Abstract

The importance of increasing cost efficiency for community hospitals in the United States has been underscored by the Great Recession and the ever-changing health care reimbursement environment. Previous studies have shown mixed evidence with regards to the relationship between linking hospitals’ reimbursement to quality of care and cost efficiency. Moreover, current evidence suggests that not only inherently financially disadvantaged hospitals (e.g., safety-net providers), but also more financially stable providers, experienced declines to their financial viability throughout the recession. However, little is known about how hospital cost efficiency fared throughout the Great Recession. This study contributes to the literature by using stochastic frontier analysis to analyze cost inefficiency of Washington State hospitals between 2005 and 2012, with controls for patient burden of illness, hospital process of care quality, and hospital outcome quality. The quality measures included in this study function as central measures for the determination of recently implemented pay-for-performance programs. The average estimated level of hospital cost inefficiency before the Great Recession (10.4 %) was lower than it was during the Great Recession (13.5 %) and in its aftermath (14.1 %). Further, the estimated coefficients for summary process of care quality indexes for three health conditions (acute myocardial infarction, pneumonia, and heart failure) suggest that higher quality scores are associated with increased cost inefficiency.

Similar content being viewed by others

Explore related subjects

Discover the latest articles, news and stories from top researchers in related subjects.Avoid common mistakes on your manuscript.

1 Introduction

In the last decade, two environmental pressures that have challenged hospitals’ financial stability and underscored the importance of hospital cost-efficiency improvements are the Great Recession and the continued effort to link hospitals’ payments to the quality of care they provide. A hospital achieves cost efficiency if it incurs the minimum cost with consideration for its respective input prices, output mix, and quality of medical care provided.

A growing body of literature demonstrates that two trends that have been associated with the recent recession, and that further highlight the importance of improving cost efficiency, are changes to patient mix and shifts in health care utilization [1–5]. Job losses led to decreases in the amount of privately-insured patients, increases in the number of Medicaid-enrolled and uninsured patients, and delays in seeking preventative care [2, 3, 6, 7]. In a survey conducted by the American Academy of Family Physicians [8] in the midst of the recent recession, fifty-four percent of interviewed physicians reported seeing significantly lower amounts of patients for routine checkups. In a recent national study, Teff and Kageleiry [5] report a positive association between the delay of preventative medical services and macroeconomic downturns. Patients’ postponement of preventative care, associated with the rising unemployment and the corresponding budget constraints, may have led to greater demand for acute care services, which are recognized as low-margin services. Maeda et al. [9] propose that the delay in preventative care may have resulted in higher admission costs to patients due to deterioration in individuals’ health during the recent recession. Using Healthcare Cost and Utilization Project (HCUP) State Inpatient Databases (SID), the authors report a positive association between unemployment rate and higher inpatient cost per discharge for Medicare and commercial patients between 2005 and 2010. This finding suggests that the effect of delaying preventative care on the demand for more costly procedures may occur in a relatively short period of time.

While previous studies have reported that declines in hospitals’ standard financial measures (e.g., operating margins) were associated with shifts in the demand for health care services during the recent recession, little is known about how hospital cost efficiency fared through that time. In a recent national study, Rosko and Mutter [10] analyzed the impact of certificate-of-need (CON) regulation on hospital cost inefficiency and found an upward trend in cost inefficiency for the years 2005–2009, a period that includes the recent recession. A number of studies have found that higher unemployment rate, a well-recognized indicator of an economic downturn, is associated with greater hospital cost efficiency [11–13]. These national studies, possibly due to the limited availability of data regarding the provision of uncompensated care, identified unemployment rate as a proxy for the financial pressures associated with uncompensated care. Hsieh et al. [14], in their assessment of Virginia hospitals’ cost efficiency between 1998 and 2004, include uncompensated care in the inefficiency estimation and find a positive relationship between this variable and hospital cost efficiency. In a recent national study, Reiter et al. [1] report that not only inherently financially disadvantaged hospitals (e.g., safety-net providers), but also more financially stable providers, experienced declines to their financial viability throughout the recession. The importance of cost-efficiency improvement has been further emphasized by increased state and federal budget deficits, as rising uncompensated care may have been inadequately offset by government support [7, 15].

In addition to the inherent pressure of an economic downturn on hospitals’ finances, the literature provides mixed evidence regarding the relationship between linking hospitals’ reimbursement to their quality of care and cost efficiency [16–19]. In a national study of United States’ (U.S.) hospitals, Jha et al. [19] found that lower risk-adjusted mortality rates (e.g., better performances on an outcome-quality care measure) are not necessarily associated with lower risk-adjusted costs, which was their proxy for cost efficiency. Further, Mukamel et al. [17], in their study of hospitals located in 134 metropolitan statistical areas, found that lower risk-adjusted mortality rates came at higher wage-adjusted expenditures per admission. Conversely, Carey and Burgess [16] who examined 137 U.S. Department of Veterans Affairs hospitals found that, for certain quality measures, higher quality care may be achievable at lower costs. This association between better performance on certain quality measures and hospital cost efficiency is in accord with the findings of Deily and McKay [18], who studied the cost efficiency of Florida hospitals with controls for outcome quality (e.g., mortality rates). In consideration of these findings, it remains unclear whether hospitals that successfully improve quality necessarily sacrifice cost efficiency.

