Abstract

Audits provide monitoring for investors. The collapse of markets across the financial crisis made assets more difficult to value, which increased risk for auditors. The money markets were at the center of the financial crisis increasing audit engagement risk on money market funds, which at the time of the crisis were highly opaque. Measuring the response to increased engagement risk with audit fees, this study finds that auditors increase their fees for the riskiest class of funds. However, no evidence was found that audit fees increased as funds increased their holdings in the riskiest class of securities.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

The financial crisis shocked markets. Specifically, financial markets stopped functioning normally meaning that the value of assets became more difficult to determine. Thus, the financial crisis created concerns for investors, stress for fund managers and risk for auditors. Doogar et al. (2015) note that large scale empirical studies on auditors’ ability to identify shifts in risk are lacking because events that trigger business environment and business risk changes are rare. The financial crisis is one of those rare events. The increase in auditor engagement risk should be followed by increases in auditor fees associated with the sources of the increased risk. In this paper, we examine if audit fees increased during the financial crisis for mutual fund portfolios with more audit risk from difficult-to-value assets and for specific high-risk, difficult-to-value assets.

Money markets were at the center of the financial crisis. Money markets stopped functioning normally, making values difficult to determine. Money markets funds (MMFs) invest in money market securities. At the time of the crisis MMFs were highly opaque, as regulation only required detailed portfolio reports every 6 months.Footnote 1 Thus, MMFs provide a natural experimental setting to determine if auditors responded to the increased risk during the financial crisis and responded to the more difficult to value assets.

We examine Prime MMFs for increased audit fees during the financial crisis. Prime MMFs were at the center of the financial crisis because of their substantial holdings in commercial paper. During the crisis, the commercial paper market collapsed making commercial paper more difficult to value due to the decline in market information, which increased audit engagement risk.Footnote 2 Additionally, Prime MMFs hold asset-backed commercial paper (ABCP) which are illiquid complex securities that were of specific concern during the financial crisis. Covitz et al. (2013) note that in the summer of 2007 the ABCP market began to plummet with the proximate cause being the default risk of mortgages. ABCP lacked market data during the crisis generating specific audit engagement risk concerns because ABCP provides funding to mortgage-backed securities.

Our benchmark for increased audit fees in Prime MMFs is Government MMFs audit fees. Government MMFs focus on liquid and easy to value securities. We expect to find an increase in audit fees in Prime MMFs relative to fees in Government MMFs. We also expect to find an increase in relative audit fees in Prime MMFs that hold more ABCP.

We find audit fees increased for Prime MMFs during the financial crisis suggesting that auditors did respond to the general increase in audit risk. This result is consistent with previous literature.Footnote 3 However, we find that audit fees do not appear to increase relative to holdings of ABCP. This suggests that auditors did not respond to the specific risk of this complex security at the center of the financial crisis. This result is counter to our general results and counter to expectations. Finding a lack of audit fee response to ABCP holdings is an important contribution.

One of our contributions is the use of Prime MMFs to examine audit engagement risk, which we believe we are the first to examine. Prime MMFs provide a natural experiment for two reasons. First, over 85% of Prime MMFs assets under management have the potential of audit engagement risk through valuation concerns during the financial crisis. Second, Government MMFs are governed by the same rules and regulations as Prime MMFs and therefore provide a control group that varies from Prime MMFs in their exposure to valuation concerns. About 67% of the assets held by Government MMFs are not subject to valuation concerns during the financial crisis.

Our results contribute to what is known about credit evaluation during the crisis. On average and over time, credit rating agencies have done a reasonable job measuring the default risk of bonds. However, during the financial crisis, the credit rating agencies did a poor job measuring the default risk of mortgage-backed securities. Doogar et al. (2015) suggest that auditors possess the ability to address increased risk from changing economic conditions, while Sikka (2009) questions auditor’s ability to identify and address increased risk. Our results suggest that auditors understand risk where they have a history of work and were able to identify changes in risk during the financial crisis in these areas. However, our results also suggest that auditors do not have unique insights into new risks.Footnote 4 Our results support the move by the AICPA to provide certification for valuation specialists that have expertise in valuing hard-to-value assets.

2 Background

In response to the financial crisis, regulators warned auditors that there would be extra scrutiny over the quality of audits and audit procedures to safeguard the audit process. Additionally, the Public Company Accounting Oversight Board (PCAOB) warned audit firms that the PCAOB would be closely monitoring audit firms to prevent them from decreasing the rigor of audits during the crisis (Goelzer 2010).Footnote 5

Subsequent to the financial crisis, PCAOB Chairman James Doty testified before a U.S. Senate committeeFootnote 6 in April 2011 and stated: “… accounting firms must do a better job of addressing in their audits the risk of misstatements in financial statements that emerge as economic conditions change.” Doty’s testimony continued with some specific concerns about auditing standards. These remarks include:

-

focus auditor attention on issues arising from mortgage and foreclosure activities,

-

risk assessment standards which are critical to providing investors a fair understanding of matters that became important during the financial crisis, such as valuation of complex securities, and

-

fair value issues arising from deficiencies related to insufficient evidence from auditors when using third party pricing sources to value financial instruments.

During the same Senate hearing, FASB Chairman Seidman (2011) testified on the role of the FASB. This testimony included a discussion of fair value accounting and its clarification provided under SFAS 157.Footnote 7 Chairman Seidman commented on the difficulty of determining the fair valueFootnote 8 of illiquid assets.Footnote 9 The difficulty of correctly valuing these assets increases the importance of a quality audit.

SFAS 157 defines value determination for auditors. SFAS 157 defines three levels of fair value: Level 1 is quoted prices in active markets, Level 2 is other than quoted prices supported with observable market data, and Level 3 is estimated prices from unobservable inputs from the best available data. The financial crisis is called a ‘financial’ crisis because financial markets collapsed. The collapse of some markets caused the use of unobservable inputs in determining fair values. The different levels create different risks and approaches from auditors to determine the value of assets.

In this section, we discuss the specific audit risks in MMFs during the financial crisis and why MMFs are an appropriate experimental setting for testing whether auditors identified and responded to the increased engagement risk.

2.1 Audits, auditors, and risk

Auditors provide credibility to the financial statements and reduce the risk that information is materially misstated (Sridharan et al. 2002). When fair value is more difficult to determine, the risk of material misstatements increases.

Audit engagement risk to the auditing firm represents potential litigation costs, reputational damage, and regulatory penalties. Reputational damage and litigation costs come when the market loses confidence in the ability or reliability of the auditing firm in determining if financial statements reasonably represent the condition of the firm.Footnote 10

Audit engagement risk includes audit risk which comes from issuing an unqualified or “clean” audit opinion on financial statements that are materially misstated. Audit risk is a function of inherent and control risk. Inherent risk comes from the possibility that the assets of the firm have unstable values, which can lead to impairment. Control risk represents risks from internal controls and valuation procedures from the firm’s management team.Footnote 11 Both of these risks increased during the financial crisis. If auditors realized an increase in audit engagement risk, they are expected to respond, which should increase audit fees.

