Abstract

By means of stochastic volatility in the mean model to allow for time-varying parameters in the conditional mean and quarterly data for the G7 countries, this article examines the dynamic nexus between the volatility of output and economic growth for the G7 countries. This approach allows us to model parameter time-variation so as to reflect changes in the effect of volatility appearing in both the conditional mean and the conditional variance. The evidence in this article indicates that the effect of output volatility on output growth is strongly time-varying and quite analogues for all the G7 countries, with a break around 1973. The effect of output volatility on growth becomes more negative after 1973, with negative and statistically significant estimates after 1973 or early 1990s. Our estimates show a reversal of the declining trend and a significant increase in output volatility in the late-2000s, indicating that the Subprime Crisis brought a temporary break in the Great Moderation. However, the Great Moderation seems to be generally restored by the mid-2010s. The effect of output growth on output volatility is insignificant for all countries except for Italy and the US, for which the estimates are positive and statistically significant. Our estimates also show that output volatility is counter-cyclical for all countries.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

A large body of macroeconomic literature considers short-run fluctuations in output and long-run growth as independent. This assumption is a standard textbook stylized fact and all macroeconomic textbooks study short-run variability in output and long-run growth as separate phenomena. For instance, the models of “new macro-consensus” (see e.g. Taylor 2000) define short-run output volatilityFootnote 1 as deviations from long-run trend output. Long-run trend and short-run output volatility are considered as two independent components. Extensive empirical literature on economic growth also rarely considers short-run output volatility as an explanatory variable for economic growth (Barro 1991; Barro and Sala-i-Martin 1992; Mankiw et al. 1992; Sala-i-Martin 1994). This traditional macroeconomic approach, however, has been challenged by the real business cycle theory (Kydland and Prescott 1982; Long and Plosser 1983; King et al. 1988), which considers output volatility as an optimal response by economic agents to stochastic technological changes. The prominent studies of Kydland and Prescott (1982), Long and Plosser (1983) and King et al. (1988) integrate the real business cycle (RBC), i.e. the short-run output volatility and economic growth.

Although the recent theoretical and empirical literature, following the RBC, considers that short-run output volatility (uncertainty) might affect long-run growth, theories are in sharp contrast in terms of their prediction on direction of the effect. The first group of studies argues that output volatility harms economic growth (Bernanke 1983; Pindyck 1991; Ramey and Ramey 1991; Stiglitz 1993; Martin and Rogers 1997, 2000a, b; Blackburn and Pelloni 2005), implying a negative effect of output volatility on economic growth. This argument is often attributed to KeynesFootnote 2 and used to support stabilization policies. Second, some theories, usually in the tradition of the neo-Schumpeterian economic growth models, predict a positive relationship between economic growth and output volatility (Solow 1956; Sandmo 1970; Mirman 1971; Black 1987; Bean 1990; Dellas 1991; Aghion and Howitt 1992; Saint-Paul 1993, 1997; Aghion and Saint-Paul 1998a, b; Caballero and Hammour 1996; Blackburn 1999; Andreou et al. 2008). Third, there exist other models predicting that output growth and output volatility are more or less independent, adding more ambiguity to already confusing literature. For instance, Friedman’s (1977) view of business cycles (see e.g. De Long 2000; Taylor 2000) and misperception theory proposed by Friedman (1968), Phelps (1969), and Lucas (1972) imply an independent output growth and output volatility.Footnote 3

The theoretical literature on the relationship between output growth and its volatility did not yet settle on a conclusion, thus, the researchers focused on empirical studies to see what does the data support. Indeed, a wide empirical literature on the link between output growth and its volatility has accumulated in the last two decades. A comprehensive survey of this literature for the G7 and other developed countries is given by Caporale and McKiernan (1996), Speight (1999), Grier and Perry (2000), Henry and Olekalns (2002), Grier et al. (2004), Elder (2004), Fountas et al. (2002, 2006), Karanasos and Schurer (2005), Fountas and Karanasos (2006, 2008), Fang and Miller (2008, 2009), Fang et al. (2008), and Conrad et al. (2010), among others.

Evidence obtained in empirical studies on output growth and its volatility, analogously to the theoretical literature, has been so far inconclusive and empirical results can best be described as mixed, if not confusing. Thus, the debate on the possible link between output growth and output volatility and direction of the impact between these two have not been settled yet either theoretically or empirically.

On the theoretical side, a wide range of models provides support to all possible links mentioned above. Models following the tradition of the neo-Schumpeterian growth and business cycle model predict a positive link between output growth and output volatility, while models following the Keynesian view emphasize the role of risk and uncertainty and predict a negative relationship.Footnote 4 Results from the empirical literature even added more ambiguity to the already existing theoretical debate. There is at least one another study finding the opposite of the evidence in a paper for the same countries and the same period.Footnote 5 Our paper focuses on shedding light onto the conflicting evidence obtained in the empirical studies.

All previous empirical studies, to the best of our knowledge, assumed a constant or time-invariant relationship between output growth and output volatility. However, a number of studies (Smith 1996; Grinols and Turnovsky 1998; Turnovsky 2000; Blackburn and Galindev 2003; Blackburn and Pelloni 2004, 2005) argued that relationship between output growth and its volatility can be “bipolar” depending on the conditions.Footnote 6 Therefore, it is possible that the sign of the correlation between output growth and its volatility can change over time and a significant correlation may become insignificant during some periods. Our study differs from the previous empirical literature by explicitly specifying, in addition to its other features, a novel time-varying parameter stochastic volatility in mean (TVP-SVM) model to test the validity of time-invariant relationship assumption.

In order to measure output growth volatility, previous studies examining the causal relation between output growth and its volatility have used standard deviation (or variance) or volatility generated by the Autoregressive Conditional Heteroskedasticity (ARCH) model of Engle (1982) and the Generalized ARCH model (GARCH) of Bollerslev (1986) to proxy output growth volatility. In the GARCH models, conditional variance of unpredictable shocks to output growth series is used as output volatility. In most of the previous empirical studies (see e.g. Caporale and McKiernan 1998; Speight 1999; Grier and Perry 2000; Fountas et al. 2002, 2004, 2006; Henry and Olekalns 2002; Blackburn and Pelloni 2004; Grier et al. 2004; Karanasos and Schurer 2005; Fountas and Karanasos 2006, 2008; Fang et al. 2008; Fang and Miller 2008; Conrad et al. 2010; Denis and Kannan 2013; Haddow et al. 2013, among others), volatility is specified as a GARCH model, which has a deterministic volatility generating mechanism.

The stochastic volatility (SV) model used in our study, on the other hand, allows uncertainty in the volatility process by allowing stochastic volatility shocks. Hence, the SV model does not impose restrictions on conditional moments, while the GARCH model does, as stated by Meddahi and Renault (2004). Moreover, the SV model usually has a better in-sample fit as well as out-of-sample forecasts (Danielsson 1994; Kim et al. 1998).

Against this backdrop, the main objective of this study is to determine the dynamic linkages between output growth and its volatility for the G7 countries using a time-varying parameter stochastic volatility in the mean model. Our paper contributes to the existing literature in three ways.

First, in contrast to previous studies that consider only models with constant coefficients in the conditional mean, the time-varying parameter model that we use permits us to assess whether the dynamic nexus between the output growth and output growth volatility has changed over time. Using a time-varying parameter stochastic volatility in the mean model, we, therefore, contribute to the existing literature by allowing a time-varying impact of output volatility on output growth. Our study is the first in the literature, to the best of our knowledge, which considers a time-varying impact of output volatility on growth. We build on the Bayesian TVP-SVM model approach of Chan (2017) and allow time-varying volatility effect on growth, optimally allowing time-varying effects and, therefore, robustly account for structural breaks.

Second, our study uses a more realistic specification to measure output uncertainty by modeling growth volatility with the SV specification. The GARCH specification used in the previous research models volatility deterministically and does not allow for volatility shocks. The absence of volatility shock limits the GARCH model’s capacity to capture the uncertainty associated with output growth. The SV model, on the other hand, allows for volatility shock and, thus, is a more realistic specification to model uncertainty.

