Abstract

Vietnam is considered one of the most vulnerable countries since it is seriously affected by climate change and natural disaster-related shocks. This study applied the household vulnerability index (HVI), originally developed by the Food, Agriculture, and Natural Resources Policy Analysis Network (FANRPAN, 2011), to measure household vulnerability trends across five socio-economic regions and to assess the impact of shocks on household vulnerability in rural areas in Vietnam. This index is mainly based on the Vietnam Access to Resources Household Survey (VARHS) dataset from 2018, which included 2,974 households in 12 provinces of Vietnam. There are five components in the HVI, namely natural assets, physical assets, financial assets, human assets, and social assets. The feasible generalised least squares method (FGLS) was then used to assess the impact of natural, biological, and economic shocks on household vulnerability. The results showed that most rural households had moderate vulnerability, comprising 85% of observed households in the whole country and five regions. The North Central and South Central Coasts ranked first among the other regions in high vulnerability levels. Moreover, the research results indicated that natural and economic shocks increased household vulnerability HVI scores by 0.01 and 0.008, respectively. Specifically, natural shocks positively impacted household vulnerability in the Northern Midlands and Mountains, with an HVI score of 0.018, while economic shocks caused an increase in HVI scores of 0.026 in the North Central and South Central Coasts. In general, households must improve their ability to cope with shocks by, for example, improving educational attainment, increasing participation in non-agricultural activities and social activities, and diversifying their income.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

Households are made vulnerable to poverty due to the prevalence of shocks and a lack of effective shock coping mechanisms. Idiosyncratic shocks—such as the illness or death of a family member—can affect an individual or an entire household. Conversely, covariate shocks—such as adverse weather conditions—can impact a larger population in an area (Shehu & Sidique, 2015). Vulnerability can be defined as the impaired ability of an individual or group to predict, cope with, and recover from the effects of natural or man-made hazards (Thabane, 2015). Shocks can be divided into several major categories: climatic; economic; political, social, or legal; criminal; health-related. Climatic shocks are related to droughts and floods, erosion, frost, and pests that affect crops or livestock. Economic shocks are related to problems with access to input, including physical access and significant price increases, decreases in output prices, and difficulties in selling agricultural and non-agricultural products (Dercon et al., 2005). Natural disasters are related to weather—such as floods, storms, heat waves, and droughts—and can have enormous impacts on health, the environment, and economic development (Gan et al., 2021; Visser et al., 2014). For example, floods often lead to disruptions in infrastructure and food transportation, and worsening food security and increasing food prices often limit urban households’ ability to access adequate food (Akampumuza & Matsuda, 2017).

There have been numerous studies on epidemic shocks (Béné, 2020; Giones et al., 2020; Hung et al., 2021; Kikuchi et al., 2021; Narayan, 2020; Nguyen et al., 2021a; Song et al., 2020) and how they seriously affect food security, the labour market, industrial networks, and even the exchange rate. For example, Dengue fever cases at three tertiary hospitals in Ho Chi Minh City in Vietnam increased from 1996 to 2009, reaching a peak of 22,860 cases in 2008. Notably, children aged 6–10 years are at the highest risk of developing Dengue shock syndrome. However, mortality is highest in younger children and decreases with increasing age (Anders et al., 2011). Hung et al. (2021) linked epidemic and economic shocks to apply a random-effects model to panel data on the stock returns of 733 companies listed on both the Ho Chi Minh City Stock Exchange and the Hanoi Stock Exchange. The results showed that the daily number of confirmed COVID-19 cases in Vietnam had a negative impact on the stock returns of companies listed on the markets. The effects were more severe for the pre-lockdown and second-stage periods than the lockdown period. The influences also varied across sectors, with the financial sector being the most affected by the pandemic. Another survey of 672 companies in Vietnam indicated that businesses had to choose cost-cutting strategies to cope with the economic shutdown caused by the COVID-19 pandemic (Nguyen et al., 2021a).

Moreover, economic shocks such as unemployment, changes in crop prices, unsuccessful investments, abandonment, loss of land, crime also increase household vulnerability. An unemployment shock remarkably increases the probability that children will enter the workforce earlier, drop out of school, or fail to advance in school. Additionally, the employment probability of 16-year-old girls increases by 50% (Duryea et al., 2007) following an unemployment shock. During the Great Recession, many United States households suffered massive capital losses in housing and financial wealth, and 5% of respondents lost their jobs. For every loss of 10% in housing and financial wealth, the estimated decrease in household spending was approximately 0.56% and 0.9%, respectively. Similarly, unemployment reduced household spending by 10% (Christelis et al., 2015). Unemployment also increases the propensity to commit crime, especially for individuals already in a criminal state (Siwach, 2018). In addition, commodity price shocks can aggravate conflict in low-income countries, where agriculture is considered a major source of employment and income (Ubilava et al., 2021). For example, the decrease in coffee prices increased conflict between individual ranchers in Peru and Colombia (Guardado, 2018).

Vietnam has a total land area of over 33 million hectares, of which agricultural and forestry land account for 34.7 and 45.1%, respectively (General Statistics Office, 2022). Most Vietnamese people heavily depend on agricultural activities. However, in recent years, climate change – represented by erratic rainfall, increased flooding, prolonged droughts, and the increased frequency of tropical cyclones and saltwater intrusion – has posed a serious threat to farmers in Vietnam (Phuong et al., 2018). In addition, there has been an increase in common diseases, such as African swine fever (ASF), which have seriously affected household livestock production activities, especially in pig herds (Nguyen-Thi et al., 2021; Qui et al., 2021). In fact, ASF in even-toed ungulates has spread to 63 provinces and cities in Vietnam, causing about six million pigs to be culled within the year following its outbreak (Pham et al., 2021). In 2019, these measures decreased the total number of pigs by 30.32% (General Statistics Office, 2022). Additional shocks also contribute to an increase in household vulnerability, including unemployment (Leichenko & Silva, 2014), changes in crop prices (Hill & Porter, 2017), job losses, and crop failures (Hadley et al., 2011). Therefore, assessing the influence of shocks related to natural disasters, epidemics or pandemics, and economic issues on household vulnerability can help policymakers provide timely and appropriate support policies for vulnerable households. To assess the impact of shocks on household vulnerability in Vietnam, this study had to answer several questions: (1) Which indicators can be applied to measure household vulnerability in rural Vietnam? (2) How severe is household vulnerability across regions? (3) How do different types of shocks affect household vulnerability?

In Vietnam, natural disasters resulted in a loss of 2.635 million USD, with a GDP loss of 1.18%, in 2017 (Vietnam Disaster Management Authority, 2021). McElwee (2010) indicated that the Mekong River Delta region has high exposure and moderate sensitivity to natural disasters. The Mekong River Delta is the primary agricultural region of Vietnam and one of the world’s most vulnerable regions to drought and salinisation (Tran et al., 2021; Yusuf & Francisco, 2009). Climate change also has a strong negative effect on farm households because they have the lowest ability to adapt to changes in extreme climate conditions (Yu et al., 2010). Ngo (2016) indicated that past climate experience is the most important determinant of adaptive measures that aid farmers in adapting to climate change. In Vietnam, disaster-related shocks have varied macroeconomic impacts in different geographical regions. The impact of a shock depends on the level of access to reconstruction funds, with wealthier and less remote areas showing faster growth after disasters (Noy & Vu, 2010). The downstream areas of the Mekong River Delta and North Central Coast are vulnerable to flood threats caused by hurricanes, especially those associated with sea-level rise (Nguyen et al., 2019). Vu and Ranzi (2017) conducted a survey in the Quang Ngai province, located on the South Central Coast. Their research showed that economic and human losses from floods can push households into poverty, and the average annual loss for tangible costs is estimated to be about 3.5% of the GDP. Arouri et al. (2015) demonstrated that three types of disasters – storms, floods, and droughts – negatively affect household expenditure and income in rural Vietnam.

