

4.3 A Role for Downward Wage Rigidities?

The limited observed changes in occupational wages suggest that the centralized wage bargaining system, which is associated with strong downward wage rigidities, plays a major role in Italy: this possibly limits the role of prices as a signal of demand shifts in the labor market. To further investigate the nature of the wage changes and to better understand whether they can actually signal changes in labour demand, I move to administrative data obtained from the Italian social security administration (INPS) databases, of which we observe a randomly sampled panel of workers corresponding to about 6.6% of the private sector workforce. These data are better suited to assess the role of wage rigidities in that they cover a large fraction of the workforce, the wage measure is less subject to measurement error as it comes from an administrative source, and it is possible to control for workers compositional effects. A major limitation of the INPS data is that there is no detailed occupation code. Therefore, I use the nationally bargained contracts interacted with blue collar, white collar and manager indicators to proxy for occupations and I then rank them according to the 2006 average wage mimicking the analysis performed on the LFS data.

As validation, I show in Fig. 5 that the changes in employment shares across occupations are similar to those of Fig. 3 based on the LFS data: the occupations in the middle of the distribution are those that experienced the largest drop in employment shares between 2007 and 2015 (the last year for which the INPS data were available at the time of the analysis). Figure 6 compares the distributions of the observed changes in annual wages for the lowest, middle and highest paying occupations as of 2006.

Change in occupational shares across different contract groups (x axis, indexed 1–5), 2007–2015. Notes: Author’s elaboration on INPS microdata; private employment excluding agriculture, health services and education. Occupation groups are proxied by five broad categories binning national contracts codes according to their 2006 average wage ranking

Distribution of wage changes across different contracts, 2009–2015. Notes: Author’s elaboration on INPS microdata; private employment excluding agriculture, health services and education. Occupation groups are proxied by five broad categories binning national contracts codes according to their 2006 average wage ranking. The share of negative changes is reported in the graph for each occupation/contract group. Panel (a) does not adjust for workforce composition, while panel (b) does by plotting within worker annual wage changes

Figure 6a shows the distribution of the average full-time workers daily wage changes between 2009 and 2015 (a period comparable to that analyzed with the LFS data). The share of changes below zero, reported on the graph, measures the extent to which wages are downward flexible. Not surprisingly, and somewhat in line with the descriptive evidence of Figs. 3 and 4, the wages of the occupations/contracts in the middle of the distribution are those that experienced fewer downward changes. However, we see that all occupation/contract groups experienced the same downward flexibility once controlling for workforce composition (by plotting within worker annual changes; Fig. 6b). The degree of wage flexibility measured by the share of changes below zero is about .3 in all occupation groups, in line with what estimated by Adamopoulou et al. (2016).

This evidence so far is not consistent with a drop in labour demand concentrated in the middle-qualification occupation group, as the routine-biased technical change would predict, and yet it shows some degree of wage flexibility across occupations. Such aggregate figures mask, however, cross-sectors heterogeneity. Panel (a) to (d) of Fig. 7 plot the composition adjusted wage changes for the five occupation groups in four sectors: manufacturing, construction, whole sail and retail trade and financial activities. In sectors where wage bargain is highly centralized and the presence of unions is stronger, e.g., manufacturing and construction, the occupations in the middle of the distribution show a slightly lower degree of flexibility than in other occupation/contract groups. On the other hand, retail trade is characterized by similar degrees of flexibility across occupations while financial services show higher heterogeneity across occupation/contract groups (and, still, not a high share of negative wage changes for the middle occupation group).

Distribution of wage changes across different contracts in four sectors, 2009–2015. Notes: Author’s elaboration on INPS microdata; private employment excluding agriculture, health services and education. Occupation groups are proxied by five broad categories binning national contracts codes according to their 2006 average wage ranking. The share of negative changes is reported in the graph for each occupation/contract group controlling for workforce composition (by plotting within worker annual wage changes). The four panel report the results for the manufacturing (panel a), construction (panel b), retail and wholesale trade (panel c) and financial service sectors (panel d)

Overall, this exercise indicates that negative demand shock can result into negative wage changes despite the rigid wage bargaining system. These changes, however, do not seem to be concentrated in the middle-paying occupation group. It is possible, however, that the large drop in employment observed in the middle of the distribution occurs exactly because of the wage rigidities. In fact, these latter are at least as strong in the middle of the occupational distribution as in other parts, and possibly stronger in manufacturing and in construction. Such wage rigidities were a possible cause for a contraction of labour demand among middle-qualification workers as employment was the only margin of adjustment left once the crisis hit (Adamopoulou et al. 2016).