Third, we also test for reverse causality from output growth to output volatility in a SV model specification. Most of the papers on the nexus between output growth and output volatility test causality from output volatility to output growth. However, studies by Friedman (1977), Taylor (1979), Brunner (1993), Fountas and Karanasos (2006), and Fountas et al. (2006) point out to the possibility of causality from-mostly via the mechanism involving inflation and inflation uncertainty-growth to output volatility. A few studies (Fountas et al. 2002, 2006; Fountas and Karanasos 2006, 2008; Fang et al. 2008; Conrad et al. 2010; Lee 2010; Chapsa et al. 2011) tested for the effect of output growth on output volatility, with result pointing to negative, positive or no significant effect. The literature on the link from output growth to output volatility remains rather sparse with inconclusive evidence. However, all the previous papers test the causality from growth to its volatility in a GARCH model. The GARCH model has a deterministic conditional volatility function and testing the causal effect within its inflexible structure is unrealistic. The SV model, on the other hand, allows for volatility shocks and fits better to a stochastic volatility specification. Our study is the first, to the best of our knowledge, in the literature that tests causality from output growth to its volatility in a stochastic volatility model.

The data used in this study are rates of changes in the seasonally adjusted quarterly gross domestic product (GDP) as proxy for output in the G7 countries. The sample for each country, with two exceptions of the start date, covers 1960:Q2–2017:Q2. The exceptions for the start date are the UK and the US, for which the start dates are 1955:Q2 and 1947:Q2, respectively. The results obtained in this paper show that the effect of output uncertainty on output growth is strongly time-varying, offering an explanation to conflicting results of the previous literature. Although the effect of output volatility on output growth became steadily more negative after 1973 for all the G7 countries, the coefficient has positive and insignificant ranges before 1973.

In general, the results of this paper indicate a significant evidence in support of the negative effect from output volatility to growth hypothesis (Bernanke 1983; Pindyck 1991; Ramey and Ramey 1991; Stiglitz 1993; Martin and Rogers 1997, 2000a, b; Blackburn and Pelloni 2005) particularly after 1973, with a statistically significant effect for the whole sample period (US), after 1973 (Canada, France, and Italy) or after 1990 (Germany and the UK). The overall time-varying pattern of the effect of output volatility on growth is exceptionally analogues for all the G7 countries. The minor differences, which are due to national macroeconomic policy effects, offer an explanation to conflicting results of the previous literature.

For Japan, the mean coefficient is estimated as positive before 1973 and negative afterwards, but the time-varying effect of output volatility on growth is statistically insignificant for the whole sample period. Although positive mean effect of output volatility on growth (Solow 1956; Sandmo 1970; Mirman 1971; Black 1987; Bean 1990; Dellas 1991; Aghion and Howitt 1992; Saint-Paul 1993, 1997; Aghion and Saint-Paul 1998a, b; Caballero and Hammour 1996; Blackburn 1999; Andreou et al. 2008) is estimated for France, Japan and, the UK before 1973, these estimates are not statistically significant and close to zero, indicating independence (Friedman 1968, 1977; Phelps 1969; Lucas 1972; De Long 2000; Taylor 2000) might hold before 1973 for these countries. In addition to France, Japan and the UK, the independence hypothesis is also supported for Canada before 1973, for Germany before 1990, for Italy before 1973, and for Japan for the whole sample period. However, this is based on statistical significance as estimates are negative for these countries. As estimates turn from negative to positive in 1973 for France, Japan, and the UK, we also find cases consistent with the bipolar view (Grinols and Turnovsky 1998; Turnovsky 2000; Blackburn and Galindev 2003; Blackburn and Pelloni 2004).

Overwhelmingly, the results from this study indicate substantial evidence of time variation in the impact of growth uncertainty on growth for each country. Effect of growth uncertainty on growth has become increasingly more negative for all countries, indicating that economic actors, over time, tend to react more to uncertainty. Overall, the time-varying parameter approach in our study brings an explanation for conflicting results in the previous empirical studies.

In terms of reverse causality, our results show that effect of growth on its uncertainty is statistically not different from zero, except for Italy and the US, for which the effect is positive and significant. As estimates of the coefficient for the effect of growth on its uncertainty are insignificant in most cases, our results do not indicate a significant evidence to support the reverse causality hypothesis. Thus, all the G7 countries, except Italy and the US, look analogues in terms of the effect of growth on growth uncertainty and country specific factors seem to play a negligible role on the reverse causality.

Our estimates of output volatility reveal significant results. The volatility estimates from the SV specification show a declining trend in output volatility since the mid-1980s as a result of the Great Moderation process. The volatility estimates are exceptionally counter-cyclical in all countries, with significant increased during the recessions of 1973–1974, 1991–1993, 1997–1998 and 2007–2011. The declining output volatility had a reversal in the late-2000s following the Subprime Crisis for all the G7 countries, with a significant increase in the volatility estimates. Thus, our results show that the Subprime Crisis possibly brought a temporary break to the Great Moderation. However, there is a significant reduction in output volatility again by the mid-2010s in most countries, although it remains high for Canada and France, indicating restoration of the Great Moderation. We also find that output volatility is highly persistent for all countries.

The paper is outlined as follows: Sect. 2 reviews the theoretical literature while empirical literature is reviewed in Sect. 3. Section 4 introduces the methodology and Sect. 5 reports the empirical results. Section 6 discusses how our findings relate to previous literature. Section 7 presents the conclusion.

2 Theoretical background

Following the RBC theory, recent theoretical and empirical literature highlights that short-run output volatility may have impact on long-run growth. However, as far as direction of the effect is concerned, the theories make conflicting predictions. The first group of studies maintains that economic growth is affected adversely by output volatility (Bernanke 1983; Pindyck 1991; Ramey and Ramey 1991) and that output volatility even impairs economic growth. This debate, which is often attributed to Keynes, is used to provide a basis for stabilization policy.

On the other hand, the second group of studies, which have been generally advanced following the tradition of the neo-Schumpeterian economic growth models, predict a positive relationship between economic growth and business cycle volatility (Solow 1956; Sandmo 1970; Mirman 1971; Black 1987; Bean 1990; Dellas 1991; Aghion and Howitt 1992; Saint-Paul 1993, 1997; Aghion and Saint-Paul 1998a, b; Caballero and Hammour 1996; Blackburn 1999; Andreou et al. 2008).

The third group of studies, on the other hand, argue that output growth and output volatility are almost independent, which makes the already complicated and inconclusive literature even more complicated and controversial. For instance, business cycles approach of Friedman (1977) (see e.g. de Long 2000; Taylor 2000) and also the misperception theory proposed by Friedman (1968), Phelps (1969) and Lucas (1972) point to an independent output growth and business cycle volatility, i.e., an independent output volatility and output growth. Put differently, these two variables do not affect each other. Some business cycle models suggest that price misperceptions lead to output fluctuations around the natural rate as a reaction to monetary shocks. On the other hand, real factors like technology are responsible for changes in output growth rate (Friedman 1968). Solow (1997), one of the more traditional Keynesians, argues that output growth and its volatility (business cycle component) can and should be categorized into two essential components that need to be examined independently.

Today, there is a growing body of theoretical literature maintaining that interaction between average output growth and its variability in an endogenous growth set-up (Smith 1996; Grinols and Turnovsky 1998; Turnovsky 2000; Blackburn and Galindev 2003; Blackburn and Pelloni 2004, 2005) is “bipolar”, i.e., either positive or negative, depending on the presence and type of certain conditions. Impact of output volatility on growth is not always obvious. As some studies (Smith 1996; Grinols and Turnovsky 1998; Turnovsky 2000) put forward, there is a positive relationship between growth rate and volatility when preferences are represented by a constant elasticity utility function and as long as risk aversion coefficient exceeds the unity. Smith (1996) highlights that whether intertemporal elasticity of substitution exceeds or falls short of the unity determines whether growth-volatility relationship will be positive or negative.

All the studies mentioned above assume a closed economy. In a stochastic general equilibrium small-open economy model of a developing country, Turnovsky and Chattopadhyay (2003) investigate effect of output volatility on growth. Turnovsky and Chattopadhyay (2003) include three more variability types in their model concerning trade, government spending, and money supply. Turnovsky and Chattopadhyay (2003) show that output volatility has an ambiguous effect on growth. This finding was also supported by numerical simulations which indicate that effect is small. Furthermore, Blackburn and Galindev (2003) investigate whether correlations between growth and its volatility will be positive or negative, considering effect of the source of technological change. They show, using a stochastic real growth model, that a positive correlation is likely to be observed when agents increase their productive efficiency by devoting time to learning or dissemination of knowledge.