Impoverished people and countries are more exposed and vulnerable to all types of climate-related shocks, including floods. The poor are frequently exposed to natural hazards, losing more wealth while receiving less support from relatives, financial systems, and the government. Therefore, climate-related natural hazards have an enormous impact on poverty (Hallegatte et al., 2016). Furthermore, Patricola and Cook (2011) showed that climate change is considered a global challenge; extreme weather conditions, such as prolonged droughts and floods, are becoming increasingly common, and crops are becoming progressively more unpredictable. These shocks typically reduce crop yields and food consumption, thus threatening food security, particularly among smallholder farming communities in developing countries (Jack & Suri, 2014; Nelson et al., 2009). From the above overview, the following hypothesis can be drawn: Shocks increase household vulnerability.

Many previous studies on the effects of shocks on household vulnerability have been conducted in various aspects various aspects. However, most of these studies only focused on the impact of each type of shock on household vulnerability. For example, Jack and Suri (2014) indicated that natural disaster shocks reduce crop yields and threaten food security, especially in developing countries. Other previous studies have also examined the impact of natural shocks (Akampumuza & Matsuda, 2017; Arouri et al., 2015; Ngo, 2016; Patricola & Cook, 2011; Vu & Ranzi, 2017), epidemic shocks (Hung et al., 2021; Kikuchi et al., 2021; Narayan, 2020; Nguyen et al., 2021a; Pham et al., 2021), and economic shocks (Christelis et al., 2015; Duryea et al., 2007; Guardado, 2018; Siwach, 2018; Ubilava et al., 2021) on household vulnerability. Therefore, it is necessary to conduct research to assess and compare the impact of the following three types of shocks on household vulnerability in rural areas in Vietnam: natural disaster, epidemic, and economic shocks. Hence, to fill the practical gaps analysed above, the Vietnam Access to Resources Household Survey (VARHS) dataset from 2018 was used in this study to explore the impact of different shocks on household vulnerability.

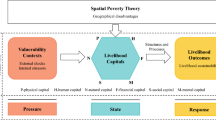

Vulnerability assessment is considered a complex process that involves using different scales in various contexts. Additionally, Feeny and McDonald (2016) indicated that vulnerability can be measured at the national, local, household, or individual level. At the household level, vulnerabilities are related to access to food, knowledge, maternal and childcare status, access to healthcare services, and water and sanitation status; it mainly concerns natural, physical, financial, and social assets (Lesotho Vulnerability Assessment Committee, 2016). The Household Social Vulnerability Index (HSVI) is calculated using the weighted averages of five livelihood assets: financial (20%), human capital (20%), social capital (20%), natural (20%), and physical (20%) assets. The HSVI includes seven indicators: livestock assets, the dependency ratio, households with a member suffering from a long-term disease, social capital contact, membership to social capital groups, the contributions of farming activities, and housing quality (Vincent & Cull, 2010). On the other hand, the Social Vulnerability Index (SVI) demonstrates how to improve the adaptability and resilience of smallholder farmers to the impacts of climate change (Dumenu & Takam Tiamgne, 2020). The SVI also shows the socio-economic and demographic factors influencing a community’s resilience to shocks (Flanagan et al., 2011).

Contrarily, the Food, Agriculture, and Natural Resources Policy Analysis Network (FANRPAN, 2011) developed the Household Vulnerability Index (HVI) to assess the vulnerability of rural households to external shocks, including epidemics, extreme weather, or food insecurity. This index is used to assess a household’s access to five livelihood capital assets: natural (land, soil, and water), physical (livestock and equipment), financial (savings, salaries, remittances, or pensions), human capital (farm labour, gender composition, and dependents), and social capital (information sources, community support, extended families, and social welfare support) assets. For example, the HVI was applied to assess the levels of household vulnerability to disaster-related climate change in the Eastern Cape in South Africa. The study found that 83% of the households in this region were moderately vulnerable (Zhou et al., 2016). Murphy and Scott (2014) showed that not only does the HVI allow for an assessment of the current condition of households, but it also supports predictions of the probability of a further reduction in living standards and the households’ exposure to further exogenous shocks. Thabane (2015) applied the HVI scores obtained from a survey of 2,581 households in Maphutseng, Lesotho. The study’s results showed that the percentage of households with high vulnerability increased by 7.8% from 2009 to 2013. Therefore, the government should urgently develop policies to improve the livelihood of households in poverty-stricken areas, including Maphutseng, and to help households better cope with shocks. In summary, the HVI provides several benefits for assessing the vulnerability of households. First, it aligns with current best practices that involve the use of a sustainable livelihood to analyse aspects of both vulnerability and coping mechanisms. Second, the HVI can be used for population-level analyses and other targeting purposes (Moret, 2014). Hence, in this study, the HVI was used to measure household vulnerability in rural areas in Vietnam.

2 Methodology

The general pathway of the applied methodology of this study involved employing the feasible generalised least squares (FGLS) regression model to assess the impact of shocks on household vulnerability in Vietnam. First, the HVI was created using a two-step method based on the five components of livelihood assets mentioned above. Second, the HVI was used to assess household vulnerability across regions in Vietnam. Finally, empirical regression models were used to find the causal relations between the HVI and shocks.

2.1 Calculating the household vulnerability index

The HVI was calculated using five livelihood assets based on the FANRPAN (2011), with 15 sub-indicators; however, there were slight differences in the financial assets used. Specifically, we used four financial asset indicators, namely savings, salaries, pension, and other income (Table 1). The new indicator (other income) included income from agricultural, forestry, and fishery activities; wild fishing and non-agricultural activities; assets for lease; the sale of assets; other sources.

To assess household vulnerability using the HVI, the research team carried out the following steps:

Step 1: Set up a table of main factors and sub-factors for this indicator.

Step 2: Calculate or set lower and upper bounds for each variable, i.e. the maximum and minimum possible values.

Specifically, this indicator was positively correlated with vulnerability. That is, an increase in the index or sub-component increased the vulnerability of the household. Therefore, the standard equation was calculated by adjusting the equation used in the Human Development Index (UNDP, 2022).

These sub-components with 15 indicators were collected to assess household vulnerability in different units and scales, so the data had to be standardised for the same scale (Table 1). Awolala et al. (2022) indicated that identifying the functional relationships between sub-indicators and household vulnerability is essential to verify the correct directional impact on vulnerability. If the sub-indicator is positively correlated with vulnerability, it signifies that the higher the indicator, the higher the household’s vulnerability. Hence, a normalisation equation was used based on min–max normalisation (Joint Research Centre—European Commission, 2008) to obtain:

where xi illustrates the normalised value of sub-component i, Xi is the actual value of sub-component i, Min(Xi) shows the minimum value of sub-component i, and Max(Xi) shows the maximum value of sub-component i. However, an increase in the sub-component decreased household vulnerability. That is, the functional relationship between the sub-component and household vulnerability was negative (negative correlation). Hence, the normalisation equation was:

The normalised index score ranged from 0 (least vulnerable) to 1 (most vulnerable). After each sub-component indicator was standardised, the average of the sub-component indicators was used to calculate the value of each major component, as follows:

where Mh is the value of the major components for household h, including natural assets (NA), physical assets (PA), financial assets (FA), human assets (HA), and social assets (SA). \({\mathbf{i}\mathbf{n}\mathbf{d}\mathbf{e}\mathbf{x}}_{{\varvec{x}}{\varvec{i}}}\) represents the sub-components indexed by the i of each major component, and n is the total of the sub-components for each major component Mh.

