Abstract

We experimentally characterize and measure the interaction between risk and time preferences. Our results indicate that risk and time preferences are intertwined. We find that decision makers are insensitive to time delay for small probabilities of gains, but become progressively more sensitive to time delay as the probability of gain increases. We compare the fit of existing decision models that capture risk and time preferences. Our results indicate that the models which allow for probability-time interaction and capture magnitude effect fit the data better. We also show that accounting for risk-time preferences interaction leads to lower estimated discount rates.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

Consider a decision maker (DM) choosing between two options: receiving $100 with 50% chance tomorrow or receiving $100 with 75% chance in 1 year. Such choices are not straightforward, because it involves trading off outcomes across both the probability and time dimensions. Many economic decisions, such as an investor investing in a start-up or a mutual fund (with different levels of riskiness and lock-up-periods), a doctor deciding on treatment options (with risky future health outcomes) for his patient, a manager choosing between different research and development (R & D) investments, a policy maker deciding between different climate change abatement policies, involve such risk-time trade offs. This paper aims to empirically characterize how decision makers actually choose between such risky prospects paid at different time points.

Future payments are inherently risky. Therefore, when a decision maker chooses between two risky options in the future, the DM’s choices are not only affected by his risk and time preferences, but also affected by the influence of his risk preferences on time preferences.Footnote 1 Empirical investigations also support this interrelationship between risk and time preferences (Keren & Roelofsma, 1995; Anderhub et al., 2001; Weber & Chapman, 2005; Baucells & Heukamp, 2010; Ida & Goto, 2009; Epper et al., 2011; Andreoni & Sprenger, 2012; Cheung, 2015; Miao & Zhong, 2015). Recognizing this interrelationship, Halevy (2008) developed an axiomatic model that can account for risk associated with future payments using a discounted utility with nonlinear probability weighting.Footnote 2 The model jointly accounts for anomalies in risk and time preferences and explains the behavioral deviations from the discounted expected utility model (Fishburn & Rubinstein, 1982). With a similar focus, Baucells and Heukamp (2012) developed the probability-time trade-off (PTT) model to capture the interaction between risk and time preferences accounting also for the magnitude effect (Chapman & Elstein, 1995).Footnote 3 In their model, the interaction between probability and time depends on outcomes through a weighting function but the utility derived from the outcomes is independent of time. The PTT model imposes a constant trade-off between probability and time delay for a specific outcome size. Alternatively, Gerber and Rohde (2018) followed a different approach to capture risk-time preferences interaction: They allowed the weighting function that captures the probability-time interaction to be independent of outcomes but instead imposed the utility to be dependent on time. One other approach developed recently is the range and sign dependent utility (RSU) model (Kontek & Lewandowski, 2017; Baucells et al., 2018), which transforms outcomes (depending on the range) instead of probabilities. Surprisingly, the RSU model generalizes the PTT model to multiple outcome prospects. The different modeling approaches discussed above capture risk-time preferences interaction and are able to explain the behavioral deviations from discounted expected utility (DEU).

Existing experimental studies have shown that time delay produces the same change in preference as the reduction in probability of receiving the outcome would induce. In fact this phenomenon explains why common ratio effect (Allais, 1953) and preference for immediate payment (Loewenstein & Thaler, 1989) is reduced when prospects are delayed and are made risky (respectively) (Keren & Roelofsma, 1995; Baucells & Heukamp, 2010; Andreoni & Sprenger, 2012). Such preference patterns can only be explained by a model that combines risk and time preferences in a non-separable fashion (Baucells & Heukamp, 2012). However, more experimental evidence is needed to understand how the risk and time preferences are combined for different outcome levels, probabilities, and time delays. In other words, there is a need to compare and evaluate alternate approaches to modeling and measuring risk and time preferences interaction.Footnote 4

Our paper aims to fill this gap by (i) providing a clean model free evidence on the interaction between the risk and time preferences for different outcome levels, probabilities, and time delays; (ii) understanding how decision makers incorporate risk and time delay into their evaluations, specifically understanding if the time delay affects the taste (utility) or the probability processing; (iii) comparing and evaluating alternate approaches to modeling risk and time preferences. In order to achieve the objectives, we conducted an experiment where we elicited present certainty equivalents of risky prospects paid at different time points in the future.Footnote 5 We used the certainty equivalents to estimate a simple model (with minimal parametric assumption), which treats time delay as a source of uncertainty (Fox & Tversky, 1995; Abdellaoui et al., 2011a). Our experimental results indicate that there is a significant interaction between the probability and the time delay of receiving the outcomes: subjects were insensitive to time delay for small probabilities of gains but become progressively more sensitive to time delay as the probability of gain increases. On the other hand, we find that the utility a subject derives from his outcomes was not dependent on time at which the subject received the outcomes. Our results, thus offer support to models that capture risk-time interaction using the interaction between probability and time. Further, our results also offer new insights for modeling probability-time interaction.

We also compared the fit of existing decision models that capture risk and time preferences. In particular, we compare the classical models that assume no interaction between risk and time preferences (discounted expected utility model, discounted rank dependent utility model, hyperbolic discounting model), models that capture risk-time preferences interaction using a probability-time interaction approach (Halevy, 2008, PTT model, RSU) and models that capture risk-time preferences interaction using a time dependent weighting and utility function (weighted temporal utility, Gerber & Rohde, 2018). Based on the Akaike information criterion (Akaike, 1998), we find that the models that capture risk-time preferences interaction and account for the magnitude effect (RSU, WTU) fit the data better. Our results also show that, when the risk-time preferences interaction is accounted for, the estimated discount rates capturing pure rate of time preferences are lower. We also replicate the above results in a follow-up incentivized online study.

The paper is organized as follows. Section 2 introduces the model. Section 3 discusses the experiment and results. Section 4 fits the existing decision models to the data. Section 5 reports the follow-up study. Section 6 presents the discussion of the experimental results and the conclusions.