In light of the recent recession and the persisting ambiguity regarding the potential tradeoff between hospital cost efficiency and the quality of care they provide, increased understanding of the relationship between hospital efficiency and process of care and outcome quality is highly sought after by policymakers. This knowledge is of particular interest for Washington State (WA) policymakers given recent changes to reimbursements policies promoted at the federal and state level that might have indirectly affected hospitals’ cost efficiency. In 2008, the Centers for Medicare and Medicaid Services (CMS) released a new payment regulation under the Inpatient Prospective Payment System prohibiting reimbursement for eight hospital-acquired conditions, termed “never events” [20, 21]. This regulation, included in the Deficit Reduction Act of 2005, denies payment for selected conditions that develop during the hospital stay. The initiative signaled a new reimbursement strategy of directly aligning payment to patient outcomes and has further underscored the importance of hospital cost-efficiency improvements. In 2010, WA passed the Hospital Safety-Net Assessment Act. The act introduced a new reimbursement program, aimed at improving quality outcomes, called the Medicaid Quality Incentive [22]. This program built upon the federal hospital-acquired conditions legislation and includes measures such as care transitions and avoidable re-hospitalizations to determine reimbursements. More recently, two pay-for-performance policies implemented as a result of the Patient Protection Affordable Care Act (PPACA) are the Hospital Value-Based Purchasing (HVBP) and Hospitals Readmissions Reduction (HRRP) programs, intended to incentivize hospitals’ provision of higher quality services at lower costs [23].Footnote 1 WA is of special interest given its poor performance in these recently implemented reimbursement policies. In Fiscal Year (FY) 2013, the initial year of implementation of the HVBP program, seventy-two percent of the state’s participating community hospitals received payment reductions, the sixth highest percentage in the nation [24]. In a recent national study, Gilman et al. [25] found that safety-net hospitals were more likely than others to be financially punished by the HVBP program. These types of providers receive disproportionate-share hospital (DSH) payments as they serve a disproportionately high numbers of patients covered by public insurance programs (e.g., Medicaid and Medicare) and those lacking insurance. In WA, forty-seven of the ninety-one community hospitals received DSH payments in 2012. Forty-four percent of the total penalties under the HVBP program were assessed to hospitals with at least thirty-six percent of total admissions being patients with public insurance or uninsured.

This study contributes to the literature by using stochastic frontier analysis (SFA) to analyze cost inefficiency of WA community hospitals between 2005 and 2012, with controls for patient burden of illness, hospital process of care quality, and hospital outcome quality. Both of the quality measures we included in this study function as central measures for the determination of hospital reimbursement adjustments in HVBP and HRRP programs. Moreover, CMS’s recent integration of the efficiency domain to the determination of hospitals’ payment adjustments accentuates the value of additional analysis pertaining to hospital cost efficiency for present and future policy guidance. The financial data and hospital-reported quality measures come from the WA Department of Health and CMS’s Hospital Compare, respectively.

2 Stochastic frontier framework

Stochastic frontier analysis assumes a neo-classical cost function in which total operating costs are a function of input prices and outputs. Following Kumbhakar and Lowell’s [26] theoretical framework and using vector notation, we described total operating expenses for hospital i at time t with the following function:

where TC is the total cost for the ith provider at time t, i = 1,..., 72 and t = 1,..., 8, Y it is a vector of outputs, P it is a vector of input prices, X it is a vector of hospital-specific characteristics, and β is a vector of parameters to be estimated. The variable v it is a measure of random noise that is assumed to be normally distributed with zero mean and constant variance (i.e., N(0,\( {\sigma}_v^2 \))). The last term in equation (1), u it , represents positive deviations from the best practice cost frontier (BPF) and indicates the time-varying cost inefficiency; it is interpreted as the deviation from expected costs, given the relevant characteristics for hospital i at time t, that is not explained by random noise [27].Footnote 2 Its distribution is assumed to be independent of v it . In this study, we specified the functional form of u it as [28]Footnote 3:

where u it is a positive variable, X lit is a vector of hospital-specific explanatory variables related to the inefficiency effects and w it are unobservable random variables.

Building upon Mutter et al. [29] and applying a translog functional form to equation (1), the cost function is econometrically specified as follows:

The structure of the above cost function is assumed to satisfy the following conditions: continuity, symmetry, linear homogeneity in prices, and concavity in input prices [30].Footnote 4 To address heterogeneity of outputs across providers, we used process and outcome quality measures and case-mix indexes as controls for quality of care and patient burden of illness.

We applied a maximum likelihood approach, allowing for time-varying inefficiency, to estimate equation (3) [28]. The predicted BPF resulting from this approach indicates the estimated costs of a fully efficient hospital (u it = 0). Cost efficiency is defined as [31]:

where CE, which stands for cost efficiency, is the ratio of the estimated stochastic frontier cost to the observed costs at time t. Equation (4) implies that this measure is between zero and one. The reciprocal of this measure is exp(u it ) and the amount by which it surpasses one is a measure of inefficiency.

3 Data

The data to estimate the proposed translog cost function come from two sources: the WA Department of Health, and Hospital Compare. We obtained financial reports of all community hospitals reporting to the state for the period 2005–2012 from the WA Department of Health, and calculated summary performance scores for each hospital based on several quality indexes reported to Hospital Compare to account for process of care and outcome quality differences. While there were a total of ninety-one community hospitals in the state by 2012, we ultimately included seventy-two providers in the sample. Financial data for one hospital were not available; four hospitals were not in operation throughout the entire period analyzed; and process of care and outcome quality measures were not reported for the remaining fourteen providers. Specialty hospitals such as Veterans Administration, psychiatric, and military hospitals were excluded from this study.