The HVI for each household was measured using Eq. (4) to get the weighted average of the index, as follows:

where HVIh is the HVI for household h, and \({{\text{w}}}_{{\text{Mi}}}\) is the number of sub-components of each major component. The HVI value fluctuated from 0 (least vulnerable) to 1 (most vulnerable).

The HVI classifies households into three categories according to their vulnerability (Fig. 1):

-

1.

Low vulnerability: Households can adapt to shocks and sustain their livelihoods with minimal changes. As a result, they need less external support to cope with these changes.

-

2.

Moderate vulnerability: Households are severely affected; they need urgent support but only temporary assistance to deal with and recover from any shock.

-

3.

High vulnerability: These are households that are considered emergency-level households; they are in an unrecoverable state and can only be recovered with specialised and long-term assistance.

Conceptual framework of shocks and vulnerability. Scource: FANRPAN, 2011

In this study, if 0 < HVI \(\le\) 0.42, it indicated low vulnerability; if 0.42 < HVI \(\le 0.\) 75, it indicated moderate vulnerability; if 0.76 < HVI \(\le\) 1, it indicated high vulnerability.

2.2 Empirical model specifications

2.2.1 Feasible generalised least squares regression

The FGLS method was used to assess the influence of shocks on household vulnerability in rural Vietnam in 2018. Bai et al. (2021) indicated that the FGLS method is more efficient than the ordinary least squares (OLS) method, which involves heteroskedasticity and cross-sectional correlations. The FLGS method can consistently estimate a large error covariance matrix by using the banding and thresholding methods.

The reduced form of the linear regression is shown below:

Yi = \({\alpha }_{0}+\sum_{i=1}^{n}{\beta }_{i}{x}_{i}+{\varepsilon }_{i}\)

Where Yi is the dependent variable, illustrating the HVI and calculated from the five components of natural, physical, financial, human capital, and social capital assets (Table 1). The HVI ranged from 0 to 1; the higher it was, the more vulnerable the household was. Xi indicates the independent variables of natural, biological, and economic shocks; the head of the household’s age, gender, ethnicity, education, household size, wages or salary, agricultural activities, non-agricultural income, resource use, housework participation, participation in social events, dependents, and marital status (divorced, widowed, or single); \({\varepsilon }_{i}\) is the error term. These variables are presented in detail in Table 2.

2.3 Data

The results were based on the 2018 VARHS, which aimed to collect 15 sub-indicators to measure the HVI. The dependent variable, explanatory variables, and control variables were collected and calculated from the VARHS 2018 dataset. The data sample included 2,974 rural households in 12 provinces of Vietnam, as obtained using a complex multi-stage sampling method. These provinces were representative of five socio-economic regions: (i) the Northern Midlands and Mountains: Lao Cai, Phu Tho, Lai Chau, and Dien Bien provinces; (ii) the Red River Delta: Ha Tay province; (iii) the North Central and South Central Coasts: Nghe An, Quang Nam, and Khanh Hoa provinces; (iv) the Central Highlands: Dak Lak, Dak Nong, and Lam Dong provinces; (v) the Mekong River Delta: Long An province. This dataset was used to assess the impact of shocks on household vulnerability in Vietnam (Fig. 2).

Social-economic regions in Vietnam, ArcGIS 10.8

Since 2002, the VARHS has been conducted due to the support of the Danida Research Institute, as well as the advice of experts. By 2009, this programme was expanded in partnership with the United Nations University World Institute for Development Economics Research (UNU-WIDER). Funding comes largely from countries and organisations such as Sweden, Finland, Denmark, Korea International Cooperation Agency (KOICA), and Department for International Development (DFID). The VARHS dataset was surveyed every two years; however, the project ended in 2018. Therefore, the VARHS dataset from 2018 is considered the final version. VARHSs are conducted to access and collect data on Vietnamese rural households related to the land, credit, and labour markets. The VARHS supports a deeper understanding of the economic status of households in rural Vietnam, with a focus on access to and the use of livelihood assets (natural, physical, financial, human capital, and social capital), so it is considered a suitable dataset to measure the HVI. It can also reflect the current trend of the impact of shocks on household vulnerability in rural areas in Vietnam. In summary, in this study, the VARHS 2018 was considered an appropriate dataset to use to measure the HVI in rural Vietnam. This dataset also helped in assessing household vulnerability across five socio-economic regions and analysing the impact of different types of shocks on household vulnerability in Vietnam.

3 Results

3.1 Household vulnerability and types of shocks among regions

Figure 3 reveals household damages in 2018 in terms of housing, paddy production, and vegetable production. Figure 4 shows visualised statistical data about epidemic shocks, namely the reduction in the number of pigs due to ASF in Vietnam in 2018 and 2019. The Northern Midlands and Mountains and the North Central region ranked first in household damage, which included the number of houses that collapsed, were swept away, flooded, had their roof ripped off, or were otherwise damaged. It was found that the Northern Midlands and Mountains are more vulnerable to natural disasters. Specifically, this region often experiences landslides and flash floods every year (Pham et al., 2020), severely affecting production activities and people’s livelihoods. Moreover, the research results showed that the provinces of Kien Giang (in the Mekong River Delta), Quang Binh, and Ha Tinh (both in the North Central region) had the highest number of damaged houses, with 13,045, 11,322, and 6,294 houses affected by natural disasters, respectively. In the North Central region, the rainy season accounts for 68–75% of the year’s rainfall, and it frequently experiences floods that severely affect people’s livelihood. It causes damage to people, production activities, property, and the ecological environment. The flood regime in Ha Tinh is more severe due to the steep terrain of the Lam River basin; in contrast, due to the hydraulic characteristics of the Nhat Le River, the flood regime in Quang Binh is more moderate (Casse et al., 2015). In general, less sturdy and precarious houses are frequently more damaged by natural disasters (e.g. floods and storms) than permanent houses. Poor households also often live in flood-prone areas, so it is more difficult for low-income families to migrate to safer areas or even repair their homes (Reed et al., 2013).

Source: Provincial Statistical Yearbook 2019, ArcGIS 10.8

Damages caused by natural disaster.

Source: General Statistics Office, 2022

Epidemic shocks— The change in the number of pigs due to African swine fever (ASF) in Vietnam.

Moreover, the natural disasters in 2018 heavily affected agricultural activities. These disasters caused damage to paddy and vegetable areas in most regions of the country, especially in the Red River Delta (Nam Dinh and Thai Bình provinces) and the North Central and South Central Coasts (Thanh Hoa, Nghe An, Ha Tinh, and Binh Thuan provinces). The total estimated damage to rice and vegetable areas in Vietnam was 189,870 hectares and 79,399 hectares, respectively.

ASF is a highly contagious and deadly viral disease (Sur, 2019). The spread of ASF outside Africa—most recently, to Mongolia and Vietnam—has raised awareness about this devastating disease, which affects food security and the global swine industry (Dixon et al., 2019). ASF first appeared in Vietnam at the end of 2018. The disease resulted in decreased pig herd numbers in several provinces in the Mekong River Delta (Long An and Tra Vinh), with a 20%–30% reduction in total pig herds. Through 2019, the epidemic heavily affected most Vietnamese provinces, especially those in the Mekong River Delta, Red River Delta, and North Central regions, causing sharp decreases in the total number of pigs. Nguyen et al. (2022) indicated that ASF is a dangerous infectious disease caused by a virus that affects pigs of all ages, and it became one of the greatest threats to the Vietnam pig industry in 2019 (Anh et al., 2023). That is, in 2019, a total of 2,377 out of 5,220 pig farms in Can Tho City, located in the Mekong River Delta, had ASF. Hence, 46 farms tested positive for ASF out of every 100 farms that were at risk of contracting it (Hien et al., 2023).

