Abstract

An internationalizing wave swept through many developing and emerging countries’ banking systems in the years before the onset of the Global Financial Crisis (GFC) in 2008. Early critics of the influx of foreign banks worried that local affiliates of international behemoths could serve key nodes for transmitting turbulent conditions in the global financial hubs to the peripheries of the world economy. The eruption of the GFC and its aftermath, it would appear, decisively settled the dispute over the merits of foreign control of national banking systems in the critics’ favor. Yet the simple foreign/domestic ownership distinction cannot answer the questions that animate this article: why did foreign-owned banks play an amplifying role during the crisis in one region (post-communist Central and Eastern Europe) but not in another (Central and South America)? What accounts for the difference in how foreign-owned banks responded to a common financial shock across the two regions? I argue that financialization of banking systems in the post-communist European group of countries is a key mediating factor that explains why the heavy foreign bank presence in the region amplified the regional effects of the global credit crunch in 2008 and the years that followed.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

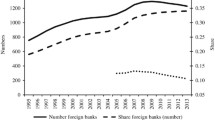

Two big changes transformed many developing and emerging market countries’ banking systems between the early 1990s and the eruption of the Global Financial Crisis (GFC) in 2008. First, the share of lending provided by state-owned banks precipitously dropped (and the number of privately owned banks exploded) as governments sold their stakes in financial institutions to private investors.Footnote 1 Second—and more important for the purposes of this article—the locus of banks’ ownership structures shifted away from residents and toward “parent” banks headquartered in the major financial centers at the core of the global financial system. Ownership data from 5234 banks in 137 countries (reported in Claessens and Van Horen 2014) reveal a worldwide increase in foreign-owned banks’ share of domestic assets, rising from under 20% in 1995 to nearly 35% in 2009. In some countries, foreign-owned banks came to control nearly the entirety of the local credit market.

Many mainstream economists in the United States (and elsewhere) welcomed the surge of cross-border banking activity in the run up to the GFC. They cited three key benefits of the growing presence of global banks in developing and emerging market countries. First, local branches and subsidiaries can tap into the parent banks’ (massive) internal capital markets, thereby increasing the amount of loanable funds in the economy, offering the promise of “raising the recipient country’s level of physical investment and growth” (Dekle and Lee 2015, p. 17). Second, in addition to being able to draw on a much larger pool of savings to finance investments, “foreign banks often introduce superior lending technologies and marketing know-how,” with positive spillover effects as domestic banks acquire and emulate the imported technologies and management practices (De Haas 2014, p. 273). Finally, a number of scholars and practitioners cited evidence that foreign banks’ subsidiaries were more resilient during periods of financial market turbulence than domestic banks, since the foreign-owned banks could turn to their deep-pocketed parent institutions for liquidity infusions during credit crunches (Arena et al. 2007; Crystal et al. 2002; De Haas 2014, p. 274; Grittersová 2017).

The benign view of the foreign takeover of developing countries’ banking systems did not go unchallenged, however. The concern raised by sociologist Fred Block about global banks’ efforts to pry open foreign financial sectors epitomizes the more critical perspective:

There is a good chance that Global Financial will be far more reluctant to make loans to local businesses than the bank it replaces. For one thing, its branches are likely to apply formulae that were developed at its international headquarters that could well be insensitive to local conditions. For another, Global Financial is going to compare the returns and risk on those loans with the returns and risk of investments that it could make anywhere else in the world (1996, p. 209).

Another critic from the heterodox wing of development economics, Robert Wade, expressed similar fears about the influx of foreign-owned banks into developing countries’ financial systems:

No country should let its banking system be taken over by foreign banks—even though in developing countries Western banks are likely to be more ‘efficient’ than domestic ones—for at times of crisis banks rely heavily on their home state and are likely to sacrifice operations in developing countries in order to protect their home base. (quoted in Epstein 2017, p. 50).

Some economic policymakers also worried about the deleterious consequences of the internationalization of national banking systems. “Domestic banks,” observed Brazilian central banker Persio Arida, “accept central bank control easily, but foreign banks do not.… You can deal with banks through regulation in normal times, but during crises you don’t have time, you need informal influence. But if the banking system is controlled by foreigners, then this does not work” (quoted in Martinez-Diaz 2009, p. 85).

The outbreak of the 2008 crisis appears to have decisively settled the dispute over the merits of foreign control of national banking systems in the critics’ favor. Rather than dampening the instability unleashed during the market panic, foreign banks in developing countries amplified the effects of the crisis. Foreign-owned affiliates served, in this view, as key nodes for transmitting the effects of the credit crunch in the crisis-stricken global financial hubs to the peripheries of the world economy. Financial sector practitioners seem to now accept this dimmer view of the merits of the internationalization of banking: 75% of practitioners surveyed by the World Bank in 2015 and 2016 agreed that global banks “contribute to international shock transmissions” (World Bank 2018, p. 6).

Descriptive data from the years when the GFC was in full swing (2008–2010) also comport with the view that the presence of foreign-owned banks made things worse for developing and emerging countries. Figure 1 shows a negative association between countries’ rates of economic growth during the GFC and foreign banks’ share of total banking assets in the year immediately before the onset of the crisis. The foreign bank share variable alone explains 33% of the between-country variation in these developing and emerging market countries’ growth performances during 2008–2010.

Growth during the GFC and foreign banks’ share of total assets

If the image of foreign-owned banks as transmitters of instability from the financial systems of their parents’ home countries to the rest of the world is correct, then we should see evidence (as in Fig. 1) that the growth-inhibiting impact of the GFC was largest in the countries where foreign-owned banks were most dominant. And, further, we would also expect to see evidence that foreign banks behaved differently during the crisis than their domestic counterparts. The lending cutbacks pursued by local affiliates of global banks in the wake of the crisis of 2008 should have been more severe than retrenchment experienced by purely domestic banks.Footnote 2 In this view the most salient dimension for predicting banks’ post-2008 lending behavior is their ownership structure: foreign-owned banks in developing countries should be stingier than domestic banks when a major liquidity crunch strikes, as it did in 2008.

But the foreign/domestic distinction cannot easily answer the question that drives this article: why did foreign-owned banks play an amplifying role during the GFC in one region (post-communist Central and Eastern Europe) but not in another (Central and South America)? Foreign banks flooded into national banking systems in both regions in the years before 2008. (Fig. 2 tracks the share of domestic assets controlled by foreign-owned banks in each region over time.Footnote 3) Both regions were thus tightly connected to the international financial system and were hard-hit by the crisis emanating from the heart of the US financial system in 2008. But it is only in the post-communist European setting that a statistically significant difference in foreign banks’ levels of post-crisis lending can be detected. In Latin America, by contrast, banks’ lending activity after the crisis was not significantly shaped by foreign/domestic ownership status. What accounts for the difference in how foreign-owned banks responded to a common shock across the two regions?

Regional trends in foreign bank ownership

The difference in the degree of financialization of the regions’ banking systems, I argue, can help us better understand why the amplification effect of foreign banks kicked on in the post-communist European setting. Following Gabor (2010) and Hardie et al. (2013), financialized banking denotes a shift away from more stable, “patient” forms of capital provision (relationship-based banking) toward very short-term (overnight), “impatient,” market-mediated forms of liquidity management (market-based banking). Wansleben’s article in this special Theory and Society issue describes a very important step in the financialization of global banking: the turn to funding short-term liquidity needs through repo markets, which transformed the circulation of credit among banks from an “entity-based” approach (in which debt contracts remained on the books of originators) to a “market-based” model, through which even the shortest-term debts can be securitized and traded.

Banking systems in the post-communist region had traveled further along the financialization path than banking systems in Latin America in the years before the GFC. As a result, when the crisis hit in 2008, the foreign affiliates of global banks in Central and Eastern Europe were more heavily exposed to a triumvirate of risks: diminished flows of liquidity from stressed parent banks, exchange rate volatility, and erosion of the local depositor base. Foreign banks responded to the greater risks they faced by curtailing their lending activities.