4.4 Demand or Supply? Trends in Sectoral Employment and in the Composition of the Labour Force

Recent contributions by Bárány and Siegel (2018) and Comin et al. (2018) show that job polarization may also be caused by secular trends in sectoral shifts away from manufacturing towards both low- and high-skilled services. Similarly, the changes observed in Italy in the most recent decade could be due to structural changes in sectoral composition, thus including within broad-sector polarization not captured by the time-specific sectoral indicators. Moreover, during the prolonged crisis the non-tradable sector may have been less affected by the collapse in global trade thus contributing to the growth of the low-pay occupations employment share. On the other hand, the collapse of the construction sector, which in 2017 is still 26% below its 2007 employment level, definitely contributed to the reduction in middle-pay routine jobs such as building trade and other related craft workers, especially during the first part of the double-dip recession (Fig. 2a, c). Table 5 summarizes these changes in the employment shares for five broad activity groups as measured in the LFS data, and shows the evolution of the within industry shares of low, middle and high-pay occupations between 2007 and 2017.Footnote 15

At the same time, recent empirical and theoretical contributions highlight the role of labour supply in shaping the pattern of polarization (Basso et al. 2017; Cerina et al. 2017; Mandelman and Zlate 2014). These analyses indicate that structural changes in the participation of women and foreign born workers, possibly endogenous to the adoption of automating technology, interplay with demand shifts. The increased participation by these groups slightly reinforce the overall polarization patterns, depress the wages of the groups they are more in direct competition with, while they allow incumbent workers to specialize and upgrade their skills thus contributing to capital accumulation and improvements in welfare. Italy recently experienced significant changes in labour supply that can be concurrent factors in determining the observed changes in the occupational structure and wage growth. In a recent work, De Philippis (2017) summarizes these patterns, which are mainly attributable to the recent migration waves, the ageing of the workforce, the secular increase in women labour force participation and the rise in college graduation rates.

To investigate more formally how changes in sectoral and labour force composition shaped the occupational changes I perform a simple Blinder–Oaxaca decomposition. Such exercise does not allow to distinguishing demand from supply factors, as there is no credible counterfactual analysis. Yet, it provides an accounting exercise on how much of the observed changes in occupational shares can be attributed to the change in the labour market share of each sector and demographic group (composition effect), and how much is instead due to unexplained factors including changes in the incidence of the sectors and workforce groups in each occupation (incidence effect).

The analysis is based on a simple regression decomposition as follows:

where the dependent variable is the linear probability of being employed in any of three broad occupation categories, low, middle and high-pay, for each individual i in time t (\(t = \{ 2007,2017\) }); the vector \(X_{it}\) contains five sectoral indicator variables and indicators for nativity status, gender, age class and education (the omitted sector group is manufacturing). By taking the difference of average outcome between two periods, we recover three quantities:

-

an incidence effect, that is the change in the incidence of a sector or a demographic group in the occupation holding their weights in the workforce fixed, \(E\left( {X_{it}^{'} } \right)\left( {\beta_{t} - \beta_{t - 1} } \right)\);

-

a composition effect, that is the change of each sector and demographic group weight in the workforce times its initial incidence, \(E\left( {X_{it} - X_{it - 1} } \right)'\beta_{t - 1}\);

-

a residual, unexplained, component.

For example, the incidence effect of a worker demographic characteristic (e.g., female gender) captures how much of the observed change of an occupation group is explained by the change in the presence of workers with that characteristic in the occupation, holding their labour market share constant. The composition effect, instead, measures how much of the observed change is due to the change of the demographic group weight in the workforce, holding the initial incidence constant.

The main results, which are presented in Figs. 8 and 9, show a high degree of heterogeneity across the three occupation groups between incidence and composition effects. Figure 8 shows that the increase in the low-pay employment share is mainly due to changes in the incidence of the various components and to sectoral composition: workforce composition, in aggregate, had a negligible role. However, once we further decompose the composition effect by each single component, we find that the increase in the presence of foreign born fueled the rise of low-pay occupations by almost one-fifth of the observed change while the increased number of college graduates in the workforce counteracted such effect (Fig. 9a). Among the different sectors, the rise of the service one, where low-pay jobs are more prevalent, was the main contributor to the increase in their observed share (Fig. 9b).