An increase in audit engagement risk should bring about an increase in audit effort.Footnote 12 First, audit firms can contract more man-hours to the project to ensure the validity of the audit resulting in more billed hours. Second, audit firms can send higher level (and thus higher paid) auditors or audit specialists to conduct the audit.Footnote 13 Either response to the increased risk is expected to lead to higher audit fees.Footnote 14 An alternative response is for audit firms to simply accept the additional risk and increase audit fees to compensate for the additional risk. However, charging higher fees while not addressing the underlying risk is not consistent with the professional standards from PCAOB.

2.2 Why prime MMFs?

Audit engagement risk includes inherent risk from the possibility that the assets of the firm have unstable values and control risk from valuation procedures from the firm’s management team. During the financial crisis, segments of the money markets collapsed creating unstable values requiring the management of MMFs to use different valuation procedures. However, there are different categories to MMFs, so in this section we discuss why Prime MMFs are our treatment group while Government MMFs are our control group.

Money market funds have three distinct categories: (1) Prime, (2) Government, and (3) Tax-free.Footnote 15 Tax-Free MMFs are not included because of the special tax treatment of these funds. Prime and Government MMFs are taxable funds that operate under the same regulations but focus holdings in different categories of securities. Here, we discuss the different categories of securities, how the different holdings create different levels of auditor engagement risk, and how relative engagement risk changed during the financial crisis.

Prime MMFs focus their investments in short-term private-issue debt while Government MMFs focus their investments in T-bills and repos on T-bills. The typical securities held by Prime MMFs are certificates of deposit (CDs), commercial paper (CP), asset-backed commercial paper (ABCP), and floating rate notes (FRnotes). Private-issue debt contains default risk, while T-bills do not. There is not an active secondary market in any of the private-issue securities from which to observe prices, while there is an active secondary market in T-bills including throughout the financial crisis. The short-term maturities of the private-issue securities create an active market in new issues. Private-issue securities are not level 1 assets because they lack active secondary markets and instead, are level 2 assets when markets function normally. To determine prices for end-of-day portfolio values, Prime MMFs use third party specialists to estimate the value of these securities.

Commercial paper is the largest category of assets held by Prime MMFs (see Table 1). There are three primary types of CP: non-financial, financial and ABCP. Kacperczyk and Schnabl (2010) report that in January of 2007 the CP market mix was: non-financial at 5.8% of the market, financial at 34.4% of the market, and ABCP at 56.8% of the market. Financial CP is unsecured debt of financial institutions. With financial institutions at the heart of the financial crisis, the financial CP market declined dramatically moving financial CP from a level 2 asset to a level 3 asset.Footnote 16

ABCP is typically issued by off-balance sheet conduits of financial institutions. ABCP was particularly risky at the time of the crisis through exposure to mortgage defaults. With the mortgage market in collapse during the crisis, the ABCP market collapsed moving ABCP from a level 2 asset to a level 3 asset. As an example, on August 9, 2007, BNP Paribus halted redemptions on three MMFs because they could not determine the fair value of the ABCP in the funds.Footnote 17

The private-issue securities held by Prime MMFs are directly exposed to the audit engagement risk concerns of the PCAOB and the FASB, while T-bills are not. Here we restate the risks outlined above from the 2011 Senate committee hearing with a statement (in italics) on why Prime MMFs audit risk increases during the crisis.

-

misstatements in financial statements that emerge as economic conditions change (the commercial paper market collapsed during the crisis moving CP from a level 2 asset to a level 3 asset),

-

issues arising from mortgage and foreclosure-activities (ABCP provides funding to mortgage-backed securities),

-

valuation of complex securities (ABCP are complex securities by design),

-

fair value issues arising from third party pricing (MMFs use third party pricing specialists),

-

fair value accounting and difficulty of determining the fair value of illiquid assets (commercial paper markets stopped functioning normally during the crisis moving private-issue securities from level 2 assets to level 3 assets).

Government MMFs focus their investments in T-bills and repos on government securities, which are typically T-bills. T-bills are default free and actively trade in a secondary market, which continued to function properly across the financial crisis. T-bills are level 1 assets. Accordingly, there is little doubt in the value of these securities. Repos on T-bills have little default risk. Repos do not trade in a secondary market, so third party specialists are used to determine value. The quality of the collateral on these repos allows repos held in Government MMFs to be level 2 assets.Footnote 18 Neither T-bills nor repos on T-bills change fair value levels during the financial crisis.

Given the focus of the securities held in Government MMFs, their auditors have little exposure to engagement risk. Additionally, Government MMFs are not exposed to the engagement risk concerns of the PCAOB and the FASB during the financial crisis. Thus, we use Government MMFs as our control group.

2.3 Hypotheses

We examine if increases in engagement risk during the financial crisis lead to increases in audit fees for risky MMFs (Prime MMFs) and risky securities (ABCP). We test two hypotheses.

H1

Audit fees for Prime MMFs increased significantly relative to Government MMFs during the 2007–2009 financial crisis.

At the time of the financial crisis, Prime MMFs were the largest purchasers of ABCP. With the collapse of the ABCP market audit engagement risk increased, which is expected to require more involved and extensive audits.

H2

Audit fees increased significantly during the financial crisis (2007 through 2009) for MMFs holding asset backed commercial paper (ABCP).

There is some literature on level 3 assets and audit fees. Ettredge et al. (2014a; b) find that audit fees in the banking industry are higher with more Level 2 and 3 assets in their portfolios in a sample period (2008–2011) that includes the financial crisis. However, over 75% of the banks in their sample have zero level 3 assets, which suggests this result may be driven by outliers. In addition, in regressions that include controls for banking industry auditor specialists the interaction of auditor specialist and level 3 assets is insignificant. Goncharov et al. (2014) find audit fees increase with exposure to more difficult to value assets in a sample period (2001–2008) that includes the financial crisis. They group level 2 and level 3 together as difficult to value because level 2 and level 3 assets do not have market values.

We examine the increase in audit fees related to changes from level 2 to level 3 in valuation levels of the private-issues securities held by Prime MMFs, in general, and specifically with ABCP. We examine if auditors were able to identify the changing risk.

We examine Prime MMFs for increased audit fees during the financial crisis. This implies that we can differentiate the crisis from the pre-crisis period. Accordingly, we provide a brief discussion of the pre-crisis period from a sample of the literature related to MMFs. McCabe (2010) notes that prior to the financial crisis sponsor risk and investor risk appears to be unimportant in MMFs and shows that Prime assets under management increase in the pre-crisis period. Kacperczyk and Schnabel (2013) examine MMFs during the financial crisis and show that prior to the middle of 2007 MMF yields, growth rates, and asset mix are relatively stable. Covitz et al. (2013) show that prior to the middle of 2007 spreads and amounts outstanding in ABCP are relatively stable followed by dramatic breaks in August of 2007. Gorton and Metrick (2012) note that in August 2007 mortgage problems begin to spill over into repos and ABCP. Finally, money market securities are substitutes for short-term banks loans. Cyree et al. (2016) show that commercial loans as a percentage of total assets for banks are stable across the pre-crisis period. Accordingly, the literature suggests a stable pre-crisis period followed by a significant break during the financial crisis. We examine if the break caused by the financial crisis results in higher audit fees for Prime MMFs and for Prime MMFs holding ABCP.