While many sounded alarms about the fragilities engendered by financialization of banking in the historically rich Northern countries at the core of the international financial system (cf. Davis 2009; Epstein 2005), the link between the dual forces of internationalization and financialization in the Central and Eastern European banking systems and those banking systems’ greater vulnerability to an imported financial market collapse was downplayed (if not ignored) in the years before the onset of the GFC. In 2007, for example, the World Bank reported “banking systems in the region, which are dominated by Western European banks, appear to be strong and able to withstand sizeable potential shocks” (quoted in Smith and Swain 2010, p. 18). One lesson that can be drawn from the comparative analysis undertaken in this article is that financialization generates submerged risks in heavily foreign-owned banking systems that can surface when financial markets in the global banks’ home countries seize up.

A second lesson speaks more directly to the financialization literature. Prior work centering on the experience of advanced Northern economies tends to tie financialization and internationalization together; for example, Hardie and Howarth observe “financialization almost always in practice involves internationalization and, always, the reverse” (2009, p. 1018). The retrospective analysis of foreign banks’ behavior during the GFC reveals, by contrast, that processes of internationalization and financialization in developing and emerging economies can become uncoupled. Both processes can proceed apace, or internationalization can move more swiftly than financialization (and vice versa). The evidence in this article suggests that financialization of banking systems functioned like a volume knob during the GFC: turning it up to higher levels made it likelier that the key nodes for transmitting the effects of the panic in the core of the international global system, foreign affiliates of international banks, would more drastically curtail their lending activities.

The plan for the rest of the article follows. In the following section, I describe some of the main governance challenges posed by the internationalization of countries’ banking systems. Next, I move to the comparison of banking systems in Central and South America and post-communist Central and Eastern Europe before and during the GFC. To gauge the extent of change in foreign-owned and domestic banks’ behavior after the GFC, I examine annual data on total customer lending from 650 banks operating in 36 Latin American and Post-Communist European countries (2002–2012). I confirm that foreign-owned banks in the post-communist region reduced local lending over and above the lending cuts imposed by non-foreign banks involved in the same national credit markets. This effect was more muted in the Central and South American countries in the sample. I then illustrate the differences in the behavior of foreign affiliates during the GFC through a comparison of the experiences of two subsidiaries of the same US-based parent bank, Citigroup’s Chilean affiliate Banco del Chile and its Polish subsidiary, Bank Handlowy. I wrap up with a discussion, drawing heavily from Gabor’s (2010, 2011) important analysis of the roots and consequences of financialized banking in the post-communist European countries, of the main propagation channels through which the turmoil in the hub of the international financial system spread throughout the region’s banking systems.

Governing internationalized banking systems

The extension of cross-border banking to the post-communist European and Latin American regions in the 1990s was driven by several factors. The barriers to entry and exit from national financial systems posed by capital controls and regulatory measures fell as many countries in each region followed the path of capital decontrol and market liberalization. Figure 3 illustrates the trend toward openness in the years before the GFC by tracking a measure (from Fernández et al. 2015) of restrictions on cross-border capital flows, ranging from a minimum of 0 (no restrictions on any asset category) to a maximum value of 1, for the set of post-communist European and Latin American countries in the sample.

Regional trends in capital account openness

Along with the move toward opening up channels for cross-border capital flows, the legal hurdles put in place by countries to keep out foreign banks were largely dismantled across the two regions in the 1990s and early 2000s.

In addition to the relaxation of entry and exit restrictions, privatization of state-owned banks offered potentially lucrative opportunities for global banking groups based in the United States, Canada, and Western Europe, who were keen to establish commercial presences in relatively “underbanked” regions (Grittersová 201, p. 26). Competitive pressure in the financial industry prompted consolidation and, as a result, in some countries foreign control over domestic banking assets became both very high and extraordinarily concentrated in just a handful of banks: in the case of Estonia, for example, foreign-owned banks (mostly Swedish) controlled 97% of the country’s banking assets, and the concentration ratio (the fraction of assets held by the country’s five biggest banks) reached 99% (Pistor 2010, p. 7).

Some longstanding governance issues associated with cross-border banking emerged as the systems in countries in both regions became more internationalized in the 1990s and early 2000s. In the absence of “hard” law-type global rules to distribute and oversee regulatory responsibilities, officials tasked with ensuring financial market stability faced the question of which country’s regulations applied: the home country or the host country in which the foreign bank had established its presence. The home-host issue had been taken up in the mid-1970s after the failures of two large, internationally connected banks (Herstatt in Germany and Franklin National in the United States) spurred the Basel Committee to establish guidelines (embodied in the “Concordat” of 1975) for distributing home and host supervisory responsibilities (Helleiner 2015). Home country authorities were tasked only with monitoring solvency requirements of the foreign branches of their banks; the bulk of regulatory responsibilities fell to the host countries’ governments (Lupo-Pasini 2017, pp. 65–66). At the time of the Concordat the extent of cross-border banking was modest and, in any case, the dominant mode of entry for foreign banks was as subsidiaries of the parent, which meant that (unlike branches) the foreign entities were legally incorporated as part of the host countries’ banking system (Lupo-Pasini 2017, p. 64).

The regulatory landscape changed during the 1980s and 1990s as the internationalization of banking accelerated. The activities of new foreign affiliates established in developing and emerging contexts, “de facto shadow banks set up to avoid the supervisory and prudential requirements of host authorities,” fell into regulatory gaps between host country supervisors who were incapable or unwilling (for fear of driving away the foreign banks they wanted to attract) to oversee them and home country authorities who “were unable to gain information on the consolidated solvency and liquidity situations of their national banks” (Lupo-Pasini 2017, p. 67). The regulatory pendulum swung toward greater home country control, embodied in three types of governance arrangements: (1) consolidated supervision (which implies a minimum degree of cooperation between home and host authorities); (2) Memoranda of Understanding (MoU), in which home country supervisors set out non-binding requirements for information sharing and other agreements between home and host country authorities); (3) Colleges of Supervisors, involving networks of home and host supervisors that meet annually to share information, but which “primarily represent the home country supervisor’s interests” (Beck 2016, p. R42).Footnote 4 In Europe, the drive toward greater economic integration deepened the commitment to home country control: the European Commission’s adoption of the “passport” system vested control in a single regulator and allowed banks and other financial institutions to operate freely across national borders with the assent of the single supervisor (Pistor 2010).

The governance gaps generated by the increasing asymmetry of home versus host authority over international banks became evident after 2008. The mismatch of incentives facing home and host authorities could be papered over during boom times; in the midst of a credit crunch and severe market turmoil, however, conflicting interests are fully revealed, as rescue operations to save highly-leveraged global banking groups drew capital away from the subsidiaries and branches to be sent back toward the ailing parent organization. While these foreign affiliates dominated peripheral countries’ local banking systems, they were often rather small parts of the global bank’s portfolio and could be jettisoned for the sake of the core country’s interests. As Pistor observes, “the regulators in Rejkjavik, Stockholm, and Vienna concerned themselves primarily with the stability of the banks they regulated, but had little interest in the stability of the markets in which their banks had come to play a dominant role” (2010, p. 23). More broadly, “the pre-crisis arrangements for cross-border cooperation,” in Beck’s words, “were focused on sunny-day cooperation, but did not constitute an adequate basis for crisis management” (2016, p. R43).

