Abstract

In this study, we examine the behaviour of unemployment in Nigeria using fractional integration & fractional cointegration techniques. Based on the fractional integration technique, we find that unemployment in Nigeria exhibits mean reverting properties but with a longer time horizon for any shock effect to fizzle out. The fractional cointegration technique reveals that unemployment shares somewhat common long run relationships with macroeconomic variables such as interest rate, inflation and output. Therefore, policy actions by relevant authority targeted at any of these macroeconomic variables may have implications on unemployment in Nigeria and vice versa. However, the results leading to these conclusions are sensitive to sample periods and intervening variables.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

Gauging the extent of persistence in unemployment rates is of vital importance to Nigeria considering its role in African economies. As one of the countries in the world where the level misery is very high (Tule et al 2017a), determining the degree of unemployment rate by policy makers becomes a sine qua non in choosing appropriate response to external shocks. In the conduct of macroeconomic policy, the implications of time series behaviour of the unemployment rate cannot be overemphasized. As posited in the natural rate hypothesis of Friedman (1968) and Phelps (1967), in the long-run, the unemployment rate should converge to a ‘‘natural rate’’, since it follows a mean reverting process and the variations from the natural rate are transitory. However, high and persistent unemployment has cast aspersion on the natural rate hypothesis. Hence, Blanchard and Summers (1987) formulated the hysteresis hypothesis to account for high and persistent unemployment rates witnessed in some European countries. In line with Blanchard and Summers (1987), there is high likelihood of unemployed workers losing valuable job skills over time. Similarly, stagflation and recession are other likely factors that may have everlasting effects on the skills of workers. Hence, any shock to unemployment may have a permanent effect and by implication, likely to exhibit a non-mean reverting process. Hence, from empirical point of view as documented in the extant literature, suffice it to say that evidence in support of the existence of the hysteresis in the unit root process abound, while on the other hand, stationarity would support the natural rate hypothesis in unemployment.

Theoretically, the dynamics of unemployment are basically underpinned by two views: the hysteresis hypothesis and the non-accelerating inflation rate of unemployment (NAIRU) hypothesis (Romer 2011). The NAIRU hypothesis is of the view that oscillations in unemployment are “cyclical deviations” from the “natural-rate”. Friedman (1968) and, Phelps (1968) who are the first proponents of the NAIRU led hypothesis, argue that unemployment should chart a stationary process. Nevertheless, Blanchard and Summers (1987), who first proposed the hysteresis hypothesis opine that shocks on unemployment rate would not have temporary effects and that the “equilibrium rate of unemployment” shifts from one level to another by an exogenous shock.

The literature on unemployment persistence has offered three strands of studies on the basis of the types of unit root tests usually employed. The first strand of studies whose findings generally support the hypothesis of hysteresis in unemployment mainly applies the conventional unit root tests (see for example, Blanchard and Summers 1987; Perron 1989; Brunello 1990; Mitchell 1993; Jaeger and Parkinson 1994; and Roed 1996). Inspired by Perron (1989)’s seminal work (1989) in which it is suggested that normal unit root tests are biased towards non-rejection in the presence of a structural break, the second strand of research focuses on whether incorporating structural breaks in the unit root model is relevant to the hysteresis hypothesis. As a consequence, Zivot and Andrews (1992) and Perron (1997) established models that permit an endogenous break. Lumsdaine and Papell (1997) and Lee and Strazicich (2003a, b) extend the work of Zivot and Andrews (1992) to test for two endogenous breaks. Exploring some of these structural break-based unit root tests, Mitchell (1993), Bianchi and Zoega (1997), Arestis and Mariscal (1999, 2000) and Papell et al. (2000) unanimously show that when structural breaks are taken into account, the hysteresis hypothesis is rejected. The third strand of studies is based on panel unit root tests with and without structural breaks (see Levin et al. 2002 and Im et al. 2003 in the case of the latter, Papell et al 2000, in the case of the former). Thus, both the time series and panel data techniques have been used to evaluate unemployment persistence in the literature.

Consequently, our study will leverage on relevant statistical considerations such as nonlinearities, fractional integration, structural breaks and endogeneity issues to empirically analyze the severity of unemployment in Nigeria. Although Tule et al (2016) and Tule et al (2017a) have done some work on the composite index of leading indicators of unemployment and the dynamic fragmentation of misery index in Nigeria, respectively, however, to the best of our knowledge, studies that have done similar work include Caporale and Gil-Alana (2018) and Tule et al (2017b). Conversely, their methodology relies on fractional integration, which ignores other stochastic features of time series as previously highlighted. Technically, the consideration of these features when they are found to be evident may upturn the findings of Tule et al (2017b) and Caporale and Gil-Alana (2018). Also, in addition to the analysis of unemployment behaviour in Nigeria, a robustness check will also be employed to offer more useful generalizations. From a policy perspective, information about unemployment persistence enables policy makers to evaluate the effectiveness of their policies in influencing the behaviour of unemployment. Thus, the study will not only be rigorous analytically, it will also produce results that can serve as input to future policy formulation and implementation process.

Understanding the persistence of unemployment will give important information on its dynamics, the magnitude of shocks it transmits to the economy, and a country's sensitivity to unemployment risk. These elements are critical for the formulation and implementation of economic policy and accelerating the restoration of employment to a steady path commensurate with a countrie's growth objectives.

Following the introduction, the paper is organized as follows: Section 2 deliberates on the empirical and theoretical findings on unemployment persistence; Section 3 discusses the methodology while Sect. 4 discusses the empirical results. Finally, Sect. 5 concludes the study.