2.4 Confounding events: regulatory changes that change audit responses

Regulatory changes can have dramatic effects on audits and audit fees. In this section we briefly discuss regulatory changes that may impact audit activity for MMFs.

We begin with the list of major GAAP changes provided in Shroff (2017) for changes that could impact audit risk in MMFs. Shroff provides a list of 30 changes during his sample period of 1991 through 2007. Most clearly do not relate to audits on MMFs. Three changes in the Shroff list could impact audit response for MMFs: SFAS 159, FIN 46(r), and SFAS 115. However, FIN 46(r) and SFAS 115 do not change during our sample. We discuss SFAS 159 briefly below.

SFAS 159 covers the fair value option for financial assets and liabilities and is effective for fiscal year-ends following November 15, 2007. However, it could be implemented in fiscal year 2007 if the entity also elects to apply the provisions of SFAS 157. SFAS 159 allows entities to choose to measure financial assets and liabilities at fair value, which include all the assets held by MMFs. This has the potential to change the audit fees of many entities, but not MMFs because they update the value of all assets daily to current market price, which is fair value. Accordingly, SFAS 159 does not change MMF audit practices.

SFAS 157 expands disclosures about the use of fair value and is effective for fiscal year-ends following November 15, 2007. The disclosures focus on inputs used to determine fair value and for recurring fair value using unobservable inputs. Unobservable inputs are used when there is little, if any, market activity (Level 3). Most money market securities seldom, if ever, trade, but the short-term nature of the money market creates an active market for new issues and thus, provides market data for level 2 valuation. MMFs use third party specialists to analyze the market and provide estimates of market value. Under SFAS 157 there will be more disclosure of this process required, which should increase audit fees across all MMFs.

Additionally, we review FASB SFAS statements, AICPA SAS and professional standards, and PCAOB alerts. In the interest of brevity, we state that our analysis did not identify any regulatory changes that would change audit risk on MMFs.

In addition to accounting and auditing regulations there are regulations that govern MMFs. Specifically, rule 2a–7 of the Investment Company Act of 1940 defines the necessary conditions for mutual funds that wish to operate as money market mutual funds. Prior to the financial crisis, the last change to rule 2a–7 occurred in 1997. Rule 2a–7 was modified in February 2010 in response to the financial crisis. Additional changes to address the financial crisis were approved in July 2014, which is after the end of our sample.

The 2010 changes to rule 2a–7 were designed to reduce risk and improve liquidity. A reduction in risk could reduce audit engagement risk in the post-crisis period. However, Akay et al. (2015) conclude that the 2010 changes did little to change the risk of securities held in Prime MMFs.

Our review of regulatory changes across our sample leads us to conclude that there were no major regulatory changes during our sample that would change the relative engagement risk between our treatment group (Prime MMFs) and our control group (Government MMFs). Accordingly, there are no control variables in regression models for any regulatory regime changes.

3 Data and models

The data for this study come from two primary sources: iMoneyNet and the Securities and Exchange Commission form N-CSR. The sample runs from 2004 to 2013. By starting in 2004, we begin after Sarbanes Oxley (SOX) was fully implemented.

MMF data comes from iMoneyNet. We gather identifying and holdings information, such as the portfolio composition and fund category, for individual funds from 2004 to 2013 for Prime MMFs and Government MMFs.

Audit fee data comes from the Securities and Exchange Commission (SEC) document N-CSR. The N-CSR is an SEC document that funds are required to file. The N-CSR is an annual filing that contains audit fees at the Central Index Key (CIK) level. The CIK number is a filing identification number assigned by the SEC. The CIK number is not necessarily designated at the individual fund level. This made hand collection of fund level fees necessary as some fund families file multiple funds under the same CIK. Our final sample only includes funds for which we can identify fund level audit fees through the N-CSR and we collect all the available fee data. We collect and analyze audit fees at a fund level. Additionally, auditor and fund audit information come from Audit Analytics. This dataset was matched with fund data using the CIK.

All datasets are combined to form a sample of 235 unique MMFs covering 1459 fund years. Table 1 reports statistics separately for Prime MMFs and Government MMFs. We start each panel with annual sample counts and the percentage of the population for each year. Panel A reports statistics for the Prime MMFs. Annually, our sample of Prime MMFs ranges from 72 to 106 funds, which represents 34–43% of the iMoneyNet population of Prime MMFs. The annual count of Prime MMFs declines post crisis. Our sample of Prime MMFs assets under management ranges from 41 to 58% of iMoneyNet population assets under management. This suggests that the Prime MMFs reporting audit fees are somewhat larger than average for assets under management. Panel B starts with these summary statistics for Government MMFs. Annually, our sample of Government MMFs ranges from 47 to 61, which represents from 21 to 40% of the iMoneyNet population of Government MMFs. There is no decline in the number of Government MMFs post crisis. Our sample of Government MMFs assets under management range from 16 to 37% of the iMoneyNet population of Government MMFs. This suggests that the Government MMFs reporting audit fees are somewhat smaller than average for assets under management. This basic sample description suggests that our sample is reasonably representative of the population. Specifically, our sample of funds that report audit fees are not just the largest funds among Prime and Government MMFs.

The remainder of the panels in Table 1 provide summary statistics for the sample. Table 1 shows that Prime funds are substantially larger than Government funds in terms of total assets. Prime funds pay higher audit fees, but larger funds should have more expensive audits, in general. Prime funds have higher annual yields, which is consistent with investing in higher risk securities. Prime funds have higher expense ratios, which is consistent with Prime funds being more actively managed. Prime and Government funds are similar in age and WAM (weighted average maturity, in days). Similar WAMs suggest that neither type of fund is stretching maturities to increase risk. Prime funds have one manager in about 56% of their fund years while Government funds have two managers in about 56% of their fund years.

3.1 MMF holdings and audit fees

Table 1 also reports portfolio compositions by fund type and shows very different portfolio compositions between Prime funds and Government funds. Government MMFs hold 28.45% in Treasuries and 38.80% in repos. Prime MMFs use the entire spectrum of allowable securities but focus on the riskier private-issue securities. The largest average portfolio position in Prime MMFs is in commercial paper (31.82%). Next, Prime funds hold 18.24% of their portfolios in FRnotes (floating rate notes) and 10.30% in FBOs (foreign bank obligations). Neither are typically described as money market securities.