As indicated by Blackburn and Pelloni (2004) in a stochastic monetary growth model, type of shocks that continuously hit an economy determine the correlation between growth and its variability. The results of their study reveal that the dominance of real (nominal) shocks determines whether the correlation will be positive (negative). Using the same model in a richer setting, Blackburn and Pelloni (2005) examine three different types of shocks, namely, technology, preferences, and monetary shocks, affecting output continuously as a result of wage contracts and technology. They find a negative correlation between output growth and output variability irrespective of the type of shock causing fluctuations in the economy.

The negative correlation between output variability and average growth is based on Keynes’s (1936) argument that when estimating revenues they will receive, entrepreneurs consider fluctuations in economic activity. Larger output fluctuations point to investment projects with higher perceived risks and consequently lower demand for investment, leading to lower output growth. Woodford (1990) obtains a similar result on sunspot equilibria, that the growth may be adversely influenced by output variability. Higher volatility in output growth brings unforeseen changes in output growth and leads to ambiguous future demand for the products of a firm. As a result, firms may choose to invest in plant and equipment less because of these increased risks and, consequently, capital stock growth rates and output decrease as the demand for investment declines. Investment irreversibilities at the firm level lead to a negative relationship between output volatility and growth as proposed by Bernanke (1983), Pindyck (1991), and Ramey and Ramey (1991). This implies that output volatility and, thus, uncertainty lead to a reduction in average output growth. Higher output volatility and planning errors resulting from uncertainty may cause suboptimal ex-post output levels and lower mean output and growth in firms when there is a commitment to technology (Ramey and Ramey 1991).

Finally, two economic theories could account for the positive impact of output volatility on growth. According to the first theory—Solow’s (1956) neoclassical growth theory—higher levels of income volatility (uncertainty) means higher savings rate (Sandmo 1970) and, thus, a higher economic growth rate equilibrium. Another explanation, which has been provided by Black (1987), asserts that firms invest in riskier technologies only if they believe that they can compensate for the extra risk with a larger income from their investments (average rate of output growth). In order to observe the effects of such investments, empirical studies using low-frequency data may be conducted as it takes time to realize investments. Furthermore, as Bean (1990) and Saint-Paul (1993) maintain, long-run growth is promoted as higher volatility enhances inventive activity. However, this argument is based on the predictability of volatility, which eliminates uncertainty. More recently, by using a model of endogenous growth that rests on the theory of learning-by-doing, Blackburn (1999) demonstrates that business cycle volatility promotes long-run growth.

There are also theories on the reverse causality from output growth to output volatility with opposite views. The first group of studies argues that higher levels of output growth rate cause higher output volatility, which is usually related to the mechanism working through the channel of inflation and inflation uncertainty. Fountas et al. (2006) point out that the effect of output growth on output volatility is related to interaction of three effects, namely, the Phillips curve, Friedman, and Taylor effects. The Phillips curve effect arises when higher output growth leads to higher inflation, i.e., the short-run Philipps curve effect. Higher inflation, in turn, may lead to higher inflation uncertainty, the so-called Friedman effect (Friedman 1977). Finally, higher inflation variability may lead to higher output variability via the second-order Philipps-curve effect, which is also known as the Taylor effect (Taylor 1979). The second group of studies uses the monetary authority behavior assumption of Brunner (1993) to infer a negative effect from output growth to output volatility. If monetary authorities respond to increased growth and use anti-inflationary policies, this will lead to reduced inflation uncertainty in reference to future inflation. Therefore, real uncertainty will increase in response to reduced nominal uncertainty, i.e., the Taylor effect.

3 Empirical evidence

Analogous to theoretical literature, evidence in empirical literate concerning link between output growth and its variability is not conclusive. Early studies that utilize cross-sectional (Kormendi and Meguire 1985) or pooled (Grier and Tullock 1989) data showed existence of a positive link between the two constructs. In their study including a panel of 92 countries and a sample of OECD countries for the period between 1960 and 1985, Ramey and Ramey (1995) find that when countries have higher output variability, they have lower growth. Another study by Zarnowitz and Moore (1986), in which the 1903–1981 period was divided into six sub-periods and high and low growth periods were compared in terms of output variability (measured by standard deviation of annual growth rate in real GNP), also show a similar result to that of the Ramey and Ramey’s (1995) study. More recently, Kneller and Young (2001) conduct a study using panel-data and demonstrate that output variability reduces growth. Furthermore, Turnovsky and Chattopadhyay (2003) reveal, in their study on 61 developing countries that, although small, different types of volatility may have an effect on growth. In an empirical study using panel data on 60 countries, Baker and Bloom (2013) show that volatility effects growth negatively.

Relationship between output variability and average growth was investigated by early empirical studies and findings are mixed. Rather than output variability measured by variance or standard deviation, more recent studies focus on output volatility and measure it by the conditional variance of unanticipated shocks to output growth estimated by GARCH models. Evidence from different (mostly the US) data sets and GARCH models is also fairly inconclusive. In their study conducted using the US data, Caporale and McKiernan (1998) and Grier and Perry (2000) reveal that output volatility affects growth positively, whereas Henry and Olekalns (2002) point to a negative effect. Speight (1999), on the other hand, obtains no evidence regarding the association between output volatility and growth in the UK. In a study conducted using the US data and allowing for asymmetries, Grier et al. (2004) show that output volatility has a positive effect on growth. In their study, Fountas et al. (2002) used data on Japan and a bivariate GARCH model including inflation and growth to investigate the effect of output volatility on growth. Similar to Speight (1999), they also obtain no evidence regarding the effect of output volatility on growth.

In a subsequent study, Fountas et al. (2004) use data from Japan and three different univariate GARCH models and confirm this finding. In a study conducted in 2006 on G7 countries, Fountas et al. (2006) obtain evidence supporting the positive output volatility-output growth hypothesis (Solow 1956; Sandmo 1970; Mirman 1971; Black 1987; Bean 1990; Dellas 1991; Aghion and Howitt 1992; Saint-Paul 1993, 1997; Aghion and Saint-Paul 1998a, b; Caballero and Hammour 1996; Blackburn 1999; Andreou et al. 2008) in all G7 countries except Japan. All the studies that have been cited so far adopt a univariate or multivariate GARCH approach. The only study that uses low-frequency (annual) data and thus provides a more appropriate test is the Caporale and McKiernan’s (1998) study, which finds support for the Black’s (1987) business cycle hypothesis (a positive effect of output volatility on output growth).

Furthermore, almost all the studies reviewed here concentrate only on the causal effect of output volatility on growth. However, the correlation between output growth and its volatility may also result from the causal effect of growth on output growth volatility. Some researchers investigate this opposite causality relationship as well (e.g. Blackburn and Pelloni 2004). However, this relationship requires more empirical investigation because only Karanasos and Schurer (2005), Fountas and Karanasos (2006), and Fountas et al. (2006) have focused on such a relationship so far.

Using monthly data pertaining to Italy for the 1962–2004 period, Karanasos and Schurer (2005) find a strong negative bidirectional relationship between growth and output growth volatility. The study by Fountas and Karanasos (2006), on the other hand, uses historical data on five European countries and reveals that in four of these countries growth affects volatility negatively. Similarly, in their study conducted for three G7 countries, namely Japan, the US and Germany, Fountas et al. (2006) find that output growth has a statistically significant negative effect on output volatility. Furthermore, in their study conducted to investigate the relationship between output growth and its volatility, Fountas and Karanasos (2008) use a long series of annual data on five European countries, namely, France, Germany, Italy, Sweden, and the UK, covering a period over 100 years. The findings of the study reveal that more uncertainty about output leads to a higher growth rate in three of the five countries, while output growth decreases uncertainty about output in all the countries except one, Sweden. On the other hand, Fang et al. (2008) indicate that uncertainty about output growth affects output volatility negatively only in Japan out of the six G7 countries (excluding France).

Taking the possible effects of structural changes in the volatility process into consideration, Fang and Miller (2008) examine the impact of the Great Moderation on the relationship between the US output growth and its volatility for the period between 1947 and 2006. Empirical findings of this study show no significant relationship between output growth rate and its volatility. This finding coincides with the traditional wisdom of dichotomy in macroeconomics. Moreover, the evidence suggests that when a one-time structural break is integrated with the unconditional variance of output, time-varying variance displays a significant decline or disappears starting in 1982 or 1984. In addition, as Fang and Miller (2009) maintain, for the case of Japan, output growth has no significant effect on output volatility and vice versa after correcting for outliers and structural shifts.