The HVI in rural Vietnam in 2018 ranged from 0.437 to 0.747. No household was categorised as low vulnerability. Most households were at a moderate vulnerability level, at 85.1%, and only 14.9% of households were at a high vulnerability level. There was a similar tendency for the five regions, with over 80% of households demonstrating medium vulnerability. The North Central and South Central Coasts ranked first in terms of high vulnerability, at 16.6%, followed by the Northern Midlands and Mountains and the Central Highlands, at 16.3% and 15.7%, respectively (Fig. 5). It was found that people living in the North Central and South Central Coasts have suffered much more than other regions, mainly due to their higher exposure to the context of vulnerability. Moreover, due to it being adjacent to the East Sea (about 642 km away), in recent years, natural disasters have occurred more frequently and at increasing intensity in this area, especially storms, floods, and other severe natural disasters (Tran et al., 2022).

Household vulnerability level among regions in Vietnam

Figures 6a and b show that the estimated damage due to economic shocks was much higher and fluctuated more than that of biological and natural shocks, at 1,097.72 USD$, 270.69 US$, and 295.7 US$, respectively (Fig. 6a). Economic shocks include changes in crop prices, unemployment, unsuccessful investments, loss of land, crime (robbery, theft), divorce, abandonment, or internal or extended family disputes. Here, the Central Highlands populations ranked first, with an average loss of 1,130 US$, and they showed stronger fluctuations compared to the others. Conversely, the Mekong River Delta showed the least damage due to economic shocks, with an average loss of 893.7 US$. Biological shocks include avian flu, pest infestation, and crop diseases. The Mekong River Delta was the region most affected by biological shocks, with a loss of 661.07 US$, and this showed more volatility. Total pig production in the Mekong River Delta decreased significantly – by 1.38% in 2018 and 51.22% in 2019 – due to ASF causing severe damage to livestock (General Statistics Office, 2022). Natural shocks include floods, droughts, typhoons, and other natural disasters. In 2018, these shocks caused an average loss of 282 US$ per household in the Central Highlands and 250.48 US$ per household in the Northern Midlands and Mountains.

a: Estimated damage due to shocks. b: Estimated damage due to shocks among regions. Note: CC: North Central and South Central Coast; CH: Central Highlands;MRD: Mekong River Delta; MM: Northern Midlands and Mountains; RRD: Red River Delta

Figure 7 shows that households in rural Vietnam faced higher rates of biological shocks than other shocks, including avian flu (2.69%), pest infestation, and crop diseases (3.19%). The average loss due to these shocks ranged from 8.7 US$ to 3,913 US$ per household. Natural shocks were the next most common, with 0.67% of households experiencing drought (e.g. in the Mekong River Delta) and 0.17% of households experiencing flooding; in addition, typhoons and other natural disasters affected 0.74% of households.

The proportion of households experiencing shocks

In recent years, residents in the Mekong River Delta have suffered from drought and saltwater intrusion more frequently (Khong et al., 2020; Loc et al., 2021; Tran et al., 2021). As a result, drought and saltwater intrusion have seriously affected people’s livelihoods and adaptive capacity (Tran et al., 2021), leading to a significant decrease in agricultural output in this region (Khong et al., 2020). Moreover, other natural disasters, such as heavy rains, flash floods, and landslides, mainly occur in the Northern Midlands and Mountains (Pham et al., 2020), while the North Central and South Central Coasts are frequently exposed to storms, heavy rain, floods, and tropical depression (Luu et al., 2019).

In terms of economic shocks, changes in crop prices caused heavy losses to many farmers (0.81%), with an average loss of 399.48 US$, followed by the shock of the serious illness, injury, or death of a household member (0.67%). Other shocks that were less widespread but just as impactful were unsuccessful investments (0.13%), crime (0.1%), and additional shocks. Price fluctuations have historically caused significant economic instability for manufacturers. For example, in Mexico and Vietnam, coffee prices have been volatile, with sudden changes causing significant shocks to coffee farmers and making them more vulnerable. Moreover, during an economic recession, coffee farmers often fall into debt and cannot recover their investment capital (Eakin et al., 2009).

Figure 8 shows the responses of households to shocks. Most households did nothing when faced with natural, biological, or economic shocks (44.21%, 67.02%, and 51.47%, respectively). Cost-cutting ranked second in coping mechanisms, with 41.05% of households having difficulty with natural shocks and approximately 25% facing biological shocks using this strategy. However, 17.65% of households experiencing economic shocks received assistance from relatives or friends. In addition, it was found that households can use savings, sell livestock and poultry, or rely on bank loans to overcome shocks. Similarly, Nguyen et al. (2020) indicated that selling durable assets is a useful strategy to cope with shocks. Receiving assistance from relatives and friends is considered the main coping strategy for health shocks.

Households’ responses to shocks

3.2 The impact of shocks on household vulnerability in Vietnam

Table 3 shows the effects of shocks on household vulnerability in Vietnam, including natural, biological, and economic shocks. First, OLS regression was used to assess the impact of shocks on household vulnerability for Vietnam as a whole and five socio-economic regions therein. The variance inflation factors of the independent variables were less than 2; in other words, perfect collinearity did not occur in this model. However, the Breusch–Pagan test was applied to these models, and it showed heteroskedasticity, with Prob > chi2 = 0.0000, except the Mekong River Delta model, which used Prob > chi2 = 0.5253. Therefore, FGLS regression was used to remedy the heteroskedasticity problem (Lee et al., 2019), with Prob > F = 0.0000 for all models in Table 2, proving that these models were statistically significant.

Testing the econometric model resulted in the discovery that natural shocks, including floods, droughts, storms, and other disasters, had a positive influence on the vulnerability level of households in Vietnam. If the estimated damage of these shocks increased by 1,000 US$, it would have increased the HVI by 0.01 points. The same trend was shown for the Northern Midlands and Mountains, but with a greater influence: The results showed an increase in HVI of 0.018 points, with significance at 10%. Opiyo (2014) indicated that when people face more than two hazards in five years, this contributes negatively to household vulnerability. Furthermore, disasters—including floods, hurricanes, heat waves, and droughts—can have a considerable influence on health, the environment, and socio-economic development (Visser, 2014). Exposure to weather shocks also reduce expenditure on basic activities and social contributions by 38 and 40 percentage points, respectively (Akampumuza & Matsuda, 2017), while moderate drought causes household consumption in rural areas of Vietnam to decrease by 9% (Hill & Porter, 2017). Ethnic minority groups living in the Northern mountainous areas of Vietnam are particularly vulnerable to climate-induced natural hazards (Nguyen et al., 2021b), especially communities such as the Thai and Hmong people living in the northwest mountainous regions (Nguyen & Leisz, 2021).

Natural shocks impact household vulnerability throughout Vietnam, particularly for populations in the Northern Midlands and Mountains. Meanwhile, economic shocks—such as changes in crop prices; shocks related to the serious illness, injury, or death of a household member; unsuccessful investments; crime—have a positive effect on household vulnerability. The total loss per household increased by 1,000 US$, leading to an increase of 0.008 HVI points at a significance of 1% and an increase of 0.026 in the scores of the North Central and South Central Coasts. Similarly, Hill and Porter (2017) showed that rainfall and price shock impacts on welfare lead to increased vulnerability. Additionally, Ubilava et al. (2021) indicated that commodity price shocks can exacerbate conflict in low-income countries where agricultural activities are considered the primary source of income. The sharp increase in food prices also increased the vulnerability of low-income groups to external shocks (Tiwari & Zaman, 2010). Contrastingly, biological shocks did not affect household vulnerability. For example, the epidemic shocks for livestock that occurred at the end of 2018, mainly due to ASF, only caused a slight decrease in pig herds in some provinces of southern Vietnam (Fig. 4). Overall, these shocks did not affect the household vulnerability of the Central Highland and Mekong River Delta regions. The cause of this low influence may have been because the impact level of the three types of shocks was weak and did not seriously affect households in these regions.