3.1 Cost variables

The dependent variable is the natural logarithm of the total operating expenses normalized by an input price, a necessary condition to obtain linear homogeneity in input prices [29, 32–34]. The two input price variables included in the cost function are the average cost per worker and the average price of capital. We created the former by dividing the sum of total salaries, wages and benefits by the total number of full-time equivalents for all staff categories. Given the aggregation of the available financial data, it was not possible to account for variation in total salaries, wages, and benefits by type of staff. The price of capital is the sum of depreciation, leases and rentals divided by the total square footage of the hospital. We log-transformed and normalized all input prices. In this study, we used the capital input price to normalize the dependent variable and the price of labor.Footnote 5

The hospital outputs included in the cost function are: total inpatient admissions, total outpatient visits, and post-admission days (total inpatient days - total admissions). As indicated in equation (3), these variables were log-transformed. Figures 1 and 2 show historical trends for hospitals’ operating costs, total admissions, input costs, and three measures that are highly associated with macroeconomic recessions (charity care, bad debt, and uncompensated care, which is the sum of charity care and bad debt). While total admissions increased on average by 2.8 % per year, the growth in operating costs was 5.9 % between 2005 and 2012. Two factors that may partially explain the growth in operating costs are labor and input costs, which account for 60 % of total operating costs. Figure 1 shows that both labor costs and capital inputs increased by 5 % and 5.1 %, respectively. The average growth in charity care and bad debt for the studied period was 12.9 % and 8.8 %, respectively, with their highest increases occurring between 2007 and 2009.

Hospitals’ operating costs, total admissions, labor costs, and capital input costs (index, 2005 = 100)

Charity care, bad debt, and total uncompensated care (index, 2005 = 100)

To account for variation in the types of services that hospitals offer, we included the following variables related to the intensity of care provided: the percent of birth admissions (total birth admissions/total admissions) * 100 %), the Medicare Case-Mix Index, the percent of emergency room visits ((total emergency room visits/total outpatient visits) * 100 %), and the percent of outpatient surgical care visits (total outpatient surgical care visits/total outpatient visits) * 100 %).

A number of studies have stressed that the importance of including quality of care measures extends beyond the benefits of controlling for output heterogeneity [19, 35, 36]. Their inclusion simultaneously addresses the upward bias in the estimation of cost inefficiency for providers with higher quality of care while assessing the direct impact of quality improvements on hospitals’ costs. Santerre and Neun [37] identify three types of measures that may reflect quality differences across providers: structural, process, and outcome quality. The first one relates to levels of amenities and personnel training, among other things. Process of care quality refers to the actions health care organizations take on behalf of patients, such as the provision of appropriate antibiotics upon admission. Lastly, outcome quality reflects the effect of medical care on patients’ health and includes measures such as post-care mortality and readmission rates. Mutter et al. [29] assess the impact on cost inefficiency of structural quality measures, such as Council of Teaching Hospitals membership, and outcome quality measures, such as excess in-hospital mortality rate index for Medicare patients and risk-adjusted iatrogenic pneumothorax rate. In our study we use hospitals’ ability to follow predetermined treatment protocols as measures of clinical process quality, risk-adjusted 30-day mortality and readmission rates for different episodes as measures of outcome quality, and teaching status as a measure of structural quality. In the case of process of care, we created three different quality indexes for three health conditions (acute myocardial infarction (AMI), pneumonia (PN), and heart failure (HF)) following the methodology proposed by the Joint Commission on Accreditation of Healthcare Organizations [19, 38]. In particular, we used the following process of care quality measures to calculate the corresponding summary quality indexes for each health condition: aspirin at arrival, aspirin at discharge, beta-blocker at discharge, and angiotensin-converter enzyme (ACE) inhibitor for left ventricular systolic dysfunction for AMI; left ventricular function assessment, ACE inhibitor for left ventricular systolic dysfunction, and smoking cessation advice for HF; and appropriate initial antibiotics within four hours of arrival, blood culture performed prior to first antibiotic, smoking cessation advice, and pneumococcal vaccination for PN. We calculated a summary score for each of the three conditions by summing the ratio of the number of times an appropriate action was performed by the total number of cases the hospital should have administered the treatment [38]. For instance, the mean value for AMI process of care quality index (0.9084) reported in Table 1 means that the average provider in the sample provided the appropriate action 90.84 % of the time. Similar to previous studies, we did not calculate summary scores for those hospitals that did not have a minimum of thirty patients for at least one of the measures for each condition. In order to control for outcome quality, we include in-hospital 30-day risk-adjusted mortality rates for AMI, HF, and PN. In light of the recently implemented HRRP pay-for-performance program, we also account for the effect of 30-day risk-adjusted readmission rates, related to the aforementioned conditions, on hospitals’ total costs.

In addition to controlling for quality measures, Folland and Hofler [39] have noted that the presence of empty beds (e.g., reservation beds) does not necessarily indicate inefficiencies within a hospital setting. Instead, intentionally allowing beds to remain unoccupied could be a strategic decision aimed at facilitating better responses to unexpected surges in demand. In acknowledgement of this, we followed Joskow [40] and constructed a reservation quality measure for beds by dividing the difference between total beds and average daily census by the square root of average daily census. We also included a time trend variable as a proxy for technological advancements. In particular, this variable can indicate whether hospitals have been acquiring more costly technology over time and thus shifting the BPF out [36].

3.2 Inefficiency variables

To estimate cost inefficiency, equation (2), we included a number of additional variables in the stochastic frontier cost function. To control for ownership, we included three categories: for-profit hospitals, government (non-federal) hospitals, and non-profit hospitals. We specified the latter as the base category. The reason for controlling for differences in organizational missions across hospitals stems from the Property Rights Theory, which suggests that since for–profit organizations place significant weight on earning profits, they are expected to achieve higher cost-efficiency levels than those of government-run or non-profit organizations [41].