2 Literature Review

2.1 Theoretical underpinnings in unemployment persistence

The theoretical underpinnings for the behaviour of unemployment can be linked to the Non-Accelerating Inflation Rate of Unemployment (NAIRU) hypothesis that states that there exists a unique long run equilibrium for unemployment rates. The implication is that there does not exist a trade-off between inflation and output and the Phillips curve is vertical in the long-run. However, in the short-run, there are transitory deviations from the long run equilibrium making unemployment stationary and mean reverting.

Phelps (1972) in his book on “Inflation Policy and Unemployment Theory” proposes a theoretical model that explains changes in NAIRU due to changes in economic rudiments in the economy, i.e. capital, interest rates and productivity. The models incorporate micro foundations to explain structural changes (Layard et al. 2005). Under the structuralist theory of unemployment, empirical analysis should be done by unit root tests such as Augmented Dickey-Fuller (ADF) Test, Kwiatkowski–Phillips–Schmidt–Shin (KPSS) and Phillips-Perron (PP)-test that account for structural changes in unemployment. If not, unit root test carried out may be biased with type 2 error in the presence of structural breaks in the deterministic components of unemployment. (See, among others, Blanchard et al. 1992; Decressin and Fatas 1995).

The second theory links the attitude and behaviour of those in employment to contributing to unemployment persistence and this has been extensively researched by Blanchard and Summers (1986, 1987) and Barro (1995). According to this phenomenon, shocks to unemployment do not die out and the variable never returns to its equilibrium rate, exhibiting an explosive process. The explanations for this process include high real wages, unemployment protection schemes, powerful workers unions and stigma associated with being out of work for a long time. This has been extensively examined by Phelps (1972); Blanchard and Summers (1986, 1987); Barro (1995); and Layard (2005), amongst others. The effect of lagged unemployment on hysteresis, can be explained in terms of insider–outsider effect as Blanchard and Summers (1986, 1987) point out or by the effect of unemployment on the human capital and search intensity of the unemployed by Okun (1973). Finally, in contrast to the NAIRU hypothesis, the hysteresis hypothesis argues that, as aggregate demand can influence the path of actual unemployment, aggregate demand policies can influence the natural rate of unemployment.

3 Empirical review of the literature on unemployment persistence

In the literature, there appears to be different causes of unemployment persistence. Neisson and Plosser (1982), Blanchard and Summers (1986, 1987), Brunello (1990), and Mitchell (1993) are of the view that EU countries’ unemployment series contains a unit root. Nonetheless, the presence of structural breaks may render the results of unit root test invalid such that the unemployment data can be assumed to be integrated of order 1 (I(1)) when in fact it is stationary around a drift after accounting for structural breaks. This latter argument is upheld by Mithcell (1993), Bianchi and Zoega (1998) Ariesis and Mariscal (1999) and Pappelle et al. (2000) who apply unit root test with structural break and find evidence supporting the structuralists’ viewFootnote 1 of unemployment.

A comparative study by Song and Wu (1997, 1998) finds evidence in support of hysteresis hypothesis in EU countries’ unemployment series, while the U.S. unemployment data are characterized by the NAIRU hypothesis (see also, Gil-Alana 2001a, b, 2002; Caporale & Gil-Alana 2007, 2008)). Gil-Alana (2001a, b), Gil-Alana (2002) and Caporale and Gil-Alana (2007, 2008) favour the structuralists’ view for EU unemployment based on the AFRIMA (Autoregressive Fractionally Integrated Moving Average) model while the NAIRU hypothesis is supported for the U.S. unemployment as reported in Song and Yangru (1997, 1998). However, unemployment in the European Community (EC) is found to be highly persistent, relative to the Nordic countries and U.S. (see Alogoskoufis & Manning 1988). For other climes like the Latin American countries, there is evidence of mean reversion in unemployment (see Ayala et al 2012).

In relation to the country of focus (i.e. Nigeria), the degree of unemployment persistence is observed within the range of {0 < d < 1}, (see Tule et al. 2017a), and is more likely to be characterized by the NAIRU hypothesis. By way of extension of the existing literature on unemployment persistence, we build on related studies by Caporale and Gil-Alana (2007, 2008, 2018) which allow for breaks in a fractional integration framework and take consideration of the possible autocorrelation in the unemployment series. The fractional integration framework has the advantage that the fractional parameter can take any real value compared to the classical I(0)/I(1) integration dichotomy. In order to obtain information on the relevance of alternative unemployment theories, it is crucial to estimate the differential parameter ‘d’ in the fractional integration framework. Specifically, an order of integration equal to 0 supports the NAIRU hypothesis, while a positive value of ‘d’ represents evidence in support of hysteresis hypothesis.