2 Models

We consider a DM who evaluates an one outcome prospect \(L_{1}=(x,E_{p}^{t};0)\) that pays monetary outcome \(x\ge 0\) at time t if event \(E_{p}\) with probability p occurs but pays zero otherwise. We also assume that the prospect \(L_{1}\) is resolved immediately but only the payment happens at time t.Footnote 6 We assume the DM calculates the value (v) of the prospect \(L_{1}\) as follows:

where \(w_{t}(.)\) is a probability weighting function that captures the weight given to an outcome paid at time t with probability p and u(.) is a utility function. The probability weighting function is strictly increasing on the probability interval with \(w_{t}(0)=0\), \(\forall t\). The utility function is also strictly increasing. Note that the model does not have an explicit discount component and allows the probability weighting function (\(w_{t}\)) to vary with time delay. Such a general approach allows to capture how a DM combines probability and time (p and t) in his evaluation. The approach is synonymous with the source function approach (Abdellaoui et al., 2011a) where different time delays to receive the outcomes correspond to different sources of uncertainty.Footnote 7 When \(t=0\), we assume the model in Eq. (1) coincides with the traditional rank dependent utility (RDU) under risk for non-delayed lotteries (e.g., Quiggin, 1982; Tversky & Kahneman, 1992). As \(w_{0}\) is a probability weighting function under RDU, \(w_{0}(1)=1\). Therefore, this allows us to extend our model to two (non-zero) outcome prospects at time \(t=0\). For example, the value (v) of prospect \(L_{2}=(x,E_{p}^{0};y)\) with outcomes \(x\ge y\ge 0\) paid at \(t=0\), is given by:

Equation (2) is critical in our empirical approach as it allows us to derive a utility function u. Also note that, our model in Eqs. (1) and (2) can be generalized to a model that can value two (non-zero) outcome prospects paid at time \(t>0\). For example, the value (v) of a prospect \(L_{2}=(x,E_{p}^{t};y)\), where \(x\ge y\ge 0,\) can be estimated using a more general value function \(v(L_{2})=w_{t}(p)u(x)+(w_{t}(1)-w_{t}(p))u(y)\) with \(w_{0}(1)=1\) and \(w_{t}(1)\le 1\). The primary focus of the paper will be to measure the model in Eq. (1) and characterize the risk-time preferences interaction. Below we discuss, how the existing decision models in the literature relate to Eq. (1).

Special cases of Eq. (1).

The value of the prospect \(L_{2}\) under the standard discounted expected utility (DEU) model is given by:

where \(\delta \in [0,1]\) is the discount factor. DEU is a special case of the model described in Eq. (1) when \(w_{t}=\delta ^{t}p\).Footnote 8 To account for anomalies in risk preferences, the DEU model can be extended to a rank dependent utility set-up (Chew & Epstein, 1990). The value of prospect \(L_{2}\) under discounted rank dependent utility (DRDU) is given by:

DRDU is a special case of the model described in Eq. (1) when \(w_{t}=\delta ^{t}w\). Other models that account for anomalies in time preferences such as the hyperbolic discounted EU model (Loewenstein & Prelec, 1992) and quasi-hyperbolic discounted EU model (Laibson, 1997) are also special cases of the model in Eq. (1) when \(w_{t}=(1+\delta t)^{-h/\delta }w\) (with \(h>0\)) and \(w_{t}=\beta \delta ^{t}w\) (for \(t>0\)), respectively. In fact, we could replace \(\delta ^{t}\) in Eq. (4) with \((1+\delta t)^{-h/\delta }\) to get hyperbolic discounted rank dependent utility (HDRDU), which can account for anomalies in risk and time preferences separately.

Model of Halevy (2008).

The model of Halevy (2008) builds on the DRDU, but also accounts for the fact that future payments are inherently risky. Therefore, apart from the discount rate that captures the pure rate of time preferences, the model also includes a stopping probability P (which captures the mortality risk or the risk of not receiving the payment) that depends on the time delay. The survival probability is then indicated by \(1-P\). Under Halevy (2008), the DM perceives the prospect \(L_{2}\) as a ternary prospect with outcomes \(L_{2}=(x,p(1-P)^{t};y,(1-p)(1-P)^{t};0,1-(1-P)^{t})\). The value of prospect \(L_{2}\) is given by:

where \(\delta\) captures the pure rate of time preferences. The Halevy (2008) model incorporates the survival probability within the weighting function and thereby allows the interaction between probability and time delay. The model is a special case of Eq. (1) when \(w_{t}=\delta ^{t}w(p(1-P)^{t})\).

Probability time-trade off (PTT) model (related to Eq. (1)).

The probability-time tradeoff model (Baucells & Heukamp, 2012) captures the risk-time preferences interaction using a weighting function that depends on both the probability and time delay. In addition the model also accounts for the magnitude effect, by allowing the discount rate within the weighting function to depend on the outcome size. The model is originally defined for one (non-zero) outcome prospect of form \(L_{1}=(x,E_{p}^{t};0)\) where \(x\ge 0\). The PTT value of prospect \(L_{1}\) is given by:

where w is the probability weighting function, \(r_{x}\) is the discount rate that depends on the size of outcome x. The discount rate \(r_{x}=r_{0}+M/x\), where a positive M indicates that discount rate is smaller for larger outcome size (capturing the magnitude effect). The discounting term \(e^{-r_{x}t}\) captures the risk associated with future payment. There is a natural similarity between the model in Eq. (1) and the probability-time trade-off model. Unlike Eq. (1), PTT parameterizes the probability and time interaction. However, unlike PTT, Eq. (1) does not capture the magnitude effect. The PTT model with a constant r would be a special case of Eq. (1)

Weighted temporal utility (WTU) model (general version of Eq. (1)).

Gerber and Rohde (2018) developed the weighted temporal utility (WTU) model for one (non-zero) outcome prospect to jointly account for risk and time preferences anomalies. The WTU value of prospect \(L_{1}\) is given by:

The WTU model is a general case of the model in Eq. (1) as it allows for both probability-time and utility-time interactions. It is an open empirical question if both the utility and probability interact with time delay. Note that the utility function \(u_{t}\) also allows the WTU model to account for the magnitude effect (see Proposition 3.1 in Gerber & Rohde, 2018).

Range and sign dependent utility (RSU) model (generalization of PTT).

