Abstract

The elasticity of substitution between capital and labor (\(\sigma\)) is usually considered a “deep parameter”. This paper shows, in contrast, that \(\sigma\) is affected by both globalization and technology, and that different intensities in these drivers have different consequences for the OECD and the non-OECD economies. In the OECD, we find that the elasticity of substitution between capital and labor is below unity; that it increases along with the degree of globalization; but it decreases with the level of technology. Although results for the non-OECD area are more heterogeneous, we find that technology enhances the substitutability between capital and labor. We also find evidence of a non-significant impact of the capital-output ratio on the labor share irrespective of the degree of globalization (which would be consistent with an average aggregate Cobb–Douglas technology). Given the relevance of \(\sigma\) for economic growth and the functional distribution of income, the intertwined linkage among globalization, technology and the elasticity of substitution should be taken into account in any policy makers’ objective function.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

The elasticity of substitution between capital and labor (\(\sigma\)) is a key macroeconomic parameter. It determines the path of economic growth, affects the functional distribution of income, and conditions the impacts of fiscal and monetary policies (Klump and de La Grandville 2000; Chirinko 2008). Given its prominence, intense efforts to estimate its value should come as no surprise (Antràs 2004; Chirinko 2008; Chirinko and Mallick 2014). However, although there is a wide range of values found for \(\sigma\) across countries and periods, most of the studies rely on Constant Elasticity of Substitution (CES) production functions which, by definition, hinder variations in its value, and lead \(\sigma\) to be treated as a deep parameter.

This paper, in contrast, takes an empirical perspective in search of potential determinants of \(\sigma\). To undertake this analysis, we depart from a class of changing elasticity of substitution production functions developed by Antony (2009a, b, 2010), whose main feature is that variations in the relative factor intensity (the capital-labor ratio) may cause changes in \(\sigma\).

To identify the change in \(\sigma\) the strategy we follow is given by Bentolila and Saint-Paul’s (2003) framework, where the relationship between the labor income share and capital intensity (the capital-output ratio) can be used to infer the magnitude of \(\sigma\). However, given the close relationship between the capital-output ratio and Antony’s main determinant of \(\sigma\) (the relative factor intensity), we focus directly on two major phenomena driving the path of the capital-labor ratio: globalization and technological change (see Sect. 2).

From a methodological point of view, we allow \(\sigma\) to be conditioned by globalization and technology by using multiplicative interaction models, which are estimated by both standard dynamic panel data models, and Mean Group-style estimators based on common factor models (see Eberhardt and Teal 2011).

Our database contains information for a maximum of 51 economies (listed in Table A1, in the “Online Appendix”), with a sample period running from 1970 to 2009. The main findings of our analysis are (1) that both globalization and technology affect the elasticity of substitution between capital and labor; and (2) that this is expressed in different patterns in the OECD and non-OECD economies.

For the OECD, the results are robust and conclusive. We find that labor and capital are complements (\(\sigma <1\)); that \(\sigma\) increases along with the degree of globalization, but it decreases with the level of technology. The first result confirms previous findings in the literature (Antràs 2004; Chirinko 2008; Chirinko and Mallick 2014); the second one implies that globalization enhances the substitutability between production factors, and provides empirical support to literature in this area (see among others, Rodrik 1997; Slaughter 2001; Saam 2008; Hijzen and Swaim 2010). The third result implies that technological change boosts factors’ complementarity, and is compatible with both the skill-biased technological change and the capital-skill complementarity hypotheses.

Although our results are not so robust for the non-OECD economies, they still yield some useful outcomes. The main one is that the elasticity of substitution between capital and labor becomes larger along with the level of technology. We hypothesize that this enhanced substitutability takes place at early stages of the development process, when standard technologies help mechanizing outdated labor-intensive tasks. With respect to globalization, however, results are more complex and difficult to interpret, even though we find evidence of a non-significant impact of the capital-output ratio on the labor share irrespective of the degree of globalization (which implies a unit \(\sigma\)). These inconclusive results could be due to the inherent heterogeneity within this area, as well as to their lower quality data. However, the fact that \(\sigma\) is larger in developing than in developed countries reinforces the capital-skill complementarity hypothesis given the larger share of skill workers in the later (Krusell et al. 2000).