4 Methodology

4.1 The fractionally integrated univariate model for persistence

One of the attractions to the fractional integration approach lies in its ability to exploit the stochastic behaviour of economic series in a fractional form unlike the traditional approaches which assume integer values in the determination of stationarity. The fractional integration approach contends that such series may be fractionally integrated such that the impact of shocks only vanishes at very long horizons, rather than assume that economic series are I(1). This methodology has also been used to examine unemployment persistence for different countries (Caporale and Gil-Alana 2007, 2008; 2018). Therefore, we test for unemployment persistence for Nigeria using the fractional integration as specified below:

where L is the lag operator \(\left( {LZ_{t} = Z_{t - 1} } \right)\)\(d\) can be any real value from (0 to 1), \(Z_{t}\) is integrated of order d and symbolized by \(Z_{t} \approx I(d)\). \(\varepsilon_{t}\) is a covariance stationary process with a spectral density function that is positive and is an integrated order \(0\left( {I\left( 0 \right)} \right)\) process and finite at zero frequency. The polynomial \(\left( {1 - L} \right)^{d}\) in Eq. (1) can be formulated on the basis of its binomial expansion such that for all real \(d\),

and therefore

Consequently, Eq. (3) can be expressed as:

Equation (4) is derived to show that \(d\) also plays a critical role in appraising the level of persistence as it defines the degree of dependence of the unemployment series (Caporale and Gil-Alana 2007, 2008; 2018; Gil-Alana & Carcel 2018; Usman & Nduka 2022). Hence, given a higher value of \(d\), would imply a higher level of memory amongst the series and by inference a higher level of persistence (Ebuh et al. 2021). In order to analyze fractional integration, we use the parametric technique, which includes the maximum likelihood estimator of Sowell (1992). This approach has the benefit of obtaining precision by employing data through parameter estimates. However, one shortcoming of this approach is that parameter estimates may be unreliable owing to misspecification. We assume that the errors are uncorrelated (white noise), and we investigate under two different model specifications: (i) with an intercept and (ii) with a linear time trend.

4.2 Fractionally cointegrated VAR (FCVAR) for Unemployment rates

This study examines the long run association between unemployment and other macroeconomic fundamentals using the FCVAR approach proposed by Johansen and Nielsen (2012). Since the traditional CVAR model is the baseline model for the FCVAR model, we begin our specification of the latter based on the former.Footnote 2 Assuming \(Z_{t}\) is a vector of I(1) time series of dimension \(p\), the CVAR model can be expressed in the error correction form as:

The FCVAR model is derived from Eq. (5) above by replacing the \(\Delta\) and \(L\) in the equation with \(\Delta^{d}\) and \(L_{b}\), respectively. This gives:

where \(\Delta^{d}\) represents the fractional difference operator, and \(L_{b} = 1 - \Delta^{b}\) is the fractional lag operator. Within the context of this study, the most relevant parameters are the long run parameters \(\alpha\) and \(\beta\) which are \(p \times r\) matrices with \(0 \le r \le p\). The rank \(r\) is the cointegration, or cofractional, rank. The columns of \(\beta\) constitute the r cointegration (cofractional) vectors such that \(\beta^{\prime}Z_{t}\) are the cointegrating combinations of the variables in the system, i.e. the long-run equilibrium relations. The parameters in \(\alpha\) are the adjustment coefficients which represent the speed of adjustment towards equilibrium for each of the variables. The short-run dynamics of the variables are captured by the parameters \(\Gamma = \left( {\Gamma_{1} , \ldots ,\Gamma_{k} } \right)\) in the autoregressive augmentation (Nielsen & Popiel 2018).Footnote 3 Note that if \(d = b = 1\), the FCVAR model reduces to the CVAR variant. Confirming that the CVAR is a special case of the FCVAR.

The procedure for estimation of the FCVAR is presented in the following steps: (i) the optimal lag length model is determined; (ii) the cointegration rank is determined; (iii) information from (i) and (ii) is used to test for fractional cointegration; and finally, (iv) the FCVAR model is compared with the CVAR model using the LR test which restricts \(d = b = 1\) under the null hypothesis. A rejection of the null hypothesis supports the FCVAR approach, if not, the CVAR approach is preferred.

5 Discussion of results

5.1 Preliminary analyses

Quarterly data over the period of 1990 to 2018 are used for the analyses. The data were obtained from Statistical Bulletin of the Central Bank of Nigeria (2019) and the Database of National Bureau of Statistics (2019). Some descriptive statistics are rendered in Table 1.The full sample is segregated into two sub-samples consisting of before and after the global financial crisis, which is denoted as Pre-GFC and Post-GFC, respectively. The Pre-GFC sample is defined as the period before the first quarter of 2008, while the Post-GFC includes the Crisis period and the period after it. From Table 1, it can be inferred that unemployment rates were higher and more volatile during the post-GFC period than the pre-GFC period as the unemployment rate recorded higher mean and standard deviation values during the former than the latter. Also, the unemployment series seem to exhibit more asymmetry during the period of post-GFC than the pre-GFC, while the sub-samples are negatively skewed with longer left tail. Similarly, following Westfall (2014), the sub-samples as shown in Table 1 are platykurtic (shorter and thinner tails).

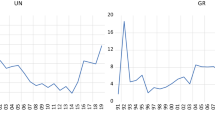

The descriptive analysis is accompanied by the plot of the unemployment rate which is shown in Fig. 1, which patently displays a mild undulating trend in unemployment rate during the period before the GFC, particularly between 1990 and 2000, which could be attributed to the aftermath of oil windfall slightly followed by the Structural Adjustment Programme pursued by the Nigerian government. The post-GFC is characterized by a steady rise in unemployment rate, which reached its zenith at 43.3 per cent in 2018Q3. Although this period ironically coincides with the return of Nigeria to democratic rule, however, long decay of infrastructure associated with military intrusion in our democratic space characterized by poor macroeconomic management and political interference in the operation of monetary policy left much to be desired. Also, between 2016 and 2017, the economy witnessed stagflation and recession. The discrepancies in the trend of unemployment rate in Nigeria, over the two sub-samples, constitute the motivation for the empirical analysis.