Recently, the range and sign dependent utility model for risk (Kontek & Lewandowski, 2017) has been extended to temporal prospects by Baucells et al. (2018). The core idea of range and sign dependent utility is that the DM transforms the outcomes (depending on the range) instead of probabilities. Surprisingly, RSU model coincides with PTT for single outcome prospects.Footnote 9

Under RSU, the reference point of the prospect \(L_{2}=(x,p;y,1-p)\) for time delay \(t=0\) is the minimal outcome y. Therefore, the RSU value of prospect \(L_{2}\) is given by:

Replacing \(D=w^{-1}\) we get:

However, when time delay \(t>0\), the DM perceives the prospect \(L_{2}\) as ternary prospect with outcomes \(L_{2}=(x,pS(t);y,(1-p)S(t);0,1-S(t))\). The S(t) is the survival probability and \(1-S(t)\) captures the risk of DM not receiving the payment. Considering a transformation function \(D=w^{-1}\), the RSU value of prospect \(L_{2}\) is given by:

where [0, x] is the outcome range and 0 is the reference point. Replacing \(D=w^{-1}\) and \(S(t)=e^{-r_{x,y}t}\), we get:

Note that for one-outcome prospects, the \(v(L_{2})\) in the Eqs. (9) and (12) coincide with the PTT model. The discount rate \(r_{x,y}\) in Eq. (12) depends on both outcomes x and y. Baucells and Cillo (2019) find that the sum of outcomes (\(x+y\)) and the largest outcome x has the highest influence on discount rate \(r_{x,y}.\) Therefore, we consider the following specifications for the discount rate \(r_{x,y}=r_{0}+M/x\) and \(r_{x,y}=r_{0}+M/(x+y)\).

In the experiment, we elicit the present certainty equivalent (CE) for a prospect \(L_{2}\) paid at time t, i.e., the sure amount payable at time 0, that the DM considers as equivalent to that particular prospect \(L_{2}\). Once the CE is elicited, the parameters of the model in Eq. (1) can be elicited by equating \(u(CE)=w_{t}(p)u(x)\). After estimating the model in Eq. (1), we also estimate the models described in this section and compare them on the degree of fit.

3 The experiment

The experiment was conducted at INSEAD Sorbonne lab in Paris and consisted of individual computer-based interviews of 50 subjects. The experiment consisted of three sections.

-

1.

In section I (time preferences), the subjects made a choice between two certain payments paid at two different dates. For each question the subject made a choice between an amount paid tomorrowFootnote 10 and an amount paid at a later date. The present certainty equivalent (CE) was elicited by changing the amount paid tomorrow (using the bisection method) until the subject expressed indifference. The four questions in section I allowed measuring the pure time preferences of the subject.

-

2.

In section II of the experiment (risk preferences), the subjects made a choice between a risky prospect and a sure outcome (both paid tomorrow). The CE of the risky prospect was elicited by changing the sure outcome until the subjects expressed indifference. The five questions in section II enabled measuring the risk preferences of the subjects.

-

3.

In section III of the experiment (risk and time preferences), the subjects made a choice between a risky prospect paid later and sure outcome paid tomorrow. The present CE of the risky prospect paid later was elicited by varying the sure-outcome (paid tomorrow) until the subject expressed indifference. The fifteen questions in section III allowed measuring the risk-time preferences interaction.

After each question in all of the three sections, a prefilled choice list was presented to the subjects to confirm their indifference point. The details regarding the experimental procedures are discussed below.

3.1 Subjects and stimuli

The 50 subjects (22 female), of mean age 24, were university students in Paris. The section I stimuli corresponds to two sure outcomes paid at two different payment dates. For the task involving risk (section II) and risk-time (section III), the subjects were asked to choose between a sure outcome paid tomorrow and a risky prospect paid tomorrow or in the future. The outcomes of the risky prospect were decided by the draw of a ball (of subject’s favorite color) from a box consisting of different colored balls at the end of the experiment. For the details of the stimuli used in different sections, please refer to the Appendix A.

3.2 Incentives

All subjects participating in the study were paid a fixed fee of €10. To supplement that amount we instituted a randomized incentive procedure. Subjects were informed that they might be able to play one of their randomly selected choices for real and win a cash amount up to €100. At the end of the experiment, subjects were asked to pick a coin from a box consisting of different colored coins.Footnote 11 If the subject picked up the coin of his or her favorite color — which they indicated at the beginning of the experiment — they were eligible to play one of their choices for real. Each subject had a \(10\%\) chance to play one of their choices for real. Six subjects received on average €80 of variable incentive based on their choices.Footnote 12 To incentivize the questions related to time preferences in our experiment, we had to make sure that the transaction costs did not affect the subject’s choices (Kirby & Santiesteban, 2003). For instance, when making a choice between immediate and a later payment, subjects might prefer an immediate payment to avoid returning to the lab to collect the real incentive (in case they win). To avoid such factors from affecting the subject’s choices, all questions were essentially a choice between two prospects paid in the future. This is the reason for estimating CE tomorrow (and not today) for all future payments. The future amount to be paid was shown to the subjects and kept within an envelope at the INSEAD-Sorbonne lab in Paris. The subjects were also given a receipt that they can use to claim their payment after the payment date. To ensure uniform transaction cost, we also required all subjects to come back to the lab to claim their incentive.

3.3 Procedures

The experiment lasted 45 minutes on average. Subjects were told at the beginning that there were no right or wrong answers and that the experimenters were interested only in their true preferences. The experiment was carried out by three experimenters through a series of individual interviews. To ensure consistency of instructions, the same video was used to explain the instructions to all subjects across different interview sessions. The experiment consisted of three sections as described before: The questions in section I were a choice between sure outcomes paid sooner or later. The questions in section II were a choice between sure outcomes and risky prospects (both paid tomorrow). The questions in section III were a choice between sure outcomes paid tomorrow and risky prospects paid in the future.

In all the three sections, the subjects can choose one of the options or express indifference between them. For section I questions, after each choice, the smaller sooner amount was varied (using the bisection method) until the subject expressed indifference between both the options and the certainty equivalence (CE) of the future sure payment was computed. In section II and III, the sure outcome paid tomorrow was varied (using the bisection method) until the subject expressed indifference and the certainty equivalence (CE) of the risky prospect was computed. After each question, based on the answers to bisection method questions, we provided a prefilled choice list to the subject and asked them to verify their choices. The choice list tabulates the subject’s choices (based on the bisection method) between different levels of sure outcomes and the prospect. The subjects can modify their choices in the choice list and the CE was computed based on the final indifference (or switching) point in the choice list. Using both bisection method and choice list, not only allows making choices easier for the subjects, but it also avoids error propagation that is common in the bisection method (Wakker & Deneffe, 1996). For an overview of the bisection method and choice list approach we adopted, please refer to the Appendix A.