Blinder–Oaxaca decomposition of observed change in occupational shares, 2007–2017. Notes: Author’s elaboration on Istat Labour Force Survey microdata; private employment excluding agriculture, health services and education. Occupations are divided into three broad categories following the OECD (2017) classification. Occupation groups 11 “Legislators and senior officials”, 23 “Teaching professionals”, 33 “Teaching associate professionals”, 6 “Skilled agricultural and fishery workers” and 92 “Agricultural, fishery and related labourers” are not included in the sample. The areas represent the contribution to the observed change in occupational employment share due to changes in labour force composition, group incidence and other unexplained factors, as described in Sect. 4.4

Contribution of single components to the compositional effect, 2007–2017. Notes: Author’s elaboration on Istat Labour Force Survey microdata; private employment excluding agriculture, health services and education. Occupations are divided into three broad categories following the OECD (2017) classification. Occupation groups 11 “Legislators and senior officials”, 23 “Teaching professionals”, 33 “Teaching associate professionals”, 6 “Skilled agricultural and fishery workers” and 92 “Agricultural, fishery and related labourers” are not included in the sample. The areas represent each demographic group (panel (a)) and sector (panel (b)) contribution to the observed change in occupational employment share due to changes in the group labour force participation, as described in Sect. 4.4

All three factors, the sector and workforce composition and the incidence component, contributed to the decline of the middle-pay occupations employment share. However, most of the observed drop can be attributed to changes in the sectoral composition and in particular to the rise of the accommodation and food and services sectors (relative to manufacturing) where middle-pay jobs are less present.

Finally, the observed negligible variation in the share of high-pay occupations masks a much richer dynamics. In aggregate, changes in workforce and sectoral compositions drove up the share of high-pay occupations, while the aggregate incidence and other unexplained factors drove it down (Fig. 6). Among the sectors, the rise of service again was the main determinant of the increase in the high-pay employment share. The rise in the college graduate share contributed positively (by more than 2.5 percentage points) to the overall change, counterbalancing—and almost netting out—the negative effects due to the increase in foreign born and to other unexplained factors.

To sum up, the composition of the Italian occupations shifted quite dramatically towards low-skill/low-pay jobs in the last decade. This stylized fact is remarkably different from what observed in other countries: already from Fig. 1, we know that the share of low-skilled jobs increased by less in other major European economies and in the US, and most of the polarization occurred in favor of high-skill/high-pay jobs. The evidence presented in this section seems to support the idea that few concurring factors have played an important role. First, changes in sectoral composition explain an important part of the growth of low-skilled occupations. This is mainly due to the rise of the accommodation and food sector and of the non-tradable service sector, which are labour intensive but determine little value added growth—as, for instance, in the case of tourism (Petrella and Torrini 2019). Second, despite a dramatic increase in labour supply among low-skilled workers in the same period, which also contributed to the rise of low-pay occupations (most notably, due to the increased presence of foreign born), wages did not dropped in these jobs. This fact points towards a complex interaction of supply and demand factors.

While routine-biased technological change is unlikely to be the only determinant of such a shift, it could have contributed to a reallocation of economic activities away from manufacturing towards the service sector, possibly triggered by the Great Recession (Jaimovich and Siu 2020), in combination with other factors including globalization and off-shoring. However, given the unique industrial structure of the Italian economy, characterized by small firms that hardly adopt any modern managerial practice and invest little in research and development, the scope for a rise of high-skill professional service has likely been limited. Therefore, low-skilled service gained important shares of overall employment thanks also to supply forces. Yet, exactly determining why Italy differs from other countries in this respect goes beyond the scope of the paper, as it relates to a much more dramatic structural transformation that requires a proper analysis.

5 Conclusions

The occupational structure of many advanced economies, including Italy, underwent some dramatic changes in the last two decades (OECD 2017). The existing US and cross-country-based literature largely attributes these changes to the adoption of automating technology that substitutes for routine tasks on the job, complement high-skill analytical labour and generates demand for low-skill manual services. The paper documents a hollowing out of the middle-pay routine-intensive jobs in the most recent decade, which are likely due to both demand factors, such as structural transformation, and supply forces related to changes in the workforce composition. Routine-biased technical change seems to play a secondary role: in combination with the contributions by Goos et al. (2009), Goos et al. (2014) and Olivieri (2012) on the period 1990s–2010s, the evidence presented herein indicate that the Italian occupational structure did not change homogenously over the past 20 years, as it would be predicted by such leading hypothesis.