Trends in Unemployment Rate in Nigeria

Table 1 presents the descriptive statistics of the data used in this study, which include unemployment rate, inflation rate, interest rate, output, West Texas Intermediate (WTI) and Brent. All the series except output, which commenced from 2010Q1, have the same start dates, commencing from 1991Q1. Consequently, there are about 112 data points for the other series except output data, which has only 36 data points. With the exception of inflation and interest rates that are leptokurtic, all the other series are found to be platykurtic, and have skewness values different from that of the normal distribution. Consequently, we find statistically significant Jarque Bera test statistic for all the series except output.

By way of further examining the series for inherent statistical properties and providing some preliminary results, the ADF unit root test is conducted for all the series. We find all the series to have unit roots, and consequently, are non-stationary. While all the series except output are integrated of order one, output is integrated of order two, given that it requires differencing twice. The ADF model with constant and trend is however favoured by unemployment rate and inflation rate, while the ADF model with constant only favours the interest rate, output, WTI and Brent. Consequent upon the foregoing, we estimate an AR(1) model for each of the series, adapting the model framework as depicted by the ADF test. The results reveal some high levels of persistence as the coefficient of the first order autoregressive term is found to range between 0.681 and 0.968. Furthermore, for the purpose of robustness and ascertaining the stationarity of the series, the Narayan et al. (2016) GARCH-based unit root testing framework is also employed. The observed high persistence is not statistically significant, except in the case of the unemployment series. This observed conflicting stance is further subjected to the fractional integration, in order to provide some additional information on the shortness, or otherwise, of the memory; with short memory confirming stationarity, while long memory stance would either be stationary of non-stationary, depending on the observed persistence level.

5.2 Fractional Integration Analyses

Following from the preliminary results in the previous section, we employ the fractional integration technique to ascertain the stance of stationarity. The fractional integration provides information on the memory length of each of the series, in which case, there are three possible outcomes. The first is when the estimated fractional integration parameter is any value between zero and half (i.e. \(0 < d \le 0.5\)), which indicates that the series is stationary (and as expected have mean reverting properties), though exhibiting long memory feats. In the second case, the fractional integration parameter lies within half and unity (i.e. \(0.5 < d < 1\)), which indicates that the series not only exhibits long memory, it is non-stationary but mean reverting. The feat indicates that the impact of shock to the series may take a longer time period to decay/fizzle out. Finally, the case where \(d > 1\), indicates that persistence may be permanent. The testing framework is therefore examined with and without deterministic trend, while adopting the Wald test to ascertain whether the fractional parameter differs significantly from half and unity, separately. The results are presented in Table 2, for the full sample, pre-GFC and post-GFC, respectively.

We find five series (Brent, inflation, interest rate, unemployment and WTI) in Table 2 to exhibit long memory consistently across sample periods, regardless of whether the model with constant only or the model with constant and trend is adopted. Each of the statistically significant fractional integration parameter is further subjected to the Wald test statistic, to ascertain the extent of long memory inherent in the corresponding series. There are consistent non-rejections of the Wald test with the null hypothesis that the fractional integration parameter is not statistically different from half (i.e. \(d = 0.5\)). However, we find consistent rejections of the Wald test with the null hypothesis that the fractional integration parameter is not statistically different from unity. Imperatively, all the series are found to exhibit long memory and are stationary, regardless of the sample period or the model structure adopted. Specifically, Nigeria unemployment rate appears to be stationary, thus confirming absence of unemployment hysteresis in Nigeria as reported by Yaya et al. (2019). We however find the output series differs a little from the other series as the former tends to exhibit short memory (i.e. \(d = 0\)), when the model with constant and trend is adopted. Conclusively, unemployment rate, as well as the other macroeconomic variables investigated, except output, exhibit long memory and are stationary with a fractional order. Therefore, the shock to these variables is not likely to a lasting effect.

5.3 Fractional Cointegration VAR (FCVAR) analyses

Having established that the integration of the unemployment rate as well as inflation rate, interest rate, WTI, Brent and output, is of a fractional order rather than integer numbers, we proceed to examine whether these series are fractionally cointegrated, by estimating both CVAR and FCVAR models of Johansen (1995) and Johansen and Nielsen, (2012), respectively. We examine the integrated parameter estimate for its closeness to unity, while adopting the LR statistics to draw the conclusion of the more preferred model. Significant LR statistics therefore indicate preference in favour of the FCVAR model over the CVAR model. Also, in cognizance of the procedure for estimating the integrated parameter in the FCVAR model framework, we follow the three steps accordingly. First, we determine the optimal lag length, from the set maximum lag of 5, using AIC. Subsequently, the cointegrating rank is also determined using the LR statistic and finally, using the optimal lag and cointegrating rank, the integrated parameters are estimated. We therefore render these analyses for models with and without deterministic trend, first for the full sample and then, as a check for robustness, the pre-GFC and post-GFC sample periods. We also consider in addition to the bivariate cointegration between unemployment and each of the stated macroeconomic variables, a trivariate case that combines unemployment rate, inflation rate and output.

For the bivariate case of unemployment and inflation under the model without deterministic trend, the optimal lag is 1 for full sample, while for the bivariate case of unemployment and interest rate under the model without deterministic trend, the optimal lag is 2 for the full sample. The optimal lag for the bivariate cases under the model with deterministic trend differ depending on the sample period considered. However, in all the cases, the optimal lag length is at least 1 (see results in Table 3). In the trivariate construct, the optimal lag is found to be 3 (Table 4). On the cointegration results (see Tables 5 and 6), we find the cointegration rank to be mostly 1. We however do not find any case of no cointegration in the stated bivariate cases, given that the non-rejection of the null hypotheses of no cointegration is observed for at least 1 cointegrating vector, and this cuts across both model constructs. Imperatively, there exists evidence of cointegration between unemployment and each of the examined macroeconomic variables. This therefore informs the further examination of the fractional integrated parameter, for the nature of the cointegrating relationship between unemployment and the other macroeconomic variables.