3.4 Validity of measurement

To ensure valid responses, we included dominance and consistency checks. The subjects were given a choice between larger sooner amount and a smaller later amount. The subjects who chose the smaller later amount were classified as violating dominance. In addition, one of the questions in each section was repeated (i.e., asked twice). Subjects who answered similarly to both the questions were classified as consistent.

3.5 Questions

We elicited certainty equivalents for the prospects in Table 1. The prospects in Table 1 were paid at time t and the CE is elicited at time T (\(t>T)\). The t and T in Table 1 correspond to month of payment and the month at which the CE is elicited (respectively). The \(t=0,2,4\) corresponds to outcomes paid tomorrow, 2 months from tomorrow or 4 months from tomorrow (respectively). The CEs of first four prospects (section I) enable measuring time preferences. The CEs elicited tomorrow for prospects \(5,\ldots ,14\) (section II and III) with different time delays (\(t=0,2,\) and 4 months) enable estimating Eq. (1) and characterizing risk preferences and risk-time preferences interaction. In addition, for prospects paid at \(t=4\), we also elicited the CE at \(T=2\). The CE elicited for 44 prospects allowed estimating different decision models described in Sect. 2.

3.6 Results

3.6.1 Data validity

There was no dominance violation but 12 subjects violated consistency checks. Out of these 12 subjects, three subjects who exhibited extreme choice inconsistencies were dropped from further analysis. The results below focus on the remaining forty seven subjects only.

3.6.2 Analysis of certainty equivalents

We indicate the CEs of prospects \(1,\ldots ,4\) by \(z_{1},\ldots ,z_{4}\). We indicate the CEs elicited at time \(T=0\) (tomorrow) for prospects \(5,\ldots ,14\) with different time delays (\(t=0,2,\) and 4 months) by \(z_{5}^{t},\ldots ,z_{14}^{t}\).

Time preferences.

The CEs \(z_{1},\ldots ,z_{4}\) allow us to measure time preferences and evaluate if they are non-stationary. Time preferences are not stationary when the degree of impatience varies depending on the time of elicitation. For instance, a subject exhibits hyperbolic discounting (or strong decreasing impatience) if the CE elicited for the same time delay decreases when the CE is elicited in the future. In other words, the subject is impatient when comparing payments in near future but becomes more patient when comparing payments far in the future. A subject is hyperbolic discounting if \(z_{4}-z_{3}>0\). Present bias (weak decreasing impatience) is a sub-case of hyperbolic discounting and it implies disproportionate preference for immediate payments. A subject is present biased if \(z_{4}-z_{1}>0\). Another commonly found anomaly is sub-additive discounting (Read, 2001), which implies that discounting over a delay is greater when the delay is divided into subintervals than when it is left undivided. Sub-additive discounting implies that \(z_{1}\times z_{4}<100\times z_{2}\) (for a power utility). The Table 2 classifies the subjects based on non-stationarity in their time preferences. We find that a significant proportion of subjects exhibit sub-additivity (p-value = 0.05). There was no significant evidence for predominance of subjects with present bias or hyperbolic discounting.

Risk preferences.

The certainty equivalents (CE) of prospects \(i=5,\ldots ,14\) (from Table 1) for delay \(t=0\) (indicated by \(z_{i}^{0})\) are computed in Table 3. Note that the first five prospects \((5,\ldots ,9)\) have different outcomes but fixed probability (\(p=0.25\)). The next five prospects \((10,\ldots ,14)\) have fixed outcomes (0 and 100), but the probability is varied from \(0.05,\ldots ,0.95\). When the probability is fixed at \(p=0.25\) and the outcomes are varied (prospects \(5,\ldots ,9)\), the subjects are risk seeking in aggregate (meaning the mean certainty equivalent is greater than expected value) for 3 out of 5 prospects (except prospect 5 and 6). When the outcome is fixed and the probabilities are varied (prospects \(10,\ldots ,14\)), consistent with literature (Kahneman & Tversky, 1979), the subjects are risk seeking for small probabilities \((p=0.05)\) but risk averse for intermediate and large probabilities \((p\ge 0.25)\). Table 13 in the Appendix B discusses the proportion of risk averse and risk seeking subjects for each question. As expected, subjects are majorly risk averse for seven out of ten prospects.

Risk and time preferences interaction.

The certainty equivalents (CE) of prospects \(i=5,\ldots ,14\) (from Table 1) for different time delays \(t=0,2,4\) (indicated respectively by \(z_{i}^{0}\), \(z_{i}^{2}\), and \(z_{i}^{4}\)) are computed in Table 4. As future payments are discounted, we expect \(z^{0}>z^{2}>z^{4}\). A 3 \(\times\) 10 ANOVA test with repeated measures rejected the null hypothesis that certainty equivalents are not influenced by the time delay (p-value = 0.002). A one-way ANOVA test with repeated measures failed to reject the null hypothesis that certainty equivalents are not influenced by the time delay only for prospect \(i=10\). In the paired t-tests we find that, certainty equivalent for prospects paid at time \(t=0\) (\(z^{0}\)) is significantly higher than the certainty equivalents of prospects paid at time \(t=2,4\) (\(z^{2}\) and \(z^{4}\)), for seven out of ten prospects. However, the \(z^{2}\) is significantly higher than \(z^{4}\) only for one out of the ten prospects. The result suggests that the subjects are less sensitive to time delays in the future.

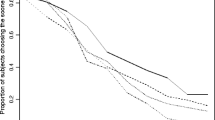

To understand more precisely the effect of probability on sensitivity to time delay, we now compare the certainty equivalents of the prospects \(10,\ldots ,14\) for different delays t. We can observe from Fig. 1 and paired t-tests reported in Table 5 that \(z^{0}\), \(z^{2},\) and \(z^{4}\) are not significantly different from one another for small probabilities (\(p=0.05,0.25\)). However, for intermediate and large probabilities \((p\ge 0.5)\), the certainty equivalents become significantly different. Thus, the results indicate that the sensitivity to time delay depends on probabilities: Subjects are less sensitive to time delay for small probabilities (especially when comparing two future payments) but become progressively more sensitive to time delay for intermediate and large probabilities. The subsequent sections will estimate the model in Eq.(1) to capture the risk-time preferences interaction.

Mean certainty equivalents for different probabilities of winning € 100. Note: The vertical lines are the standard error bars

3.6.3 Estimating Eq. (1)

Utility function.

The Eq. (1) assumes that the utility u of outcomes does not vary with the time of payment. Below, we estimate the utility function u of Eq. (1) and test if different utility functions \(u_{t}\) are required to explain choices for different time delays.