To check for robustness and explore to what extent heterogeneities are relevant in driving the results for the non-OECD countries, we further study the impact of globalization by considering alternative country classifications by income level (low, middle, and high) and the world region they belong to (Europe and Central Asia, East Asia and Pacific, Latin America and Caribbean, and Sub Saharan Africa). For the high income group, and for Europe and Central Asia, the findings closely resemble those for the OECD countries. They thus seem to confirm what appears a solid piece of evidence regarding the positive relationship between globalization and \(\sigma\). For the middle income group, and the other three world regions, the absence of a significant pattern seems also a robust finding. It is only the low income level group which detaches from the rest by showing a similar globalization effect on \(\sigma\) to the one found for the developed countries. Given the small number of countries within this group, however, this result should be considered with caution and open to further research.

Our findings are related to the functional distribution of income and economic growth. From the economic growth literature we have learned that the more flexible a production function is (i.e. the higher the value of \(\sigma\)), the larger the potential growth that can be achieved. However, the value of \(\sigma\) does also affect the functional income distribution. Given that this effect depends on the pattern followed by the capital-output ratio, a higher value of \(\sigma\) has an ambiguous impact on functional inequality. Consequently, the intertwined linkage among globalization, technology and the elasticity of substitution should be taken into account in any policy makers’ objective function.

In any case, this analysis should be considered as a first step in trying to understand how globalization and technological change affect \(\sigma\). Unfortunately, a clear identification of the transmission channels remains an important issue for future research.

The remaining of the paper is structured as follows. Section 2 places our paper in the literature, while Sect. 3 deals with some crucial theoretical issues. Section 4 presents the econometric methodology and Sect. 5 the data. Section 6 shows the results. Section 7 concludes.

2 \(\sigma\), factor intensities, globalization and technology

The elasticity of substitution between capital and labor, \(\sigma\), is a key parameter to understand the sources of economic growth and the resulting consequences for the economy’s functional distribution of income. This has led the literature to be concerned mainly with the value of \(\sigma\) but not as much, to the best of our knowledge, to the reasons why it may vary, to its empirical determinants, and to the consequences of the changes in these determinants.

In the Cobb-Douglas framework, in which the value of \(\sigma\) is constant and equal to one, we can learn on the relative contribution of the production factors to growth (Solow 1957). However, the technology is exogenously given, growth is achieved through capital deepening, and the factor shares are constant through time. Under the more flexible CES framework, \(\sigma\) may divert from unity, and appraisals may be conducted in terms of two crucial issues.

The first one is the relationship between the elasticity of substitution and the evolution of factor shares. When \(\sigma\) differs from unity, the dynamics of the labor share may be examined under the assumption of perfect or imperfect competition in the product market (Bentolila and Saint-Paul 2003; Raurich et al. 2012; Karabarbounis and Neiman 2014). Overall, this strand of literature has provided insights on the causes behind the downward trend experienced by the labor income share in last decades.

The second issue is the relationship between the elasticity of substitution and relative factor intensity (i.e. the ratio between capital and labor, or between labor and capital), which has been used to account for another major phenomenon such as structural change—a systematic change in the relative importance of various sectors. In this regard, Acemoglu and Guerrieri (2008) show that sectors with greater capital intensity tend to grow more, because they respond further to capital deepening. The resulting situation, of non-balanced growth, is still compatible in the long-run with Kaldor stylized facts.

Although most of the literature has tended to work with CES type production functions, growing attention has been devoted to relax the assumption of a constant elasticity of substitution, and understand the determinants of \(\sigma\) and the reasons why it may vary. One possibility is the development of Variable Elasticity of Substitution (VES) production functions (Revankar 1971).Footnote 1 This type of function, however, implies a parametric and strictly monotonic path of \(\sigma\), which has to be above or below 1, but cannot cross.

