Abstract

Inequality evidence based on surveys, tax records, or their combination often result in divergent trends, fueling the distributional debate in Latin America. Beyond the strengths and weaknesses of these sources and their combination, tax-survey data face two shortcomings: they are unable to account for aggregate household or national income, and they are affected by firm owners’ decisions about the distribution of profits, changing which incomes researchers can actually observe. We combine social security data, household surveys and matched personal and firm tax records, which allows us to accurately account for all income sources, particularly capital incomes at the firm and individual level. Based on these unique data, we assess inequality trends in Uruguay, showing that increasing profit-distribution by firms pushes tax-survey top shares upwards, but that this trend is offset when undistributed profits are accounted for. These results call for caution when using tax-survey data without considering changes in profit-distribution.

Article PDF

Similar content being viewed by others

Avoid common mistakes on your manuscript.

Data Availability

Social Security and Tax micro-data (both for individuals and firms) are not available since they were provided to Instituto de Economía-Universidad de la República by the uruguayan tax authority Dirección General Impositiva under a non-sharing with third parties agreement. These data may be requested directly to Dirección General Impositiva.

Survey and National Accounts data is publicly available at Instituto Nacional de Estadísticas and Banco Central del Uruguay web-pages, and may be downloaded directly without any specific authorization. Survey data: https://www.ine.gub.uy/encuesta-continua-de-hogares1. National Accounts data: https://www.bcu.gub.uy/Estadisticas-e-Indicadores/Paginas/Cuentas-Nacionales-e-Internacionales.aspxhttps://www.bcu.gub.uy/Estadisticas-e-Indicadores/Paginas/Cuentas-Nacionales-e-Internacionales.aspx.

References

Alstadsæter, A., Jacob, M., Kopczuk, W., Telle, K.: Accounting for business income in measuring top income shares. In: Proceedings. Annual Conference on Taxation and Minutes of the Annual Meeting of the National Tax Association, volume 110, pp. 1–39. JSTOR (2017)

Altimir, O.: Income distribution statistics in latin america and their reliability. Rev. Income Wealth 33(2), 111–155 (1987)

Alvaredo, F.: A note on the relationship between top income shares and the gini coefficient. Econ. Lett. 110(3), 274–277 (2011)

Alvaredo, F., De Rosa, M., Flores Beale, I., Morgan, M., et al: The inequality (or the growth) we measure: data gaps and the distribution of incomes. CEPR discussion papers (2022)

Alvaredo, F., Gasparini, L.: Recent trends in inequality and poverty in developing countries. In: Atkinson, A., Bourguignon, F. (eds.) Handbook of Income Distribution, vol. 2, pp. 697–805. Elsevier (2015)

Amarante, V., Colafranceschi, M., Vigorito, A.: Uruguay’s Income Inequality and Political Regimes over the Period 1981–2010. In: Cornia, A. (ed.) Falling Inequality in Latin America. Policy Changes and Lessons, WIDER Studies in Development Economics. Oxford University Press (2014)

Arulampalam, W., Devereux, M.P., Maffini, G.: The direct incidence of corporate income tax on wages. Eur. Econ. Rev. 56(6), 1038–1054 (2012)

Atkinson, A.B., Piketty, T.: Top incomes over the twentieth century: a contrast between continental european and english-speaking countries. oup Oxford (2007)

Atkinson, A. B., Piketty, T., Saez, E.: Top incomes in the long run of history. J. Econ. Lit. 49(1), 3–71 (2011)

Blanchet, T., Chancel, L., Gethin, A.: How unequal is europe? evidence from distributional national accounts, 1980-2017. WID. world Working Paper, vol. 6 (2019)

Blanchet, T., Flores, I., Morgan, M.: The weight of the rich: improving surveys using tax data. J. Econ. Inequal. 20(1), 119–150 (2022)

Bourguignon, F.: Appraising income inequality databases in latin america. J. Econ. Inequal. 13(4), 557–578 (2015)

Bucheli, M., Lustig, N., Rossi, M., Amábile, F.: Social spending, taxes and income redistribution in Uruguay. The World Bank (2013)

Burdín, G., De Rosa, M., Vigorito, A., Vilá, J.: Falling inequality and the growing capital income share: reconciling divergent trends in survey and tax data. World Dev. 152, 105783 (2022)

Burkhauser, R.V., Feng, S., Jenkins, S.P., Larrimore, J.: Recent trends in top income shares in the united states: reconciling estimates from march cps and irs tax return data. Rev. Econ. Stat. 94(2), 371–388 (2012)

Cornia, G.A.: Falling inequality in Latin America: Policy changes and lessons. OUP Oxford (2014)