Holdings in ABCP are the focus in Hypothesis 2: do Prime MMF audit fees increase with larger holdings in ABCP. Table 1 shows that, on average, Prime MMFs hold 10.20% of their portfolios in ABCP, which leads us to ask if this level of ABCP exposure is material to audit fees. Reserve Primary broke the buck and ultimately closed during the financial crisis from a 1.2% exposure to short-term Lehman debt at the time of Lehman’s bankruptcy. Consequently, the average ABCP position in Prime MMFs represents sufficient exposure to be of concern during the financial crisis.

Prime MMFs hold an average of 10.2% of their assets in ABCP across the sample, but the sample average does not provide information about holdings during the financial crisis. So, we calculate the average portfolio position of Prime MMFs in ABCP by year across the sample to determine fund exposure to ABCP across the crisis. The average annual ABCP position prior to the crisis is in excess of 10% with the peak annual average at 13.5% in 2007, the first year of the crisis. Across the crisis the average annual holdings decline to 11.1% in 2008 and 6.8% in 2009. Following the crisis, the annual average rebounds in 2010 to 8.7% and remains at roughly 8% annually for the remainder of our sample. The average annual holdings suggest that during 2007 and 2008 Prime MMFs had above sample average holdings while 2009 was the annual average minimum for our sample. The annual averages show that Prime MMFs had sufficient exposure in ABCP across the financial crisis to warrant increased audit resources.

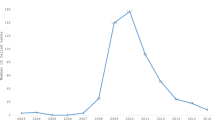

Having demonstrated Prime MMFs’ exposure to risky securities we move to plots of audit fees. Figure 1 plots mean and median audit fees by year for Prime MMFs and Government MMFs. The plot provides four important insights. First, Prime MMFs, as a group, pay higher audit fees across years, which is expected as Prime MMFs are larger and riskier. Second, mean audit fees for Prime funds peaked in 2009 while mean fees on Government funds were flat in 2009. Government MMFs show an uptick in mean audit fees in 2008. Third, median audit fees show a positive drift from 2006 to 2008. This increase could be the result of SFAS 157. SFAS 157 becomes effective for fiscal year-ends after November 15, 2007. SFAS 157 requires additional disclosures from auditors of MMFs. Finally, mean audit fees for Prime MMFs return to pre-crisis levels in 2010, which is consistent with the abatement of the crisis risk on Prime MMFs.

This graph shows the mean and median audit fee for Prime funds and Government funds

Figure 1 shows a spike up in mean audit fees for Government MMFs in 2008 and Prime MMFs in 2009. This raises the question about outliers influencing the means. Accordingly, Fig. 2 shows a scatter plot of the MMF audit fees used in the study. Government funds are in the left pane while Prime funds are in the right. The X-axis is the audit year, while the Y-axis is the audit fee. These fees are not transformed and show the dollar amount charged to the individual MMFs. There is a clear outlier in 2008 in Government MMFs. There is also a large outlier in 2009 in Prime MMFs. Additionally, there is a grouping of higher audit fees for Prime MMFs from 2007 through 2009 suggesting the possibility of higher crisis audit fees for risker Prime MMFs.

This figure shows a scatterplot of the audit fees charged to individual money market funds for each audit year. The Y-axis represents the dollar amount charged. The X-axis is the audit year. The figure is separated into two sections. The left pane represents Government money market funds. The right pane shows the audit fees for prime money market funds

To limit the effect of these few extreme outliers on our analysis, we transform the data using the natural log of the audit fees charged to the funds. We use the natural log of audit fees charged to MMFs as the dependent variable for all regressions. This transformation both limits the effect of extreme outliers and provides a reasonable economic explanation of the coefficients from the regressions.

3.2 Regression model

In this section, we present the full model used to test our hypotheses. We will estimate different specifications of the model using OLS. The dependent variable for all regressions is the natural log of audit fees [Ln (Audit Fees)].Footnote 19 In each regression, we cluster standard errors by fund. The full model is as follows:

3.2.1 Test variables

The first test variable is Prime: Prime equals 1 for Prime MMFs and equals zero for Government MMFs. Prime is our general proxy for engagement risk. Prime and Government MMFs are governed by the same set of regulations, so the functional difference between the two types of funds is the classes of securities on which they focus.

The second set of test variables are the crisis years: 2007, 2008, and 2009. The variables 2007, 2008, and 2009 are dummy variables, which have the value of one if the audit occurred in the corresponding year. Therefore, 2007, 2008, and 2009 allow us to test whether audit fees are higher during the financial crisis than in non-crisis years. To test for increased engagement risk in Prime MMFs during the financial crisis, we interact the Prime dummy with the test variables of 2007, 2008, and 2009. These interactions test Hypothesis 1.

The next set of test variables are portfolio Holdings.Footnote 20 The variables for the Holdings of the funds are represented by each security class and allow for tests of increased audit fees on riskier assets. The Holdings variables are the percentage of assets under management held in each security calculated at the fund level.

The security holdings allow us to test Hypothesis 2. Specifically, we want to determine if auditors charge higher fees for Prime MMFs that hold more ABCP during the financial crisis. These tests will require interaction terms between Prime, ABCP, and 2007, 2008, and 2009.

3.2.2 Control variables

Audit fees are a function of client size, complexity, and engagement risk. Table 1 shows that Prime MMFs are larger in size than Government MMFs. We control for size of the MMF in all regressions with Ln(Assets) of the MMF. Table 1 also shows that Prime MMFs focus their investments in different securities than Government MMFs. The differences in securities allow us to use Government MMFs as a benchmark for complexity and audit engagement risk. Therefore, our baseline regression includes Ln(Assets) and the Prime dummy variable along with the crisis years’ dummy variables.

Table 2 provides the distribution of audit years and provides a number of important insights. First, the Big 4 audit firms account for more than 96% of the audit years in our sample. Second, MMF audits are dominated by the Big 4 and that there is not a dominate specialist among the Big 4 for MMFs.Footnote 21 In addition to the auditor counts reported in Table 2, we examine the frequency of auditor changes. Our sample contains 1459 fund years, and we find a total of 33 auditor changes across the sample. Eight of the auditor changes occurred during the financial crisis with six changes in Prime MMFs and two changes in Government MMFs. This suggests that MMFs are not auditor shopping, in general, and specifically not during the financial crisis. Following the audit fee literature, we use auditor fixed effects (Auditor Controls) to control for the auditing firm. We use a dummy variable for each of the Big 4 firms.

We include two additional controls for risk in MMFs. McCabe (2010) suggests that MMFs that are affiliated with banks were more likely to engage in risky behavior. We use a dummy variable (Bank affiliated) with the value of one if the MMF is affiliated with a bank. Roughly one quarter (27%) of the funds in the sample are affiliated with a bank. Also, longer-term securities are riskier. WAM is the asset-weighted number of days until portfolio maturity. We use WAM as a second control for MMF risk.