But the governance problems ran deeper than misaligned incentives during an unprecedented financial system crisis. If the home country authorities are asleep at the wheel and the host country’s authorities have limited capacity to control developments in the banking system, the conditions for a debt-fueled, unsustainable financial expansion can arise. Indeed, there were foreign bank-led credit booms in the immediate years before the 2008 crash in both post-communist Europe and in Latin America—though the boom was more pronounced in the European setting (Hansen and Hansen and Sulla 2013). Pistor (2010) gives a hypothetical example of a host country that, in light of a worrisome acceleration in the private credit market, attempts to throw sand in the wheels of credit creation by raising reserve requirements and imposing administrative ceilings on bank lending. Domestic banks are likely to comply, and subsidiaries of the foreign bank may follow the rules as well—but the global bank from the home country can get around the restrictions by lending directly to customers or by establishing entities that “are not subject to Host’s banking regulations and thus proved unresponsive to the imposed restrictions” (Pistor 2010, p. 6). The vulnerabilities of the banking system are amplified if large shares of the new loans are denominated in foreign currencies (Chitu 2012).

The upshot of this discussion is that the internationalization of developing and emerging countries’ banking systems builds up financial fragilities that are exacerbated by governance gaps. Below, I bring in bank-level data from 36 countries in the two regions to analyze more systematically how the fragilities played out by comparing foreign-owned banks’ behavior to their domestic counterparts before and during the GFC. The analysis of the bank-level lending data confirms that internationalization did not produce the same consequences everywhere: foreign-owned banks’ lending cutbacks were deeper in the post-communist countries than in their Central and South American counterparts. Before moving to the main analysis, however, I briefly compare trends in the organization and trajectory of the regions’ banking systems to see if there are any other obvious factors aside from the degree of financialization that might account for puzzling difference in foreign affiliates’ behavior across the regions during the crisis. To preview, the regions look quite similar along several relevant dimensions in the immediate years before the crisis—and, if anything, the descriptive data suggest that the banking systems of post-communist European were slightly healthier, on average, than the Latin American countries. These measures do not, however, account for submerged risks associated with financialization of the regions’ banking systems, which, as I argue in the final section of this article, sheds light on why foreign banks acted as amplifiers for the crisis in the post-communist region.

Foreign banks and local credit markets in crisis: comparing post-communist European and Latin American banking systems

The country-level evidence in Fig. 1 suggests the possibility that global banks, when they expanded their operations through branches and subsidiaries to the credit markets in low- and middle-income countries, served as engines of transmission for the liquidity shock in the financial centers to the rest of the world. Many of the local affiliates of global banks were, after all, more dependent on international wholesale funding markets than domestic banks. And when the interbank lending markets in the global financial centers completely broke down after the shock of Lehman Brothers’ September 2008 bankruptcy and liquidation, the foreign-owned banks that funded their lending activities primarily through the international funding market were forced to cut back on their supply of credit to a greater extent than local, stand-alone banks. In some cases, the local affiliates were called upon by the parent bank to redirect some of their capital to credit-starved subsidiaries in other places (Aiyar 2012; Didier et al. 2011; Mihaljek 2010, pp. 18–19). The testable implication from this line of thinking is that lending by foreign affiliates of big international banks dipped more dramatically during the depths of the crisis than lending by domestic banks, irrespective of the national or regional context in which the banks were operating.

The severity and duration of the downturn after 2008 in the post-Communist countries of Central and Eastern Europe, paired with the fact that “Latin America, a region that has traditionally been severely affected by international financial turbulence, was relatively resilient during the global financial crisis,” made economists more attentive to differences in how banks were operating in the two regions (Brunnermeier et al. 2012, p. 14). And there are some notable differences identified by economists. First, the foreign banks operating in Latin America tended to channel their activities through local branches that preserved a significant degree of autonomy from the headquarters bank. The multinational banks operating in post-communist Europe maintained a more hierarchical structure in which funding flowed from the center and senior members of the parent bank were more heavily involved in governance and risk management decisions (Cull and Martínez Pería 2013; Grittersová 2017; Kamil and Rai 2010).

Second, some economists suggested that foreign banks and their branches and subsidiaries were likelier to lend to firms and households in foreign currencies in post-communist countries than in the Latin American setting (Brown and De Haas 2012; Myant and Drahokoupil 2012). Foreign currency (FC) lending indeed accounted for a majority of loans in several non-Eurozone countries in the region—but, as is the case for foreign bank penetration, there was significant within-region variation in the levels of FC lending. And, further, a closer look at regional averages shows that there was no notable difference in the pre-GFC share of lending denominated in foreign currencies: comparing the 17 Latin American and 17 post-communist countries in my sample for which pre-2008 data are available (Chitu 2012), the average share of FC lending was 50.8% for the Latin American and 50.3% for the post-communist countries.Footnote 5

Finally, some have noted that many of the local affiliates of foreign banks in Latin America funded their credit creation primarily through their local currency deposit bases, while in the post-communist region a good deal of the funding for the expansion of domestic credit came directly from parent banks headquartered in Western Europe or from the wholesale markets (Brown and De Haas 2012; Cull and Martínez Pería 2013). These differences in pre-GFC funding practices are better understood, however, as symptomatic of the underlying driver of the divergent regional outcomes.

Pointing to inter-regional differences in the lending and funding strategies followed by foreign affiliates and their global parent banks raises a follow-on question: why did banks’ pre-crisis practices differ so much across these regions? In the final sections of the article, I interpret these differences and their post-2008 consequences through the lens of financialization of banking systems—but there are other plausible reasons for the variation that I document more systematically in the next section.

For one, the parent banks driving the internationalization of banking systems in each region by setting up de novo branches or acquiring local affiliates were based in different locations: the dominant foreign institutions in the post-communist setting were mainly headquartered in Western European countries like Austria, Germany, France, and Italy, while the foreign influx in Central and South America was spearheaded by American, Canadian, and Spanish banks (Cull and Martínez Pería 2013; Grittersová 2017, p. 43). Perhaps the difference in the behavior of local affiliates during the GFC mirrors the performance of different business models and management practices followed by the parent banks that focused their expansionist energies in one region rather than the other. Because it is difficult to categorize, let alone measure, the different business models and practices followed by the parent banks of foreign affiliates in these regions, I try in the subsequent sections to address this issue indirectly by including bank-level fixed effects in the regression models, which absorbs the effects of bank-specific, time-invariant factors that are hard to measure directly. Further, comparing the post-crisis experience of two subsidiaries of the same US-based bank—Citigroup’s Chilean affiliate Banco de Chile and its Polish subsidiary, Bank Handlowy—provides a way to generate some illustrative evidence by controlling for the identity of the parent bank while moving across different regional contexts.

We might also wonder about how the regulatory environment differs across the two regions. Perhaps foreign banks took greater risks because banking systems in the post-communist countries were more laxly regulated. On this point, however, there is little evidence of any systematic differences in the stringency of banking regulations between the two regions. Simple difference-of-means tests fail to detect statistically distinguishable differences in any of the most relevant regulatory and supervisory categories captured in Barth et al.’s (2008) database of countries’ banking system regulator practices: on average, measures of practices that limit foreign involvement in the domestic banking system (by, for example, requiring foreign banks to enter as subsidiaries rather than branches), capital adequacy requirements, and the authority of banking system supervisors look similar for the set of post-communist and Latin American countries analyzed in this article. Likewise, there is no obvious regional differences in the stringency of the “macroprudential” regulations that might have curtailed the riskiest practices followed by local affiliates of foreign banks (such as FC lending to unhedged households and firms): only in four of the 18 Latin American (Argentina, Brazil, Colombia, and the Dominican Republic) and three of the 18 post-communist European countries (Moldova, Romania, and Ukraine) were any kinds of significant limits on foreign currency lending imposed before the GFC erupted in 2008 (Cerutti et al. 2017).

The risk to the post-communist countries posed by the behavior of foreign-owned entities that had come to dominate their banking systems was not picked up by many conventional measures of financial vulnerability—which helps explain why the severity of the credit crisis in the region took many observers by surprise. It was not obvious that the foreign influx rendered the post-communist region more susceptible to contagion from a crisis in the core. In Fig. 4, using bank-level data aggregated to the national level by Andrianova et al. (2015), I track one indicator of financial fragility: the ratio of “impaired,” non-performing loans to gross loans.