In fact, the descriptive evidence shows a decline in middle-pay occupations while almost all the employment growth has been among low-pay, low-qualified occupations. Until the mid-2000s, instead, the decline of middle-pay occupations occurred in favor of the growth in high-pay, high-qualified occupations (Olivieri 2012). The regression analysis supports such evidence, although the results from indexes that summarize the characteristics of the occupations in terms of tasks performed are not always coherent. Overall, the occupations in which employment and employment shares grew the most were those intensive in manual tasks; those in which they grew the least were associated with more routine tasks. Moreover, occupational wage growth does not exhibit the same patterns, differently from what it would be predicted after a pure demand shift. The evidence presented herein, thus, does not support the hypothesis that only demand factors, such as routine-substituting technology, were the main drivers of the observed occupational change consistent with the observed limited adoption of automating technology in Italy, which prevents the extent of routine task substitution. Even though, ideally, one wants to analyze a longer time period and more detailed occupational data to better distinguish each channel, the evidence presented in this paper points to other demand and supply structural determinants of occupational change highlighted also by the most recent international literature (Comin et al. 2018; Bárány and Siegel 2018; Mandelman and Zlate 2014; Basso et al. 2017).

Interestingly, part of the destruction of middle-pay routine-intensive jobs occurred during the Great Recession, similarly to what observed for the US by Jaimovich and Siu (2020). Determining whether this occupational shift is purely cyclical or due to demand forces, including automation technology triggered by the recession, is difficult and such interactions between structural and cyclical factors have not been investigated thoroughly in the literature. In the Italian case, in particular, the empirical evidence provided here seems to suggest that also cyclical factors played an important role, especially, because of the collapse of the construction sector.

There has been a great deal of discussion about the potential for automation to substitute for routine labour both in manufacturing and in services (Brynjolfsson and McAfee 2011; Frey and Osborne 2017; OECD 2017). Such concerns are definitely well posed given the advancements of artificial intelligence and robotics, but the exact extent of such substitution has been limited and the prospects for the labour market still uncertain (Autor and Salomons 2018). Still, the OECD (2017) suggested that we could observe up to 10% of job positions disappearing in the next 10–20 years in Italy due to technology-labour substitution. The strong creation of low-qualified manual-intensive occupations and the limited adoption of automating technology observed in the most recent decade imply that a strong reversal in both trends must occur for the OECD hypothesis to occur.

Notes

It is important to notice that the analysis is subject to the break in the classification of occupations in 2011 that cannot be fully accounted for. See Sect. 3.2 for a discussion of this issue.

Rosolia (2010) estimates milder growth rates at the tails of the wage distribution than those estimated by Olivieri (2012). The administrative data used by both works do not contain occupational codes: polarization is measured only examining wage percentiles growth and not occupational average wage growth.

Wages are reported in the LFS as gross monthly earnings from labour for employees only and are top-coded at 3000 euros per month. I perform two adjustments: first, I impute hourly earnings for self-employed workers using a simple linear prediction based on observable characteristics (age, foreign-born status, education level, region, part-time status as well as gender, marital status and number of children both separate and interacted). Second, I adjust top-coded earnings by a factor 1.25 following Autor et al. (2009). Results, available upon request, are robust if I do not impute wages to self-employed, if I do not adjust top-coded earnings or if I adjust them by a factor of 1.5.

This is a more coarse classification than that adopted in the US: the Census, American Community Survey, and Current Population Survey contain about 300 three-digit occupations based on the Standard Occupational Classification, or its adaptations.

Starting from the official many-to-many crosswalk between CP2001 and CP2011 occupational codes produced by Istat, the matching procedure uses as weights the 2011 employment of each CP2011 occupation divided by all potential employment if one were using CP2001 codes. Therefore, the solution I adopt to solve for the structural break smooths the series in 2011 around the levels observed between 2007 and 2010 (as I adapt the definition of occupations to the one prevailing before 2011). Although this solution is arbitrary, it creates smooth occupational shares series that are not dramatically affected by statistical artifacts. I am not aware of any other official crosswalk that allows to smooth the occupational series. The crosswalk between the two classifications is available upon request.