Finally, the literature on audit fees typically includes some additional controls.Footnote 22 We use MMF gross annual yield (Yield) as a control for performance. We use the MMF expense ratio (Expense) as a control for efficiency. Along with the expense ratio, we include the number of fund managers (Managers) as another control for efficiency. Goldie et al. (2018) include a control for fund age. We include MMF age (Age), which we measure as years from inception. Goncharov et al. (2014) include a year-end dummy variable that aligns with the audit busy season to capture higher audit fees when resources are constrained. Ireland and Lennox (2002) define the audit busy season as December 1 through March 31. We follow this definition and include a busy season (Busy) dummy variable that equals 1 during the busy season.Footnote 23

Before estimating the regression model, we examine the correlations between the variables. The pairwise correlations in Table 3 use the full data sample. An asterisk identifies if the two variables are correlated at the 1% level. Examination of the correlations between variables provides a preliminary look at how all the variables interact.

In the top of the first column, assets and audit fees have a 38% positive correlation significant at a 1% level. This finding supports previous literature as asset size has been shown as a driver of audit fees.

Hypothesis 2 asks if holdings of ABCP associate with higher audit fees during the financial crisis. Table 3 suggests that holdings in ABCP are not significantly positively correlated with audit fees. This lack of correlation is not consistent with Hypothesis 2.

T-bills and repos are negatively correlated with CP and ABCP. This finding is consistent with funds holding a relatively risky portfolio being less likely to hold T-bills and repos. T-bills and repos are also negatively correlated with audit fees, which is consistent with these assets requiring less audit resources to determine fair value and therefore lower audit fees.

4 Analysis

We ask, did auditors increase audit fees during the financial crisis and if so, was the increase in fees focused on the most difficult to value assets? This section of the paper is our empirical analysis of these research questions.

4.1 Baseline regression analysis: prime versus government funds

Our full sample is 235 unique MMFs covering 1459 fund years. We use all the data for our baseline regressions. We address the outliers in audit fees by using the natural log of audit fees as our dependent variable.

Hypothesis 1 provides the first research question of this study; did audit fees increase during the crisis? Accordingly, our model includes the crisis years’ dummy variables (2007, 2008, and 2009). The full sample includes both Prime and Government MMFs, so the model includes the dummy variable Prime. A comparison of the two types of funds should reveal whether auditors responded to the funds with more audit engagement risk.

Table 4 presents two different models (without and with interaction terms). Column 1 of Table 4 shows the parameter estimates on the test variables 2008 and 2009 are significant and positive, as is, the parameter estimates on the variable Prime. The parameter estimates of Prime in column 1 suggest that Prime MMFs, on average, have audit fees approximately 20% higher than Government funds.

Column 2 of Table 4 reports results with interactions between Prime and the crisis dummy variables (2007, 2008, and 2009). This model also includes the addition of auditor fixed effects. The interactions are the first direct tests of Hypothesis 1 on whether Prime funds saw an increase in audit fees relative to Government funds during the years of the financial crisis. The Prime coefficient continues to be significant and positive and shows an approximately 15% difference between audit fees in Prime MMFs and Government MMFs. This finding is consistent with the previous model in column 1. The variable Prime*2008 is significant and positive at the 5% level. The positive coefficient of 0.104 suggests an audit fee increase of approximately 10% between Prime and Government funds in 2008. This loading suggests that the average audit fee of over $35,000 for Prime funds increased by $3500 more than Government funds during the peak of the crisis, 2008. The variable Prime*2009 is not significant. Recall, that Table 1 shows that the 2009 sample of Prime MMFs declined by about 18%, but Fig. 1 shows Prime MMF average audit fees are highest in 2009. In the next section, we re-visit 2009 in Prime MMFs with a more direct test. Overall, Table 4 supports Hypothesis 1 and confirms that Prime fund audits resulted in increased fees during the heart of the financial crisis in 2008.

Models reported in Table 4 includes all our control variables, and the results on these variables provide some interesting insights. Ln (Assets) is significant and positive suggesting the larger funds pay higher audit fees. Fund age has a significant and positive parameter estimate. This is consistent with older funds being larger and more complex. The audit busy season dummy variable (Busy) is significant and negative. This suggests that MMFs pay lower audit fees during the busy audit season. Based on previous literature, this result is not as expected. Auditor fixed effects increases the model explanatory power by about 33%. Finally, Bank affiliated MMFs pay higher audit fees. McCabe (2010) suggests that bank affiliated MMFs engage in risky behavior and we find that these funds pay higher audit fees after identifying Prime MMFs and crisis years. This suggests that we may not have fully defined audit risk for MMFs, so we take a closer look at this result.

McCabe defines distressed ABCP has ABCP held by a MMF that receives sponsor’s support and he assumes that MMFs receiving sponsor support are more risky. He finds that bank affiliated MMFs are more likely to receive sponsors support and concludes that bank affiliated MMFs have been engaging in risky behavior. However, McCabe also finds no association between bank affiliated MMFs and his other measures of risk. With these mixed results from McCabe in conjunction with our positive parameter estimate, we examine our bank affiliated MMFs.

As we noted above in the discussion of control variables, bank affiliated MMFs are about 27% of our sample and almost all the bank affiliated MMFs in our sample are Prime MMFs. Following from McCabe we need to determine the bank affiliated MMFs that received sponsor support and we find that 5.73% of the bank affiliated MMF years have sponsor support with 2/3 of the support occurring during the crisis (11 crisis period sponsor support among 90 bank affiliated crisis fund years). Using the sub-sample of bank affiliated MMFs we re-estimate our baseline regressions from Table 4 with the inclusion of a sponsor support dummy variable. The sponsor support dummy variable is insignificant in all specifications of the model. These results suggest that sponsor support does not lead to higher audit fees and therefore is not a proxy for risk in our sample.

McCabe thinks bank affiliated MMFs engage in risky behavior in the form of holding distressed ABCP. Next, we examine the portfolios of bank affiliated MMFs to determine if these funds hold more ABCP than non-bank MMFs. We find that during the pre-crisis period that bank affiliated MMFs hold substantially less ABCP than their non-bank counter parts. In 2007, median holdings of ABCP for bank affiliated MMFs is 1% of total assets while the median holdings for non-bank MMFs is 10%. In 2008 non-bank funds drop ABCP to a median of 4% of total assets while bank affiliated MMFs increase to a median of 14% of total assets.Footnote 24 In 2009 both groups show a reduction in median holdings of ABCP. Following that crisis, both groups add holdings in ABCP and both settle at a median of 7% of total assets in the last year of our sample (2013). The median ABCP held by each group across our sample years shows that neither group consistently held more ABCP and therefore neither group consistently held a more risky portfolio.

McCabe concludes that bank affiliated MMFs engage in risky behavior based on sponsor’s support and holdings in ABCP. Our sample of bank affiliated MMFs has limited instances of sponsor support and has portfolios that do not systematically hold more ABCP. We conclude that the significant and positive parameter estimate on the bank affiliation dummy variable is not related to risk. Agency costs offer a possible explanation for this result, but exploring this explanation is beyond the scope of this paper and will be left to future research.