Financial fragility as measured by loan impairment

It is only after the eruption of the GFC that this measure of fragility spikes for the post-communist European countries; in fact, before the crisis the regional average was substantially better than the average for the Central and South American countries. Similarly, tracking a measure (see Fig. 5) of real-time perceptions of countries’ levels of financial stress (Gandrud and Hallerberg 2019) gives little reason to suspect that the post-communist countries were substantially more vulnerable than the other region covered in this article: the “FinStress” score only moves significantly higher for the group of post-communist countries in 2007, after which the trends for the two regions follow their anticipated paths.Footnote 6 Prior to 2007, the average FinsStress score for the region is significantly lower than the score for Latin America or all other (advanced, emerging, and developing) countries outside of the two regions.

Financial fragility as measured by the FinStress Index

On several observable dimensions, then, the pre-crisis banking systems of post-communist Europe appeared no more vulnerable than the pre-crisis banking environments in Central and South American to the effects of a financial crisis imported from the parent banks’ home countries. Yet, as the data in Figs. 4 and 5 show, conditions deteriorated more quickly in the post-communist countries after 2008—and the conditions in this group of countries’ banking systems remained turbulent for a longer stretch of time. Next, I turn to the bank-level data that I use to test for the region-specific effects of foreign ownership. The evidence points to systematic differences in the post-GFC lending behavior of foreign affiliates of global banks in the two regions: foreign-owned banks in post-communist countries responded more aggressively to the crisis conditions than domestic counterparts.

Bank-level evidence for regional differences in foreign-owned banks’ behavior

The data on banks’ lending behavior that I use in the statistical tests come from OSIRIS, a commercial database compiled by the financial services firm Bureau van Dijk. The dataset includes information on total annual customer lending for up to 650 publicly listed banks in 18 Latin American and 18 post-communist countries, covering the ten years between 2002 and 2012.Footnote 7 The countries in the sample are listed in Table 1.

The main dependent variable in the analysis is the change in each of the banks’ (logged) total customer lending between the previous year (t – 1) and the current (t) year. To distinguish whether the ownership in year t for each of the banks was primarily domestic or foreign, I drew on the classifications in Claessens and Van Horen’s (2014) database. I extended their dichotomous foreign/domestic ownership coding for all banks in the 36 countries in my sample through 2012.

Some simple difference-of-means tests, reported in Table 2, yield results that fit with the general expectation that foreign-owned banks were stingier in the wake of the crisis than domestic banks. In the pre-crisis period, both domestic and foreign banks expanded their lending at rates that were statistically indistinguishable; after the onset of the GFC, however, the big difference in the average values of the lending variable emerges, and the relative stinginess of the foreign banks compared to the domestic banks is statistically significant at the 0.001 level.

Does the post-crisis difference in banks’ lending patterns hold for both regions? Table 3 shows the t-test statistics for the post-crisis period in Latin America and the post-communist European countries. The statistically significant difference in average lending by foreign versus domestic banks in the wake of the crisis is only observed in the post-communist group of countries; in Latin America, the decline after 2008 was somewhat less pronounced for the domestic-owned banks, but the difference compared to international banks is not statistically significant.

The difference-of-means tests are suggestive, but a stronger test is needed to confirm that the negative effect of foreign ownership on lending in the post-crisis period is limited to the post-communist European countries. I use a “difference-in-differences” approach to pin down the direction and size of the effect of banks’ ownership status during the Global Financial Crisis; following Dekle and Lee (2015), the setup allows me to compare the change in foreign-owned banks’ pre- and post-crisis lending behavior to the change in lending by banks that faced similar crisis-induced challenges (namely, reduced demand for and supply of credit) but which happened to be owned by residents of the country. To implement the difference-in-differences estimator I use the following model specification:

The dependent variable in the model is the change in the total (logged) amount of customer lending by bank i from year t – 1 to year t. The model captures the effect of the outbreak of the crisis from 2008 onward on the level of lending in each of the 630 banks operating in the 36 countries that constitute the dataset (GFC equals 1 in 2008 and each subsequent year), the effect of foreign ownership, and an interaction term (GFC*foreign-owned), for which a negative and significant coefficient (γi < 0) indicates that the foreign-owned banks operating in the country responded to the crisis and its aftermath with a bigger drawback of credit than the domestic banks. The inclusion of bank dummy variables is intended to screen out the impact of unmeasured (and perhaps unobservable) time-invariant factors at the level of the individual bank that might affect lending behavior (Dekle and Lee 2015).

The results from the data analysis are presented in Table 4. The table shows three different models: column (1) displays results from the “pooled” analysis in which banks from both regions are included, and columns (2) and (3) show separate results from the analyses of domestic and foreign banks’ behavior in the Latin American and post-Communist countries. The first model, using the pooled sample, shows that the crisis induced (unsurprisingly) a general reduction in the expansion of bank credit, but the foreign-owned banks were particularly stingy in 2008 and the years that followed: the negative and significant interaction term indicates that the “treated” cases (non-domestic banks) cut back more than the “control” cases (domestic banks) during the crisis. In keeping with the simpler difference-of-means tests, and in line with the expectations laid out in the previous section, the effect of foreign ownership is not consistent across regions: there is no evidence to support the claim that foreign banks responded to the crisis differently from domestic banks in the Latin American countries; there was a sharp decline in credit across the region after 2008, but the credit markets in these countries proved to be fairly resilient, and I do not find a statistically significant distinction between the global affiliates and the stand-alone domestic banks in the region. The post-Communist region is a different story: when the difference-in-differences approach is taken to the bank lending data from the 18 post-Communist countries for which I have data, the “treatment” effect (foreign ownership) is negative and significant. Foreign-owned banks, on average, cut lending by 8% more than the domestic banks in the region during the crisis years (2008–2012). One reasonable implication to draw from the results is that the presence of foreign-owned banks was a contributing factor to the deeper and longer post-2008 economic downturns suffered by the countries in the post-communist region.

The findings broadly comport with the statistical results reported by Adams-Kane et al. (2013), Choi et al. (2013), De Haas et al. (2012), Dekle and Lee (2015), and Haselmann et al. (2016).Footnote 8 While the severity of the credit crunch in Central and Eastern Europe is widely recognized—and in fact spurred an ad hoc cooperative response, the 2009 “Vienna Initiative” that sought commitments from parent banks in the North and Western parts of Europe to maintain exposure levels via their subsidiaries and branches in five post-communist countries (Latvia, Hungary, Romania, Bosnia-Herzegovina, and Serbia)—not all analysts agree that foreign banks amplified the crisis in the region. Bonin and Louie (2017), for example, argue that the behavior of the “big 6” foreign banks was similar to domestic banks in the first 2 years of the GFC (2008 and 2009), but other foreign banks markedly cut back on lending in the crisis. Epstein’s (2017) qualitative study of banking in the region provides the most direct challenge to the evidence from my statistical analyses: she contends, based largely on interviews with bank managers and regulators, that the subsidiarization strategy adopted by foreign banks in these countries (over 80% of the foreign affiliates were set up as subsidiaries) meant that global banks began to view the region as a “second home market.” It was, according to Epstein, in these parent banks’ long-run interest not to cut and run. She finds convincing evidence that foreign-owned banks did not pull up stakes and leave the region in droves. Epstein does not, however, systematically compare bank-level data from post-Communist European countries to other regions; in fact, the comparison she draws is between foreign banks in the post-communist and Northern parts of Europe (notwithstanding the limited penetration of foreign banks in historically rich Northern countries’ banking systems).Footnote 9

In addition to the results reported in Table 4, I estimated models with country (rather than bank-level) fixed effects, which included direct measures of bank-specific conditions.Footnote 10 In these specifications I found very similar relationships among the key explanatory variables (ownership status, GFC period, and the interaction between foreign-ownership and the post-2008 time period) and the outcome variable (the first difference in the [logged] measure of banks’ total lending to customers): in the post-communist European sample the foreign*GFC measure was negatively signed and significant.