De Rosa, M., Flores, I., Morgan, M.: More unequal or not as rich? On the missing half of latin american income. Technical report (2022)

De Rosa, M., Sinisclachi, S., Vilá, J., Vigorito, A., Willebald, H.: La evolución de las remuneraciones laborales y la distribución del ingreso en Uruguay; futuro en foco Cuadernos Sobre Desarrollo Humano: Montevideo, Uruguay (2018)

Deaton, A.: Measuring poverty in a growing world (or measuring growth in a poor world). Rev. Econ. Stat. 87(1), 1–19 (2005)

Dwenger, N., Steiner, V., Rattenhuber, P.: Sharing the burden? empirical evidence on corporate tax incidence. German Econ. Rev. 20(4), e107–e140 (2019)

Fairfield, T., Jorratt De Luis, M.: Top income shares, business profits, and effective tax rates in contemporary c hile. Rev. Income Wealth 62, S120–S144 (2016)

Ferreira, F.H., Lustig, N., Teles, D.: Appraising cross-national income inequality databases: an introduction. J. Econ. Inequality 13(4), 497–526 (2015)

Flachaire, E., Lustig, N., Vigorito, A.: Underreporting of top incomes and inequality: a comparison of correction methods using simulations and linked survey and tax data. Rev. Income Wealth (2022)

Flores, I.: Income under the carpet: what gets lost between the measure of capital shares and inequality. http://precog.iiitd.edu.in/people/anupama (2018)

Garbinti, B., Goupille-Lebret, J., Piketty, T.: Income inequality in france, 1900–2014: evidence from distributional national accounts (dina). J. Public Econ. 162, 63–77 (2018)

Gasparini, L., Bracco, J., Galeano, L., Pistorio, M.: Desigualdad en países en desarrollo:> ajustando las expectativas? Documentos de Trabajo del CEDLAS (2018)

Goolsbee, A.: What happens when you tax the rich? evidence from executive compensation. J. Polit. Econ. 108(2), 352–378 (2000)

Jenkins, S.P.: Pareto models, top incomes and recent trends in uk income inequality. Economica 84(334), 261–289 (2017)

Kopczuk, W., Zwick, E.: Business incomes at the top. J. Econ. Perspectives 34(4), 27–51 (2020)

Liu, L., Altshuler, R.: Measuring the burden of the corporate income tax under imperfect competition. Natl. Tax J. 66(1), 215–237 (2013)

Lustig, N., et al.: The missing rich in household surveys: causes and correction approaches technical report, Tulane University, Department of Economics (2019)

Lustig, N., Teles, D., et al: Inequality convergence: how sensitive are results to the choice of data? Technical report (2016)

Meyer, B.D., Mok, W.K., Sullivan, J.X.: The under-reporting of transfers in household surveys: its nature and consequences (2015)

Morgan, M.: Extreme and persistent inequality: new evidence for Brazil combining national accounts, surveys and fiscal data, 2001-2015. World Inequality Database (WID. org) Working Paper Series 12, 1–50 (2017)

Novokmet, F., Piketty, T., Zucman, G.: From soviets to oligarchs: inequality and property in Russia 1905-2016. J. Econ. Inequal. 16(2), 189–223 (2018)

OECD: OECD framework for statistics on the distribution of household income, consumption and wealth. OECD Publishing (2013)

Piketty, T.: Income inequality in france, 1901–1998. J. Political Economy 111(5), 1004–1042 (2003)

Piketty, T., Alvaredo, F., Assouad, L.: Measuring inequality in the middle east 1990-2016: the world’s most unequal region? (2017)

Piketty, T., Chancel, L.: Indian income inequality, 1922-2014: from british raj to billionaire raj? (2017)

Piketty, T., Saez, E., Zucman, G.: Distributional national accounts: methods and estimates for the united states. Quarterly J. Econ. 133(2), 553–609 (2018)

Saez, E., Zucman, G.: The rise of income and wealth inequality in America: evidence from distributional macroeconomic accounts. J. Econ. Perspectives 34(4), 3–26 (2020)

Smith, M., Yagan, D., Zidar, O., Zwick, E.: Capitalists in the twenty-first century. Quarter. J. Econ. 134(4), 1675–1745 (2019)

Suárez Serrato, J.C., Zidar, O.: Who benefits from state corporate tax cuts? a local labor markets approach with heterogeneous firms. Amer. Econ. Rev. 106(9), 2582–2624 (2016)

Torregrosa-Hetland, S.: Inequality in tax evasion: the case of the spanish income tax. Appl. Econ. Anal. 28(83), 89–109 (2020)