The primary focus of this study is on the audit fees charged to Prime MMFs. The findings in Table 4 support that Prime funds paid higher audit fees and paid higher audit fees during the heart of the crisis (i.e., in 2008). Audit fees were increased, however the specific assets driving the increase in fees is unknown at this point.

4.2 Fund holdings

The results in Table 4 show Prime MMFs pay higher audit fees during the financial crisis. Prime MMFs hold securities that are more difficult to value. These securities are expected to require more auditor attention to certify value. With an increase in incentives to “get it right”, we expect to find a positive correlation between more difficult to value securities and audit fees.

Table 5 presents the regression results on only Prime MMFs and aims to directly address Hypothesis 2. The regressions reported include the specific asset categories. Column 1 of Table 5 reports that Prime funds continue to show above average audit fees in 2008 and 2009. The results in column 1 include all the specific types of securities, and all of the parameter estimates are insignificant. This finding suggests that auditors did not associate additional fees with a specific type of asset.

Column 2 reports Prime MMF results adding interaction terms between 2007, 2008, and 2009 and ABCP. The 2008 and 2009 coefficients continue to be positive and significant. The crisis parameter estimates in Column 2 suggests auditors increased audit fees by approximately 12–20% for these Prime MMFs over the peak years of the crisis in 2008 and 2009. This finding signals that auditors did understand that Prime funds needed more auditor attention throughout the crisis. However, the purpose of this model is to determine if the auditors charge higher fees to Prime funds holding more ABCP during the financial crisis. The parameter estimates on all the interaction terms are insignificant. These results suggest that during the financial crisis auditors did not increase fees for Prime MMFs based on holding this difficult to value and complex security with exposure to mortgages. These results combined with earlier results suggest that audit fees increased for Prime MMFs as the money markets collapsed causing their securities to move from level 2 to level 3 assets without focused attention on the most complex and difficult to value securities within those funds.

In both regressions in Table 5 the parameter estimate of bank affiliated MMFs continues to be significant and positive, as in our baseline regressions. As noted above, that bank affiliated Prime MMFs added ABCP in 2008. Accordingly, we re-estimate the models in Table 5 without the bank affiliated variable. All the results on ABCP, including the interactions, remain insignificant.

Our results suggest that auditors did increase audit fees during the height of the crisis but not based on the level of ABCP holdings within a Prime fund. More complex level 3 securities, such as ABCP, are expected to involve higher audit fees. This expectation is especially true during the financial crisis when auditors faced increased pressure to “get it right.”

4.3 Dif-in-Dif analysis

Our baseline regressions use the entire sample with control variables suggested by the audit fee literature. This approach is subject to concerns about omitted variables. Dif-in-Dif analysis provides a method to address the omitted variable concerns. In this section, we re-examine our baseline results using two different Dif-in-Dif matched samples.

4.3.1 Matched sample with treatment MMFs surviving entire sample period

We begin the matching process by identifying the set of Prime MMFs that survive the entire sample period (2004 through 2013). We find 38 Prime MMFs that exist in each of these 10 years. We match each Prime MMF with a Government MMF using propensity scores on total assets, WAM and age.

With the matched sample we revisit Fig. 1 for the appearance of higher Prime MMF audit fees during the financial crisis. Figure 3 plots trend lines for the average difference in audit fees between the treatment group fund (Prime MMFs) and the matched control group fund (Government MMFs). The first panel plots the trend for the pre-crisis period (years 2004, 2005 and 2006). The pre-crisis period trend line is basically flat. The second panel plots the trend for the crisis period (years 2007, 2008 and 2009). The crisis period trend is upward sloping. The trend line analysis suggests a change in the difference in audit fees between Prime and Government MMFs during the financial crisis with Prime MMF (treatment) audit fees increasing relative Government MMF (control) audit fees.

This figure uses the propensity score matched sample to generate two fitted value trend lines with 95% confidence intervals. The trend lines represent the difference in fees between a prime fund and its propensity score matched government fund. The pre-period represents the three years before the crisis. The crisis-period represents the three years during the height of the crisis

4.3.2 Regression analysis: matched sample treatment MMFs surviving entire sample period

With our matched sample trend lines showing increasing Prime MMF audit fees relative to Government MMF audit fees during the crisis period, we can move to our Dif-in-Dif sample regression analysis. We will re-visit our regressions from Tables 4 and 5 with some adjustments to fit the Dif-in-Dif analysis. We report the results in Table 6 and use data from the entire sample period (2004 through 2013).

Column 1 of Table 6 contains only the Prime dummy and year dummy variables for the pre-crisis period (2004, 2005, and 2006) and the crisis period (2007, 2008, and 2009). The post crisis year dummy variables (2010, 2011, 2012 and 2013) are omitted and thus are contained in the intercept. We also omit Ln (Assets) as it was one of the variables used in the matching process. Column 1 reports that the parameter estimate on Prime is insignificant suggesting that in our matched sample that Prime and Government MMFs pay similar audit fees. In the crisis years, only 2009 has a significant parameter estimate and it is positive, which is consistent with higher audit fees in this year. All parameter estimates on the pre-crisis year dummy variables (2004, 2005, and 2006) are significant and negative, which is consistent with pre-crisis audit fees being lower than post-crisis audit fees.

Column 2 adds the Prime MMF and crisis years’ interactions to the variables used in column 1. All the interaction parameter estimates are insignificant. These results suggest that in this matched sample Prime MMF audit fees do not increase during the crisis relative to Government MMF audit fees. These results are inconsistent with the results from our baseline regressions.

Column 3 has Big 4 auditor fixed effects in addition to the variables used in column 2. The auditor fixed effects substantially increase the explanatory power of the model. However, the auditor fixed effects do not change the results on any of our test variables. The Prime dummy and all the crisis years’ interaction remain insignificant.

These Dif-in-Dif results are very different from the results in our baseline regressions. Dif-in-Dif tests are designed to address omitted variables, which may suggest that our baseline regressions have some omitted variables. However, an alternative explanation may exist. We suggest that Prime MMFs create engagement risk for auditors during the financial crisis and specifically that the engagement risk is when assets could be mis-valued hiding ‘break-the-buck’ MMFs. In this Dif-in-Dif analysis, our sample of Prime MMFs are 38 Prime funds that survive across the entire sample, including four post crisis years. Surviving across all years suggests that auditors of this set of Prime MMFs is likely exposed to little, if any, engagement risk.

As a final point of this Dif-in-Dif analysis, the 38 surviving Prime MMFs include the single audit fee outliers in 2007 and 2008 and the two audit fee outliers in 2009. This point suggests that the difference in results from our baseline regressions and the regressions from this Dif-in-Dif analysis is not related to a change in outliers.