As previously argued by Pindyck (1991), Bredin and Fountas (2009) assert that in the majority of the European Union (EU) countries, output growth uncertainty is negatively related to the average growth rate. These findings have important implications for the development of macroeconomic theory, as it has recently been highlighted that economic growth and business cycle variability should be analyzed simultaneously in macroeconomic modelling (Blackburn and Pelloni 2005). In their study conducted on the UK, Conrad et al. (2010) find that whether variability affects growth positively or not depends on the included lag of the variability measure. In contrast to Conrad et al.’s (2010) finding, Denis and Kannan (2013) and Haddow et al. (2013) present evidence that output volatility has a negative effect on growth in the UK. The heterogenous results in the existing literature on the relationship between uncertainty and growth point to the need for further empirical studies, which our study aims to fulfill.

4 Methodology

As it is clear from the previous studies available in the literature, most economic and financial time series display structural instability (also see, for instance, Canova 1993; Cogley and Sargent 2001; Koop and Potter 2007). A method commonly used in modelling this structural instability is the time-varying parameter (TVP) model. In such models, parameters in the conditional mean can change through time. Studies conducted recently on time series emphasize the importance of time-varying volatility in macroeconomic and financial time series and likely misleading conclusions when the time-varying feature of the data is ignored. In such models, heteroscedastic errors are usually modelled by using stochastic volatility specification (see, for instance, Cogley and Sargent 2005; Primiceri 2005). It was demonstrated in D’Agostino et al. (2013) in relation to macroeconomic forecasts that both structures (time-varying parameter and stochastic volatility) have a significant influence on generating precise forecasts. Chan (2017) developed a univariate time series model with time-varying parameters and stochastic volatility in order to investigate the time-varying effects of stochastic volatility on the level of a time series. The model developed by Chan (2017) is based on Koopman and Hol Uspensky’s (2002) volatility in the mean (SVM) model. Koopman and Hol Uspensky’s (2002) volatility in the mean (SVM) model was, indeed, developed for financial time series as an alternative to Engle et al. (1987) ARCH in the mean (ARCH-M) model. Our study uses the TVP-SVM model of Chan (2017) in order to investigate the dynamic effect of output uncertainty on output growth. We additionally allow lagged output growth to affect the output volatility.

An optimal approach for modelling structural instability is the time-varying parameter (TVP) approach in which some parameters of a model evolve over time in a stochastic manner. In this paper, we allow the impact of output volatility on output growth to be time-varying, capturing any structural instability in the macroeconomic environment that may alter output volatility-output growth relationship. The stochastic volatility (SV) model of Koopman and Hol Uspensky (2002) fits better to time series with conditional heteroskedasticity. Compared to the GARCH models, volatility in the SV model is specified as a latent stochastic process that allows volatility shocks. In this study, we combine the TVP and SV approaches that robustly allow structural breaks and volatility shocks. Additionally, we allow past (lagged) output growth affect output uncertainty. The TVP-SV model used in our study is proposed by Chan (2017) and specified as follows:

where \(\varvec{\theta}= \left( {\tau_{t} ,\alpha_{t} } \right)'\), \(\varvec{\varOmega}\) is a \(2 \times 2\) covariance matrix and \(\varvec{\nu}_{t}\) is \(2 \times 1\) vector of independently, identically and normally distributed (IID) errors. \(\varepsilon_{t}\) and \(\xi_{t}\) are also IID morally distributed error terms. We assume that \(\varepsilon_{t}\), \(\xi_{t}\) and \(\varvec{\nu}_{t}\) are mutually uncorrelated. The log volatility \(h_{t}\) follows a stationary ARX(1) process with \(\phi < 1\). In the model given in Eqs. (1)–(3), \(\exp \left( {h_{t} } \right)\) is the variance of the transitory component (\(\varepsilon_{t}\)) of \(y_{t}\), therefore, we can interpret \(\alpha_{t}\) as the impact of transitory output growth volatility on the level of output growth. The parameter \(\beta\) measures the impact of output growth on its volatility. The parameter \(\phi\) is a first-order serial correlation (autoregressive) coefficient and measures persistence of output volatility. In the empirical section, the model in Eqs. (1)–(3) is estimated using the efficient Markov chain Monte Carlo (MCMC) sampler developed in Chan (2017).Footnote 7 The growth series of all the G7 countries show some varying trend over the long sample period we examine. Therefore, we specify a time-varying trend (\(\tau_{t}\)) in Eq. (1).

The process \(\left\{ {h_{t} } \right\}_{t = T}^{0}\) appearing in Eq. (2) defines the log conditional variance and unobserved and, thus, it is a latent process with initial state \(h_{0}\) distributed according to a stationary autoregressive process of order 1, AR(1). The latent process \(\left\{ {h_{t} } \right\}\) arises as an approximation to stochastic volatility diffusion of Hull and White (1987) and Chesney and Scott (1989) and, therefore, based on a well-developed theory. This latent process defined in Eq. (2) is also more consistent with unobservable volatility. Volatility is the result of flow of news into markets and not directly observable. Thus, interpreting the latent volatility process \(\left\{ {h_{t} } \right\}\) as representing random and uneven flow of new information is convenient, because it is very difficult, if not impossible, to model information flow directly. This interpretation of the stochastic volatility model is proposed by Clark (1973) and Tauchen and Pitts (1983), which is more realistic than conditional variance of the GARCH models as a measure of volatility. As shown by Taylor (1986, 1994), the SV models can be seen as analogous to continuous time option pricing models and, therefore, fit naturally well into the theoretical framework most of the finance theory has been developed on.

The SV model has some unique features that makes it more attractive in modeling volatility dynamics compared to other models such the GARCH. The conditional volatility in GARCH models is perfectly and deterministically explained by past observations, whereas the SV model allows additional uncertainty in volatility by introducing stochastic shock term \(\xi_{t}\) in Eq. (2). An important consequence of this feature of the SV models is the absence of any moment restriction requirements (see e.g. Meddahi and Renault 2004), which is an important requirement in the GARCH model and reduces its flexibility. The absence of moment restrictions in the SV model implies that it can have better in sample fit than the GARCH model and likely to give better forecasts unlike the GARCH model, which are known with their poor out of sample forecasting performance (Danielsson 1994; Kim et al. 1998). Although they look simple in their dynamic property with an AR(1) specification, SV models are, indeed, quite flexible in their capacity to model persistence in volatility. Granger and Newbold (1976) show that autocorrelations of the log volatility process \(\left\{ {h_{t} } \right\}\) implies an autoregressive moving average process for the square of \(y_{t}\) with orders (1,1), i.e. ARMA(1,1), and, therefore, can capture high persistence. Therefore, the AR(1) structure in Eq. (2), when all components of the model are considered, is not restrictive in terms of volatility persistence and, indeed, more flexible than a GARCH(1,1) process (Davidian and Carroll 1987; Shephard 1996).

5 Empirical results

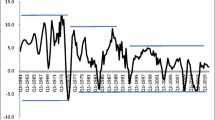

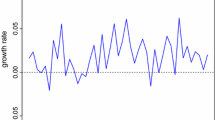

In our empirical analysis, we investigate the relationships between real output growth and output growth volatility of the G7 countries, namely Canada, France, Germany, Italy, Japan, the UK and the US using the seasonally adjusted GDP as a proxy for output growth. The data are at the quarterly frequency for 1960:Q2–2017:Q2 period for Canada, France, Germany, Italy and Japan, for 1955:Q2–2017:Q2 period for the UK, and for 1947:Q2–2017:Q2 period for the US, respectively. Data were obtained from the Organisation for Economic Co-operation and Development (OECD). The quarterly GDP growth series is calculated as \(y_{t} = \ln \left( {X_{t} /X_{t - 1} } \right)*100\), where \(X\) is the real GDP. The real output growth series (\(y_{t}\)) for the G7 countries are shown in Fig. 1.

Time series of output growth

We report the descriptive statistics for the quarterly output growth series in percent in Table 1. The descriptive statistics reported in Table 1 are the mean, standard deviation (S.D.), minimum (min), maximum (max), skewness and excess kurtosis statistics, the Jarque–Bera normality test (JB), the Ljung–Box first [Q(1)] and the fourth [Q(4)] autocorrelation tests and the first [ARCH(1)], and the fourth [ARCH(4)] order Lagrange multiplier (LM) tests for the ARCH effect. \(n\) shows the number of observations for output growth series of the G7 countries. Firstly, the mean of output growth series for Canada, France, Germany, Italy, Japan, the UK and the US are 0.776, 0.675, 0.614, 0.603, 0.953, 0.604 and 0.782, respectively. This shows that average output growth is the lowest for Italy and the highest for Japan. Secondly, considering the values of the S.D. of output growth series, we observe that output growth volatility is the highest in Japan (1.309), while it is the lowest in Canada (0.882).