Moreover, I also exclude from all the subsequent analyses the flowing two-digit occupation groups: 23 “Teaching professionals”, 33 “Teaching associate professionals”, and 92 “Agricultural, fishery and related labourers”.

Similarly, Goos et al. (2014) rank occupations based on external wage data sources (i.e., panel household survey like the ECHP and the EU-Silc which contains two-digits occupation codes) since the EU LFS do not report wage information at all.

The DOT recorded objective and subjective dimensions of occupational requirements for each six-digit occupation and classified them in 44 variables. The RTI is constructed as the difference in the logarithms of routine cognitive and routine manual minus the logarithms of non-routine analytic, non-routine interactive and non-routine manual scores. Each of these indexes is based on the percentiles values corresponding to their rank in the task intensity distribution (Autor et al. 2003; Autor et al. 2009; Autor and Dorn 2013).

O*NET is the most recent equivalent to DOT. Peri and Sparber’s (2009) measures are interpretable as percentiles, i.e. each occupation is associated with more than one index that characterizes its content of manual and communication tasks relative the use in other occupations. Acemoglu and Autor (2011) also use O*NET to construct task intensity indexes, but their version has only an ordinal interpretation. Acemoglu and Autor (2011) and Autor and Dorn (2013) also use occupational groups rather than task indexes given the arbitrary judgment involved in classifying occupations by aggregating the numerous variables contained in O*NET and DOT..

The only exception is the OECD Programme for the International Assessment of Adult Competencies (PIAAC) that allows constructing task-based index of occupational content for each OECD country (see Arntz et al. 2017, for a recent application). However, PIAAC it has been released very recently and classifying occupations based on recent task specialization may cause endogeneity problems as the task content of occupations evolve exactly because of technological advancements.

The results are robust when measuring employment on hours worked rather than on person counts.

I defer to Sect. 5 a discussion of how recessions and changes in occupational structure could be related.

I need to aggregate industrial sectors into five broad categories. This is because of the changes in the industrial (ATECO) classifications in 2011, which affected mainly service subsectors. Although the service subsectors (professional services, personal services, transportation and communication) are not fully comparable over time, it is worth noting two facts. First, the largest change in the employment share was in the transportation, utilities and ICT (+2.6 between 2007 and 2017 versus +0.3 in professional services and +1.7 in the personal service sector). Second, personal services have among the highest incidence of low-pay occupation (around 60% in 2007), and professional services have the highest incidence in high-pay occupations (64% in 2007). Such large degree of heterogeneity within the service sector is hindered when looking at the aggregated figures.

References

Acemoglu, D., & Autor, D. (2011). Skills, tasks and technologies: Implications for employment and earnings. In O. Ashenfelter & D. Card (Eds.), Handbook of labour economics (Vol. 4B, pp. 1043–1171). Amsterdam: North-Holland.

Adamopoulou, E., Bobbio, E., De Philippis, M. et al. (2016). Wage rigidities and business cycle fluctuations: A linked employer-employee analysis. IZA Journal of Labour Policy. https://doi.org/10.1186/s40173-016-0078-5.

Arntz, M., Gregory, T., & Zierahn, U. (2017). Revisiting the risk of automation. Economics Letters, 159, 157–160.

Autor, D. H., & Dorn, D. (2013). The growth of low-skill service jobs and the polarization of the US labour market. American Economic Review, 103(5), 1553–1597.

Autor, D. H., Katz, L. F., & Kearney, M. S. (2006). The polarization of the U.S. labour market. American Economic Review, 96(2), 189–194.

Autor, D. H., Katz, L. F., & Kearney, M. S. (2008). Trends in U.S. wage inequality: Revising the revisionists. Review of Economics and Statistics, 90(2), 300–323.

Autor, D. H., Levy, F., & Murnane, R. J. (2003). The skill content of recent technological change: An empirical exploration. Quarterly Journal of Economics, 118(4), 1279–1333.

Autor, D., & Salomons, A. (2018). Is automation labour-displacing: Productivity growth, employment, and the labour share. Brookings Papers on Economic Activity (forthcoming).

Ballatore, R., Colonna, F., & Depalo e Santiago Pereda-Fernández, D. (2018). Educational mismatch in Italy: An appraisal. Bank of Italy Occasional Paper (forthcoming).

Bank of Italy. (2018). Annual Report on 2017. Rome, Italy

Bárány, Z. L., & Siegel, C. (2018). Job polarization and structural change. American Economic Journal: Macroeconomics, 10(1), 57–89.