United Nations: System of national accounts. https://unstats.un.org/unsd/nationalaccount/docs/SNA2008.pdf (2008)

United Nations: System of National Accounts 2008 (2009)

WIL: Distributional national accounts guidelines: methods and concepts used in the world inequality database (2021)

Wolfson, M.C., Veall, M.R., Brooks, W.N., Murphy, B.B.: Piercing the veil: private corporations and the income of the affluent (2016)

Zwijnenburg, J.: The use of distributional national accounts in better capturing the top tail of the distribution. J. Econ. Inequal, pp. 1–10 (2022)

Acknowledgements

We are grateful to the inequality research group Instituto de Economía-UdelaR for their inputs and contributions. We would like to especially thank Andrea Vigorito for her insights and suggestions throughout the whole process of writing this article; we also extend our thanks to Martín Leites and Luciana Méndez, coordinators of the group, and to the participants of the seminar in which we presented this article. We are also very grateful to the World Inequality Lab’s team for their continuous help and invaluable comments at different stages of this process: in particular, we would like to thank Facundo Alvaredo, Ignacio Flores, and Marc Morgan. We are also grateful to the participants in the session on “DINA in developing countries” at the First WIL Conference in December 2017, and the participants in the session “Income Distribution” at the IX Conference of the Network of Inequality and Poverty (Uruguayan session, November 2017), who commented on early versions of this paper. We thank Nora Lustig, with whom we discussed in depth many of the key aspects of this effort. Finally, we thank Gustavo González, former coordinator of Asesoría Económica at Dirección General Impositiva, and to his staff, Fernando Peláez and Sol Mascarenhas, for the invaluable help and comments received during this research. Any errors remain our own.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of Interests

The authors have no competing interests to declare that are relevant to the content of this article.

Additional information

Publisher’s note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendix

Appendix

GDP and income inequality 1986-2019. Note. In the primary axis GDP is presented with GDP 2005 = 100, whilst percapita household income gini index (estimated based on the household survey) is depicted on the secondary axis. During the period 2009-2016 (between vertical lines, period with tax data available), gini index dropped by about 7 points, and National Income grew at a 5.5% rate

Income shares by estimation step, 2009-2016. Note. Own estimates based on tax-survey data (DGI-ECH) and National Accounts 2012, 2016 (BCU). The figure depicts aggregate income by estimation step: the dark-green area is the sum of tax-survey incomes, the orange area are incomes added during scaling to household sector based on scaling factors depicted in Fig. 2, while the blue area represents reaming imputed incomes of Fig. 14. All incomes from national accounts are net of depreciation, based on Wid.World data for other Latin American Countries

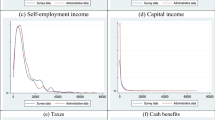

Proxies of firm ownership, 2016. Note. Own estimates based on tax-survey data (ECH-DGI). Alt. 1 refers to the distribution of taxable capital incomes from DGI. Alt. 2 refers in turn to the sum of all taxable and non-taxable capital incomes, including rents and owner occupied housing rents. The preferred alternative (Alt. 3), is equivalent to the second one, but excludes owner occupied housing rent and includes total incomes reported in the household survey by firm-owners

Functional income distribution, 2009-2016. Note. Own estimates based on tax-survey data (DGI-ECH) and National Accounts 2012, 2016 (BCU). The figure presents the distribution of net national incomes in capital and labor shares and their components. All incomes from national accounts are net of depreciation, based on Wid.World data for other Latin American Countries

Capital incomes composition. Note. Own estimates based on firm tax data (DGI), tax-survey data (ECH-DGI) and National Accounts 2012, 2016 (BCU). Solid filled areas represent national account’s aggregates, while doted line depicts aggregate investment incomes (dividends, interest, etc.) from tax-survey data. This line is conceptually consistent with national account’s investment income received by households (light blue area), D4-S14. All incomes from national accounts are net of depreciation, based on Wid.World data for other Latin American Countries

Income aggregates of non-household sector. Note. Own estimates based on National Accounts 2012, 2016 (BCU). Dots in dark represent actually observed data points in national accounts. Undistributed profits are allocated based on the capital ownership proxy, while remaining components of national income are distributed proportionally to total incomes from tax-survey data. All incomes from national accounts are net of depreciation, based on Wid.World data for other Latin American Countries