The values of skewness statistics show that output growth series of Canada, Germany, Japan and the US are skewed to the left, while it indicates a positive skewness for France, Italy and the UK, meaning that the distributions of the output growth series of France, Italy and the UK are skewed to the right. The excess kurtosis statistics reveal that all growth series are fat-tailed, indicating a higher than normal probability of large positive and negative output growth rate realization. Moreover, the values of the JB statistic indicate a deviation from normality for all series. The JB test statistic values show that output growth series has strongly non-normal distributions for all countries. The values of Ljung–Box for autocorrelation an LM statistic for the ARCH effect show there is serial correlation and ARCH effects in the growth series of all the G7 countries.

To test the stationarity properties of the output growth series, we use the augmented Dickey–Fuller (ADF) test of Dickey and Fuller (1979) and Said and Dickey (1984), Kwiatkowski–Phillips–Schmidt–Shin (KPSS) test of Kwiatkowski et al. (1992), Generalized-Least Squares differenced Dickey–Fuller (DF-GLS) test of Elliott et al. (1996), and Ng-Perron (MZa and MZt) unit root tests of Ng and Perron (2001). Table 2 reports unit root test results for output growth in all countries. Lag orders for the ADF and DF-GLS tests are selected using the Schwarz information criterion (SCB). The long-run variance in the KPSS and Ng-Perron tests is estimated using the quadratic spectral kernel suggested by Andrews (1991) in conjunction with the Andrews (1991) automatic bandwidth selection procedure.

Table 2 reports two versions of all tests, one with only a constant in the deterministic component given in panel A of Table 1 and the other with both a constant and a linear trend in the deterministic component given in panel B of Table 2. From panels (A) and (B) of Table 2, it is seen that the nonstationary null hypothesis is rejected for the output growth series using the ADF, DF-GLS, MZa and MZt test at conventional significance levels for all of the countries, except for Canada for which the DF-GLS does not reject the nonstationarity. Panels (A) and (B) of Table 2 also presents results for the KPSS test, which takes stationarity as the null hypothesis. The evidence from panels (A) and (B) of Table 2 show that the stationarity null hypothesis is rejected at the 5% level for Canada, France, Germany, and Italy when only a constant is included in the test regression, while the stationary null is rejected at the 5% level for France and Japan when a constant plus a linear trend is included in the test regression. The results in Table 2 shows that the KPSS test does not agree with others and its conclusions vary with the specification of the deterministic component. The KPSS test results are sensitive to the specification of the deterministic trend component. Therefore, we make our model specification robust against this by including a time-varying trend component in Eq. (1).Footnote 8

Results of the posterior moments and quantiles of the TVP-SV in the mean model parameter estimates are reported in Table 3. Estimates, standard errors, and 90% credible intervals are obtained using the efficient MCMC based on band and sparse matrix algorithm of Chan (2017). From the estimates of the coefficient \(\beta\), we observe that growth series has a negative but statistically insignificant effect on the real volatility as predicted by Pindyck (1991) and Blackburn and Pelloni (2005) for France. However, the results show that the effect of growth on its uncertainty is, although positive as predicted by Mirman (1971), Black (1987), and Blackburn (1999), for Canada, Germany, and the UK, the estimates are statistically not different from zero. Growth has a positive and significant effect on its volatility only for Italy and the US. Thus, the evidence on the reverse causality from growth to its volatility is only significant for Italy and the US. Our results do not show any significant evidence for the reverse causality from growth to its uncertainty.

Figure 2 presents estimates of \(h_{t}\) and \(\alpha_{t}\) and the associated 90% credible intervals obtained from 50,000 posterior draws. The results in Fig. 2 encompass most of the empirical findings in the previous literature. For instance, considering the Great Moderation, the oil shock in the 1970s, the Global financial crisis and WW II (only for the US) there is substantial variability in growth volatility. The study entitled “Has the Business Cycle Changed and Why?” by Stock and Watson (2002) report a large decline in the US macroeconomic volatility during the mid-1980s, which is well confirmed by the estimates of \(h_{t}\) in Fig. 2g. This phenomenon is called the “Great Moderation” by James Stock and Mark Watson in their study (Stock and Watson 2002; Fountas et al. 2006; Fang and Miller 2008; Ozdemir 2010; Balcilar and Ozdemir 2013). What is more, the Great Moderation is a reduction in the volatility of business cycle fluctuations beginning in the mid-1980s. These have been caused by institutional and structural changes in developed countries in the later part of the twentieth century.

Evolution of volatility and impact of volatility on growth. Note: The figure plots the evolution of the log output volatility \(h_{t}\) (left panel) and the time-varying impact of the output volatility on output growth \(\alpha_{t}\) (right panel). The solid lines are the estimated posterior means and the shaded regions denote the 90% credible confidence intervals. The results are based on 50,000 posterior with a burn-in period of 50,000

Parallel to the dynamics in volatility of business cycle fluctuations, major economic variables such as real gross domestic product growth, industrial production, employment rate, unemployment rate and inflation rate in developed countries began to decline in volatility starting around the mid-1980s. The dynamics of the output volatility \(h_{t}\) reported in the left panel of Fig. 2 show us that there is a decline in the output volatility of the G7 countries in the early 1980s compared to the periods before the 1980s.Footnote 9 Furthermore, it can be stated that output volatility has become more stable during the mid-1980s and also during the late 2000s than it was before the 1980s as a result of the Great Moderation. However, output volatility peaks again similar to the dynamics before the Great Moderation following the aftermath of the Subprime Crisis (Global Financial Crisis).

The left panel of Fig. 2 shows that the output volatility in all the G7 countries significantly increased from 2007 to 2012. Although, the output volatility in Canada, France, the UK, and the US did not reach historical peak levels in this period, it did so in Germany, Italy, and Japan. Thus, the Subprime Crisis brought a significant break in the Great Moderation. But, when the output growth volatility series are examined, it is obvious that the output volatility series of the G7 countries show high reductions after the Subprime Crisis, starting around 2011. Besides, when the output volatility series for the G7 countries are examined, it is seen that output volatility in the aftermath of the Subprime Crisis period has fallen to low levels, which are comparable to the levels in the mid-1980s and the late 2000s sub-periods. Only exceptions are Canada and France, as the output growth volatility estimates for these countries, although have fallen significantly since it reached the peak level in 2009, are still higher than the levels observed during the Great Moderation. Thus, the rise in output volatility during the 2007–2011 period is a temporary and the Great Moderation seems to be restored for most of the G7 countries, if not for all. Our estimates show that the disruption in the Great Moderation period beginning in 2007 was a temporary blip and does reflect a shift to a more volatile economy going forward.

The parameter \(\phi\) measures the persistence of volatility shocks. The estimates of \(\phi\) vary from 0.961 (Japan) to 0.986 (UK), indicating very high persistence. High volatility persistence points out to the long-lasting effect of volatility shocks and challenges for stabilization policies. As the estimates of \(h_{t}\) show, the volatility shock of the Subprime Crisis indeed took a long time until the volatility could be restored to previous levels with the introduction of extensive macroeconomic stabilization policies in all the G7 countries.

According to the right panel of Fig. 2, the extent of time variation in the estimates of \(\alpha_{t}\) is substantial, underlining the significance of time-varying parameters. According to the results reported in the right panel of Fig. 2, growth uncertainty has a significant negative impact on growth following the mid-1970s for Canada, while it has an insignificant negative effect up to the early 1970s. Considering France, Japan, and the UK growth uncertainty has an insignificant positive effect on growth until the early 1970s. The estimates of \(\alpha_{t}\) for France, Japan and the UK are negative after around the early 1970s, statistically significant after the late 1980s for France and after the early 1990s for the UK, while statistically insignificant for the whole period for Japan. The estimates of \(\alpha_{t}\) for Germany are negative for the whole sample period, but it is insignificant until the early 1990s, while the impact is significantly negative after the early 1990s. For Italy, it has a significant negative effect following the beginning of the 1970s, while it has an insignificant negative effect up to the beginnings of the 1970s. For the UK, \(\alpha_{t}\) estimates are positive before the early 1970s, it is close to zero between the early 1970s and the late 1970s and it is negative after the late 1970s.