Additionally, household characteristics significantly influenced the HVI. For example, having a female household head increased HVI scores in the North Central and South Central Coasts by 0.015. Female-headed households are particularly vulnerable to the more serious effects of shocks due to a lack of access to beneficial resources and opportunities to embrace credit, land, and non-agricultural employment (Akampumuza & Matsuda, 2017). Furthermore, each additional year of age of the household head reduced the HVI score in the whole country and the Northern Midlands and Mountains by 0.001. However, the household head’s age only moderately affected HVI scores in the North Central and South Central Coast and Central Highlands regions, at 0.0005 and 0.0002, respectively. Opiyo et al. (2014) and Smith et al. (2015) also found evidence that the household head’s age is a significant demographic factor affecting socio-economic vulnerability. However, households headed by individuals over 65 years are often more vulnerable than those headed by younger people (Dwyer et al., 2004). As a result, it may be more difficult for elderly household heads to prepare strategies that enable their families to cope with the stresses and adverse effects of climate change, potentially making them more vulnerable (Opiyo et al., 2014).

If the household head has a higher education, resilience after natural disasters can be improved; education is associated with higher levels of long-term recovery (Frankenberg et al., 2013). That is, the lower the number of educated household members, the higher the vulnerability of the household (Jimoh et al., 2021). Pichler and Striessnig (2013) also indicated that better education provides noticeable short-term effects on vulnerability reduction. Education raises awareness and provides access to critical information, allowing educated people to respond and recover faster and more effectively to warnings and disasters. Investing in education is a vital strategy to prepare communities for the uncertainty of disasters resulting from future climate events. Education also empowers people and helps reduce vulnerability to climate change-related disasters (Striessnig et al., 2013). In other words, household heads with a low level of education may be more vulnerable to climate change-related disasters, including food and water insecurity (Zhou et al., 2016). In the present study, one additional year of schooling or higher education decreased the HVI for the whole country, Northern Midlands and Mountains, and Central Highlands by 0.001, as well as for the North Central and South Central Coasts by 0.002.

In addition, households with heads that are married are more vulnerable than households with heads that are divorced, widowed, or single. This may be because married women are more susceptible to domestic violence from their husbands (Putra et al., 2019). Additionally, married mothers are more vulnerable to depression and have problems with their relationships with their partners relating to a lack of love and support (Kadir & Bifulco, 2013). Herbst-Debby et al. (2021) showed that divorce increases the risk of poverty for women but reduces the risk for men. Further, widowhood tends to increase the risk of poverty for men, while women become more vulnerable as the number of children increases. Contrastingly, Zhou et al. (2016) indicated that households with an unmarried household head tend to show a higher vulnerability to climate change-related disasters than households with a married household head. A substantial proportion of the households considered highly vulnerable to climate change-related disasters had household heads that were widowed or single. Widowed or divorced families are also 37.4% more likely to be vulnerable than married families (Opiyo et al., 2014).

Furthermore, the household size variable must be considered. Increasing the household by one member decreased the HVI scores for the Red River Delta and Mekong River Delta by 0.02, which was higher than the score of the whole country and Northern Midlands and Mountains at 0.018. Household size affects the HVI score because the more members there are in a household, the more likely it is that one member would engage in various activities that would benefit the entire household (Walugembe et al., 2019). Opiyo et al. (2014) also suggested that household size has a great influence on households’ vulnerability level. That is, when a household’s size increased by one member, the household’s vulnerability score was lower than the levels representing moderate and high vulnerability (Thabane, 2015).

In addition, some households have many dependents, particularly young children and the elderly. Dependence, a form of vulnerability that requires the support of a specific person, can increase household vulnerability (Dodds, 2014). In the absence of social systems to take care of these dependents, family resources can be exhausted, consequently increasing the household’s vulnerability (Mustafa et al., 2011). The research results showed this phenomenon in all regions of Vietnam, except the North Central and South Central Coasts.

Economic activities have a significant impact on household vulnerability. Households with members participating in household production related to agriculture, forestry, aquaculture, and housework or chores were more vulnerable than others, with HVI scores of 0.005 (whole country), 0.004 (Northern Midlands and Mountains), and 0.006 (Central Highlands). Agricultural activities are affected by climate change because they are directly dependent on climate change (Praveen & Sharma, 2019); hence, participating in agricultural activities causes an increase in vulnerability.

Joining non-farm activities decreased HVI scores by 0.002 for the whole country and by 0.005 in the North Central and South Central Coasts; households with access to non-farm activities are less vulnerable, which can reduce poverty significantly (Bui & Hoang, 2021; Imai et al., 2015).

Employment status is also an important factor in a household’s vulnerability. Increasing the number of members working for wages or a salary outside the home reduced household vulnerability scores by 1.86 in the Mekong River Delta. Houses with higher unemployment or increased family sizes are more likely to receive a lower income, so they have little or no financial resources to spend on the prevention of and support for emergencies or disasters related to extreme climatic events. Most of the household heads in the rural areas of Vietnam were unemployed and did not own land or other assets, so they had to rely on government subsidies (Zhou et al., 2016).

Increased housework or chores also raised household vulnerability, with scores fluctuating from 0.03 to 0.07. This may be because, as Tabler and Geist (2021) demonstrated, spending time doing housework is associated with depressive symptoms for female caregivers.

Participating in social activities helped to reduce the HVI score by 0.006; the higher a household member’s participation in social organisation, the lower the household vulnerability (Jimoh, 2021). In general, participating in social activities showed the greatest marginal effect values compared to the other variables. It was found that accessing social support networks and participating in community organisations help some individuals increase their capacity (Mustafa et al., 2011) and are related to reduced vulnerability. That is, those who participated in a higher number of family-strengthening activities were more likely to reduce vulnerability than those with lower participation levels (Walugembe et al., 2019).

In summary, the HVI was applied to measure household vulnerability based on five major livelihood assets (natural, physical, financial, human capital, and social capital) with 15 sub-indicators. The results showed that the HVI fluctuates from 0.437 to 0.747, so most households are at a moderate level of vulnerability. Specifically, approximately 92.7% of households living in the Mekong River Delta were identified as moderately vulnerable, followed by those in the Red River Delta at 89.5%. Moreover, FGLS regression was applied to analyse how different types of shocks affect household vulnerability. The results showed that natural and economic shocks increase household vulnerability nationwide. In addition, in the North Central and South Central Coasts, economic shocks significantly increase the HVI.

4 Conclusions and policy implications

The HVI was applied to measure household vulnerability in rural areas in Vietnam based on five livelihood assets, namely natural, physical, financial, human capital, and social capital assets. The results showed that most households (85.1%) in rural areas in Vietnam were at a moderate vulnerability level, while 14.9% were categorised as being at a high vulnerability level. Unfortunately, no households were at the low vulnerability level. The trends of the five socio-economic regions were also similar. For high vulnerability, the North Central and South Central Coasts ranked first, followed by the Northern Midlands and Mountains. Moreover, natural and economic shocks increased household vulnerability, while biological shocks did not affect household vulnerability, in rural areas during the period under study. Natural shocks—such as floods, droughts, storms, and others—caused an average loss of 250.48 US$ per household in the Northern Midlands and Mountains. Due to low adaptive capacity, most households had weak responses when experiencing natural, biological, or economic shocks. Therefore, to limit the impact caused by shocks, households must improve their capacity to respond to various shocks, increase their participation in social activities and non-farm activities, improve their educational levels, and diversify their income.