Utility function of Eq. (1).

The utility function u in Eq. (1) can be constructed using the certainty equivalent elicited for prospects \(i=5,\ldots ,9,11\) in Table 1. Note that, the six prospects have probabilities fixed but outcome varying, this makes the utility elicitation task easier. A prospect \(i=5,\ldots ,9,11\) in Table 1 pays outcome \(x_{i}\) with probability 0.25 and outcome \(y_{i}\) with probability 0.75. The certainty equivalents of the prospects \(5,\ldots ,9,11\) are indicated by \(z_{5}^{0},\ldots ,z_{9}^{0},z_{11}^{0}\). By equating the elicited CE to Eq. (1), we can construct the utility function u. The utility function u minimizes \(||z_{i}^{0}-u^{-1}((w_{0}(0.25)(u(x_{i})-u(y_{i}))+u(y_{i})))||\) for \(i=5,\ldots ,9,11\). Other studies have used similar approaches to estimate utility under nonexpected utility framework (Abdellaoui et al., 2011a, b, c). We assume a power parametric specification for the utility function i.e., \(u(x)=x^{\alpha }\) for \(\alpha >0\), \(u(x)=ln(x)\) for \(\alpha =0\), and \(u(x)=-(x^{\alpha })\) for \(\alpha <0\), which implies constant relative risk aversion (CRRA) (see Wakker, 2008, 2010). Table 6 provides the mean and median power parameters \((\alpha )\) of the utility function.Footnote 13 The mean and median power parameters indicate that the utility function u is concave. Consistent with the literature, major proportion of subjects (73%) have concave utility.

Utility function for two and four month delays.

In this sub-section, we check if different utility functions are required for different time delays. In order to do that, we assume that the utility function in Eq. (1) varies with time delay t, indicated by \(u_{t}\). We construct the utility function for delays \(t=2,4\) by using the certainty equivalents \(z_{i}^{t}\) elicited tomorrow for prospects \(i=5,\ldots ,9,11\) and the utility function u elicited for zero time delay. The utility function \(u_{t}\) minimizes \(||z_{i}^{t}-u^{-1}((w_{t}(0.25)(u_{t}(x_{i})-u_{t}(y_{i}))+u_{t}(y_{i})))||\) for \(i=5,\ldots ,9,11\) and \(t=2,4\). Table 7 lists the mean, median, and standard deviation of the utility function parameters for two and four month delay. Figure 2 plots the cumulative distribution of power parameters of the utilities. A one-way ANOVA test with repeated measures did not reject the null hypothesis of the stationarity of the utility for different time delays (p-value\(=0.61\)). Paired t-tests also show that there is no difference in the power parameter of utilities for different time delays (p-values > 0.35). Thus, the utility from future payments did not differ from the utility from immediate payments.

Empirical distribution of utility powers

Probability-time interaction.

In the previous section, we showed that the utility of outcomes for different time delays are not different from each other. This and our model free evidence suggests that the risk-time interaction might be due to the interaction between probability and time delay. To understand the nature of the interaction, we estimate the probability weight \(w_{t}\) in Eq. (1) without any parametric assumptions.

Estimating the probability weighting.

The certainty equivalents \(z_{i}^{t}\) elicited for prospects \(i=10,\ldots ,14\) allows estimating the probability weights without any parametric assumptions. The probability weight \(w_{t}\) for probabilities \(p=0.05,\ldots ,0.95\) is given by \(w_{t}(p)=\frac{u(z_{i}^{t})}{u(100)}\) for \(i=10,\ldots ,14.\) Table 8 lists the probability weights. We can observe that mean \(w_{0}\) is inverse-s shaped, it overweights small probabilities (\(p=0.05\)) and underweights intermediate and large probabilities (\(p>0.25\)). Table 9 compares the difference between probability weights for different time delays. A 3 \(\times\) 5 ANOVA test with repeated measures rejected the null hypothesis that probability weights are not influenced by the time delay (p-value = 0.0001). We also did a one-way ANOVA with repeated measures to test if time delay affects the probability weights for different probability levels. We find that for small probabilities (\(p\le 0.25\)), the time delay has no effect on probability weights (p-value = 0.22). However, for large probabilities (\(p\ge 0.5\)), the time delay has a significant effect on probability weights (p-value=0.003). The paired t-tests reported in Table 9 also supports the conclusion. Thus, consistent with our model free evidence, we observe that subjects are insensitive to time delay for small probabilities but become progressively more sensitive to time delay as the probability of gain increases. Figure 3 plots the mean probability weight w with standard error bars for different probabilities.

Mean probability weights for different time delays

Thus, we estimated the parameters of source function model in Eq. (1) and characterized the risk-time preferences interaction with minimal parametric assumptions. Our results show that there is no interaction between utility and time delay, but there is a significant interaction between probability and time delay: subjects are insensitive to time delay for small probability of gains but become progressively more sensitive to time delay as probability of gain increases. In the next section, we compare the fit of axiomatic models described in Section 2 to our data. The model fitting exercise will help us understand the best way to model risk and time preferences.

4 Parametric model fitting

We estimate the models described in Section 2 using maximum likelihood by assuming normally distributed standard errors (see Appendix C for details). For the model fitting exercise, we assume u is of power parametric specification and weighting function w is a Prelec two-parameter weighting function (Prelec, 1998) i.e., \(w(p)=e^{(-\beta (-log(p))^{\gamma })}\), where \(\beta \ge 0\) captures probabilistic pessimism (elevation of weighting function) and \(0\le \gamma \le 1\) captures the sensitivity to probabilities (steepness of weighting function). To estimate the parameters of PTT (without the magnitude effect M), we extend the model to two non-zero outcome prospects in the Appendix C. In fact, RSU generalizes PTT to multiple outcome prospects by also taking into account the magnitude effect. We consider two specifications for the discount rate \(r_{x,y}\) in the RSU model i.e., \(r_{x,y}=r_{0}+M/x\) and \(r_{x,y}=r_{0}+M/(x+y)\). The RSU model with \(r_{x,y}=r_{0}+M/(x+y)\) fits the data better and it is reported in Table 10. The RSU model with other specifications for discount rate \(r_{x,y}\) are reported in Appendix C.Footnote 14Footnote 15 A positive M indicates that the larger outcomes have smaller discount rates (magnitude effect). We estimate the WTU model by extending it to two non-zero outcome prospects (see Appendix C for details) and by parameterizing the utility function parameter \(\alpha\) to vary with time delay: \(\alpha (t)=\alpha +Kt\). A negative value for K indicates that subjects have more concave utility for outcomes paid in the future.