The evidence for the UK shows that growth uncertainty has a significant negative impact on growth after the late 1970s, while the impact is not significant before the late 1970s. Lastly, for the United States, the evidence indicates that growth uncertainty has a significant negative impact on growth over the entire sample period. These findings indicate that growth uncertainty has a significantly negative impact on growth as predicted by Pindyck (1991) hypothesis after about the mid-1970s for Canada and Italy and after about the early 1990s for France and the UK, with two exceptions. The exceptions are Japan and the United States, where growth uncertainty has a significantly negative impact on growth as predicted by Pindyck (1991) hypothesis for the whole sample period for the US and negative after the early 1970s but insignificant for the whole sample period for Japan.

The estimates of \(\alpha_{t}\) have a downward trend for all countries, implying that volatility has become more detrimental to growth over time. Large differences across countries in terms of the effect of volatility on output growth correspond to periods before the Great Moderation, i.e., the mid-1980s. These differences can be explained by the diverse monetary policies and structural differences across the countries before the mid-1980s. The Great Moderation brought analogues monetary policies (inflation targeting and loose monetary policy to promote growth) and other changes (such as the falling global prices, improved infrastructure, new technology, and confidence in banking) that had similar effects in all of the G7 countries, explaining the analogues effect of output volatility on growth across the countries.

The evaluation of the effect of output volatility on growth should depend primarily on macroeconomic policy, particularly on monetary policy. Thus, country-specific factors might be important. Our results show that country-specific factors only play a minor role in the effect output volatility on economic growth, because estimates of \(\alpha_{t}\) across all countries show quite similar time-varying pattern. The effect of uncertainty on the growth rates is exceptionally analogous for all the G7 countries, showing a downward trend after the start of 1987.

As we see from Fig. 2, the effect of volatility on the growth are exceptionally analogous in all G7 countries. The effect is strongly time-varying with a declining trend. Output volatility harms economic growth in all countries and the effect becomes more and more significant after the start of the Great Moderation in the early 1980s. The 2007–2008 Subprime Crisis and the ensuing Great Recession brought a break to the calm of the Great Moderation with significant increases in volatility. However, the disruption at the beginning with the 2007–2008 Subprime Crisis looks a temporary blip and does not signal a shift to a more volatile economy moving forward. Thus, the Great Moderation effect with less volatility in output continues.

However, the estimation results for the effect of output volatility on growth show that uncertainty has a continuously increasing impact on growth with the start of the Great Moderation in the early 1980s across all G7 countries. Although the calm of the Great Moderation is ensuing and the volatility level in all G7 countries is declining, the effect of the output volatility is becoming more and more negative over time, indicating that decision-makers should be more concerned on the uncertainty and volatility harms the output growth more than before. For all countries, the effect of output uncertainty on growth is about 2.5 times higher in 2017 than its level in the early 1980s before the start of the Great Moderation, except for the US for which the effect is about 1.7 times higher.

6 Comparison of findings with the previous literature

The findings of the studies investigating the link between the output growth and its volatility for the G7 countries are mixed. The evidence reported in Table 3 of this study shows that output growth series has a positive effect for Canada, Germany, Italy, Japan, the UK, and the US, but the effect is insignificant except for Italy. Thus, our results only weakly support the hypothesis that growth is a positive determinant of output volatility as predicted by Black (1987) and Blackburn (1999). This evidence is parallel to the findings of Fountas et al. (2002) for Japan, Fang et al. (2008) only for Japan out of six (except France) of the G7, Conrad et al. (2010) for the UK. Contrary to the results obtained for Canada, Germany, Italy, Japan, the UK, and the US, the evidence for France indicates that the output growth appears to have a negative effect on output volatility, as predicted by Pindyck (1991) and Blackburn and Pelloni (2005). This finding is not similar to the evidence of Fountas and Karanasos (2007) for four (UK, Germany, France and Italy) of the G7 countries. Overall, the evidence on the reverse causality from growth to output volatility is very weak.

Overall, the evidence from Fig. 2 shows that output growth uncertainty is a negative and significant determinant of output growth as predicted by Pindyck (1991) for the most of the study sample for Canada, France, Germany, and Italy. The effect is negative for the full period considered for the US. However, estimates are, although negative after the early 1970s, are insignificant for the whole period for Japan, partially supporting the independence hypothesis. This evidence is parallel to the findings of Karanasos and Schurer (2005) for Italy and Fang et al. (2008) only for Japan out of six (except France) of the G7 countries. In sum, as the estimates of the \(\alpha_{t}\) measuring the effect of output volatility on output growth turn from positive to negative for France, Japan, and the UK, our results brings evidence in favor of the bipolar view (Grinols and Turnovsky 1998; Turnovsky 2000; Blackburn and Galindev 2003; Blackburn and Pelloni 2004). In terms of the magnitudes of the estimates of \(\alpha_{t}\), the minimum and maximum of the estimates are within the interval [− 1.144, − 2.861] for Canada, [0.110, − 1.939] for France, [− 0.498, − 2.010] for Germany, [− 0.581, − 2.547] for Italy, [0.142, − 0.914] for Japan, [0.470, − 1.865] for the UK, and [− 2.586, − 3.347] for the US. Thus the lowest values are mostly less than − 2.

Fountas and Karanasos (2008) use annual industrial production index data that spans 100 years starting around the mid-1800s and ending in the late 1990s to estimate the effect of output volatility on growth for France, Germany, Italy, Sweden, and the UK. They use a AR-GARCH in the mean specification where volatility is estimation by the GARCH(1,1) model. Their estimates for the effect of volatility on growth are 0.108, 2.351, 2.838, and 7.297, for France, Germany, Italy, and the UK, respectively. Thus, their findings are positive and statistically significant and, thus, squares with the findings of Caporale and McKiernan (1998), which finds support for the Black’s (1987) business cycle hypothesis (a positive effect of output volatility on output growth). Our findings are in sharp contrast to their findings for most of the sample period covered.

We only have positive but insignificant estimates for France and the UK, which only corresponds to the period before 1973. There are three reasons that may explain the difference between our findings and that of Fountas and Karanasos (2008). First, the constant parameter AR-GARCH model specification in Fountas and Karanasos (2008) might be misspecified for a time series data that spans more than 100 years. Over 100 years, the parameters of the model are likely to have breaks due to structural changes in the economy and radical changes in the economic policy environment. Moreover, the GARCH specification does not allow volatility shocks and volatility is deterministically modelled with moment restrictions, which is another specification issue. Second, most of the span of their data does not overlap with the span of our data. The total overlap is about 40 years (from 1960s to 1990s). Third, they use industrial production index to proxy output, which might have different properties.Footnote 10 Overall, our findings encompass the empirical evidence obtained in the previous literature and offer an explanation to conflicting evidence they have obtained: the effect of output volatility on output growth is state dependent up to a sing change and display substantial time variation.

In comparison to earlier literature, another eye-catching stylized feature of the results is the counter-cyclical uncertainty estimates as evidenced by the level of the log stochastic volatility estimates presented in the left panel of Fig. 2. A number of recent studies find significant evidence that both micro and macro uncertainty is counter-cyclical (see, among others: Schwert 1989; Campbell et al. 2001; Storesletten et al. 2004; Meghir and Pistaferri 2004; Bloom et al. 2007, 2018; Alexopoulos and Cohen 2009; Popescu and Rafael Smets 2010; Bachmann and Bayer 2011; Guvenen et al. 2014; Arslan et al. 2015; Jurado et al. 2015; Berger and Vavra 2018).Footnote 11

As a measure of output uncertainty, the log stochastic volatility estimates in Fig. 2 show strong counter-cyclical behaviour for all countries. The log volatility rises with strong peaks in recession periods. We observe peaks in the log volatility estimates in the recessions during the 1973–1974 oil price shock period, during the recession period in 1991–1993 (the First Gulf War), the 1997–1998 recession associated with the Asian crises and more strongly during the Global Recession following the 2007–2008 Subprime Crisis. The log volatility increases reaching peak levels during recessions and then decreases during the recovery periods. This behaviour is maintained with temporary breaks in the overall declining trend in output volatility. The stylized counter-cyclical behaviour of output volatility is quite analogous across all G7 economies.