On the comparison between FCVAR and CVAR (see Tables 7 and 8), we find the integrated parameter to be greater than 1, in all the bivariate cases using the full sample periods and adapting models with and without deterministic trend, except in the case where unemployment is paired with inflation rate and adapting model with deterministic trend. In the trivariate case, which combines unemployment, inflation and output, the integrated parameter is found to be far less than 0.5 when model with deterministic trend was adopted, and greater than 1 for the model without deterministic trend. Consequently, the FCVAR model is preferred over the CVAR model in all the bivariate cases, except the bivariate construct that paired unemployment with inflation in model without deterministic trend. Under a different model structure, when deterministic trends are incorporated, the FCVAR model is consistently preferred over the CVAR model. The bivariate case, pairing unemployment and output, unarguably favours FCVAR over CVAR, regardless of the model structure. This feat of FCVAR preference is also observed in the trivariate case. Imperatively, while FCVAR model is more likely to be preferred over the CVAR when a model without deterministic trend is employed, the incorporation of a deterministic trend could further improve the preference of FCVAR over the CVAR model. While unemployment appears to share common long run relationships individually with inflation, interest rate and output, the observed long run relationships are better formed with FCVAR, rather than CVAR. Also, Nigeria unemployment rate therefore exhibits long memory but is non-stationary, thus shock to rate of unemployment may be permanent.

6 Robustness Check

Following from the foregoing, having established the consistency in the preference in favour of the FCVAR over the CVAR, we proceed to examine the sensitivity of the result to different choices, with respect to the sample periods (Pre-GFC and Post-GFC) and incorporation of a global factor as an exogenous variable. The sensitivity of our results to these factors are discussed subsequent sections.

6.1 Are results sensitive to the sample periods?

Following the consistent preference of the FCVAR over the CVAR model, when the full sample data is examined under the models with and without a deterministic trend, we further ascertain if the results would be sensitive to the sample period considered. Consequently, the same analyses, as with the full sample data, are conducted using the pre-GFC and post-GFC samples. On the optimal lag, for the bivariate case of unemployment and inflation, under the models with and without deterministic trend, optimal lags of 1 and 3 are observed for the pre-GFC and post-GFC sample periods, respectively. In the case of unemployment and interest rate, under the model without deterministic trend, the optimal lag is 3 for both pre-GFC and post-GFC, and lags 2 and 3 for pre-GFC and post-GFC, respectively, when the model with a deterministic trend is estimated (see results in Table 3). Across pre-GFC and post-GFC periods, cointegration rank is observed to be mostly 1. However, with reference to the pre-GFC period, we only reject the null of no cointegration at rank 1, only when the model with deterministic trend is adapted, but not so with the model without deterministic trend. This is indicative of presence (absence) of a long run relationship between unemployment and any of the macroeconomic variables – inflation and interest rate, when model with (without) deterministic trend is used. Interestingly, the stance of long run relationship between unemployment and the macroeconomic variables is established for the post-GFC period, as with the full sample period, earlier discussed. Consequently, the rejection of the null hypotheses of no cointegration of at least 1 cointegrating vector is observed in all the sub-categorizations except the bivariate models pairing separately unemployment with inflation and interest rate under the model without deterministic trend (see results in Tables 5 and 6).

The contest for preference between CVAR and FCVAR as presented in Tables 7 and 8 reveals a higher preference in favour of CVAR over the FCVAR in the pre-GFC period and a higher preference in favour of the later over the former in the post-GFC period. The integrated parameter is observed to be slightly greater or less 1 (ranging between 0.939 and 1.285), in the pre-GFC period, while it is within the domain of 0.010 and 0.011, which is far less than 0.5, in the post-GFC period. While the pre-GFC period is characterized by integrated parameters that are closer to unity and long run relationships that are better formed by CVAR, the post-GFC period integrated parameters are closer to zero and the long run relationship between unemployment and the macroeconomic variables are better formed by FCVAR. Imperatively, the sample periods have differing stances in terms of the preferred model and the integrated parameter estimates, which is indicative of the sensitivity of estimated results to the sample period.

6.2 Are FCVAR results sensitive to incorporated intervening variables?

Here, we consider two global crude oil prices separately as intervening variables and introduce same in the subsequent analyses of fractional cointegration between unemployment and selected macroeconomic variables. The global oil prices are WTI and Brent and are incorporated as exogenous variables. While attempting to examine the impact of incorporating an intervening variable, we simultaneously check for the sensitivity of the results to the choice of global oil price used. We therefore compare the extended fractional cointegration model, which incorporates the global oil price as an intervening variable, with the version without any intervening variables (baseline). The comparison is done using the log-likelihood and the LR test statistic. While the former is used to compare the extended version with the baseline, the latter is employed to determine how best to treat the intervening variable; whether as endogenous or exogenous. Rejection of the null hypothesis of the LR test implies that the intervening variable should be treated endogenously, and exogenously, if otherwise. The results for the bivariate and trivariate model constructs, with and without deterministic trend, are presented in Tables 9 and 10.