Aggregate level results.

The aggregate level results are reported in Table 10. We compare the model based on the Akaike information criterion (AIC). Lower the AIC, better the model fits the data taking into account the number of parameters in the model. We can observe that models that assume no risk-time preferences interaction (DEU and DRDUFootnote 16) have a high AIC and therefore does not fit the data very well. In fact, the PTT model without the magnitude effect parameter and the Halevy (2008) model, which capture the risk-time interaction, fit the data better than DEU and DRDU. Our results also shows that accounting for magnitude effect is important: RSU and WTU have a better fit than Halevy and PTT without magnitude effect (PTT*). One more important observation from Table 10 is that the monthly discount rate becomes smaller when we start accounting for the risk-time preferences interaction.

Individual level results.

The individual level results are reported in Tables 11 and 15 (Appendix C). Consistent with aggregate level results, we can observe that the mean log-likelihood is highest for models (RSU and WTU) that capture risk-time preferences interaction and account for the magnitude effect. Also, note that the parameters estimated at individual level are closer to aggregate level results. In the case of RSU model, although the mean discount rate for a month is extremely low, it is compensated by a higher value for the magnitude effect parameter M. The trimmed mean \(M=3.2\), implies that for the sum of outcome ranges considered in our experiment [25, 175], the mean monthly discount rate is \(10.9\%\;(12.8\%-1.8\%)\) higher for a prospect whose sum of outcomes equals 25 compared to a prospect whose sum of outcomes equals 175. Estimating Halevy (2008) model also allowed us to calibrate the mortality risk (that the payment will not be received) in our experiment. The median mortality risk is extremely low (less than \(0.01\%\)). We also find that the parameter K of the WTU model is negative indicating that utility function becomes more concave for future payments.

In addition, for each of the 47 subjects, we compared the models pairwise based on the degree of fit (AIC). Pairwise comparisons prevent similar models competing for the same subjects from crowding out each other (Kothiyal et al., 2014). We find that RSU model (followed by WTU) performs best in all pairwise-comparisons (see Table 15 Appendix C for more details).

5 Follow-up study

In order to replicate the results of the experiment, we conducted a follow-up study with 198 subjects (47% Female, Age \(\sim ~23\)). The study was conducted online and our subjects were Master in Management (MIM) students of IE Business School in Madrid, Spain. We elicited CEs of the 198 subjects using bisection method for 28 prospects with different outcomes, probabilities, and time of payment. The prospects were a subset of the 44 prospects used in Table 1. As the study was conducted online, we reduced the number of questions to make the task easier for the subjects. However, the CEs elicited for the 28 prospects were sufficient to replicate the core findings of our first experiment. All participating subjects received class credits for participation, in addition 5% of the subjects received amazon vouchers based on their choices. For more details on the study logistics, refer to Appendix E.

We replicated the results of the first experiment in the follow-up study and provide a stronger statistical evidence: As in the first experiment, (1) subjects predominantly exhibit sub-additive discounting. In addition, they are risk seeking for small probabilities and risk averse for large probabilities of gains. (2) our model free evidence based on certainty equivalence (in Figure 8, Appendix E) shows that, subjects are insensitive to future time delays for small probabilities \((p\le 0.5)\). However, for large probabilities \((p>0.5)\), subjects are more sensitive to time delays. (3) We find that the the utility of the subjects is unaffected by time delay (Table 17, Appendix E). However, the time delay significantly impacts the probability weights as in the first experiment i.e., the probability weights are insensitive to time delay for small probability of gains but become progressively more sensitive to time delay as the probability of gain increases (Fig. 9 and Table 21, Appendix E). (3) Finally, we fit the models in Section 2 to all the 198 subjects. We find that models that account for risk-time preferences interaction and account for the magnitude effect fit the data better than other models (see Table 22 in Appendix E). For more details on the results, refer to Appendix E.

6 Discussion and conclusions

Our main experiment and the follow-up study allowed us to measure the risk preferences, the time preferences, and the risk-time preferences interaction. First we focus on the model free evidence based on certainty equivalents (CEs). We find that significantly higher proportion of our subjects are sub-additive (Read, 2001), but we do not find a significant evidence for predominance of subjects with decreasing impatience. Other studies in the literature that controlled for sub-additive discounting also find a similar proportion of decreasingly impatient subjects (e.g., Halevy, 2015). The risk attitudes of our subjects are consistent with the findings in literature (Abdellaoui et al., 2011c). Our subjects are risk seeking for small probabilities and risk averse for intermediate and large probabilities.

Focusing on the risk-time preferences interaction, we find that the certainty equivalents of a prospect for different time delays are not significantly different from one another for small probabilities (\(p=0.05,0.25\)). However, for intermediate and large probabilities, the certainty equivalents become significantly different. Thus, our results indicate that subjects are less sensitive to time delay for small probabilities of gains but become progressively more sensitive to time delay for intermediate and large probabilities of gains. Previous experimental studies have shown that a time delay produces the same effect as reduction in probability. They have explored how changes to the probability of receiving outcomes affect the non-stationarity in time preferences (Keren & Roelofsma, 1995; Baucells & Heukamp, 2010; Andreoni & Sprenger, 2012). Here, we show that the time preferences (discount rates) themselves may depend on the outcome probabilities. In fact, our results imply that, in many contexts such as public lotteries or start up investing, where the probability of winning is small, the time delay of receiving the outcomes will matter less. Therefore, a start-up offering a large gain with small chance far into the future might be valued higher than an equivalent start-up offering a slightly smaller gain with the same chance, earlier. On the other hand, when we consider investments where the gains are likely, e.g., returns from highly rated government bond investments, the time delay of receiving the outcomes will matter more.