Moreover, community intervention is necessary to reduce exposure to and limit the impact of natural disasters. Hence, public responses will be more effective if appropriate programmes and mechanisms are established before natural disasters occur, such as the building of a natural disaster warning system or dyke and drainage system in flood-affected areas. In addition, different types of shocks negatively impact households in different ways, so households need to receive support programmes to cope with the specific shocks that they are experiencing (e.g. disaster, financial, or housing assistance).

Data availability

The datasets are used and analysed in this study are available from the corresponding author on reasonable request.

References

Akampumuza, P., & Matsuda, H. (2017). Weather shocks and urban livelihood strategies: The gender dimension of household vulnerability in the Kumi District of Uganda. The Journal of Development Studies, 53(6), 953–970. https://doi.org/10.1080/00220388.2016.1214723

Anders, K. L., Nguyet, N. M., Chau, N. V. V., Hung, N. T., Thuy, T. T., Lien, L. B., & Simmons, C. P. (2011). Epidemiological factors associated with dengue shock syndrome and mortality in hospitalized dengue patients in Ho Chi Minh City, Vietnam. The American journal of tropical medicine and hygiene, 84(1), 127. doi: https://doi.org/10.4269/ajtmh.2011.10-0476

Anh, H. H., Na, L., Thuy, N. N., Beaulieu, A., & Hanh, T. M. D. (2023). Knowledge, Attitude, and Practices of Swine Farmers related to Livestock Biosecurity: A Case Study of African Swine Fever in Vietnam. The Journal of Agricultural Sciences - Sri Lanka, Vol. 18, No 3, September 2023. Pp 307–328, https://doi.org/10.4038/jas.v18i3.9780.

Arouri, M., Nguyen, C., & Youssef, A. B. (2015). Natural disasters, household welfare, and resilience: Evidence from rural Vietnam. World Development, 70, 59–77. https://doi.org/10.1016/j.worlddev.2014.12.017

Awolala, D. O., Ajibefun, I. A., Ogunjobi, K., & Miao, R. (2022). Integrated assessment of human vulnerability to extreme climate hazards: Emerging outcomes for adaptation finance allocation in Southwest Nigeria. Climate and Development, 14(2), 166–183. https://doi.org/10.1080/17565529.2021.1898925

Bai, J., Choi, S. H., & Liao, Y. (2021). Feasible generalized least squares for panel data with cross-sectional and serial correlations. Empirical Economics, 60(1), 309–326.Available at: https://doi.org/10.1007/s00181-020-01977-2.

Béné, C. (2020). Resilience of local food systems and links to food security—A review of some important concepts in the context of COVID-19 and other shocks. Food Security, 12(4), 805–822. https://doi.org/10.1007/s12571-020-01076-1

Bui, L. K., & Hoang, H. (2021). Non-farm employment, food poverty and vulnerability in rural Vietnam. Environment, Development and Sustainability, 23(5), 7326–7357. https://doi.org/10.1007/s10668-020-00919-3

Casse, T., Milhøj, A., & Nguyen, T. P. (2015). Vulnerability in north-central Vietnam: Do natural hazards matter for everybody? Natural Hazards, 79, 2145–2162. https://doi.org/10.1007/s11069-015-1952-y

Christelis, D., Georgarakos, D., & Jappelli, T. (2015). Wealth shocks, unemployment shocks and consumption in the wake of the Great Recession. Journal of Monetary Economics, 72, 21–41. https://doi.org/10.1016/j.jmoneco.2015.01.003

Dercon, S., Hoddinott, J., & Woldehanna, T. (2005). Shocks and consumption in 15 Ethiopian villages, 1999–2004. Journal of African Economies, 14(4), 559–585. https://doi.org/10.1093/jae/eji022

Dixon, L. K., Sun, H., & Roberts, H. (2019). African swine fever. Antiviral Research, 165, 34–41. https://doi.org/10.1016/j.antiviral.2019.02.018

Dodds, S. (2014). Dependence, care, and vulnerability. Vulnerability: New essays in ethics and feminist philosophy, 181–203.

Duryea, S., Lam, D., & Levison, D. (2007). Effects of economic shocks on children’s employment and schooling in Brazil. Journal of Development Economics, 84(1), 188–214. https://doi.org/10.1016/j.jdeveco.2006.11.004

Dwyer, A., Zoppou, C., Nielsen, O., Day, S., & Roberts, S. (2004). Quantifying social vulnerability: a methodology for identifying those at risk to natural hazards.

Eakin, H., Winkels, A., & Sendzimir, J. (2009). Nested vulnerability: Exploring cross-scale linkages and vulnerability teleconnections in Mexican and Vietnamese coffee systems. Environmental Science and Policy, 12(4), 398–412. https://doi.org/10.1016/j.envsci.2008.09.003

FANRPAN, 2011. Measuring vulnerability—challenges and opportunities. Food Agriculture and Natural Resources Policy Analysis Network, 2 (11) (2011), pp. 1–35

Frankenberg, E., Sikoki, B., Sumantri, C., Suriastini, W., & Thomas, D. (2013). Education, vulnerability, and resilience after a natural disaster. Ecology and Society: A Journal of Integrative Science for Resilience and Sustainability, 18(2), 16. https://doi.org/10.5751/ES-05377-180216

Gan, C. C. R., Oktari, R. S., Nguyen, H. X., Yuan, L., Yu, X., Alisha, K. C., ... & Chu, C. (2021). A scoping review of climate-related disasters in China, Indonesia and Vietnam: Disasters, health impacts, vulnerable populations and adaptation measures. International Journal of Disaster Risk Reduction, 66, 102608. https://doi.org/10.1016/j.ijdrr.2021.102608

General Statistics Office of Vietnam , 2022. https://www.gso.gov.vn/so-lieu-thong-ke/

Giones, F., Brem, A., Pollack, J. M., Michaelis, T. L., Klyver, K., & Brinckmann, J. (2020). Revising entrepreneurial action in response to exogenous shocks: Considering the COVID-19 pandemic. Journal of Business Venturing Insights, 14, e00186. https://doi.org/10.1016/j.jbvi.2020.e00186

Guardado, J. (2018). Land tenure, price shocks, and insurgency: Evidence from Peru and Colombia. World Development, 111, 256–269. https://doi.org/10.1016/j.worlddev.2018.07.006

Hadley, C., Linzer, D. A., Belachew, T., Mariam, A. G., Tessema, F., & Lindstrom, D. (2011). Household capacities, vulnerabilities and food insecurity: Shifts in food insecurity in urban and rural Ethiopia during the 2008 food crisis. Social Science and Medicine, 73(10), 1534–1542. https://doi.org/10.1016/j.socscimed.2011.09.004

Hallegatte, S., Vogt-Schilb, A., Bangalore, M., & Rozenberg, J. (2016). Unbreakable: building the resilience of the poor in the face of natural disasters. World Bank Publications.