A careful look through all the sub-categorizations shows that regardless of the global oil price proxy used as the intervening variable and also, regardless of how the intervening variable is treated, the extended fractional cointegration model does not perform better than the baseline fractional cointegration model. The feat is also replicated across the different sample periods, for all the bivariate and trivariate cases for models with and without deterministic trend. The extended FCVAR models are consistently observed to have smaller log-likelihood than the baseline FCVAR models, indicating that the inclusion of oil price in the FCVAR analyses of Nigeria’s unemployment rate may have little or no impact. However, on the treatment of the intervening variable in the extended FCVAR model, we adjudge the intervening variable to be treated as endogenous (exogenous) if we reject (do not reject) the null hypothesis. Consequently, we find the exogenously incorporated oil price to have smaller log-likelihood in most cases than the endogenized oil price, across all the sub-categorizations, when WTI is used, and something somewhat similar when Brent is used. Although oil price does not seem to significantly improve the fit of the FCVAR model, it must be endogenized if at all it has to be incorporated in the FCVAR analyses.

Furthermore, on the fractional parameter estimates that are obtained from the extended and baseline FCVAR models (see results in Tables 11 and 12), it is shown that baseline model seems to have greater fractional parameter estimates than the extended version with unemployment and inflation, while for the case of unemployment and interest rate, the baseline is less than the two extended versions.

7 Conclusion

Information about unemployment persistence facilitates adequate evaluation of the effectiveness of enacted policies. Rigorous analytic research efforts are thus required to provide the necessary information that would serve as input for subsequent policy formation and implementation. This study therefore sets out to test for unemployment persistence in Nigeria, using fractional integration and fractional cointegration techniques. We complement the research works in this area (see Tule et al. 2016; Tule et al. 2017a, b; and Caporale and Gil-Alana 2018), given that they also adopt that the fractional integration technique and, we in addition provide robustness checks for possible generalization of results.

We utilize quarterly data spanning a period of 1990 to 2018 and obtained from Statistical Bulletin of the Central Bank of Nigeria (2019) and the database of National Bureau of Statistics (2019). Our variables include unemployment rate, inflation rate, interest rate, output, and West Texas Intermediate and Brent crude oil prices. We offer some preliminary data analyses to establish the presence, or absence, of some salient statistical features. From the ADF test and the estimated coefficient of the AR(1) model, the series are found to have unit roots and exhibit some differing levels of persistence. For the purpose of robustness in the unit root test framework, the Narayan et al. (2016) GARCH-based unit root test is also conducted.

Furthermore, the individual series are examined using the conventional fractional integration technique, under different model specifications – model with constant only and model with constant and trend; and different sample periods – full sample, pre-GFC and post-GFC. We find that all the series are fractionally integrated with values in the neighbourhood of 0.5. The Wald test is thereafter employed to ascertain whether the estimated integrated parameter values differ statistically, first from a hypothetical value 0.5 and then, 1.0. We find that the estimated integrated parameter estimates are not significantly different from 0.5, but are significantly different from unity. Imperatively, all the series exhibit long memory but are stationary and consequently have mean reverting properties. Nigeria unemployment rate is here shown to be stationary in support of Yaya et al.’s (2019) stance of absence hysteresis of unemployment in Nigeria. This translates to quick fizzling out of the impacts of shocks to these variables, especially unemployment.

Following a three step procedure for the estimation of the FCVAR model, we ascertain the optimal lag, the cointegration rank and finally, the integrated parameter estimates, along with the log-likelihood and likelihood ratio test statistics. The integrated parameter is thus estimated for models with and without deterministic trend, using all the three sample periods earlier stated. We pair unemployment with each of the other macroeconomic variables, resulting in different bivariate relationships and thereafter, combine unemployment with inflation and output, in a trivariate relationship structure. While we find differing optimal lags and cointegration rank to be mostly 1, we estimate the FCVAR model, and by default, the CVAR model, with which we compare the fit of our model. Generally, the FCVAR model is preferred to the CVAR model, across the sub-categorizations particularly with the incorporation of a deterministic trend. Convincingly, we state here that unemployment shares common long run relationships with inflation, interest rate and output, which is better formed with the FCVAR model. Also, Nigeria unemployment rate exhibits long memory but is non-stationary, thus shocks to rate of unemployment may be permanent. This implies that the hysteresis of unemployment does hold in the Nigerian context, going by the result of the FCVAR estimated integrated parameter, and opposes the stance of Yaya et al. (2019). The presence of cointegration modifies the findings, which might explain why the fractional integration estimation and fractional cointegration estimation yielded different results.

As a good practice, we further subject our results to robustness checks, in a bid to answer two pertinent questions. The first hinging on the sensitivity of our results to sample period, while the second ascertains the sensitivity of our results to the incorporation of an intervening variable, say global oil price. On the sensitivity to sample period, we find the integrated parameters in pre-GFC period to be closer to unity with long run relationships that are better formed by the CVAR model, while the integrated parameters in the post-GFC period are closer to zero, with the established long run relationships between unemployment and the macroeconomic variables being better formed by the FCVAR model. The pre-GFC stance differs markedly from the full sample and the post-GFC periods. Thus, our results appear sensitive to the sample periods. On the sensitivity to intervening variables, we find that the choice of oil price does matter. Also, the model incorporating oil price appears to underperform the one without it, and exogenously incorporated oil price tends to have smaller log-likelihood compared to when oil price is treated endogenously. However, there seems to be no empirical validation for including oil price as an intervening variable in the estimation of integrated parameters using the FCVAR model, and if at all it has to be included, it must be treated endogenously.