An alternative is the changing elasticity of substitution production function (Antony 2010), which can be seen as a second generation of VES production functions overcoming the previous restriction. The simplest version takes the form of a dual elasticity of substitution production function, such as Eq. (4) below (Antony 2009a, b). The intuitive idea behind is that the consideration of different relative factor intensities—reflecting, for example, a process of capital deepening—may be embedded in an otherwise standard CES production function, and thus be associated to different elasticities of substitution.

The production functions by Antony, however, do not specify the mechanisms through which changes in relative factor intensities affect \(\sigma\), nor the direction of the change in \(\sigma\) associated to such different intensities. From a theoretical point of view, this can be learned from the works by Saam (2008) and Irmen (2008). Saam (2008) develops a model where openness to trade may raise the elasticity of substitution between capital and labor, and, thereby, the prospects of economic growth. Irmen (2008), in turn, makes explicit that a key condition for this result to hold is that capital intensities in the economies considered grow at different rates.

In this context, there are three transmission channels by which openness to trade is expected to affect capital intensities. The first one is a change in intertemporal preferences affecting the saving rate, and thus causing a different path in capital accumulation. The second one arises from Heckscher–Ohlin-type models, which predict that economies specialize in the production of goods that use the relatively abundant factor. This would explain the specialization of OECD countries in capital-intensive goods, and hence their relative increase in capital deepening. The third transmission channel is the possibility of vertical fragmentation of the production process between developed and developing countries, which could cause further capital deepening in both groups (Jones and Kierzkowski 1998; Feenstra and Hanson 1999, 2001).

Of course, the possibility of vertical fragmentation is intimately related to its feasibility brought by technological progress. In effect, the literature has shown that capital intensities also react to technological progress, which may have additional effects on \(\sigma\). In the standard neoclassical textbook model, technology is modelled as labor-augmenting to ensure the existence of a steady state (Barro and Sala-i Martin 2004). Departing from this benchmark, Acemoglu (2003) adds the possibility of capital-augmenting technical change, and shows that in the long-run the model behaves similarly to the standard one, with just labor augmenting innovations along the balanced growth path. However, capital-augmenting innovations may also take place along the transition path. This allows movements in the factor shares, provided the value of \(\sigma\) is below unity. A similar feature is present in Bentolila and Saint-Paul (2003), where capital-augmenting technical change is one of the determinants that may cause short- and medium-run departures from the long-run equilibrium.

In this context, the transmission channel by which technology is expected to affect capital intensities are efficiency gains. These may induce capital deepening by increasing labor productivity that will, in turn, boost the marginal productivity of capital. Along these lines, Madsen (2010), for example, extends the model by Abel and Blanchard (1983) to show the causal relationship between total factor productivity (TFP) and capital-deepening.

In a nutshell, the direction of the change in \(\sigma\) associated to different relative factor intensities in Antony (2009a, b, 2010) is ambiguous. We do have Saam (2008), however, who specifies that openness to trade increases \(\sigma\) by enhancing capital deepening. The problem with Sam is that openness to trade is just a “a co-determinant” of the elasticity of substitution, which is independent of technology (Irmen 2008).Footnote 2 Hence, from an empirical perspective, the missing point after Saam and Antonys work is to examine how the elasticity of substitution responds to globalization and technology, taking simultaneously into account the linkage between the two.

3 Theoretical background

Given the previous discussion, and to shed light into the above mentioned missing point after Saam’s (2008) work, we extend Bentolila and Saint-Paul’s (2003) framework by departing from the class of changing elasticity of substitution production function proposed by Antony (2009a, b, 2010), in which different factor intensities yield different values for the elasticity of substitution.

3.1 The share-capital schedule and \(\sigma\)

Bentolila and Saint-Paul (2003) show that—under a set of assumptions such as a differentiable production function, constant returns to scale, and that labor is paid its marginal product—a unique function g exists relating the labor income share (\(s_{L}\)) and the capital-output ratio (k):

This stable relationship is called the share-capital (SK) schedule (or curve). It is unaltered by changes in relative factor prices or quantities, and by labor-augmenting technical progress. Shifts of the SK schedule may be explained by capital-augmenting technology or by the increase of intermediate inputs prices. In turn, factors that generate a gap between the marginal product of labor and the real wage (for example, union bargaining power, and labor adjustment costs), would cause shifts off the SK curve.