Herbst-Debby, A., Endeweld, M., & Kaplan, A. (2021). Differentiated routes to vulnerability: Marital status, children, gender and poverty. Advances in Life Course Research, 49, 100418. https://doi.org/10.1016/j.alcr.2021.100418

Hien, N. D., Nguyen, L. T., Isoda, N., Sakoda, Y., & Stevenson, M. A. (2023). Descriptive epidemiology and spatial analysis of African swine fever epidemics in Can Tho, Vietnam, 2019. Preventive Veterinary Medicine, 211, 105819. https://doi.org/10.1016/j.prevetmed.2022.105819

Hill, R. V., & Porter, C. (2017). Vulnerability to drought and food price shocks: Evidence from Ethiopia. World Development, 96, 65–77. https://doi.org/10.1016/j.worlddev.2017.02.025

Hung, D. V., Hue, N. T. M., & Duong, V. T. (2021). The impact of COVID-19 on stock market returns in Vietnam. Journal of Risk and Financial Management, 14(9), 441. https://doi.org/10.3390/jrfm14090441

Imai, K. S., Gaiha, R., & Thapa, G. (2015). Does non-farm sector employment reduce rural poverty and vulnerability? Evidence from Vietnam and India. Journal of Asian Economics, 36, 47–61. https://doi.org/10.1016/j.asieco.2015.01.001

Jack, W., & Suri, T. (2014). Risk sharing and transactions costs: Evidence from Kenya’s mobile money revolution. American Economic Review, 104(1), 183–223. https://doi.org/10.1257/aer.104.1.183

Jimoh, M. Y., Bikam, P., & Chikoore, H. (2021). The influence of socioeconomic factors on households’ vulnerability to climate change in semiarid Towns of Mopani. South Africa. Climate, 9(1), 13. https://doi.org/10.3390/cli9010013

Joint Research Centre-European Commission, 2008. Handbook on constructing composite indicators: methodology and user guide. OECD publishing.

Kadir, N. B. Y. A., & Bifulco, A. (2013). Insecure attachment style as a vulnerability factor for depression: Recent findings in a community-based study of Malay single and married mothers. Psychiatry Research, 210(3), 919–924. https://doi.org/10.1016/j.psychres.2013.08.034

Khong, T. D., Loch, A., & Young, M. D. (2020). Perceptions and responses to rising salinity intrusion in the Mekong River Delta: What drives a long-term community-based strategy? Science of the Total Environment, 711, 134759. https://doi.org/10.1016/j.scitotenv.2019.134759

Kikuchi, S., Kitao, S., & Mikoshiba, M. (2021). Who suffers from the COVID-19 shocks? Labor market heterogeneity and welfare consequences in Japan. Journal of the Japanese and International Economies, 59, 101117. https://doi.org/10.1016/j.jjie.2020.101117

Lee, C. Y., Huang, T. S., Liu, M. K., & Lan, C. Y. (2019). Data science for vibration heteroscedasticity and predictive maintenance of rotary bearings. Energies, 12(5), 801.Available at: https://doi.org/10.3390/en12050801.

Leichenko, R., & Silva, J. A. (2014). Climate change and poverty: Vulnerability, impacts, and alleviation strategies. Wiley Interdisciplinary Reviews: Climate Change, 5(4), 539–556. https://doi.org/10.1002/wcc.287

Loc, H. H., Van Binh, D., Park, E., Shrestha, S., Dung, T. D., Son, V. H., ... & Seijger, C. (2021). Intensifying saline water intrusion and drought in the Mekong Delta: From physical evidence to policy outlooks. Science of the Total Environment, 757, 143919. https://doi.org/10.1016/j.scitotenv.2020.143919

Luu, C., von Meding, J., & Mojtahedi, M. (2019). Analyzing Vietnam’s national disaster loss database for flood risk assessment using multiple linear regression-TOPSIS. International Journal of Disaster Risk Reduction, 40, 101153. https://doi.org/10.1016/j.ijdrr.2019.101153

McElwee, P. (2010).The social dimensions of adaptation of climate change in Vietnam: The social dimensions of adaptation of climate change in Vietnam (English). Development and climate change discussion paper; no. 17 Washington, D.C.: World Bank Group. http://documents.worldbank.org/curated/en/955101468326176513/The-social-dimensions-of-adaptation-of-climate-change-in-Vietnam.

Mustafa, D., Ahmed, S., Saroch, E., & Bell, H. (2011). Pinning down vulnerability: From narratives to numbers. Disasters, 35(1), 62–86. https://doi.org/10.1111/j.1467-7717.2010.01193.x

Narayan, P. K. (2020). Has COVID-19 changed exchange rate resistance to shocks? Asian Economics Letters, 1(1), https://doi.org/10.46557/001c.17389

Nelson, G. C., Rosegrant, M. W., Koo, J., Robertson, R., Sulser, T., Zhu, T., ... & Lee, D. (2009). Climate change: Impact on agriculture and costs of adaptation (Vol. 21). Intl Food Policy Res Inst.

Ngo, Q. T. (2016). Farmers’ adaptive measures to climate change induced natural shocks through past climate experiences in the Mekong River Delta, Vietnam. https://mpra.ub.uni-muenchen.de/id/eprint/78055

Nguyen, H. H., Ngo, V. M., & Tran, A. N. T. (2021a). Financial performances, entrepreneurial factors and coping strategy to survive in the COVID-19 pandemic: Case of Vietnam. Research in International Business and Finance, 56, 101380. https://doi.org/10.1016/j.ribaf.2021.101380

Nguyen, K. A., Liou, Y. A., & Terry, J. P. (2019). Vulnerability of Vietnam to typhoons: A spatial assessment based on hazards, exposure and adaptive capacity. Science of the Total Environment, 682, 31–46. https://doi.org/10.1016/j.scitotenv.2019.04.069

Nguyen, T. A., Nguyen, B. T., Van Ta, H., Nguyen, N. T. P., Hoang, H. T., Nguyen, Q. P., & Hens, L. (2021b). Livelihood vulnerability to climate change in the mountains of Northern Vietnam: Comparing the Hmong and the Dzao ethnic minority populations. Environment, Development and Sustainability, 23(9), 13469–13489. https://doi.org/10.1007/s10668-020-01221-y

Nguyen, T. T., Nguyen, T. T., & Grote, U. (2020). Multiple shocks and households’ choice of coping strategies in rural Cambodia. Ecological Economics, 167, 106442. https://doi.org/10.1016/j.ecolecon.2019.106442

Nguyen, V. T., Cho, K. H., Mai, N. T. A., Park, J. Y., Trinh, T. B. N., Jang, M. K., ... & Le, V. P. (2022). Multiple variants of African swine fever virus circulating in Vietnam. Archives of Virology, 167(4), 1137–1140. https://doi.org/10.1007/s00705-022-05363-4

Nguyen, Y. T. B., & Leisz, S. J. (2021). Determinants of livelihood vulnerability to climate change: Two minority ethnic communities in the northwest mountainous region of Vietnam. Environmental Science and Policy, 123, 11–20. https://doi.org/10.1016/j.envsci.2021.04.007

Nguyen-Thi, T., Pham-Thi-Ngoc, L., Nguyen-Ngoc, Q., Dang-Xuan, S., Lee, H. S., Nguyen-Viet, H., ... & Rich, K. M. (2021). An assessment of the economic impacts of the 2019 African swine fever outbreaks in Vietnam. Frontiers in veterinary science, 8, 686038. https://doi.org/10.3389/fvets.2021.686038

Noy, I., & Vu, T. B. (2010). The economics of natural disasters in a developing country: The case of Vietnam. Journal of Asian Economics, 21(4), 345–354. https://doi.org/10.1016/j.asieco.2010.03.002

Opiyo, F. E., Wasonga, O. V., & Nyangito, M. M. (2014). Measuring household vulnerability to climate-induced stresses in pastoral rangelands of Kenya: Implications for resilience programming. Pastoralism, 4(1), 1–15. https://doi.org/10.1186/s13570-014-0010-9