Basso, G., Peri, G., & Rahman, A. (2017). Computerization and immigration: Theory and evidence from the Unites States. NBER Working Paper No. 23935.

Brandolini, A., Gambacorta, R., & Rosolia, A. (2018). Inequality amid income stagnation: Italy over the last quarter of a century. Bank of Italy Occasional Paper No. 442.

Brunetti, I., Cirillo, V., & Ricci, A. (2018). Tecnologia e variazione dell’occupazione nei mercati locali del lavoro. INAPP Working Paper No. 13.

Brynjolfsson, E., & McAfee, A. (2011). Race against the machine. Lexington: Digital Frontier Press.

Bugamelli, M., & Lotti, F. (eds.) (2018). La crescita della produttività in Italia: La storia di un cambiamento al rallentatore. Bank of Italy Occasional Paper No. 422.

Cerina, F., Moro, A., & Rendall, M. P. (2017). The role of gender in employment polarization. CMF Discussion Papers 2017-04. University of Zurich, Department of Economics, Working Paper No. 250.

Cirillo, V. (2016). Employment polarisation in European industries. International Labour Review, 157(1), 39–63.

Comin, D., Lashkari, D., & Mestieri, M. (2018). Structural change with long-run income and price effects. NBER Working Paper no. 21595.

D’Amuri, F., & Peri, G. (2014). Immigration, jobs, and employment protection: Evidence from Europe before and during the great recession. Journal of the European Economic Association, 12(2), 432–464.

De Philippis, M. (2017). The dynamics of the Italian labour force participation rate: Determinants and implications for the employment and unemployment rate. Bank of Italy Occasional Paper no. 396.

Fernandez-Macias, E. (2012). Job polarisation in Europe? Changes in the employment structure and job quality, 1995-2007. Work and Occupations, 39(2), 157–182.

Frey, C. B., & Osborne, M. A. (2017). The future of employment: How susceptible are jobs to computerisation? Technological Forecasting and Social Change, 114, 254–280.

Goos, M., & Manning, A. (2007). Lousy and lovely jobs: The rising polarization of work in Britain. Review of Economics and Statistics, 89(1), 118–133.

Goos, M., Manning, A., & Salomons, A. (2009). Job polarization in Europe. American Economic Review, 99(2), 58–63.

Goos, M., Manning, A., & Salomons, A. (2014). Explaining job polarization: Routine-biased technological change and offshoring. American Economic Review, 104(8), 2509–2526.

Jaimovich, N., & Siu, H. E. (2020). Job polarization and jobless recoveries. The Review of Economics and Statistics, 102(1), 129–147.

Mandelman, F., & Zlate, A. (2014). Offshoring, low-skilled immigration, and labour market polarization. Atlanta FED, Working Paper 2014-28.

OECD. (2017). OECD employment outlook 2017. Paris: OECD Publishing. https://doi.org/10.1787/empl_outlook-2017-en.

Olivieri, E. (2012). Il cambiamento delle opportunità lavorative. Bank of Italy Occasional Paper no. 117.

Olivieri, E., & Nellas, V. (2012). The change of job opportunities: The role of computerization and institutions. Working Paper DSE no. 804.

Peri, G., & Sparber, C. (2009). Task specialization, immigration, and wages. American Economic Journal: Applied Economics, 1(3), 135–169.

Petrella, A., & Torrini, R. (eds.). (2019). Turismo in Italia: Numeri e potenziale di sviluppo. Bank of Italy Occasional Paper no. 503.

Rosolia, A. (2010). L’Evoluzione delle retribuzioni in Italia tra il 1986 e il 2004 secondo i dati dell’archivio WHIP. Politica Economica, 2.

Schivardi, F., & Schmitz, T. (2018). The IT revolution and Southern Europe’s two lost decades. Working paper.

Schivardi, F., & Schmitz, T. (2019). The IT revolution and Southern Europe’s two lost decades. Journal of the European Economic Association. https://doi.org/10.1093/jeea/jvz048.

US Department of Labor. (1977). Dictionary of occupational titles (4th ed.). Washington, DC: US Government Printing Office.