7 Conclusion

In this article, we re-examine the dynamic link between growth and growth uncertainty relationship in a stochastic volatility in the mean model with time-varying parameters in the G7 countries using the data on quarterly output growth. To do this, the TVP-SV model is used in this study since researchers such as Chan (2017) noted that the volatility appears in both the conditional mean and the conditional variance and its coefficient in the former is time-varying. Parallel to the evidence as elaborated by Chan (2017) in the literature, the first main result from this study shows substantial time-variation in the coefficient associated with the volatility. Also, the evidence from this study indicates that the impact of output uncertainty on growth is substantially time-varying and negative with breaks for the most of the sample in France, Japan, and the UK, while it is negative for the full sample period in Canada, Germany, Italy, and the US. The estimates are statistically significant either after the mid-1970 or the early 1990s, except for the US where estimates are significant for the whole study period. Lastly, the output growth series is not a significant determinant of output volatility for every country, with the exception of Italy and US, where the output growth appears to have a positive and significant effect on output volatility. Our results are complementary to the previous studies but obtain strong support for time-variation in the impact of growth uncertainty on growth.

To sum up, the results suggest that there are strong linkages between output growth and its volatility in the G7 countries, specifically since the mid-1980s–beginning of the Great Moderation. The evidence obtained from the early 1980s indicates that there is no significant evidence on the impact of output growth uncertainty on output growth series in each country of the G7. There has been obviously improved macroeconomic performance in industrialized and developing countries since the 1980s, with the exception of the oil price shocks of the 1970s and the 2007–2008 Global Financial Crisis sub-periods. The improved macroeconomic performance reduces macroeconomic volatility in industrialized and developing countries. Therefore, output growth and its volatility are now much more stable than they were in the 1970s and the environment of greater macroeconomic stability in the past three decades. The results obtained from this study indicate that less uncertainty leads to a higher rate of growth as a result of the Great Moderation for all the G7 countries. In this context, when the results of our study and the results of other studies in the literature are compared, estimates of the dynamic relationships between output growth and its volatility will be sensitive to the frequency of output growth series, the time span and the method employed. Therefore, the results of this study put forward that it is of great importance that further studies considering the structural changes in the series ought to be considered on the dynamic relationships between these series for the G7 countries as well as other developed and developing countries.

Notes

In macroeconomics literature, terms “output fluctuations”, “business cycle”, “output variability”, “output volatility” and “output uncertainty” are used interchangeably. Following the literature, we also use these terms as synonyms.

Keynes (1936) argues that output uncertainty leads to riskier returns on investment and this, in turn, leads to a negative impact on investment and output.

Economists who are more traditional Keynesians, such as Solow (1997), believe that output growth and its volatility (business cycle component) can (and should) be decomposed into two distinct components and each is analyzed separately, implying they are independent.

Explanations for the “bipolar” view are reviewed in Sect. 2.

See Chan (2017, p. 27) for the priors used in the estimation.

Time series plots of growth rates in Fig. 1 indicate that all of the growth series show some trend. We thus take a constant plus a linear trend case as more realistic than only a constant case.

Most economists take the mid-1980s as the start of the Great Moderation period. The Centennial Gateway Project uses a different convention for dating the various episodes of Federal Reserve history and defines the end of the Great Inflation episode as 1982, this marks the beginning of the next episode—the Great Moderation—as the early 1980s. Early 1980s is as the beginning of the Great Moderation is also consistent with our estimates.

A former version of this paper used industrial production index and the same TVP-SV model specification. Indeed, most of the estimates of \(\alpha_{t}\) were positive when industrial production index was used. Upon the request by an anonymous referee, this version of the paper uses quarterly GDP as a measure of output. The TVP-SV estimation results with industrial production index are available from the authors upon request.

Schwert (1989) finds evidence supporting counter-cyclical volatility in macro stock returns and Campbell et al. (2001), Bloom et al. (2007) and Gilchrist et al. (2009) in firm-level (micro) stock returns. Bachmann and Bayer (2011), Kehrig (2011) and Bloom et al. (2018) find counter-cyclical volatility in plant, firm, industry and aggregate output and productivity. Moreover, Berger and Vavra (2018) finds supporting evidence for counter-cyclical volatility in in price changes while Meghir and Pistaferri (2004), Storesletten et al (2004) and Guvenen et al. (2014) find supporting evidence in consumption and income series. Popescu and Rafael Smets (2010), Bachmann et al. (2013) and Arslan et al. (2015) find higher disagreement among forecasters and higher within-forecaster dispersion in forecasts of GDP and prices. Alexopoulos and Cohen (2009) obtains evidence that the word “uncertainty” is more frequently associated with the word “economy” during recessions. Jurado et al. (2015) finds empirical evidence that uncertainty factor indicator is counter-cyclical.

References

Aghion P, Howitt P (1992) A model of growth through creative destruction. Econometrica 60(2):323–351

Aghion P, Saint-Paul G (1998a) Virtues of bad times interaction between productivity growth and economic fluctuations. Macroecon Dyn 2(3):322–344

Aghion P, Saint-Paul G (1998b) Uncovering some causal relationships between productivity growth and the structure of economic fluctuations: a tentative survey. Labour 12:279–303

Alexopoulos M, Cohen J (2009) Nothing to fear but fear itself? Exploring the effect of economic uncertainty. Manuscript, University of Toronto working paper

Andreou E, Pelloni A, Sensier M (2008) Is volatility good for growth? Evidence from the G7. The University of Manchester, Centre for Growth and Business Cycle Research, Discussion Paper 097

Andrews D (1991) Heteroskedasticity and autocorrelation consistent covariant matrix estimation. Econometrica 59(3):817–858

Arslan Y, Atabek A, Hulagu T, Şahinöz S (2015) Expectation errors, uncertainty, and economic activity. Oxf Econ Pap 67(3):634–660

Bachmann R, Bayer C (2011) Uncertainty business cycles-really? NBER Working Paper No. 16862

Bachmann R, Caballero RJ, Engel EM (2013) Aggregate implications of lumpy investment: new evidence and a DSGE model. Am Econ J Macroecon 5(4):29–67

Baker SR, Bloom N (2013) Does uncertainty reduce growth? Using disasters as natural experiments. NBER Working Paper No. 19475

Balcilar M, Ozdemir ZA (2013) Asymmetric and time-varying causality between inflation and inflation uncertainty in G-7 countries. Scott J Polit Econ 60(1):1–42

Barro RJ (1991) Economic growth in a cross section of countries. Q J Econ 106(2):407–443

Barro RJ, Sala-i-Martin X (1992) Convergence. J Polit Econ 100(2):223–251

Bean C (1990) Endogenous growth and the pro-cyclical behaviour of productivity. Eur Econ Rev 34:355–394

Berger D, Vavra J (2018) Dynamics of the US price distribution. Eur Econ Rev 103:60–82

Bernanke BS (1983) Irreversibility, uncertainty, and cyclical investment. Q J Econ 98(1):85–106

Black F (1987) Business cycles and equilibrium. Blackwell, New York

Blackburn K (1999) Can stabilisation policy reduce long-run growth? Econ J 109(452):67–77

Blackburn K, Galindev R (2003) Growth, volatility and learning. Econ Lett 79(3):417–421

Blackburn K, Pelloni A (2004) On the relationship between growth and volatility. Econ Lett 83(1):123–127

Blackburn K, Pelloni A (2005) Growth, cycles and stabilisation policy. Oxf Econ Pap 57(2):262–282

Bloom N, Bond S, Van Reenen J (2007) Uncertainty and investment dynamics. Rev Econ Stud 74(2):391–415

Bloom N, Floetotto M, Jaimovich N, Saporta-Eksten I, Terry SJ (2018) Really uncertain business cycles. Econometrica 86(3):1031–1065

Bollerslev T (1986) Generalized autoregressive conditional heteroskedasticity. J Econom 31(3):307–327

Bredin D, Fountas S (2009) Macroeconomic uncertainty and performance in the European Union. J Int Money Finance 28(6):972–986

Brunner A (1993) Comment on inflation regimes and the sources of inflation uncertainty. J Money Credit Bank 25(3):512–514

Caballero R, Hammour M (1996) On the timing and efficiency of creative destruction. Q J Econ 111(3):805–852

Campbell JY, Lettau M, Malkiel BG, Xu Y (2001) Have individual stocks become more volatile? An empirical exploration of idiosyncratic risk. J Finance 56(1):1–43

Canova F (1993) Modelling and forecasting exchange rates with a Bayesian time-varying coefficient model. J Econ Dyn Control 17(1–2):233–261

Caporale T, McKiernan B (1996) The relationship between output variability and growth: evidence from post war UK data. Scott J Polit Econ 43:229–236

Caporale T, McKiernan B (1998) The Fischer Black hypothesis: some time-series evidence. South Econ J 64(3):765–771