Besides differences in hospitals’ mission, it is also important to acknowledge the regulatory pressures presented by public payers. Since 1983, reimbursement from public payers has been based on the prospective payment system. This payment system, intended to shift cost uncertainty from third-party payers to providers, sets predetermined rates for treatments. Hospitals that spend less than the reimbursement rates are allowed to keep the difference, but a health care provider that incurs a cost of providing a service that is higher than the rate it is reimbursed is forced to absorb the extra costs. To acknowledge the pressure that the prospective payment system may apply on hospitals’ budgets, we included Medicaid admissions and Medicare admissions as a percentage of total admissions. To reflect macroeconomic fluctuations, we included three different variables: charity care admissions per bed, bad debt admissions per bed, and uncompensated care admissions per bed. Following previous studies, we constructed these measures by dividing total charity care charges and bad debt by the hospital’s average charge per admission divided by the number of hospital beds [14, 42, 43]. Uncompensated care admissions per bed are the sum of charity care admissions per bed and bad debt admissions per bed. To control for the effect of market competition on cost inefficiency, we created a Herfindahl-Hirschman Index (HHI) with market boundaries defined by county. Building upon Mutter and Rosko [44], we calculated HHI by summing the squares of the market shares of admissions for all of the hospitals within a county. This index approaches one in a county with a high degree of market concentration (e.g., one or two providers serving a county) and approaches zero in markets with high competition. Since higher HHI index values reflect less competitive pressure, we anticipated that cost inefficiency would be directly related to HHI [44]. The last control variable, trend, allows for time-varying efficiency [36].

4 Results

Four different models are presented in this section. In Model I (the base model), we do not account for quality of care. In addition, uncompensated care is accounted for using charity care and bad debt as two separate inefficiency-effects variables. In Model II, we control for quality of care by including three clinical process of care quality measures in the cost function. In Model III, outcome quality measures are added to the cost function. In Model IV, the sum of charity care and bad debt are included as the joint measure of uncompensated care. We did this in recognition of the previous studies that have noted that the wide variation in the classification of charity care and bad debt cases across healthcare providers, may lead to inaccurately measured differences in charity care provision [14, 45, 46].

To determine the appropriate estimation technique and model specification for our dataset we performed a number of likelihood restriction tests, which are reported in Table 2. The first indicates whether a SFA is superior to an ordinary least squares (OLS) estimation. The test’s null hypothesis is that OLS parameters are consistent, implying that deviations from the BPF are due only to statistical noise. As shown in Table 2, we rejected this hypothesis in favor of the SFA approach. The second hypothesis test concerns the functional form of the cost frontier. In this case, a Cobb-Douglas specification is compared to a less restrictive form, the translog transformation. Based on the chi-squared (χ2) value in Table 2, we found the translog functional form was the more appropriate specification of the cost function. The third test relates to the statistical distribution of the inefficiency variable u it . We rejected a half-normal distribution in favor of a truncated-normal. The last test considers the validity of the included cost-inefficiency variables as a group. The rejection of this test’s null hypothesis validates the inclusion of these inefficiency variables. Based on these diagnostic tests, we used the SFA approach to estimate a translog cost function with a truncated-normal distribution in all three models.

The parameter estimates for the translog cost function are reported in Table 3. We estimated this preferred model using the maximum likelihood approach outlined in Battese and Coelli [28]. The signs of some of the coefficients of the output and input price variables do not correspond to our ex-ante expectations. This may be due to the presence of multicollinearity from the inclusion of squared and interaction terms in the estimation [10, 36].Footnote 6

The estimated coefficients for total admissions and the price of labor are both significant and have the expected signs across all models. The coefficients of the variables we included to control for the intensity of care provided, such as Medicare case-mix and percentage of emergency department visits, are positive and significant in all four models with the exception of births admissions as a percentage of total admissions. These results suggest that, for instance, the severity of Medicare patient cases is positively correlated with operating costs. The coefficient for reservation quality indicates that, while designating beds for unexpected surges in admissions may be desirable, this strategy is associated with higher operating costs.

In the case of the two types of quality measures included in these models, process of care quality and outcome quality, the estimated coefficients suggest a positive association between the provision of higher quality care and hospital operating costs. With regard for clinical process of care quality, better performance in AMI, PN, and HF cases is positively correlated with costs. This suggests that following established procedures that are intended to promote higher quality of care, is associated with increased operating costs. This result is consistent with the findings of Jha et al. [19], who reported that low-cost hospitals do not necessarily provide better process of care quality. In the case of the outcome quality measures, the coefficients for risk-adjusted 30-day mortality rates are positive and significant, and thus suggest that lower mortality rates are associated with higher costs. A plausible reason for this could be hospitals investing in costly resources in an effort to improve patient outcomes. The coefficients for the readmission rates categories are positive, but only that of the AMI readmission rate is significant, which suggests that lower readmission rates are associated with lower costs. These are relevant findings in light of the renewed efforts to realign the growth of healthcare costs with healthcare outcomes in the U.S., such as the HVBP and the HRRP pay-for-performance programs.

The positive coefficient of the time-trend variable in the cost function suggests a direct correlation between time and costs. Since this variable serves as a proxy for new technology adoption, the association implies that hospitals have been able to shift their BPF through time by acquiring more costly technology. Rosko and Mutter [10] discuss a new type of medical arms race in which hospitals utilize what the authors refer to as “retail strategy” practices. These strategies include technology acquisition, which permits hospitals to deliver higher margin services [10, 47]. Our result is in accord with this “retail strategy” hypothesis.

The estimated coefficients for the inefficiency-effects variables are reported in Table 4. The coefficients for ownership status (for-profit and non-federal government providers) are negative. This suggests that for-profit hospitals are associated with higher cost efficiency when compared to non-profit providers, which is in line with the Property Rights Theory [35, 44, 48–50]. The negative coefficients for Medicaid and Medicare shares of admissions suggest that the reimbursement policies of public payers are positively associated with cost efficiency. Since the payment rates from public insurance are based on a prospective payment system and tend to be below cost, this result implies that hospitals respond to financial pressure from reimbursement policies by decreasing their cost inefficiency.