4.3.3 Regression analysis: matched sample treatment MMFs surviving pre-crisis period

Our first Dif-in-Dif analysis required Prime MMFs to survive the entire sample period. In this Dif-in-Dif analysis we require that the treatment sample of Prime MMFs must only survive across the pre-crisis period. This will increase the treatment sample, and this sample will include Prime MMFs that closed or merged during the crisis or post-crisis period. The MMFs that close or merge may expose their auditors to engagement risk, which should cause higher audit fees. We match this set of Prime MMFs with Government MMFs through propensity matching based on total assets, WAM and age.

Table 7 reports the regression results for the second matched sample. The first three columns of Table 7 report the same regression models as Table 6 for comparison.

Column 1 of Table 7 reports results that are similar to Table 6 column 1, as audits fees are higher than average in 2009 and lower than average in 2004, 2005, and 2006. However, in Table 7 we see the Prime MMF audit fees are significant and positive, which suggests that Prime MMFs pay higher audit fees than a matched sample of Government MMFs.

Column 2 of Table 7 adds the Prime and crisis years’ dummy variables interactions to the variables reported in column 1. All the interaction parameter estimates are significant and positive, which suggests that Prime MMFs pay higher audit fees than Government MMFs during the years of the financial crisis. This result is counter to our first Dif-in-Dif analysis, but it is consistent with our baseline regressions. Column 3 includes auditor fixed effects with the variables in column 2. The auditor fixed effects substantially increase the explanatory power of the model, but little changes among the Prime and year dummies. These results continue to support that Prime MMFs pay higher fees, on average, and pay higher fees during the financial crisis.

The results reported in column 4 include fund control variables, as in our baseline regressions, with Prime, year dummies, and interactions. Adding the control variables more than doubles the explanatory power of the model. The results in column 4 continue to support that Prime MMFs pay higher fees, on average, and pay higher fees during the financial crisis. The control variables bank affiliated and busy, are significant as in the baseline regressions with the same signs.

The results reported in column 5 include variables for fund holdings with Prime, year dummies, interactions, and control variables. As in our baseline regressions, none of the fund holdings variables are statistically significant. The results in column 5 continue to support that Prime MMFs pay higher fees, on average, and pay higher fees during the financial crisis.

Finally, we add various ABCP interaction terms to the model in column 5. All the ABCP interactions parameters are insignificant. This result is consistent with all our previous results on the lack of any association between ABCP and higher audit fees. We do not report these results in Table 7 in the interest of brevity, but they are available upon request.

The results from the second Dif-in-Dif analysis are consistent with our baseline regressions while the results from the first Dif-in-Dif analysis are not consistent. We state that auditor engagement risk comes, in part, from the risk of material misstatements of asset values and that this risk is particularly important in Prime MMFs during the financial crisis as the value of some money securities were in question during the crisis. A decline in portfolio values of anything more than ½ percent would break-the-buck and cause remedial action by the fund’s board (closure) or the fund’s family (sponsor support). Either would create reputational issues for the auditor that certified the value of the fund’s assets. The second Dif-in-Dif analysis allows Prime MMFs to close or merge during or after the financial crisis. We assume that Prime MMFs that closed or merged did so for a valid business reason that would cause engagement risk for the fund’s auditor. Accordingly, we believe that the matched sample that only requires Prime MMFs to survive the pre-crisis period is the appropriate sample to test for engagement risk.

5 Conclusion

The 2007–2009 financial crisis highlighted the risks associated with valuing securities when financial markets are not functioning normally. Using MMFs, this study analyzes whether independent auditors responded to the heightened risk during the crisis.

This study focuses on Prime MMFs because of their increased audit engagement risk as their assets moved from level 2 valuation to level 3 valuation. Results show that audit fees did increase for Prime funds during the financial crisis and increased more as the crisis progressed. This finding supports auditors recognized an increase in risk and responded appropriately.

Asset backed commercial paper (ABCP) was at the center of the financial crisis. ABCP is a complex and difficult to value security with exposure to the mortgage market. ABCP was held almost exclusively by Prime funds. Our analysis suggests that independent auditors did not increase fees in response to the levels of ABCP in Prime MMFs.

Doogar et al. (2015) suggest that auditors possess the ability to address increased risk from changing economic conditions, while Sikka (2009) questions auditor’s ability to identify and address increased risk. Our results suggest that auditors understood the general risk of a financial crisis but did not respond to a specific risk in this crisis. This is a common and reoccurring issue across this crisis. Our results support the recent expansion of the ABV (Accredited Business Valuation) designation by the AICPA to meet increased demands for valuation specialists to value hard-to-value assets.Footnote 25

Notes

The weighted average maturity (WAM in Table 1) is less than 45 days.

Anderson and Gascon (2009) note that heightened financial market uncertainty caused lenders to shift away from CP and into default-free securities. Commercial paper outstanding was $2.2 trillion in July 2007 at the beginning of the crisis. Commercial paper outstanding was $1.2 in December 2009 at the end of the crisis.

See Sikka (2009).

The PCAOB is a private-sector not-for-profit corporation created by the Sarbanes–Oxley act of 2002 to oversee the audits of public companies and further the public interest of accurate and independent audit reports.

Specifically, he testified on April 6, 2011 before the Senate Committee on Banking, Housing and Urban Affairs, Subcommittee on Securities, Insurance, and Investment.

SFAS 157 was issued September 2006 and began effective for fiscal year-ends after November 15, 2007.

Bell and Griffin (2012) suggest auditors face significant challenges and risks when auditing high-uncertainty fair value estimates.

Robinson et al. (2018) find that managerial discretion may have distorted values of level 3 assets held by banks.

Ball (2009) suggests that the financial crisis was the first big test for auditors under Sarbanes–Oxley.

Doty (2011) notes deficiencies related to insufficient evidence from auditors when using third party pricing sources to value financial instruments.

Goldie et al. (2018) identify PWC as an audit specialist in bond mutual funds. They find higher audit fees for bond funds associated with PWC audits. Their sample period is 2005 through 2009, which includes the financial crisis.

Doogar et al. (2015) suggests auditors had the ability to recognize changes in risk, but that limitations in regulations may have prevented them from addressing it in an appropriate manner.

MMFs typically invest in the wholesale market, which means large dollar units. Large means $1 million, which is the common unit size for negotiable CDs, repos, and commercial paper. Federal agency debt trades in $500,000 unit size. Treasury bills are the exception and trade in $100 units. The Treasury wants all investors to be able to buy its debt.

From July 2007 through December 2009, the amount of financial CP outstanding declined from $781 bil. to $593 bil., which is about a 24% decrease.

Taylor and Williams (2009) note that BNP Paribus’ halting redemptions in these funds is generally recognized as the beginning of the financial crisis. At the time of the BNP Paribus action the amount outstanding in the ABCP market was about $1.2 trillion and by August 2008 (the month before Lehman filed for bankruptcy) the amount outstanding in ABCP had declined by $500 billion (Akay et al. 2013). By the end of the financial crisis in December 2009, the amount of ABCP outstanding had declined to $452 bil., which is about a 62% decrease across the financial crisis.