In Table 5, I report results from three other models. In these specifications, the (logged) lending indicator in year t becomes the outcome variable; on the right hand side, the specifications are identical to those reported in Table 4, with the addition of the lagged (by 1 year) lending measure. Again, the results are consistent with the region-specific impact of foreign ownership status on banks’ lending behavior during the post-GFC period.

A tale of two foreign-owned banks during the crisis

The big global banks that led the internationalizing charge tended to pick one region as their key sphere of influence--American, Canadian, and Spanish banks, for example, carved up the Latin American market, while Western European banks dominated the post-communist systems. This pattern raises the possibility that it is the difference in the home bases for the foreign-owned banks, not something about the nature of the host regions’ banking systems, that better explains the puzzle of inter-regional variation in foreign banks’ lending behavior during the GFC.

Comparing the experiences of a sizeable number of well-matched affiliates of the same parent bank that operate in different regional contexts would help rule out the alternative explanation—but finding these matched pairs of banks is no easy task. I identified two banks that come closest to fitting the bill: Banco de Chile, a Chilean subsidiary of the US-based megabank Citigroup, and a Polish subsidiary, Bank Handlowy. The comparison supplies illustrative, but far from definitive, evidence in line with the argument in the article.

In 2001 Citi acquired a controlling stake in Bank Handlowy (which is among the top ten largest banks in the country), after the Polish government, under heavy pressure from the United States, IMF, and EBRD, abandoned a plan to preserve the state-run bank’s monopoly in the national credit market and fully opened the banking sector to foreign investors (Smith and Swain 2010). Citi’s expansion into the Chilean banking market a bit came later; after a year of on-and-off talks with Banco de Chile’s major shareholder, the business conglomerate Quiñenco, the American bank finally confirmed the acquisition of nearly 40% of the shares in the country’s second largest bank in July 2008.Footnote 11

The serious trouble for Citigroup started soon after. Citi’s holdings of structured credit instruments tied to the American mortgage market, which had been kept off the bank’s balance sheet through a legal arrangement known as a structured investment vehicle (an innovation pioneered, not coincidentally, by Citi), blew up when housing prices began to plummet across the country (Faroohar 2016). By August 2008 Citi was totting up losses of $55.1 billion (Hardie and Howarth 2009, p. 1030). Citi’s survival was ensured through a combination of liquidity injections through the Federal Reserve’s Term Auction Facility and the absorption of “toxic” assets through the United States government’s Troubled Asset Relief Program (TARP). The government bailout notwithstanding, the scale of Citi’s losses and the paralysis in the credit markets that followed the September 2008 bankruptcy of Lehman Brothers led the financial press to speculate about both Banco de Chile and Bank Handlowy’s prospects.Footnote 12

Citigroup ultimately held onto both its Chilean and Polish subsidiaries through the depths of the Global Financial Crisis. But the two banks’ performances after the eruption of the crisis in 2008 could hardly have been more dissimilar (see Fig. 6). Between 2008 and 2013 total lending by Bank Handlowy grew by only 1.1%; in 2009, the bank’s lending outlays fell by 15%. During that same time period Banco de Chile’s lending increased by 52.9%; and the decline in the bank’s lending during the single worst year of the crisis, 2009, was only 3.4%, by contrast. The banks’ deposit bases followed similarly divergent trajectories: Bank Handlowy grew its deposits by 10% between 2008 and 2013 while Banco de Chile’s deposit base expanded by 36.8%.

Lending during and after the Global Financial Crisis by two Citi affiliates

Why did two subsidiaries of the same crisis-stricken parent bank follow such radically different paths during the GFC? Chile, a commodity exporter during a global demand slump, was no more shielded than Poland was from the effects of the credit crunch in the core of the international financial system. And by comparison to other countries in its region Poland’s economic growth performance in the first years of the GFC was relatively strong (Bohle and Greskovits 2012, p. 245; Mihaljek 2010; Smith and Swain 2010). Further, there is no evidence to suggest that the parent had chosen to abandon its Polish subsidiary; in December 2008 Shirish Apte, Citi’s chief executive in charge of the bank’s Central and Eastern European operations, told reporters “I say categorically and absolutely we will never sell Citi Handlowy. This is one of the most important banks in Citigroup.”Footnote 13

The more likely driver of the difference is the deeper enmeshment of Citi’s Polish affiliate in a heavily financialized banking environment. Financialization in Poland’s banking system manifested in several ways. Lending was tilted toward ordinary consumers and households rather than small and medium-sized enterprises (Haselmann et al. 2016). A large proportion—over 50% by 2007—of lending to households was denominated in foreign currencies (namely Swiss francs).Footnote 14 Once the Polish national currency, the zloty, weakened (falling by over 20% against the euro in just the fourth quarter of 2008)—due in large part to the drying up of “carry trade” activities, in which financial market players, including many foreign-owned banks in the region, borrowed short-term in cheaper, lower-yielding currencies to speculate in higher-yielding assets (Gabor 2010)—the cost for borrowers to service their foreign-currency debts skyrocketed.Footnote 15 Borrowers were then forced to liquidate their balances with banks like Handlowy in order to continue to make payments on their debts. In the face of uncertainty about Citi’s willingness to continue supporting Bank Handlowy, depositors that still had some savings began to shift them to purely domestic banks. With a shrinking deposit base, lower quality assets cluttering the balance sheet, and a struggling parent bank, the fact that Bank Handlowy drastically cut back on its local lending does not seem so surprising.Footnote 16

How financialization made internationalized banking systems more fragile

What role, then, might the financialization of the post-communist banking systems beyond Poland have played in amplifying the effects of the credit crisis in the region? The discussion in this section focuses on recovering some of the other submerged (at least until 2008) sources of vulnerability that had built up as these countries’ banking systems were taken over by foreign-owned entities.

One of the striking features of the post-communist Central and Eastern European countries’ economic trajectories is that the highly varied paths they followed out of the collapse of central planning in the 1990s nonetheless yielded, in Berglof and Bolton’s (2002, p. 77) evaluation, “remarkably similar” banking systems a decade later. Gabor’s (2010, 2011) recounting of the run up to the GFC describes in rich detail how the process of financialization in Central and Eastern European countries reshaped both money markets and banking systems in the region in similar, and important, ways.

In the traditional banking model, unsecured lending in the money markets flows from the banks with excess reserves to “banks where credit activity outpaced deposit growth and resulted in reserve shortfalls” (Gabor 2010, p. 251). Central banks provide forward guidance by targeting the long-term interest rate and using open market operations to keep market prices for liquidity in line with the target. The financialization of European money markets, however, allowed banks to turn credit risks into tradable assets; as a result, “banks no longer had to rely on retail deposit activity (or central bank liquidity) but could instead tap institutional investors’ large pools of liquidity against collateral—usually securitized bonds—and a promise of repurchase at some very near term, the day after or later” (Gabor 2010, pp. 251–252). The need for collateral to post in the wholesale market spurred the search for “private safe assets” (since the creation of “safe” public assets could not keep up with demand), which fueled waves of securitization.

This process should be familiar from the development of the US repo market in the years before 2008 (see, for example, Wansleben’s article in this special issue). Perhaps less familiar is the role that financialization of money markets played in generating vulnerabilities in the post-communist banking environment. The introduction of the euro in 1999, coupled with regionwide regulatory harmonization efforts, led to a tripling in the size of the euro area repo market between 2002 and 2007 (to around 65% of the euro area’s GDP) (Gabor 2010, p. 253). Global banks with local affiliates operating in Central and Eastern European countries recognized that they could cheaply fund consumer loans (which would be more grist for the securitization mill) in a region that was experiencing booming demand for credit by tapping the wholesale money markets.