The analysis of the SK schedule is stressed to deserve special attention because it is closely related to \(\sigma\) by means of the following equation:Footnote 3

In Eq. (2), the response of the labor share to changes in the capital-output ratio is related to \(\sigma\), the labor demand elasticity with respect to wages holding capital constant (\(\eta\), which is always negative), and the value of the capital-output ratio (k, which is always a positive).

This expression can be used to endorse the estimation of the labor share elasticity with respect to the capital-output ratio (\(\varepsilon _{S_{L}-k}\)), which is interpreted in terms of the value of \(\sigma\):

In general, the first situation (\(\sigma <1\)) has been associated to developed economies, because of their largest proportion of skilled workers (relative to non-skilled workers) making them more complementary to capital. In turn, the second scenario (\(\sigma >1\)) is more connected to the situation in developing economies, where the larger share of low-skilled workers makes capital and labor more substitutes.Footnote 4

The relationships represented by expression (3) can thus be used to identify the impact on \(\sigma\) of different driving forces.

3.2 An augmented SK curve

Consider a standard CES production function such as:

where Y is output, K is capital, L is labor, A represents capital-augmenting technical change, B labor-augmenting technical change, and \(\epsilon =((\sigma -1)/\sigma )\) where \(\sigma\) is the elasticity of substitution between capital and labor. In that case, under the assumption that labor is paid its marginal product, it can be easily shown that:

This reflects the relationship between the labor income share and the capital-output ratio, which is conditioned to the value of sigma, as explained in (3).

Now consider a dual elasticity of substitution production function which takes the following general form:

where y is output per worker in efficiency units \((y=Y/BL)\), x represents the relative efficiency factor intensity \((\frac{K}{BL})\), and \(x{_b}\) is a baseline value of that relative factor intensity.Footnote 5 The intuition behind this type of production functions is that \(\sigma\) can take different values depending on the relative factor intensity. More specifically, if \(x \ne x{_b}\), then \(\sigma = \frac{1}{1-\rho }\); in turn, if \(x = x{_b}\), then \(\tilde{\sigma } = \frac{1}{1-v}\), where \(\rho\) and v represent the two values that \(\epsilon\) may take depending on the particular factor intensities characterizing each economy or, in a given economy, different time periods. A generalization of this type of production function is presented in Antony (2010), where it is extended to allow for multiple values of \(\sigma\), conditioned on a diversity of intervals of the relative factor intensities.Footnote 6

Using Eq. (4), the corresponding SK schedule may be represented by:

This expression reproduces the essence of Eq. (1) by establishing a relationship between the labor income share and the capital-output ratio. However, this relationship is now conditioned by the value of the input factor intensity, being it either \(x=x{_b}\) or \(x \ne x{_b}\). The crucial point is that this value affects the impact of the capital-output ratio on the labor income share by changing the elasticity of substitution. That is, depending on the value of x, in this simple dual case we will have two possible slopes of the SK curve.

To conclude, given the void in the literature empirically connecting a changing elasticity of substitution to globalization and technology, and given the augmented SK curve obtained by extending Bentolila and Saint-Paul (2003) to meet Antony (2009a, b, 2010), we next move to the empirical analysis.

4 Empirical analysis

In this section we explain the empirical model to be estimated (Sect. 4.1) along with the econometric tools needed (Sect. 4.2).

4.1 Empirical model

Our empirical analysis departs from Bentolila and Saint-Paul (2003), who regress the labor share against the capital-output ratio, controlling for factors that may shift the SK schedule. However, their estimation of a linear additive model assumes that the impact of each explanatory variable is independent of the values taken by the rest of the determinants. This is in contrast to our aim of studying the potential cross-dependencies among the capital-output ratio, globalization and technology, and leads us to move beyond such type of estimation. One simple way to proceed is by including interaction terms among the variables of interest so that the estimated model is still based on Bentolila and Saint-Paul (2003), but augmented with interaction terms such as:

where vector \(\varvec{X_{it}}\) contains Bentolila and Saint-Pauls’s (2003) standard control variables, k is the capital-output ratio, TFP is a proxy of capital-augmenting technological change, and KOF is an empirical measure of globalization. Variables involved in the interaction terms are also included individually in vector \(\varvec{X_{it}}\).