Notes

Changes in the underlying equilibrium unemployment rate due to the interplay of changes in real macroeconomic variables and institutions. The structuralist school assumes that unemployment is mean-reverting towards an occasionally changing natural rate.

Excluding theoretical papers, the application of the FCVAR approach is limited, to the best of our knowledge, as few papers have been published in this regard. The most prominent involves commodity returns (see Dolatabadi, Nielsen, & Xu 2016; Dolatabadi et al. 2018) exchange rates (see Gil-Alana & Carcel 2018), Inflation persistence (Tule et al. 2020), Islamic stocks (Salisu et al. 2020), political support & economic voting (see Nielsen & Shibaev 2018; Jones, et al. 2014) and interlinkages between precious metals and Oil (Usman & Akadari, 2021).

We use the Nielsen and Popiel (2018) Matlab program to estimate both the CVAR and the FCVAR models.

References

Alogoskoufis GS, Manning A (1988) On the persistence of unemployment. Economic Policy 3(7):427–469

Arestis P, Mariscal IBF (1999) Unit roots and structural breaks in OECD unemployment. Econ Lett 65:149–156

Arestis P, Mariscal IBF (2000) OECD Unemployment: structural breaks and stationarity. Appl Econ 32:399–403

Ayala A, Cuñado J, Gil-Alana LA (2012) Unemployment hysteresis: empirical evidence for Latin America. J Appl Econ 15(2):213–233

Barro RJ (1995) Inflation and economic growth. No 5326, NBER Working Papers, National Bureau of Economic Research, Inc

Bianchi M, Zoega G (1997) Challenges facing natural rate theory. Eur Econ Rev 41:535–547

Bianchi M, Zoega G (1998) Unemployment Persistence: Does the size of the shock matter? J Appl Economet 13(3):283–304

Blanchard OJ, Summers LH (1986) Hysteresis and the European unemployment problem. NBER Macroecon Annu 1:15–78

Blanchard OJ, Summers LH (1987) Hysteresis in unemployment. Eur Econ Rev 31:288–295

Blanchard OJ, Katz LF, Hall RE, Eichengreen B (1992) Regional evolutions. In: Brookings papers on economic activity. vol 1992(1), pp 1–75

Brunello G (1990) Hysteresis and the Japanese unemployment problem: a preliminary investigation. Oxf Econ Pap 42(3):483–500

Caporale GM, Gil-Alana LA (2007) Nonlinearities and fractional integration in the US unemployment rate. Oxford Bull Econ Stat 69(4):521–544

Caporale GM, Gil-Alana LA (2008) Modelling the US, UK and Japanese unemployment rates: fractional integration and structural breaks. Comput Stat Data Anal 52(11):4998–5013

Caporale GM, Gil-Alana LA (2018) Unemployment in Africa: a fractional integration approach. S Afr J Econ 86(1):76–81

Central Bank of Nigeria (2019)Statistical database for macroeconomic variables. http://statistics.cbn.gov.ng. Accessed 15 Jan 2019

Decressin J, Fatas A (1995) Regional labor market dynamics in Europe. Eur Econ Rev 39(9):1627–1655

Dolatabadi S, Narayan PK, Nielsen MA, Xu K (2018) Economic significance of commodity return forecasts from the fractionally cointegrated VAR model. J Futur Mark 38(2):219–242

Dolatabadi S, Nielsen M, Xu K (2016) A fractionally cointegrated VAR model with deterministic trends and application to commodity futures markets. J Empir Financ 38B:623–639

Ebuh GU, Salisu A, Oboh V, Usman N (2021) A test for the contributions of urban and rural inflation to inflation persistence in Nigeria. Macroecon Finance Emerg Market Econ. https://doi.org/10.1080/17520843.2021.1974507

Friedman M (1968) The role of monetary policy. Am Econ Rev 58:1–17

Gil-Alana LA (2001a) A fractionally integrated exponential model for UK unemployment. J Forecast 20(5):329–340

Gil-Alana LA (2001b) The persistence of unemployment in the USA and Europe in terms of fractionally ARIMA models. Appl Econ 33(10):1263–1269

Gil-Alana LA (2002) Structural breaks and fractional integration in the US output and unemployment rate. Econ Lett 77(1):79–84

Gil-Alana LA, Carcel H (2018) A fractional cointegration var analysis of exchange rate dynamics. North Am J Econ Finance. https://doi.org/10.1016/j.najef.2018.09.006

Im KS, Pesaran MH, Shin Y (2003) Testing for Unit Roots in Heterogeneous Panels. Journal of Econometrics 115(1):53–74

Jaeger A, Parkinson M (1994) Some evidence on hysteresis in unemployment rates. Eur Econ Rev 38(2):329–342

Johansen S (1995) Likelihood-based inference in cointegrated vector autoregressive models. Oxford University Press on Demand, Oxford

Johansen S, Nielsen M (2012) Likelihood inference for a fractionally cointegrated vector autoregressive model. Econometrica 80:2667–2732

Jones M, Nielsen M, Popiel MK (2014) A fractionally cointegrated VAR analysis of economic voting and political support. Can J Econ 47:1078–1130

Layard R, Layard PRG, Nickell SJ, Jackman R (2005) Unemployment: macroeconomic performance and the labour market. Oxford University Press on Demand, Oxford

Lee J, Strazicich MC (2003) Minimum Lagrange multiplier unit root test with two structural breaks. Rev Econ Statist 85(4):1082–1089