A large share of this consumer lending activity in the region was, as noted above, conducted in foreign, “hard” currencies (in addition to euros, households in the region often borrowed in Swiss francs—in Hungary as well as Poland, more than half of household debt by the end of 2008 was denominated in Swiss francs). Just over 85% of direct lending by parent banks was denominated in foreign currencies (Pistor 2012). For the banks, lending in foreign currencies offloaded exchange risk onto the borrowers. Further, affiliate banks found it was much easier (and more profitable) to securitize FC loans than loans issued in the local currency (Brown et al. 2014). For prospective borrowers, the expectation that the local exchange rate would, if anything, continue to strengthen as foreign capital flooded in combined with lower interest rates to make these foreign currency-denominated loans particularly attractive. International banks before the GFC “appeared to attach little risks to the strategies of cross-border wholesale financing” (Gabor 2010, p. 257).

But this activity, facilitated by financialization, created significant vulnerabilities in the region’s banking systems. When the run in the repo market started in the fall of 2008, major banks in financial centers worldwide began the deleveraging process. Liquidity injections from central banks and bailout packages to plug the holes blown in banks’ balance sheets by “toxic” assets may have been helpful at home but did nothing to staunch deleveraging pressures that hit the host countries in the Central and Eastern parts of Europe. Non-residents exited those countries’ money markets in droves: in 2008, $57 billion left the region “as banking groups withdrew their capital to protect their home base” (Pistor 2012, p. 145). The outflow of capital put downward pressure on many of the countries’ currencies, which made the foreign currency loans contracted by millions of households more difficult (if not impossible) to pay back. (Figure 7 sets the nominal effective exchange rate at 100 in 2007 for both the post-communist Europe countries and for the members of the Latin American group to illustrate the divergent trajectories of average exchange rates in the two regions.)

Effective exchange rates in two regions (The exchange rate measures are calculated from Darvas’s (2012) database)

The impaired loans that had not been offloaded and remained on foreign affiliates’ balance sheets thus accelerated the drawback of credit as parent banks pulled funding from the affiliates. And in an effort to try to restore market confidence governments throughout the region began to implement austerity measures, with economic growth-killing consequences (Bohle and Greskovits 2012, pp. 227–248; Gabor 2010, pp. 265, 267).

How did the Latin American countries by and large escape the dynamics that characterized the experience of the GFC in the post-communist setting? The basic claim in the article is that the greater degree of financialization in emerging Europe was a key driver of the difference. A complete explanation for why financialization of banking systems in the run up to the GFC went further in post-communist Europe than in the countries of Central and South America lies well beyond the scope of this article. But several plausible candidates for explaining the different trajectories of financialization in the two regions can be identified. First, as Mihaljek (2010, p. 6) notes, before the crisis the emerging European countries were showered with a “genuine deluge of cross border bank inflows.” Data from the Bank for International Settlements shows that between 2002 and 2007 gross inflows of cross-border private capital to 17 countries in the region increased fivefold, from $90 billion to $440 billion. During that same time period the Latin American countries, by contrast, experienced a decrease of gross cross-border bank inflows that amounted to 4 % of the region’s GDP (Mihaljek 2010, pp. 7–8). Sequencing and geography seem to play important roles in accounting for the pattern of bank-driven capital inflows before 2008: several Latin American countries experienced severe banking crises in the late 1990s and early 2000s, which drove foreign capital away and depressed the demand for credit across the region (Cardim de Carvalho et al. 2010, p. 882). At the same time the demand for credit spiked in the booming US economy, keeping some of the funding that American megabanks might otherwise have exported to countries in its nearby region at home. In the early 2000s the “underbanked” Central and Eastern Europe countries appeared to parent banks in the West like booming credit markets, by comparison. The “deluge” of foreign capital in the form of cross-border bank loans to banks and the non-banking sectors thus accelerated the processes of banking financialization in the region (Gabor 2010, pp. 171–181).

Another plausible factor, highlighted in Gabor’s (2010, 2011, 2012) tracing of the post-communist path toward banking system financialization, involves the IMF’s coercive pressure, embodied by the conditional lending arrangements into which nearly every country in the region entered in the 1990s and early 2000s. Some prudential policy instruments that might have thrown sand in the wheels of the financialization process kicked off by the surging inflows of capital to the region in the run-up to 2008 were, in Gabor’s telling, taken off the table due to the requirements of IMF conditionality. Indeed, the IMF appears to have been particularly attentive to financial sector liberalization in the post-Communist countries. The comprehensive data on conditionality assembled by Kentikelenis et al. (2016) reveals that in the years between 1990 and 2007 there were, on average, two more financial sector conditions in the post-communist lending programs than in the average IMF programs for the Latin American countries in the sample.

To summarize, this discussion of the forces that worked to amplify the local effects of the global credit crunch suggests that it was not internationalization of banking alone that drove the deeper crisis in the post-communist region but the combination of internationalization and financialization. The GFC prompted a rethink of the nature of international financial market regulation; unfortunately, existing governance structures seem poorly suited to mitigating the kinds of vulnerabilities that financialization generated in the post-communist European countries.

Conclusion

The drive toward ever-greater internationalization of banking drew attention from cheerleaders and critics alike to the foreign/domestic ownership distinction as the key factor shaping the fragility of countries’ banking system. In this article I suggest that the foreign/domestic ownership distinction, while important, is on its own insufficient; the distinction cannot fully explain why foreign-owned banks played an amplifying role during the Global Financial Crisis in one region (post-communist Central and Eastern Europe) but not in another (Central and South America). In answer to the question of what accounts for the inter-regional difference in how foreign-owned banks responded to a common financial shock across the two regions, I made the case that financialization generated submerged risks that surfaced when the crisis hit.

The combination of internationalization and financialization in the post-Communist countries’ banking systems turned particularly toxic when the crisis erupted in 2008—but the influx of foreign-owned banks and cross-border connectedness was not, however, all bad news for the region. The costs of opening up the banking sector need to be weighed against the potential benefits. For example, Grittersová’s (2019) statistical analysis of the determinants of credit ratings for 18 emerging European countries in the pre-crisis years (1995–2006) shows that greater shares of foreign ownership robustly improved ratings and lowered the costs of borrowing in sovereign bond markets. Grittersová argues that foreign-owned banks’ roles in increasing the level of financial transparency, disciplining host governments’ fiscal policies, and providing a more liquid backstop in a downturn than domestic banks worked to reassure raters of countries’ creditworthiness. The credibility that foreign affiliates can import along with their parent banks’ capital in normal times needs, however, to be weighed against their potential amplifying effects when a systemic crisis strikes in the heart of the global financial system.

And even if a degree of normalcy returned to banking systems after the worst of the GFC subsided, the unsettling political legacy of the deeper crisis in emerging Europe should not be ignored. As financial conditions in the post-Communist countries worsened during the GFC, mass public support for the governments in power plummeted across the region. Aggregated data on executive approval ratings from all 18 of the Latin American countries and from 6 of the emerging European countries, compiled in the Executive Approval Database (Carlin et al. 2019) and tracked in Fig. 8, demonstrate how many voters turned on their leaders in the post-Communist environment in the years after 2008. Populists in Hungary, Poland, Romania, and elsewhere, capitalizing on the fact that foreign-owned banks had become “objects of hate and loathing during the financial crisis,” garnered public support by going after the outsiders.Footnote 17 Hungary’s Victor Orban is a case in point; as Matthias Siller, the manager of the $800 billion Baring Eastern European fund, observes, Orban “ignored the threat that the banks would pull out and won. And that makes him a bit of a model for the rest of eastern Europe, which is somewhat dangerous for the banks.”Footnote 18 If systemic financial turbulence erupts again, populist-leaning governments in post-communist Europe may well look at the foreign affiliates that stayed as easy targets for expropriation.