Since the Lehman bankruptcy is a key event in the financial crisis, we need to mention Lehman’s use of repo 105 and repo 108 transactions. These transactions were used by Lehman to window-dress its balance sheet in the months leading up to it bankruptcy. These transactions relate to the amount of collateral Lehman provided and did not reflect general market conditions. Accordingly, this is unlikely to affect the price of other repos. See, Griffiths et al. (2012) for a discussion of these transactions.

Using the natural log of audit fees is common practice in the audit fee literature. An alternative method to natural logs to control for outliers is to winsorize the data. We estimate all of our regression models with winsorized (at various levels) dollar audit fees as the dependent variable. The winsorized data yields similar results to the natural log of audits fees. We do not report the winsorized results in the interest of brevity.

The variables are defined in “Appendix”.

Recall from footnote #13 that Goldie et al. (2018) identify PWC as an audit specialist in bond mutual funds and that as a bond audit specialist they receive higher audit fees. Their sample period is 2005 through 2009, which includes the financial crisis.

Prime funds have 39% of their audits done during the busy season, while Government funds have 34% of their audits done during the busy season.

2008 saw the TARP to bailout banks. Also, the Fed implemented AMLF to support Prime MMFs holding ABCP [see, Akay et al. (2013)] and CPFF to purchase ABCP (Fairbanks et al. 2019). This support could explain that increase in ABCP in bank affiliated MMFs, but exploring this increase is beyond the scope of this paper.

See, Wall Street Journal, 8/20/2018, CPAs fight to Protect part of the Turf.

References

Akay OO, Griffiths MD, Kotomin V, Winters DB (2013) A look inside AMLF: what traded and who benefited. J Bank Finance 37(5):1643–1657

Akay OO, Griffiths MD, Winters DB (2015) Changing rule 2a–7 and the risk profiles of money market mutual funds. J Appl Finance 25(1):15

Anderson R, Gascon C (2009) The commercial paper market, the Fed, and the 2007–2009 financial crisis. Fed Reserve Bank St Louis Rev 91(6):589–612

Asthana SC, Boone JP (2012) Abnormal audit fee and audit quality. Audit J Pract Theory 31(3):1–22

Ball R (2009) Market and political/regulatory perspectives on the recent accounting scandals. J Account Res 47(2):277–323

Bell TB, Griffin JB (2012) Commentary on auditing high-uncertainty fair value estimates. Audit J Pract Theory 31(1):147–155

Blankley AI, Hurtt DN, MacGregor JE (2012) Abnormal audit fees and restatements. Audit J Pract Theory 31(1):79–96

Covitz D, Liang N, Suarez GA (2013) The evolution of a financial crisis: collapse of the asset-backed commercial paper market. J Finance 68(3):815–848

Cyree KB, Griffiths MD, Winters DB (2016) US bank lending activity in the postcrisis world. J Financ Res 39(4):389–410

Desai H, Rajgopal S, Yu JJ (2016) Were information intermediaries sensitive to the financial statement-based leading indicators of bank distress prior to the financial crisis? Contemp Account Res 33(2):576–606

Doogar R, Rowe SP, Sivadasan P (2015) Asleep at the wheel (again)? Bank audits during the lead-up to the financial crisis. Contemp Account Res 32(1):358–391

Doty J (2011). https://www.banking.senate.gov/public/index.cfm/hearings?ID=0F533E5B-DC43-4FC2-A415-5DF2AE8806DA

Ettredge M, Fuerherm EE, Li C (2014a) Fee pressure and audit quality. Acc Organ Soc 39(4):247–263

Ettredge ML, Xu Y, Yi HS (2014b) Fair value measurements and audit fees: evidence from the banking industry. Audit J Pract Theory 33(3):33–58

Fairbanks J, Griffiths M, Winters D (2019) Financial crisis solutions in the commercial paper market. Manag Finance 22:3–22

Goelzer D (2010) Speech presented at the 2010 AICPA national conference on current SEC and PCAOB developments, Washington, DC

Goldie BA, Li L, Masli A (2018) Do mutual fund investors care about auditor quality? Contemp Account Res 35(3):1505–1532

Goncharov I, Riedl EJ, Sellhorn T (2014) Fair value and audit fees. Rev Acc Stud 19(1):210–241

Gorton G, Metrick A (2012) Securitized banking and the run on repo. J Financ Econ 104(3):425–451

Griffiths MD, Kotomin V, Winters DB (2012) A crisis of confidence: understanding money markets during the financial crisis. J Appl Finance 22(2):61–82

Ireland JC, Lennox CS (2002) The large audit firm fee premium: a case of selectivity bias? J Account Audit Finance 17(1):73–91

Kacperczyk M, Schnabl P (2010) When safe proved risky: commercial paper during the financial crisis of 2007–2009. J Econ Perspect 24(1):29–50

Kacperczyk M, Schnabl P (2013) How safe are money market funds? Q J Econ 128(3):1073–1122

McCabe PE (2010) The cross section of money market fund risks and financial crises (no. 2010–51). Board of Governors of the Federal Reserve System (US)

Robinson D, Smith T, Valencia A (2018) Does managerial opportunism explain the differential pricing of level 3 fair value estimates? J Financ Research 41(2):253–289

Seidman L (2011). https://www.banking.senate.gov/public/index.cfm/hearings?ID=0F533E5B-DC43-4FC2-A415-5DF2AE8806DA

Shroff N (2017) Corporate investment and changes in GAAP. Rev Acc Stud 22(1):1–63

Sikka P (2009) Financial crisis and the silence of the auditors. Acc Organ Soc 34(6–7):868–873

Sridharan UV, Caines WR, McMillan J, Summers S (2002) Financial statement transparency and auditor responsibility: Enron and Andersen. Int J Audit 6(3):277–286

Taylor JB, Williams JC (2009) A black swan in the money market. Am Econ J Macroecon 1(1):58–83

Xu Y, Carson E, Fargher N, Jiang L (2013) Responses by Australian auditors to the global financial crisis. Account Finance 53(1):301–338

Zhang Y, Monroe GS, Gasbarro D, Cullen G, Shailer G (2011, Aug) Asset securitizations and audit effort. In: 24th Australian finance and banking conference

Acknowledgements

The authors thank seminar participants at Western Michigan University, Louisiana Tech University, University of South Dakota and Utah Valley University for their comments. Additionally, we thank Matt Hart and Matthew Whitledge for their comments.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendix

Rights and permissions

About this article

Cite this article

Allen, K.D., Winters, D.B. Auditor response to changing risk: money market funds during the financial crisis. Rev Quant Finan Acc 56, 1057–1086 (2021). https://doi.org/10.1007/s11156-020-00918-5

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11156-020-00918-5