Our results also aid in understanding how a DM incorporates time delay into his valuations: does the time delay interact with the utility (taste) of outcomes or does it interact with the probabilities (likelihood judgement)? In our experiment, we find that there is no interaction between the utility and time delay. However, we find that there is a significant interaction between probability and time delay: For small probabilities (\(p\le 0.25\)), the weighting functions for different delays cannot be separated from one another. Only for intermediate and large probabilities, the weighting functions become significantly different from one another. These result confirms our earlier conclusion on probability-time interaction based on observing only the CEs and also points to the fact that, subjects in our experiment might have treated the future payments as inherently risky (Halevy, 2008; Baucells & Heukamp, 2012). However, this does not mean that utility and time delay does not interact with one another in real world decision making. As pointed out in Gerber and Rohde (2018), changes to the baseline consumption can affect the utility received from future payments. In our experiment, as the outcome size and time delay is small (maximum delay of 4 months), the changes to baseline consumption may not have been very apparent to the subjects.Footnote 17

In addition, the nature of probability-time interaction we observed also has implications for modeling. For instance, Baucells and Heukamp (2012) assume the probability-time trade-off axiom, which implies constant trade-off between probability and time delay for a specific outcome size. The insensitivity to time delay under small probabilities, would imply that dividing the probabilities of two prospects by the same constant \(\theta \in [0,1]\) might break the indifference between the prospects and shift the preference towards the prospect with larger probability. We observe that \(72\%\) of our subjects have such preference in our experiment that violates the probability-time trade-off axiom (see Appendix D for details). Andreoni and Sprenger (2012) also find similar common ratio violations in their experiment. These findings imply that future models should relax the PTT axiom and modify the parametric specification \(w(pe^{-rt})\) for the probability-time interaction function (Baucells & Heukamp, 2012).

Finally, we fit the existing decision models to our data and compare them. We find that models that assume no risk-time interaction (DEU and DRDU) perform poorly compared to models that assume risk-time interaction. This confirms our earlier finding that risk-time preferences interaction should be taken into account while building models. Our results also show that models that capture probability-time interaction and account for magnitude effect (RSU, WTU) perform better than other models at both the individual and the aggregate level. Considering the significance of magnitude effect, policy makers should be careful in choosing the outcome size for eliciting time preferences in the field. Another important insight from our model fitting exercise is that, the monthly discount rate becomes smaller when we account for risk-time preferences interaction. Previous studies have shown that controlling for utility curvature and probability weighting is important in estimating discount rates (Andersen et al., 2008; Attema et al., 2010; Abdellaoui et al., 2019). We show that, in addition, policy makers and decision analysts should take into account the risk-time preferences interaction while estimating discount rates capturing “pure” time preferences.

To sum up, the contribution of the paper is three fold. First, we develop an experiment to provide clean model free evidence on how DMs combine outcomes, probabilities, and time delays into their valuation. We show that DMs are insensitive to time delay for small probability of gains, but become progressively more sensitive to time delay as the probability of gain increases. Second, we use a simple model to show that time delay affects mainly the probability processing. Third, we compare the fit of existing axiomatic decision models that capture risk and time preferences. We show that models which capture risk-time preferences interaction and account for the magnitude effect best fits our data. We also replicate the results in a follow-up study.

Notes

Prelec and Loewenstein (1991) showed that there are many parallels between the impacts of risk and time preferences on decision making.

The model is based on the axiomatic system developed by Chew and Epstein (1990) that extends non-expected utility to temporal prospects.

Magnitude effect implies that people are more patient when discounting larger outcomes.

Andreoni and Sprenger (2012) focus on common ratio property as applied to intertemporal risk and show that different alternatives to DEU cannot explain the observed choices. In contrast, our study does not focus on a specific property but explores in more general how risk and time preferences interact with each other by estimating different decision models and comparing them.

We use the terms “time of payment” and “time delay” interchangeably. All models discussed in the section focus on the present value of the prospect, therefore time of payment corresponds to time delay.

For prospect \(L_{2},\) this can be inferred by substituting \(w_{t}=\delta ^{t}p\) into the more general form of Eq. (1) described above.

Note that, although, RSU agrees with PTT when evaluating value (or certainty equivalent) of a single outcome prospect, range effects may intervene in RSU when comparing two single outcome prospects.

The sooner payment was not paid immediately but tomorrow, to ensure the transaction costs were similar for both the choices.

We used colored coins as a substitute for the colored balls that were used in the experimental stimuli

If the subject was chosen to receive real incentive, then one of the questions was randomly selected. For that specific question, one of the choices in the choice list was randomly selected and the uncertainty (if any) was resolved immediately by picking a coin from a box consisting of different colored coins. The subjects were paid on the specific date based on their choices and the resolved uncertainty.

The results are for forty four subjects. For three subjects, the algorithm did not converge.

We estimate the RSU model by assuming \(S(t)=pe^{-rt}\).

The parameters of RSU are also elicited for an alternate specification of the discount rate \(r_{x}=r_{0}\left[ 1+\frac{M}{x}\right]\) in Table 14, Appendix C.

We also estimated the hyperbolic discounted rank dependent utility (HDRDU) model, but the estimated AIC was higher than the DRDU model.

In fact, when we consider all 44 prospects and estimate the WTU model, the K parameter is negative indicating the dependence of utility on time of payment.

References

Abdellaoui, M., Baillon, A., Placido, L., & Wakker, P. P. (2011a). The rich domain of uncertainty: Source functions and their experimental implementation. American Economic Review, 101, 695–723.

Abdellaoui, M., Diecidue, E., & Öncüler, A. (2011b). Risk preferences at different time periods: An experimental investigation. Management Science, 57, 975–987.

Abdellaoui, M., Kemel, E., Panin, A., & Vieider, F. M. (2019). Measuring time and risk preferences in an integrated framework. Games and Economic Behavior, 115, 459–469.

Abdellaoui, M., L’Haridon, O., & Paraschiv, C. (2011c). Experienced vs. described uncertainty: Do we need two prospect theory specifications? Management Science, 57, 1879–1895.

Akaike, H. (1998). Information theory and an extension of the maximum likelihood principle. In Selected papers of hirotugu akaike (pp. 199–213). Springer.

Allais, M. (1953). Le comportement de l’homme rationnel devant le risque: Critique des postulats et axiomes de l’école américaine. Econometrica, 21, 503–546.

Anderhub, V., Güth, W., Gneezy, U., & Sonsino, D. (2001). On the interaction of risk and time preferences: An experimental study. German Economic Review, 2, 239–253.

Andersen, S., Harrison, G. W., Lau, M. I., & Rutström, E. E. (2008). Eliciting risk and time preferences. Econometrica, 76, 583–618.

Andreoni, J., & Sprenger, C. (2012). Risk preferences are not time preferences. American Economic Review, 102, 3357–76.