Executive approval ratings before and after the GFC

One final lesson that could be drawn from the evidence presented in this article is that foreign-owned banks do not just produce but also respond to financialization by adopting strategies that replicate the practices associated with financialized banking (namely, short-termism and greater exposure to and trading of risks). The experience of the GFC showed that foreign ownership in heavily financialized banking systems can become particularly destructive when governance gaps are large, transmission channels from the core of the global financial system to the periphery are partly hidden, and when policymakers are incapable or unwilling to intervene at the micro-level to control, for example, the extension of foreign currency loans to ordinary borrowers. There have been some noteworthy improvements in the post-GFC regulatory frameworks, particularly in Europe; however, the processes that promoted the financialization of banking systems in emerging markets have proved difficult to reverse, partly because, as Wansleben points out in his contribution, policymakers in the global financial core (and elsewhere) took responsibility for promoting firms’ post-crisis profitability and supporting the very liquidity management strategies that contributed to the crisis in the first place. This article used the GFC to identify an instance of regional divergence in an era of financialization, but convergent pressures may prove difficult for emerging banking systems to resist.

Notes

In eight post-communist countries in Central and East Europe (Bulgaria, Croatia, Czech Republic, Hungary, Poland, Romania, Slovakia, and Slovenia), for example, the share of assets held by state-owned banks fell from 71% in 1995 to 10% in 2010; the share of state-owned assets in the total assets of the banking systems of six Latin American countries declined over the same period from 41% to 19% (Cull and Martínez Pería 2013, p. 4862).

Several post-GFC studies by economists have shown that foreign-owned banks indeed served as transmission channels for the spread of the credit crunch beyond the United States and Western Europe (e.g., Adams-Kane et al. 2013; Aiyar 2012; Dekle and Lee 2015; Cetorelli and Goldberg 2011; De Haas and Van Horen 2011; Didier et al. 2011).

Lupo-Pasini notes the asymmetry as well: “the home’s authorities still retain the highest degree of control over the consolidated bank’s balance sheet and are not legally required to receive the approval of the host supervisors before making a decision” (2017, p. 75).

Pre-2008 FC lending data for Venezuela and Serbia are unavailable. Dropping the three dollarized Latin American countries (Ecuador, El Salvador, and Panama) lowers the regional average to 40.6%.

Gandrud and Hallerberg’s (2019) FinStress measure (which ranges from a minimum of 0 to a maximum of 1) is based on unsupervised text analysis of a corpus of 20,000 Economist Intelligence Unit reports issued between 2003 and 2011.

Not all of the 650 banks provide lending data for each of the years between 2002 and 2012; some banks opened after 2002 and others were dissolved before the end of the time series. In addition, some of the banks in the database did not report balance sheet data to Bureau van Dijk for one or more years in the observation window.

Choi et al.’s (2013) analysis of gross lending data from a global sample of banks (3615) between 2005 and 2009 reveals that foreign-owned affiliates curtailed credit growth more than domestic banks at the height of the GFC. Dekle and Lee (2015) gather an even larger global sample of banks and find that American and European-owned affiliates cut back on lending more than domestic counterparts in 2009. De Haas et al. (2012) and Haselmann et al. (2016) look only at Central and Eastern European countries and, in line with the findings reported in this article, find that foreign banks contracted credit more than domestic banks.

While observing that “foreign affiliates of multinational banks in emerging Europe were more affected and transmitted the external shocks [in 2008] to a greater extent than those operating in Latin America,” Grittersová (2017, p. 203) similarly argues that most Western banks did not cut and run during the GFC and that their presence helped assuage market players’ concerns about the post-communist countries’ creditworthiness.

Alongside the country dummies, foreign ownership status, the GFC indicator, and the foreign*GFC interaction, I added time-varying measures of banks’ profitability, solvency ratio, loan-loss provisioning, size of deposit base, and liquid assets.

“And the winner is: Banco de Chile,” Business News Americas, July 23, 2007. Under De Haas Claessens and Van Horen's (2014; 2011) coding rule, Banco de Chile falls under the threshold for foreign ownership until Citi acquired a 50% stake in 2010. But equity ownership and control may not perfectly line up in this case, and I follow Anginer et al. (2017), who identify Banco de Chile as one of Citigroup’s foreign subsidiaries alongside Bank Handlowy from 2008 to the present. (Citi holds, by comparison, a 75% stake in Bank Handlowy.)

“Fitch: Citi could end up selling stake in Banco de Chile,” Business News Americas, March 10, 2009; “Some Polish banks may be taken over in wake of financial crisis,”

Poland Business Newswire, October 2, 2008; “Will Citi Sell Bank Handlowy?” Polish New Bulletin, December 3, 2007; “Banking Sector on the Move,” Polish News Bulletin, June 30, 2009.

“Citi reassures no plan to sell Handlowy,” Global Banking News, December 9, 2008.

“Swiss franc loans keep allure,” Financial Times, February 27, 2008.

One indicator of carry trade activity is the proportion of currency markets instruments with very short (<7 days) maturities (Gabor 2010). In Poland, 77% of currency instruments in 2007 and 82% in 2010 were short-term; in Chile the proportion never exceeded 25%.

“Kreditklemme gefährdet Polens Wachstum,” Der Standard, March 9, 2009.

Erik Berglof, “Financial Prey for the Populists,” Project Syndicate, April 2, 2019. https://www.project-syndicate.org/commentary/populists-foreign-banks-withdrawal-from-emerging-europe-by-erik-berglof-2019-04.

Boris Groendahl and James M. Gomez, “It’s Déjà vu all over again as Eastern populism rattles banks,” Bloomberg, March 27, 2019. https://www.bloomberg.com/news/articles/2019-03-27/it-s-deja-vu-all-over-again-as-eastern-populism-rattles-lenders.

References

Adams-Kane, J., Caballero, J.A., & Lim, J.J. (2013). Foreign bank behavior during financial crises. World Bank Policy Research Paper 6590.

Aiyar, S. (2012). From financial crisis to great recession: the role of globalized banks. American Economic Review, 102(3), 225–230.

Andrianova, S., Baltagi, B., Beck, T., Demetriades, P., Fielding, D., Hall, S., Koch, S., Lensink, R., Rewilak, J., & Rousseau, P. (2015). A new international database on financial fragility. University of Leicester, Department of Economics.

Anginer, D., Cerutti, E., & Martínez Pería, M. S. (2017). Foreign bank subsidiaries’ default risk during the global crisis: what factors help insulate affiliates from their parents? Journal of Financial Intermediation, 29, 19–31.

Arena, M., Reinhart, C., & Vasquez, F. (2007). The lending channel in emerging economies: Are foreign banks different? IMF Working Paper WP/07/7.

Barth, J., Caprio, G., & Levine, R. (2008). Banking regulations are changing: for better or worse? Comparative Economic Studies, 50, 537–563.

Beck, T. (2016). Regulatory cooperation on cross-border banking – progress and challenges after the crisis. National Institute Economic Review, 235, R40–R49.

Berglof, E., & Bolton, P. (2002). The great divide and beyond: financial architecture in transition. Journal of Economic Perspectives, 16(1), 77–100.

Block, F. (1996). The vampire state. London: Verso.

Bohle, D., & Greskovits, B. (2012). Capitalist diversity on Europe’s periphery. Ithaca: Cornell University Press.

Bonin, J. P., & Louie, D. (2017). Did foreign banks stay committed to emerging Europe during recent financial crises? Journal of Comparative Economic Studies, 45(4), 793–808.

Brown, M., & De Haas, R. (2012). Foreign banks and foreign currency lending in emerging Europe. Economic Policy, 27(69), 57–98.