The negative coefficient for the HHI variable suggests that a higher degree of market concentration (i.e., HHI closer to one) is associated with lower cost inefficiency. This result is counterintuitive based on cost production theory that states that market competition encourages producer to implement cost minimization strategies. As previous studies have pointed out, the introduction of the prospective payment system not only shifted some of the cost uncertainty to providers, but also gradually transformed the nature of market competition from service-based to price-leadership [41, 47, 51]. The inverse relationship found in this study between cost inefficiency and market concentration suggests that WA hospitals engage in service-based competition. This finding is consistent with those of previous studies [12, 52, 53].

The coefficients for the summary performance scores (AMI, PN, and HF clinical process of care quality indexes) are positive; this suggests that better process of care quality is associated with higher cost inefficiency. Hospitals may implement several strategies to adapt to the pay-for-performance paradigm shift in the industry. For example, providers may attempt to perform better by increasing the level of personnel training, diversifying amenity offerings, or acquiring more advanced technology [54]. Though these strategies may have facilitated the desired performance improvements, hospitals may have escalated training levels to unnecessary heights or administered diagnostic tests in excess. If providers overcompensated for the pay-for-performance programs, their responses may prove to be unsustainable given the associated effects on cost efficiency. Further, the positive coefficient for the trend variable suggests that movements away from the BPF have been associated with the passage of time. These are important findings given the renewed efforts to simultaneously decrease cost inefficiency and foster higher quality in the U.S. health care system.

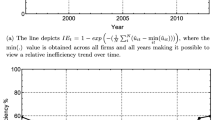

Table 5 presents the estimated mean hospital cost inefficiency per year. For all three models, there is a positive association between cost inefficiency and time. In particular, a noteworthy trend is the increase in the estimated cost inefficiency from pre-recession to post-recession years. The mean values reported in Table 5 suggest that while hospitals have generally prevented further attrition of their cost efficiency, it remains well below that of the pre-recession years. Also, it is important to note the decrease in the mean cost inefficiency with the inclusion of quality variables. This decrease highlights the importance of controlling for outcome quality variables in order to reduce an upward bias in the estimation of cost inefficiency [29].

A recurring issue in the implementation of SFA, which is also of great relevance for policy formation, is the stability of the cost-inefficiency estimates. Following Bauer et al. [55], we tested the inefficiency estimates consistency using five conditions: inefficiency levels, inefficiency rankings, the identification of extreme performers, stability over time, and correlations with standard measures of hospitals’ financial performance through the period studied. The findings corresponding to the first three conditions are reported in Table 6. The distributional characteristics of the cost-inefficiency estimates suggest that their levels are consistent across all three models. While absolute measures of cost inefficiency are important, the relative ranking of hospitals may be more relevant to policymakers. The positive and significant Spearman rank-order correlations indicate that the hospitals’ rankings across models are consistent. In addition to the results regarding the first three consistency conditions, Table 6 presents the percentage of hospitals that are identified across all models with inefficiency estimates in the bottom seventy-fifth percentile (lower triangle) and in the top seventy-fifth percentile (upper triangle). For instance, of the providers identified in the bottom seventy-fifth percentile (e.g., highest cost inefficiency) by Model II, 89.2 %, 91.2 % and 90.7 % are also ranked in the bottom quartile by Model I, Model III, and Model IV, respectively.

While all of these findings indicate consistency across models regarding levels, rankings and extreme performers, the consistency condition that is highly useful for policy purposes is the stability of hospital cost-inefficiency estimates over time. To determine whether this condition was satisfied, we calculated rank-order correlations between cost-inefficiency estimates in each year i, where i = 2005,…, 2011, and in each year j, where j = 2006,…, 2012, with i < j. Table 7 shows the average rank-order correlations between each pair of years. All of the correlation coefficients are positive and significant. For instance, the first entry in column one (93.2), represents the average of seven correlations of cost-inefficiency rankings that correspond to a one-year interval: 2005 with 2006, 2006 with 2007, 2007 with 2008, 2008 with 2009, 2009 with 2010, 2010 with 2011, and 2011 with 2012. Following this logic, the second column shows the mean correlation of cost inefficiency that corresponds to a two-year interval (e.g., 2005 with 2007, 2007 with 2009, Etc.). The mean correlation coefficients reported in Table 7 suggest that cost-inefficiency rankings are stable but decline over time for all three models. For instance, for Model II, the mean correlation for a seven-year period gap (e.g., 2005 and 2013) is 77.6 compared to 89.1 for a three-year period gap. However, it is important to note that even after seven years, the rankings are highly correlated with 2005 rankings.

Table 8 reports Pearson correlation coefficients between the estimated cost-inefficiency scores and frequently used measures of hospitals’ financial performance through the period studied [36, 56]. We found a positive correlation between operating costs per adjusted admission, a general measure of cost inefficiency, and our estimated inefficiency scores. In the case of operating margin, a measure of hospital profitability, the correlation coefficient is negative, suggesting that cost inefficiency is negatively related with profitability levels. Labor productivity, measured as full-time equivalent employees per adjusted admission, has a negative correlation with cost inefficiency. The correlation coefficients for the other efficiency ratios also show the expected associations.

5 Conclusion

In consideration of the potential tradeoff between hospital cost efficiency and improvements in care quality, we examined WA hospitals’ cost inefficiency through the recent recession with controls for both process of care and outcome quality. Using SFA, we estimated hospital cost inefficiency based on a translog cost function for the period 2005–2012. The average estimated level of cost inefficiency before the Great Recession (10.4 %) was lower than it was during the Great Recession (13.5 %) and in its aftermath (14.1 %). The estimated coefficients for the process of care quality indexes for the three health conditions (AMI, PN, and HF) suggest that higher quality scores are associated with increased cost inefficiency. In the case of the outcome quality measures (30-day risk-adjusted mortality rates for AMI, PN, and HF), lower rates are correlated with higher costs. These findings are relevant to the current policy debate surrounding the implications of the HVBP for hospitals’ finances, as this pay-for-performance program includes the Clinical Process of Care domain and the recently implemented Outcome domain to determine reimbursement adjustments [23]. Pay-for-performance policies are frequently formed with three often competing objectives: hospital financial viability, provision of quality care, and cost efficiency [36]. While past and new reimbursement policies have been designed to realign the growth of healthcare costs with heath care outcomes, unintended consequences, such as increases in cost inefficiency, could diminish their effectiveness and sustainability.