Lee J, Strazicich MC (2003b) Minimum Lagrange multiplier unit root test with two structural breaks. Rev Econ Stat 85(4):1082–1089

Levin A, Lin CF, Chu C (2002) Unit root tests in panel data: asymptotic and finite-sample properties. J Econ 108(1):1–24

Lumsdaine RL, Papell DH (1997) Multiple trend Breaks and the unit-root hypothesis. Rev Econ Statist 79(2):212–218

Mitchell WF (1993) Testing for unit roots and persistence in OECD unemployment rates. Appl Econ 25(12):1489–1501

Narayan PK, Liu R, Westerlund J (2016) A GARCH model for testing market efficiency. J Int Finan Markets Inst Money 41:121–138

National Bureau of Statistics (2019) Statistical database for urban and rural inflation rates. http://www.nigerianstat.gov.ng/elibrary. Accessed 15 Jan 2019

Nelson CR, Plosser CR (1982) Trends and random walks in macroeconmic time series: some evidence and implications. J Monet Econ 10(2):139–162

Nielsen MA, Shibaev SS (2018) Forecasting daily political opinion polls using the fractionally cointegrated vector autoregressive model. J R Stat Soc Ser A 181(1):3–33

Nielsen MA, Popiel MK (2018) A Matlab program and user’s guide for the fractionally cointegrated VAR model. Queen’s Economics Department Working Paper No. 1330.

Okun AM, Fellner W, Greenspan A (1973) Upward mobility in a high-pressure economy. Brook Pap Econ Act 1973(1):207–261

Papell DH, Murray CJ, Ghiblawi H (2000) The structure of unemployment. Rev Econ Stat 82(2):309–315

Perron P (1989) The great crash, the oil price shock, and the unit root hypothesis. Econ J Econ Soc 57:1361–1401

Perron P (1997) Further evidence on breaking trend functions in macroeconomic variables. J Econ 80(2):355–385

Phelps E (1968) Money-wage dynamics and labor-market equilibrium. J Polit Econ 76(4):678–711

Phelps ES (1972) Inflation policy and unemployment theory

Phelps ES (1967) Phillips curves, expectations of inflation and optimal unemployment over time. Economica 34:254–281

Roed K (1996) Unemployment hysteresis-macro evidence from 16 OECD countries. Empiric Econ 21(4):589–600

Romer C (2011) The continuing unemployment crisis: causes, cures, and questions for further study. In: Speech presented at livable lives initiative symposium. Washington University, Vol 12

Salisu AA, Ndako UB, Adediran IA, Swaray R (2020) A fractional cointegration VAR analysis of Islamic stocks: a global perspective. North Am J Econ Finance 51:101056

Song FM, Yangru WU (1997) Hysteresis in unemployment evidence from 48 US states. Econ Inq 35(2):235–243

Song FM, Wu Y (1998) Hysteresis in unemployment: evidence from OECD countries. Q Rev Econ Finance 38(2):181–192

Song FM, Yangru W (1997) Hysteresis in unemployment evidence from 48 US states. Econ Inquiry 35(2):235–243

Sowell F (1992) Modeling long-run behavior with the fractional ARIMA model. J Monet Econ 29(2):277–302

Tule MK, Ajilore TO, Ebuh GU (2016) A composite index of leading indicators of unemployment in Nigeria. J Afr Bus 17(1):87–105. https://doi.org/10.1080/15228916.2016.1113909

Tule MK, Chiemeke CC, Oduh MO, Ndukwe CO (2017a) Assessing the severity of unemployment in Nigeria. J Afr Bus 19(4):1–23. https://doi.org/10.1080/15228916.2017.1343031

Tule MK, Egbuna EN, Dada E, Ebuh GU (2017b) A dynamic fragmentation of misery index in Nigeria. J Cogent Econ Finan 5(1):336295

Tule MK, Salisu AA, Ebuh GU (2020) A test for inflation persistence in Nigeria using fractional integration & fractional cointegration techniques. Econ Model 87:225–237

Usman N, Akadiri SS (2021) The persistence of precious metals and oil during the COVID-19 pandemic: evidence from a fractional integration and cointegration approach. Environ Sci Pollut Res 29(3):3648–3658

Usman N, Nduka KN (2022) Announcement effect of COVID-19 on cryptocurrencies. Asian Econ Lett 3:29953

Westfall PH (2014). “Kurtosis as peakedness, 1905–2014.” The American Statistician 68(3): 191–195. Retrieved 18 July 2019 from http://www.ncbi.nlm.nih.gov/pmc/articles/PMC4321753/

Yaya OS, Ogbonna AE, Mudida R (2019) Hysteresis of unemployment rates in Africa: new findings from Fourier ADF test. Qual Quant. https://doi.org/10.1007/s11135-019-00894-6

Zivot E, Andrews DWK (1992) Further evidence on the great crash, the oil-price shock and the unit root hypothesis. J Bus Econ Statist 10:251–270

Acknowledgements

The authors gratefully acknowledge the insightful comments and suggestions of the peer-reviewers towards improving the quality of this manuscript.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Disclaimer statement

Any views stated are exclusively those of the author(s) and should not be construed as representing those of the Central Bank of Nigeria (CBN).

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

About this article

Cite this article

Godday, E.U., Usman, N. & Salisu, A.A. Testing for unemployment persistence in Nigeria. Econ Change Restruct 55, 2605–2630 (2022). https://doi.org/10.1007/s10644-022-09395-3

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10644-022-09395-3