Brown, M., Kirschenmann, K., & Ongena, S. (2014). Bank funding, securitization, and loan terms: evidence from foreign currency lending. Journal of Money, Credit and Banking, 46(7), 1501–1534.

Brunnermeier, M., et al. (2012). Banks and cross-border capital flows: Policy challenges and regulatory responses. Washington, DC: Brookings Institution.

Cardim de Carvalho, F. J., de Paula, L. F., & Williams, J. (2010). Banking in Latin America. In A. N. Berger, P. Molyneux, & J. O. S. Wilson (Eds.), The Oxford handbook of banking (pp. 868–902). New York: Oxford University Press.

Carlin, R.E., Hartlyn, J., Hellwig, T., Love, G.J., Martinez-Gallardo, C., & Singer, M.M. (2019). Executive approval database 2.0. Available for download at www.executiveapproval.org.

Cerutti, E., Claessens, S., & Laeven, L. (2017). The use and effectiveness of macroprudential policies: new evidence. Journal of Financial Stability, 28, 203–224.

Cetorelli, N., & Goldberg, L. S. (2011). Global banks and international shock transmission: evidence from the crisis. IMF Economic Review, 59(1), 41–76.

Chitu, L. (2012). Was unofficial Dollarisation/Euroisation an amplifier of the “great recession” of 2007-09 in emerging economies? European Central Bank Working Paper Series No. 1473.

Choi, M.J., Gutierrez, E., & Martínez Pería, M.S. (2013). Dissecting foreign bank lending behavior during the 2008-2009 crisis. World Bank Policy Research Working Paper 6674.

Claessens, S., & van Horen, N. (2014). Foreign banks: trends and impact. Journal of Money, Credit, and Banking, 46(1), 295–326.

Crystal, J. S., Dages, B. G., & Goldberg, L. S. (2002). Has foreign bank entry led to sounder banks in Latin America? Current Issues in Economics and Finance, 8(1), 1–6.

Cull, R., & Martínez Pería, M. S. (2013). Bank ownership and lending patterns during the 2008-09 crisis: evidence from Latin America and Eastern Europe. Journal of Banking & Finance, 37, 4861–4878.

Darvas, Z. (2012). Real effective exchange rates for 178 countries: A new database. Bruegel Working Paper 2012/06.

Davis, G. (2009). Managed by the markets. New York: Oxford University Press.

De Haas, R. (2014). The dark and the bright side of global banking: a (somewhat) cautionary tale from emerging Europe. Comparative Economic Studies, 56, 272–282.

De Haas, R., & Van Horen, N., (2011). Running for the exit: international banks and crisis transmission. European Bank for Reconstruction and Development Working Paper No. 124.

De Haas, R., et al. (2012). Foreign banks and the Vienna initiative: turning sinners into saints. European Bank for Reconstruction and Development Working Paper No. 143.

Dekle, R., & Lee, M. (2015). Do foreign banks cut their lending more than the domestic banks in a financial crisis? Journal of International Money and Finance, 50, 16–32.

Didier, T., Hevia, C., & Schmukler, S.L. (2011). How resilient and countercyclical were emerging economies to the global financial crisis? World Bank Policy Research Working Paper 5637.

Epstein, G. A. (2005). Introduction. In G. A. Epstein (Ed.), Financialization and the world economy (pp. 3–16). Northampton: Edward Elgar.

Epstein, R. A. (2017). Banking on markets: The transformation of bank-state ties in Europe & beyond. New York: Oxford University Press.

Faroohar, R. (2016). Makers and takers: The rise of finance and the fall of American business. New York: Crown Business.

Fernández, A., Klein, M.W., Rebucci, A., Schindler, M., & Uribe, M. (2015). Capital control measures: a new dataset. NBER working paper 20970.

Gabor, D. (2010). (De)Financialization and crisis in Eastern Europe. Competition and Change, 14(3–4), 248–270.

Gabor, D. (2011). Central banking and Financialization. New York: Routledge.

Gabor, D. (2012). The road to financialization in central and Eastern Europe: THE early policies and politics of stabilizing transition. Review of Political Economy, 24(2), 227–249.

Gandrud, C., & Hallerberg, M. (2019). The measurement of real-time perceptions of financial stress: implications for political science. British Journal of Political Science, 49(4), 1577–1589.

Grittersová, J. (2017). Borrowing credibility: Global banks and monetary regimes. Ann Arbor: University of Michigan Press.

Grittersová, J. (2019). Foreign banks and sovereign credit ratings: Reputational capital in sovereign debt markets. European Journal of International Relations (OnlineFirst).

Hansen, N-J.H, & Sulla, O. (2013). Credit growth in Latin America: Financial development or credit boom? IMF Working Paper 13/106 (May).

Hardie, I., & Howarth, D. (2009). Die Krise but not La Crise? The financial crisis and the transformation of German and French banking systems. Journal of Common Market Studies, 47(5), 1017–1039.

Hardie, I., et al. (2013). Banks and the false dichotomy in the comparative political economy of finance. World Politics, 65(4), 691–728.

Haselmann, R., Wachtel, P., & Sobott, J. (2016). Credit institutions, ownership and Bank lending in transition economies. In T. Beck & B. Casu (Eds.), The Palgrave handbook of European banking (pp. 623–643). London: Palgrave.

Helleiner, E. (2015). Regulating the regulators: The emergence and limits of the transnational financial legal order. In T. Halliday & G. Shaffer (Eds.), Transnational legal orders (pp. 231–257). New York: Cambridge University Press.

Kamil, H., & Rai, K. (2010). The global credit crunch and foreign banks’ lending to emerging markets: Why did Latin America fare better? IMF Working Paper WP/10/102.

Kentikelenis, A. E., Stubbs, T. H., & King, L. P. (2016). IMF conditionality and development policy space, 1985–2014. Review of International Political Economy, 23(4), 543–582.

Lupo-Pasini, F. (2017). The logic of financial nationalism: The challenges of cooperation and the role of international law. New York: Oxford University Press.

Martinez-Diaz, L. (2009). Globalizing in hard times: The politics of banking sector opening in the emerging world. Ithaca: Cornell University Press.

Mihaljek, D. (2010). The spread of the financial crisis to central and Eastern Europe: Evidence from the BIS data. In R. Matousek (Ed.), Money, banking and financial markets in central and eastern Europe (pp. 5–27). New York: Palgrave Macmillan.

Myant, M., & Drahokoupil, J. (2012). International integration, varieties of capitalism and resilience to crisis in transition economies. Europe-Asia Studies, 64(1), 1–33.

Pistor, K. (2010). Host’s dilemma: Rethinking EU banking regulation in light of the global crisis. Columbia University law School Law & Economics Working Paper No. 378.

Pistor, K. (2012). Into the void: Governing finance in central and Eastern Europe. In G. Roland (Ed.), Economies in transition (pp. 134–152). London: Palgrave Macmillan.

Smith, A., & Swain, A. (2010). The global economic crisis, eastern Europe, and the former Soviet Union: models of development and the contradictions of internationalization. Eurasian Geography and Economics, 51(1), 1–34.

World Bank. (2018). Global financial development report 2017/2018: Bankers without Borders. Washington, DC: World Bank.

Acknowledgments

For very helpful comments I thank Bruce Carruthers, Adam Goldstein, Kim Pernell-Gallagher, participants at the March 2018 conference on financialization and market governance at Northwestern University, and panelists at the June 2019 SASE conference hosted by the New School for Social Research.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher’s note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

About this article

Cite this article

Nelson, S.C. Banks beyond borders: internationalization, financialization, and the behavior of foreign-owned banks during the Global Financial Crisis. Theor Soc 49, 307–333 (2020). https://doi.org/10.1007/s11186-020-09381-6

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11186-020-09381-6