The upward trend in hospital cost inefficiency is troubling in the wake of the so-called “productivity adjustment factor”, a provision in the PPACA founded on the assumption that productivity growth in the health care industry will closely follow that of the general economy [57]. Total factor productivity (TFP) growth is defined as the sum of changes in cost efficiency, technical progress (e.g., technology improvement), and scale efficiencyFootnote 7 [58]. Our findings suggest that the BPF shifted out (due to the acquisition of new technology suggested by the sign of the trend variable), which could potentially reflect an increase in productivity. However, providers may be moving further away from the BPF due to decreasing hospital cost efficiency. These dynamics may partially reconcile our findings with regard to cost efficiency with those of Romley et al. [59], who report that U.S. hospitals’ productivity between 2002 and 2011 grew at a faster rate than in previous years.

Limitations of this research pertain to the availability of quality measures and the challenges that health production analysis entails. While there have been significant improvements in the reporting and release of quality measures, there is still an important number of hospitals for which data are missing in multiple years. Since seventy-two WA community hospitals report process of care and outcome quality measures, great caution should be taken when generalizing these findings to providers not included in our sample. With regard to the second limitation stemming from the complexity of health production, while SFA approach allows for the estimation of cost inefficiency, this estimate only pertains to the production of the intermediate good (healthcare services) and does not allow for comprehensive inferences about the production of health (e.g., greatest increase in health with lowest inputs costs) [60].

While a more comprehensive evaluation is required to assess hospitals’ performance beyond cost inefficiency, the findings in this study suggest that policymakers must take great care when introducing new reimbursement policies. The upward trend in WA hospitals’ cost inefficiency through the recent recession, coupled with financial penalties from new programs such as the HVBP and HRRP programs, is especially concerning given CMS’s recent integration of the efficiency domain to the determination of future HVBP payment adjustments.

6 Appendix

6.1 Best practice cost frontier

Developed independently by Aigner et al. [61] and Meeusen and Van den Broeck [62], SFA estimates cost inefficiency by decomposing deviations from the BPF into a random and a deterministic error. The deterministic error is assumed to represent hospital cost inefficiency. The BPF represents the cost level that would result from full efficiency, given the hospital’s particular set of outputs and input prices. Cost efficiency is therefore defined as the ratio of the predicted best-practice total costs to observed total costs and ranges from zero (e.g., full inefficiency) to one (e.g., full efficiency).

6.2 Statistical distribution of uit

Specification of the statistical distribution of the inefficiency variable u it , and implicitly that of w it , is a recurring issue in this type of model. Four different probability distribution functions have been identified in the literature: half-normal, gamma, exponential, and truncated normal [63]. In many cases u it is assumed to follow a half-normal distribution. An alternative approach is to assume a truncated normal distribution, which is a generalization of the half-normal [64]. However, in the absence of evidence-based consensus or substantial guidance from economic theory, the assignment of statistical properties to the inefficiency variable constitutes an empirical challenge. In light of this quandary, we performed a log-likelihood restriction test to determine the distribution that best fit the dataset [63].Footnote 8 In the application of SFA for hospitals, the heterogeneity of outputs across providers is another concern [29]. In this context, output heterogeneity refers to the significant variation in the types of patients treated. If the issue is left unaddressed, the cost inefficiency for a provider with a greater proportion of high-risk cases could potentially be overestimated. The current literature suggests that including quality measures and severity-case indexes considerably mitigates the upward bias in cost inefficiency [29, 44].

6.3 Cost function structure

The structure of the cost function is assumed to satisfy the following conditions: continuity, symmetry, linear homogeneity in prices, and concavity in input prices. The continuity of the cost function in terms of its first and second derivatives is satisfied given the specification of equation (3). Symmetry refers to the fact that the second cross derivatives are symmetric (e.g., α nj = α jn and α mk = α km ). Linear homogeneity in prices is achieved when a proportional increase in all input costs results in total costs increasing by the same proportion: ln(TC(Y, tP)) = ln (tTC(Y, P)) = ln (t) + ln (TC) for all P. This property ensures that the cost-minimizing input choices do not change if input prices experience the same percentage increase. In this case, the allocation of inputs is only a function of the ratios of the inputs’ prices. In order to satisfy the homogeneity assumption, the following restrictions are applied to equation (3): \( \sum_m{\alpha}_m=1,\sum_{n,j}{\alpha}_{nj}=0,\mathrm{and}\ \sum_n{\alpha}_n=0 \). Lastly, a cost function must be concave in input prices. This property implies that while total costs increase as an input’s price increases, its percentage change is smaller than that of the input’s price due to the substitution effect among inputs.

Notes

Under HVBP, CMS reduces all participating hospitals’ base operating Diagnosis Related Groups (DRG) payment amounts by a fixed percentage at the beginning of each fiscal year to set aside for later redistribution based on hospital performance. The hospitals’ final adjustment factors determine how much of the initial reduction they each earn back. The HRRP program is designed to diminish hospitals’ monetary gain from inappropriate readmissions pertaining to specific medical conditions. In FY 2013, hospitals received adjustment factors based on their excess thirty-day risk-adjusted readmission rates related to heart attack, heart failure, and pneumonia cases. CMS uses the adjustment factors to determine the proportion of the hospitals’ base operating DRG payments they will be returning each hospital for that year.

See section 6.1 for further discussion of the BPF.

See section 6.2 for discussion of the probability distribution function of this error term.