Patricola, C. M., & Cook, K. H. (2011). Sub-Saharan Northern African climate at the end of the twenty-first century: Forcing factors and climate change processes. Climate Dynamics, 37(5), 1165–1188. https://doi.org/10.1007/s00382-010-0907-y

Pham, L. M., Parlavantzas, N., Le, H. H., & Bui, Q. H. (2021). Towards a Framework for High-Performance Simulation of Livestock Disease Outbreak: A Case Study of Spread of African Swine Fever in Vietnam. Animals, 11(9), 2743. https://doi.org/10.3390/ani11092743

Pham, N. T. T., Nong, D., Sathyan, A. R., & Garschagen, M. (2020). Vulnerability assessment of households to flash floods and landslides in the poor upland regions of Vietnam. Climate Risk Management, 28, 100215. https://doi.org/10.1016/j.crm.2020.100215

Phuong, L. T. H., Biesbroek, G. R., Sen, L. T. H., & Wals, A. E. (2018). Understanding smallholder farmers’ capacity to respond to climate change in a coastal community in Central Vietnam. Climate and Development, 10(8), 701–716. https://doi.org/10.1080/17565529.2017.1411240

Pichler, A., & Striessnig, E. (2013). Differential vulnerability to hurricanes in Cuba, Haiti, and the Dominican Republic: the contribution of education. Ecology and society, 18(3). https://www.jstor.org/stable/26269356

Praveen, B., & Sharma, P. (2019). A review of literature on climate change and its impacts on agriculture productivity. Journal of Public Affairs, 19(4), e1960. https://doi.org/10.1002/pa.1960

Putra, I. G. N. E., Pradnyani, P. E., & Parwangsa, N. W. P. L. (2019). Vulnerability to domestic physical violence among married women in Indonesia. Journal of Health Research, 33(2), 90–105. https://doi.org/10.1108/JHR-06-2018-0018

Qui, N. H., Guntoro, B., Syahlani, S. P., & Linh, N. T. (2021). Factor affecting the information Sources and communication channels toward pig farmer’s perception of African swine fever in Tra Vinh province. Vietnam. Tropical Animal Science Journal, 44(2), 248–254. https://doi.org/10.5398/tasj.2021.44.2.248

Shehu, A., & Sidique, S. F. (2015). The effect of shocks on household consumption in rural Nigeria. The Journal of Developing Areas, 353–364. https://www.jstor.org/stable/24737325

Siwach, G. (2018). Unemployment shocks for individuals on the margin: Exploring recidivism effects. Labour Economics, 52, 231–244. https://doi.org/10.1016/j.labeco.2018.02.001

Smith, E. F., Keys, N., Lieske, S. N., & Smith, T. F. (2015). Assessing socio-economic vulnerability to climate change impacts and environmental hazards in New South Wales and Queensland. Australia. Geographical Research, 53(4), 451–465. https://doi.org/10.1111/1745-5871.12137

Song, P., Zhang, X., Zhao, Y., & Xu, L. (2020). Exogenous shocks on the dual-country industrial network: A simulation based on the policies during the COVID-19 pandemic. Emerging Markets Finance and Trade, 56(15), 3554–3561. https://doi.org/10.1080/1540496X.2020.1854723

Striessnig, E., Lutz, W., & Patt, A. G. (2013). Effects of educational attainment on climate risk vulnerability. Ecology and Society, 18(1). http://www.jstor.org/stable/26269263

Sur, J. H. (2019). How far can African swine fever spread?. Journal of veterinary science, 20(4). DOI: https://doi.org/10.4142/jvs.2019.20.e41

Tabler, J., & Geist, C. (2021). Do gender differences in housework performance and informal adult caregiving explain the gender gap in depressive symptoms of older adults? Journal of Women and Aging, 33(1), 41–56. https://doi.org/10.1080/08952841.2019.1681243

Thabane, K. (2015). Determinants of vulnerability to livelihood insecurity at household level: Evidence from Maphutseng, Lesotho. Journal of Agricultural Extension, 19(2), 1–20. https://doi.org/10.4314/jae.v19i2.1

Tiwari, S., & Zaman, H. (2010). The impact of economic shocks on global undernourishment. World Bank Policy Research Working Paper, (5215). https://papers.ssrn.com/abstract=1559733

Tran, D. D., Dang, M. M., Du Duong, B., Sea, W., & Vo, T. T. (2021). Livelihood vulnerability and adaptability of coastal communities to extreme drought and salinity intrusion in the Vietnamese Mekong Delta. International Journal of Disaster Risk Reduction, 57, 102183. https://doi.org/10.1016/j.ijdrr.2021.102183

Tran, P. T., Vu, B. T., Ngo, S. T., Tran, V. D., & Ho, T. D. (2022). Climate change and livelihood vulnerability of the rice farmers in the North Central Region of Vietnam: A case study in Nghe An province. Vietnam. Environmental Challenges, 7, 100460. https://doi.org/10.1016/j.envc.2022.100460

Ubilava, D., Atalay, K., & Hastings, J. V. (2021). Commodity Price Shocks and the Seasonality of Conflict (No. 2021–03).

UNDP, 2022. Human development reports 2021–22, https://hdr.undp.org/content/human-development-report-2021-22

Vietnam Disaster Management Authority. 2021. Statistics of damage caused by natural disasters. https://phongchongthientai.mard.gov.vn/Pages/Thong-ke-thiet-hai.aspx.

Visser, H., Petersen, A. C., & Ligtvoet, W. (2014). On the relation between weather-related disaster impacts, vulnerability and climate change. Climatic Change, 125(3), 461–477. https://doi.org/10.1007/s10584-014-1179-z

Vu, T. T., & Ranzi, R. (2017). Flood risk assessment and coping capacity of floods in central Vietnam. Journal of Hydro-Environment Research, 14, 44–60. https://doi.org/10.1016/j.jher.2016.06.001

Walugembe, P., Wamala, R., Misinde, C., & Larok, R. (2019). Child and household social-economic vulnerability: Determinants transition from moderate and critical vulnerability levels in rural Uganda. Childhood Vulnerability Journal, 2(1), 29–50. https://doi.org/10.1007/s41255-020-00011-y

Yu, B., Zhu, T., Breisinger, C., & Hai, N. M. (2010). Impacts of climate change on agriculture and policy options for adaptation. International Food Policy Research Institute (IFPRI).

Yusuf, A. A., & Francisco, H. (2009). Climate change vulnerability mapping for Southeast Asia. http://hdl.handle.net/10625/46380

Zhou, L., Sibanda, M., Musemwa, L., & Ndhleve, S. (2016). Vulnerability to climate change related disasters in the Eastern Cape Province: An application of the Household Vulnerability Index (HVI). Journal of Human Ecology, 56(3), 335–353. https://doi.org/10.1080/09709274.2016.11907071

Acknowledgments

We would like to thank the editor and reviewers for their constructive comments and suggestions that helps us to improve the manuscript. This research is funded by University of Economics Ho Chi Minh City, Viet Nam.

Funding

This research was funded by University of Economics Ho Chi Minh City, Viet Nam.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

The authors declare no conflict of interest.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Springer Nature or its licensor (e.g. a society or other partner) holds exclusive rights to this article under a publishing agreement with the author(s) or other rightsholder(s); author self-archiving of the accepted manuscript version of this article is solely governed by the terms of such publishing agreement and applicable law.

About this article

Cite this article

Khai, T.T., Nguyet, V.T.A. Assessing the impact of shocks on household vulnerability: evidence from rural areas in Vietnam. Environ Dev Sustain (2024). https://doi.org/10.1007/s10668-023-04429-w

Received:

Accepted:

Published:

DOI: https://doi.org/10.1007/s10668-023-04429-w