Acknowledgements

I thank three anonymous referees, the editor Filomena Maggino, Matteo Bugamelli, Federico Cingano, Francesco D’Amuri, Marta De Philippis, Alfonso Rosolia, Paolo Sestito and Eliana Viviano for their comments. The views expressed in this paper are those of the author and do not necessarily reflect those of the Bank of Italy.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendices

Appendix A: A Comment on the Structure of Occupation in Italy

As discussed in Sect. 3.2, one of the main caveat of using task-based index is that they are defined on US occupational characteristics. Therefore, the regression evidence above is based on the implicit assumption that the degree of substitutability between automating machines and different types of labour is common to all countries. However, the analysis above carries little information on how routine-substituting technology affects Italian occupational employment shares and wages if Italy differs with respect to the US and the rest of Europe in terms of occupational characteristics (e.g., tasks performed, wage settings) and technology adoption. Similarly, Figs. 3 and 4 are based on the Italian occupational wage distribution, which may differ from those observed in the US and in Europe. For instance, the polarization curves carry little information on the changes in substitutability between automating technology and labour if Italian occupations are paid differently than in other countries exactly because of a different degree of complementarity with capital.

Table 1 reports occupational groups ranked by mean occupational wage as reported by Goos et al. (2014) along with their wage ranking in Italy based on the 2006 SES (column (b)) and the indexes of occupational characteristics: column (c) reports the Autor and Dorn (2013) relative intensity index (expressed in standard deviations), columns (d) to (f) report each of three components of the RTI index (Goos et al. 2009) and, finally, columns (g) to (m) report D’Amuri and Peri (2014) tasks percentile indexes.

The table shows some interesting patterns, especially in terms of wage rankings. Comparing Goos et al.’s wage ranking (columns (a)) with the Italian wage ranking in column (b) we see that the rankings largely overlap, thus proving robustness of the descriptive analysis (the correlation between the Italian SES and the Goos et al. rankings is 0.93). However, there are some substantial differences regarding single occupations. At the top end, for instance, physical, mathematical and engineering professionals earn less in Italy than in the European average. In the middle, qualified labourers and technicians earn less in Italy than in Europe; and at the bottom of the occupational distribution, customer service clerks and salespersons are ranked 8th and 16th in Italy, respectively, versus 14th and 20th in Europe. Moreover, life science and health associate professionals, which are classified among the better paying occupations by the OECD and Goos et al., have about the same as the 2006 median wage in Italy. The opposite is true, for instance, for drivers and mobile plant operators who seem to be well paid in Italy despite they mainly perform manual and routine tasks.

Several factors contribute to determining the differences in average occupational wages between Italy and Europe. Among others, the lower extent of technological adoption in Italy which limits the complementarities between high-skilled professionals and technology (Bugamelli and Lotti 2018; Bank of Italy 2018; Schivardi and Schmitz 2019), and inefficiencies in the matching process between workers of different skill levels, which lead to low high-skill premia (Ballatore et al. 2018).

This simple observation puts into question the ability of such index measures to capture the substitutability between technological capital and labour in countries with different institutional features and technological adoption. While the decline in routine-intensive jobs has been observed everywhere in the most advanced economies, and it is confirmed in Italy too, it is unclear whether identification strategies based on occupational characteristics have proven robust enough to identify in the routine-biased technical change the main driver for such a profound transformation of the labour market.

Change in employment shares and real wage without top-coding correction (percentage points). Notes: Author’s elaboration on 2007–2017 Istat Labour Force Survey microdata (2009–2017 for wage growth); private employment excluding agriculture, health services and education. Occupation groups 11 “Legislators and senior officials”, 23 “Teaching professionals”, 33 “Teaching associate professionals”, 6 “Skilled agricultural and fishery workers” and 92 “Agricultural, fishery and related labourers” are not included in the sample. Top coded earnings at 3000 euros are not corrected differently from what reported in Fig. 3. The wage deciles are calculated for the average occupational wage as measured in the 2006 Eurostat Structure of Earnings Survey for Italy

Appendix B: Additional Analyses Over the Period 2011–2017

The following Tables B.1, B.2 and B.3 provides additional analyses to test the robustness of the results to the structural break in occupational classification occurring in 2011. Compared to Tables 2, 3, and 4 the results are robust and qualitatively similar despite the change in the base year.

Rights and permissions

About this article

Cite this article

Basso, G. The Evolution of the Occupational Structure in Italy, 2007–2017. Soc Indic Res 152, 673–704 (2020). https://doi.org/10.1007/s11205-020-02460-2

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11205-020-02460-2