Attema, A. E., Bleichrodt, H., Rohde, K. I., & Wakker, P. P. (2010). Time-tradeoff sequences for analyzing discounting and time inconsistency. Management Science, 56, 2015–2030.

Baucells, M., & Cillo, A. (2019). The intuitive present value of cash flows. Working Paper.

Baucells, M., & Heukamp, F. H. (2010). Common ratio using delay. Theory and Decision, 68, 149–158.

Baucells, M., & Heukamp, F. H. (2012). Probability and time trade-off. Management Science, 58, 831–842.

Baucells, M., Kontek, K., & Lewandowski, M. (2018). Range and sign dependent utility for risk and time. Working Paper.

Chapman, G. B., & Elstein, A. S. (1995). Valuing the future: Temporal discounting of health and money. Medical Decision Making, 15, 373–386.

Cheung, S. L. (2015). Risk preferences are not time preferences: On the elicitation of time preference under conditions of risk: comment. American Economic Review, 105, 2242–60.

Chew, S. H., & Epstein, L. G. (1990). Nonexpected utility preferences in a temporal framework with an application to consumption-savings behaviour. Journal of Economic Theory, 50, 54–81.

Epper, T., Fehr-Duda, H., & Bruhin, A. (2011). Viewing the future through a warped lens: Why uncertainty generates hyperbolic discounting. Journal of Risk and Uncertainty, 43, 169–203.

Fishburn, P. C., & Rubinstein, A. (1982). Time preference. International Economic Review, 23, 677–694.

Fox, C. R., & Tversky, A. (1995). Ambiguity aversion and comparative ignorance. The Quarterly Journal of Economics, 110, 585–603.

Gerber, A., & Rohde, K. I. (2018). Weighted temporal utility. Economic Theory, 66, 187–212.

Halevy, Y. (2008). Strotz meets allais: Diminishing impatience and the certainty effect. American Economic Review, 98, 1145–1162.

Halevy, Y. (2015). Time consistency: Stationarity and time invariance. Econometrica, 83, 335–352.

Ida, T., & Goto, R. (2009). Simultaneous measurement of time and risk preferences: Stated preference discrete choice modeling analysis depending on smoking behavior. International Economic Review, 50, 1169–1182.

Kahneman, D., & Tversky, A. (1979). Prospect theory: An analysis of decision under risk. Econometrica, 47, 263–291.

Keren, G., & Roelofsma, P. (1995). Immediacy and certainty in intertemporal choice. Organizational Behavior and Human Decision Processes, 63, 287–297.

Kirby, K. N., & Santiesteban, M. (2003). Concave utility, transaction costs, and risk in measuring discounting of delayed rewards. Journal of Experimental Psychology: Learning, Memory, and Cognition, 29, 66.

Kontek, K., & Lewandowski, M. (2017). Range-dependent utility. Management Science, 64, 2812–2832.

Kothiyal, A., Spinu, V., & Wakker, P. P. (2014). An experimental test of prospect theory for predicting choice under ambiguity. Journal of Risk and Uncertainty, 48, 1–17.

Kreps, D. M., & Porteus, E. L. (1978). Temporal resolution of uncertainty and dynamic choice theory. Econometrica, (pp. 185–200).

Laibson, D. (1997). Golden eggs and hyperbolic discounting. The Quarterly Journal of Economics, 112, 443–478.

Loewenstein, G., & Prelec, D. (1992). Anomalies in intertemporal choice: Evidence and an interpretation. The Quarterly Journal of Economics, 107, 573–597.

Loewenstein, G., & Thaler, R. H. (1989). Anomalies: Intertemporal choice. Journal of Economic perspectives, 3, 181–193.

Miao, B., & Zhong, S. (2015). Risk preferences are not time preferences: Separating risk and time preference: Comment. American Economic Review, 105, 2272–86.

Noussair, C., & Wu, P. (2006). Risk tolerance in the present and the future: An experimental study. Managerial and Decision Economics, 27, 401–412.

Prelec, D. (1998). The probability weighting function. Econometrica, 66, 497–527.

Prelec, D., & Loewenstein, G. (1991). Decision making over time and under uncertainty: A common approach. Management Science, 37, 770–786.

Quiggin, J. (1982). A theory of anticipated utility. Journal of Economic Behavior & Organization, 3, 323–343.

Read, D. (2001). Is time-discounting hyperbolic or subadditive? Journal of Risk and Uncertainty, 23, 5–32.

Tversky, A., & Kahneman, D. (1992). Advances in prospect theory: Cumulative representation of uncertainty. Journal of Risk and Uncertainty, 5, 297–323.

Wakker, P. (2010). Prospect Theory for Risk and Ambiguity. Cambridge University Press.

Wakker, P. P. (2008). Explaining the characteristics of the power CRRA utility family. Health Economics, 17, 1329–1344.

Wakker, P., & Deneffe, D. (1996). Eliciting von Neumann-Morgenstern utilities when probabilities are distorted or unknown. Management Science, 42, 1131–1150.

Weber, B. J., & Chapman, G. B. (2005). The combined effects of risk and time on choice: Does uncertainty eliminate the immediacy effect? does delay eliminate the certainty effect? Organizational Behavior and Human Decision Processes, 96, 104–118.

Acknowledgements

We thank Manel Baucells, Enrico Diecidue, Matthias Seifert, Konstantinos Stouras for their helpful comments on this draft of the paper. We also thank Mohammed Abdellaoui, Ehud Lehrer, and Bob Nau for their helpful comments during the different stages of the project. We acknowledge the help rendered by INSEAD Sorbonne lab research assistants Hoai Huong Ngo and Jean-Yves Mariette with the data collection. We also gratefully acknowledge support from the People Programme (Marie Curie Actions) of the European Union’s Seventh Framework Programme FP7/2007-2013/ under REA grant agreement 290255 and HEC Paris.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher’s Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Supplementary Information

Below is the link to the electronic supplementary material.

Rights and permissions

Springer Nature or its licensor holds exclusive rights to this article under a publishing agreement with the author(s) or other rightsholder(s); author self-archiving of the accepted manuscript version of this article is solely governed by the terms of such publishing agreement and applicable law.

About this article

Cite this article

Somasundaram, J., Eli, V. Risk and time preferences interaction: An experimental measurement. J Risk Uncertain 65, 215–238 (2022). https://doi.org/10.1007/s11166-022-09394-9

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11166-022-09394-9