See section 6.3 for more details about assumptions of the structure of the cost function.

The results of the estimation do not depend on the input price chosen for normalization.

The estimated coefficients assuming a Cobb-Douglas cost function for the output and input variables are positive and significant (p < 0.05).

Scale efficiency refers to the level of output that minimizes the average cost of producing one unit of output [58].

References

Reiter K, Jiang H, Wang J (2014) Facing the Recession: How did Safety-net Hospitals Fare Financially Compared with Their Peers? Health Serv Res 49:1747–1766

Lusardi A, Schneider DJ, Tufano P (2010) The economic crisis and medical care usage. National Bureau of Economic Research. http://www.nber.org/papers/w15843. Accessed 6 June 2015

Mortensen K, Chen J (2013) The Great Recession and Racial and Ethnic Disparities in Health Services use. J Am Med Assoc Intern Med 173(4):315–317

Dranove D, Garthwaite C, Ody C (2014) Health Spending Slowdown is Mostly due to Economic Factors, not Structural Change in the Health Care Sector. Health Aff 33(8):1399–1406

Teff N, Kageleiry A (2014) State-Level Unemployment and the Utilization of Preventive Medical Services. Health Serv Res 49(1):186–205

Gordon T (2012) State and Local Budgets and the Great Recession. http://www.brookings.edu/research/articles/2012/12/state-local-budgets-gordon

Cawley J, Moriya AS, Simon KI (2011) The impact of the macroeconomy on health insurance coverage: Evidence from the Great Recession (Working Paper No. 17600). National Bureau of Economic Research. http://www.nber.org/papers/w17600. Accessed 6 June 2015

American Academy of Family Physicians (2009) Patient Care During the 2008–2009 Recession–Online Survey. http://www.aafp.org/dam/AAFP/documents/media_center/recession/Executive-Summ-Patient-Care-Recession-Survey-20090520.pdf. Accessed 6 June 2015

Maeda JL, Henke RM, Marder WD, Karaca Z, Friedman BS, Wong HS (2014) Association Between the Unemployment Rate and Inpatient Cost per Discharge by Payer in the United States, 2005–2010. BMC Health Serv Res 14:378

Rosko MD, Mutter RL (2014) The Association of Hospital Cost-Inefficiency with Certificate-of-Need Regulation. Med Care Res Rev 71(3):280–298

Rosko MD (1999) Impact of Internal and External Environmental Pressures on Hospital Inefficiency. Health Care Manag Sci 2:64–78

Rosko MD (2001a) Cost Efficiency of U.S. hospitals: A Stochastic Frontier Approach. Health Econ 10:539–551

Rosko MD, Proenca J (2005) Impact of Network and System use on Hospital X-Inefficiency. Health Care Manag Rev 30:69–79

Hsieh H, Clement D, Bazzoli G (2010) Impacts of Market and Organizational Characteristics on Hospital Efficiency and Uncompensated Care. Health Care Manag Rev 35(1):77–87

Newhouse J, Garber A, Graham R, McCoy M, Mancher M, Kibria A (2013) Variation in health care spending: Target decision making, not geography. Committee on geographic variation in health care spending and promotion of high-value care; Board on Health Care Services; Institute of Medicine (IOM)

Carey K, Burgess Jr JF (1999) On Measuring the Hospital Cost/Quality Trade-off. Health Econ 8(6):509–520

Mukamel DB, Zwanziger J, Tomaszewski KJ (2001) HMO Penetration, Competition, and Risk-Adjusted Hospital Mortality. Health Serv Res 36(6):1019–1035

Deilya ME, McKay NL (2006) Cost Inefficiency and Mortality Rates in Florida Hospitals. Health Econ 15:419–431

Jha AK, Orav EJ, Dobson A, Book RA, Epstein AM (2009) Measuring Efficiency: The Association of Hospital Costs and Quality of Care. Health Affairs (Millwood) 28(3):897–906

Deficit Reduction Act of 2005. Pub L No. 109–171, [S] 5001(c), 120 Stat 4, 30

CMS 2008 Changes to the hospital inpatient prospective payment systems and fiscal year rates: final rule. 42 CFR [S] 411–413, 489

WSHCA 2010 Hospitals–Safety Net Assessment. https://legiscan.com/WA/text/HB2956/2009. Accessed 6 June 2015

CMS (2012) Hospital Value-Based Purchasing Program frequently asked questions. Medicare.gov. http://www.cms.gov/Medicare/Quality-Initiatives-Patient-Assessment-Instruments/hospital-value-based-purchasing/Downloads/FY-2013-Program-Frequently-Asked-Questions-about-Hospital-VBP-3-9-12.pdf. Accessed 26 June 2015

Kaiser Health News (2012) By State: hospital Quality Bonuses and Penalties http://khn.org/news/value-based-purchasing-by-state-chart. Accessed June 1, 2015

Gilman M, Adams E, Hockenberry J, Milstein A, Wilson I, Becker E (2015) Safety-net Hospitals More Likely than Other Hospitals to Fare Poorly Under Medicare’s Value-Based Purchasing. Health Aff 34(3):398–405

Kumbhakar S, Lovell CK (2000) Stochastic frontier analysis. Cambridge University Press, Cambridge, England

Lovell C (1993) Production frontiers and productive efficiency. In: Fried H, Lovell C, Schmidt S (eds) The measurement of productive efficiency. Oxford University Press, New York, pp. 82–111

Battese G, Coelli T (1995) A Model for Technical Inefficiency Effects in a Stochastic Frontier Production Function for Panel Data. Empir Econ 20:325–332

Mutter R, Rosko M, Wong H (2008) Measuring Hospital Inefficiency: The Effects of Controlling for Quality and Patient Burden of Illness. Health Serv Res 43:1992–2013