Pre-tax Gini index by source and imputation step, 2009-2016. Note. Own elaboration based on tax records, household surveys, and national accounts. First step estimates (panel a) are the result of the combination of tax data and household surveys. Second step estimates (panel b) include imputed undistributed profits and taxes, and in third step estimates (panels c and d), incomes are scaled up to National Income aggregates by income source. National series uses the micro database of firm owners, and our preferred imputation method (based on a probit model, see Section 2.2.2). We also depicts the series based on SNA as robustness. All estimates refer to pre-tax personal income distribution

Firm’s profits by alternative, 2009-2016. Note. Own estimates based on firm tax data (DGI), tax-survey data (ECH-DGI), National Accounts 2012, 2016 (BCU), and Balance of Payments (BCU). Both panels depict observed dividends observed in tax-survey data, investment incomes of households excluding interest, undistributed profits and capital incomes sent abroad (computed based on Balance of Payments). All but undistributed profits are equivalent in both panels. In Panel a, undistributed profits are calculated based on national accounts, while Panel b presents undistributed profits computed based on firms’ tax files. All incomes from national accounts are net of depreciation, based on Wid.World data for other Latin American Countries (undistributed profits from panel b are already net of depreciation)

Private capital incomes paid to the rest of the world. Note. Own estimates based on Balance of Payments (BCU) and Impuesto a la Renta de los No Residentes (IRNR) series (DGI). Balance of payments series is constructed based on Central Bank data for two periods: 2009-2012 and 2013-2016. The latter series has an updated methodology but has not been matched with the previous one, resulting in higher private primary income (1.B-credit), i.e., capital incomes paid to the rest of the world by the private sector. The 2009-2012 series was thus adjusted by the ratio of the two period averages. IRNR series is constructed by dividing IRNR aggregate taxes collected by its main flat rate (7%)

Pre-tax income shares of National Income by imputation method, 2009-2016. Note. Own elaboration based on tax records, household surveys, and national accounts. All estimates refer to pre-tax personal income distribution. Top 1, 10, middle 40 (p51-90) and bottom 50%’s shares depicted in panels a, b, c and d respectively.The 5 series show alternatives for the allocation of undistributed profits. Our preferred series uses the matched base of individuals/firms to identify owners, and for the firms for which this identification is not posible, imputes through a probit model (probit series). The new individuals and new individuals (avg) series creates new perceivers for the unmatched firms (1 individual per firm or the average number of individuals per firm of the matched base). The top firm series allocates the non-distributed dividends to the recipient of the highest income of the firm, while the last alternative uses the SNA for the imputation. For more details see Section 2.2.2

Top 10% income composition, 2009-2016. Note. Own elaboration based on tax records, household surveys, and national accounts. First step estimates (panel a) are the result of the combination of tax data and household surveys. Second step estimates (panel b) include imputed undistributed profits and taxes, and in third step estimates (panels c and d), incomes are scaled up to National Income aggregates by income source. Panel c uses the micro database of firm owners, and our preferred imputation method (based on a probit model, see Section 2.2.2). Panel d shows the series based on SNA as robustness

Middle 40% income composition, 2009-2016. Note. Own elaboration based on tax records, household surveys, and national accounts. First step estimates (panel a) are the result of the combination of tax data and household surveys. Second step estimates (panel b) include imputed undistributed profits and taxes, and in third step estimates (panels c and d), incomes are scaled up to National Income aggregates by income source. Panel c uses the micro database of firm owners, and our preferred imputation method (based on a probit model, see Section 2.2.2). Panel d shows the series based on SNA as robustness

Bottom 50% income composition, 2009-2016. Note. Own elaboration based on tax records, household surveys, and national accounts. First step estimates (panel a) are the result of the combination of tax data and household surveys. Second step estimates (panel b) include imputed undistributed profits and taxes, and in third step estimates (panels c and d), incomes are scaled up to National Income aggregates by income source. Panel c uses the micro database of firm owners, and our preferred imputation method (based on a probit model, see Section 2.2.2). Panel d shows the series based on SNA as robustness

Growth Incidence Curves (GIC), 2009-2015. Note. Own elaboration based on tax records, household surveys, and national accounts. Preferred imputation method for undistributed profit based on micro database of firm owners and on a probit model (see Section 2.2.2). All estimates refer to pre-tax personal income distribution

Rights and permissions

Springer Nature or its licensor (e.g. a society or other partner) holds exclusive rights to this article under a publishing agreement with the author(s) or other rightsholder(s); author self-archiving of the accepted manuscript version of this article is solely governed by the terms of such publishing agreement and applicable law.

About this article

Cite this article

De Rosa, M., Vilá, J. Beyond tax-survey combination: inequality and the blurry household-firm border. J Econ Inequal 21, 537–572 (2023). https://doi.org/10.1007/s10888-023-09566-w

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10888-023-09566-w