Chan JC (2017) The stochastic volatility in the mean model with time-varying parameters: an application to inflation modeling. J Bus Econ Stat 35(1):17–28

Chapsa X, Katrakilidis C, Tabakis N (2011) Dynamic linkages between output growth and macroeconomic volatility: evidence using Greek data. Int J Econ Res 2(1):152–165

Chesney M, Scott L (1989) Pricing European currency options: a comparison of the modified Black–Scholes model and a random variance model. J Financ Quant Anal 24(3):267–284

Clark PK (1973) A subordinated stochastic process model with finite variance for speculative prices. Econometrica 41(1):135–155

Cogley T, Sargent TJ (2001) Evolving post-world war II US inflation dynamics. NBER Macroecon Annu 16:331–373

Cogley T, Sargent TJ (2005) Drifts and volatilities: monetary policies and outcomes in the post WWII US. Rev Econ Dyn 8(2):262–302

Conrad C, Karanasos M, Zeng N (2010) The link between macroeconomic performance and variability in the UK. Econ Lett 106(3):154–157

D’Agostino A, Gambetti L, Giannone D (2013) Macroeconomic forecasting and structural change. J Appl Econom 28(1):82–101

Danielsson J (1994) Stochastic volatility in asset prices estimation with simulated maximum likelihood. J Econom 64(1–2):375–400

Davidian M, Carroll RJ (1987) Variance function estimation. J Am Stat Assoc 82(400):1079–1091

De Long B (2000) The triumph of monetarism. J Econ Perspect 14:83–94

Dellas H (1991) Stabilization policy and long term growth: are they related?. University of Maryland, Mimeo

Denis S, Kannan P (2013) The impact of uncertainty shocks on the UK Economy. IMF Working Paper No. 13/66

Dickey DA, Fuller WA (1979) Distribution of the estimators for autoregressive time series with a unit root. J Am Stat Assoc 74:427–431

Doepke M (2004) Accounting for fertility decline during the transition to growth. J Econ Growth 9(3):347–383

Elder J (2004) Another perspective on the effects of inflation uncertainty. J Money Credit Bank 36(5):911–928

Elliott G, Rothenberg TJ, Stock JH (1996) Efficient tests for an autoregressive unit root. Econometrica 64(4):813–836

Engle RF (1982) Autoregressive conditional heteroscedasticity with estimates of the variance of United Kingdom inflation. Econometrica 50:987–1007

Engle RF, Lilien DM, Robins RP (1987) Estimating time varying risk premia in the term structure: the Arch-M model. Econometrica 55:391–407

Fang W-S, Miller SM (2008) The great moderation and the relationship between output growth and its volatility. South Econ J 74(3):819–838

Fang W-S, Miller SM (2009) Modeling the volatility of real GDP growth: the case of Japan revisited. Jpn World Econ 21(3):312–324

Fang W-S, Miller SM, Lee CS (2008) Cross-country evidence on output growth volatility: nonstationary variance and GARCH models. Scott J Polit Econ 55(4):509–541

Fountas S, Karanasos M (2006) The relationship between economic growth and real uncertainty in the G3. Econ Model 23(4):638–647

Fountas S, Karanasos M (2008) Are economic growth and the variability of the business cycle related? Evidence from five European Countries. Int Econ J 22(4):445–459

Fountas S, Karanasos M, Kim J (2002) Inflation and output growth uncertainty and their relationship with inflation and output growth. Econ Lett 75(3):293–301

Fountas S, Karanasos M, Mendoza A (2004) Output variability and economic growth: the Japanese case. Bull Econ Res 56(4):353–363

Fountas S, Karanasos M, Kim J (2006) Inflation uncertainty, output growth uncertainty and macroeconomic performance. Oxf Bull Econ Stat 68(3):319–343

Friedman M (1968) The role of monetary policy. Am Econ Rev 58:1–17

Friedman M (1977) Nobel lecture: inflation and unemployment. J Polit Econ 85:451–472

Gilchrist S, Sim J, Zakrajsek E (2009) Uncertainty, credit spreads and aggregate investment. Boston University, Mimeo

Granger CW, Newbold P (1976) Forecasting transformed series. J R Stat Soc Ser B Methodol 38(2):189–203

Grier K, Perry M (2000) The effects of real and nominal uncertainty on inflation and output growth: some GARCH-M evidence. J Appl Econom 15(1):45–58

Grier K, Tullock G (1989) An empirical analysis of cross-national economic growth: 1951–1980. J Monet Econ 24(2):259–276

Grier KB, Henry ÓT, Olekalns N, Shields K (2004) The asymmetric effects of uncertainty on inflation and output growth. J Appl Econom 19(5):551–565

Grinols E, Turnovsky SJ (1998) Risk, optimal government finance, and monetary policies in a growing economy. Economica 65(259):401–427

Guvenen F, Ozkan S, Song J (2014) The nature of countercyclical income risk. J Polit Econ 122(3):621–660

Haddow A, Hare C, Hooley J, Shakir T (2013) Macroeconomic uncertainty: what it is, how can we measure it and why does it matter? Bank Engl Q Bull 53(2):100–109

Henry O, Olekalns N (2002) The effect of recessions on the relationship between output variability and growth. South Econ J 68(1):683–692

Hull J, White A (1987) The pricing of options on assets with stochastic volatilities. J Finance 42(2):281–300

Jurado K, Ludvigson SC, Ng S (2015) Measuring uncertainty. Am Econ Rev 105(3):1177–1216

Karanasos M, Schurer S (2005) Is the reduction in output growth related to the increase in its uncertainty? The case of Italy. WSEAS Trans Bus Econ 3:116–122

Kehrig M (2011) The cyclicality of productivity dispersion. US Census Bureau Center for Economic Studies Paper No. CES-WP-11-15

Keynes JM (1936) The general theory of employment, interest, and money. Macmillan, London

Kim S, Shephard N, Chib S (1998) Stochastic volatility: likelihood inference and comparison with ARCH models. Rev Econ Stud 65(3):361–393

King R, Plosser C, Rebelo S (1988) Production, growth, and business cycles: II. New directions. J Monet Econ 21(2–3):309–341

Kneller R, Young G (2001) Business cycle volatility, uncertainty, and long-run growth. Manch Sch 69(5):534–552

Koop G, Potter SM (2007) Estimation and forecasting in models with multiple breaks. Rev Econ Stud 74(3):763–789

Koopman SJ, Hol Uspensky E (2002) The stochastic volatility in the mean model: empirical evidence from international stock markets. J Appl Econom 17(6):667–689

Kormendi RC, Meguire PG (1985) Macroeconomic determinants of growth: cross-country evidence. J Monet Econ 16(2):141–163

Kwiatkowski D, Phillips PCB, Schmidt P, Shin Y (1992) Testing the null hypothesis of stationarity against the alternative of a unit root: how sure are we that economic series are non-stationary? J Econom 54:159–178

Kydland F, Prescott E (1982) Time to build and aggregate fluctuations. Econometrica 50(6):1345–1370

Lee J (2010) The link between output growth and volatility: evidence from a GARCH model with panel data. Econ Lett 106:143–145

Long J, Plosser C (1983) Real business cycles. J Polit Econ 91(1):39–69

Lucas RE (1972) Expectations and the neutrality of money. J Econ Theory 4:103–124

Mankiw NG, Romer D, Weil DN (1992) A contribution to the empirics of economic growth. Q J Econ 107:408–437

Martin P, Rogers CA (1997) Stabilization policy, learning by doing, and economic growth. Oxf Econ Pap 49:152–166

Martin P, Rogers CA (2000a) Long-term growth and short-term economic instability. Eur Econ Rev 44:359–381

Martin P, Rogers CA (2000b) Optimal stabilization policy in the presence of learning by doing. J Public Econ Theory Assoc Public Econ Theory 2(2):213–241

Meddahi N, Renault E (2004) Temporal aggregation of volatility models. J Econom 119(2):355–379

Meghir C, Pistaferri L (2004) Income variance dynamics and heterogeneity. Econometrica 72(1):1–32

Mirman LJ (1971) Uncertainty and optimal consumption decisions. Econometrica 39:179–185

Ng S, Perron P (2001) Lag length selection and the construction of unit root tests with good size and power. Econometrica 69(6):1519–1554

Ozdemir ZA (2010) Dynamics of inflation, output growth and their uncertainty in the UK: an empirical analysis. Manch Sch 78(6):511–537