Baumol WJ, Panzar JC, Willig RD (1982) Contestable markets and the theory of industry structure. Harcourt Brace Jovanovich Inc, New York

Battese G, Heshmati A, Hjalmarsson L (2000) Efficiency of Labour use in the Swedish Banking Industry: A Stochastic Frontier Approach. Empir Econ 25:623–640

Herr A (2008) Cost and Technical Efficiency of German Hospitals: Does Ownership Matter? Health Econ 17(9):1057–1071

Besstremyannaya G (2011) Managerial Performance and Cost Efficiency of Japanese Local Public Hospitals: A Latent Class Stochastic Frontier Model. Health Econ 20(S1):19–34

Herr A, Schmitz H, Augurzky B (2011) Profit Efficiency and Ownership of German Hospitals. Health Econ 20(6):660–674

Li T, Rosenman R (2001) Estimating Hospital Costs with a Generalized Leontief Function. Health Econ 10:523–538

Rosko MD, Mutter RL (2010) Inefficiency Differences Between Critical Access Hospitals and Prospectively Paid Rural Hospitals. J Health Polit Policy Law 35(1):95–126

Santerre RE, Neun SP (2013) Health economics: Theory, insights and industry studies, 6th edition, 6th edn. South-Western

Kahn III CN, Ault T, Isenstein H, Potetz L, Van Gelder S (2006) Snapshot of Hospital Quality Reporting and pay-for-Performance Under Medicare. Health Aff 25(1):148–162

Folland S, Hofler R (2001) How Reliable are Hospital Efficiency Estimates? Exploiting the Dual to Homothetic Production. Health Econ 10:683–698

Joskow P (1980) The Effects of Competition and Regulation on Hospital bed Supply and the Reservation Quality of the Hospital. Bell J Econ 11:421–447

Rosko MD (1996) Understanding Variations in Hospital Costs: An Economic Perspective. Ann Oper Res 67:1–21

Banks D, Paterson M, Wendel J (1997) Uncompensated Hospital Care: Charitable Mission or Profitable Business Decision? Health Econ 6:133–143

Rosko M, Mutter R (2008) Stochastic Frontier Analysis of Hospital Inefficiency: A Review of Empirical Issues and an Assessment of Robustness. Med Care Res Rev 65:131–166

Gaskin DJ (1997) Altruism or Moral Hazard: The Impact of Hospital Uncompensated Care Pools. J Health Econ 16(4):397–416

Davidoff AJ, LoSasso AT, Bazzoli GJ, Zuckerman S (2000) The Effect of Changing State Health Policy on Hospital Uncompensated Care. Inquiry 37(3):253–267

Rosko MD (2004) The Supply of Uncompensated Care in Pennsylvania Hospitals: Motives and Financial Consequences. Health Care Manag Rev 29(3):229–239

Berenson R, Bodenheimer T, Pham H (2006) Specialty-Service Lines: Salvos in the new Medical Arms Race. Health Aff 25:337–343

Rosko M (2001b) Impact of HMO Penetration and Other Environmental Factors on Hospital X Inefficiency. Med Care Res Rev 58:430–454

Sari N (2003) Efficiency Outcomes of Market Concentration and Managed Care. Int J Ind Organ 21:1571–1589

McKay N, Deily M (2005) Comparing High- and low-Performing Hospitals Using Risk Adjusted Excess Mortality and Cost Inefficiency. Health Care Manag Rev 30:347–360

Devers KJ, Brewster LR, Casalino LP (2003) Changes in Hospital Competitive Strategy: A new Medical Arms Race? Health Serv Res 38:447–469

McKay N, Deily M, Dorner F (2002/2003) Ownership and Changes in Hospital Inefficiency, 1986–1991. Inquiry 39:388–399

Rosko M, Proenca J, Zinn J, Bazzoli G (2007) The Impact of Membership in Different Types of Systems on Hospital Cost Inefficiency. Inquiry 44:335–349

Donabedian A (1988) The Quality of Care: How Can It Be Assessed? J Am Med Assoc 260(12):1743–1748

Bauer PW, Berger AN, Ferrier GD, Humphrey DB (1998) Consistency Conditions for Regulatory Analysis of Financial Institutions: A Comparison of Frontier Efficiency Methods. J Econ Bus 50:85–114

Coyne JS, Richards MT, Short R, Shultz K, Singh SG (2009) Hospital Cost and Efficiency: Do Hospital Size and Ownership Type Really Matter? J Healthc Manag 54(3):163–174

MedPAC (2015) Context for Medicare Payment Policy. Report to the Congress: Medicare payment policy

Coelli TJ, Rao DSP, O’Donnell CJ, Battese GE (2005) An introduction to efficiency and productivity analysis, 2nd edn. Springer, USA

Romley JA, Goldman DP, Sood N (2015) US Hospitals Experienced Substantial Productivity Growth During 2002–11. Health Aff 34(3):511–518

McGinnis JM, Williams-Russo P, Knickman JR (2002) The Case for More Active Policy Attention to Health Promotion. Health Aff 21(2):78–92

Aigner D, Lovell K, Schmidt P (1977) Formulation and Estimation of Stochastic Frontier Production Models. J Econ 6:21–37

Meeusen W, Van den Broeck J (1977) Efficiency Estimation from Cobb-Douglas Production Functions with Composed Error. Int Econ Rev 18:435–444

Greene WH (2003) Econometric analysis. Prentice Hall, Upper Saddle River, NJ

Stevenson R (1980) Likelihood Functions for Generalized Stochastic Frontier Estimation. J Econ 13:58–66

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Izón, G.M., Pardini, C.A. Cost inefficiency under financial strain: a stochastic frontier analysis of hospitals in Washington State through the Great Recession. Health Care Manag Sci 20, 232–245 (2017). https://doi.org/10.1007/s10729-015-9349-8

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10729-015-9349-8