Given Eq. (6), the impact of the capital-output ratio on the labor share is:

and depends on the values taken by the capital-output ratio, globalization, and technological change.

An important aspect, regarding the interpretation of the estimated multiplicative coefficients, is that their analysis just provides a measure of the influence at the mean value of the variables involved. In order to obtain a comprehensive picture, we evaluate this impact at a relevant range of values taken by the modifying variable so as to compute the corresponding marginal effects and standard errors (see Brambor et al. 2006). Once they are computed, we get an evaluation of how the sign of \(\hat{\varepsilon }_{s_{L}-k}\) responds to the changing values of globalization and technological change. Our analysis uses this information to identify the influence of these two major phenomena as determinants of \(\sigma\) [recall Eq. (3)].

4.2 Econometric methodologies

Our empirical study adopts two different approaches. The main analysis is based on results obtained by standard dynamic panel data techniques (System GMM). However, to further explore potential cross-country heterogeneities, we also present our results when obtained by different Mean Group-style estimators (see Eberhardt and Teal 2011; Pesaran 2015 for details on these estimators).

Given that our analysis relies on the estimation of dynamic panel data with yearly frequency, our first approach is subject to the well known dynamic panel bias (Nickell 1981). In order to overcome this problem, our estimations will be carried out by System GMM (denoted in our empirical analysis as BB, on account of the developments in Blundell and Bond 1998). The key contribution of this method is the estimation of a system of equations, one in differences and one in levels, in which the levels of the variables lagged twice, and more, are used as instruments in the difference equation, while the lags of the variables in differences are used as instruments in the level equation.Footnote 7

GMM estimators were originally developed for panel data with a large number of cross-sections relative to the time dimension of the panel. In contrast, the cross-section and time dimensions of our database are, at most, similar in the best case. This could cause estimation problems such as the risk of “instruments proliferation”, which could bias the Hansen test to generate p-values artificially close to 1 and over fit endogenous variables. As Roodman (2009) explains, this is because the instruments count quartic in the time dimension of the panel. To avoid this problem, we have followed Roodmans’ (2009) recommendations of reducing as much as possible, as well as checking the sensitivity of the results to alternative number of lags.Footnote 8

Unfortunately, the fact that GMM methods require a large number of cross-section units hinders the possibility of disaggregating beyond the standard OECD vs non-OECD countries classification. To circumvent this constraint, our second approach will be the estimation of different Mean Group-style estimators based on a common factor model. This will provide us with a robustness check on the first set of results, and will allow a further disaggregation of the sample.

One of the salient features of this approach is that it allows for a country-specific impact of the regressors on the dependent variable. Unobservable factors in the error term are represented by a country fixed-effect and a common factor with different factor loadings which control, respectively, for time-invariant and time-variant heterogeneity. Simultaneously, the regressors can be affected by these, or other common factors. These unobservable processes represent both common global shocks and local spillovers (Chudik et al. 2011; Eberhardt et al. 2013). In addition, these methods are suitable for accounting for structural breaks and business cycle distortions, thus making the use of yearly data perfectly valid.

Estimation by these methods cannot accommodate all the controls that were considered in the estimation of Eq. (6). Indeed, given the way they control for unobservable factors, they have recently been used to estimate economic growth regressions without imposing any specific structure to the production technology (see Eberhardt and Teal 2011; Eberhardt et al. 2013; Eberhardt and Presbitero 2015 among others). We thus use this approach to further explore the role played by globalization in the absence of extra controls and consideration of cross-country heterogeneities that turn the empirical representation into:

Equation (8) is estimated by different methods. All of them allow for a country-specific impact of the variables of interest, but differ in the way they control for potential unobservable heterogeneity. We first present the results for the Pesaran and Smith (1995) Mean Group estimator (MG), which accounts for \(\beta\) heterogeneity, but assumes that the unobservables have a common impact through time (empirically accounted by adding country-specific linear trends). Then, we present those obtained using the more flexible Pesaran (2006) Common Correlated Effects Mean Group estimator (CMG), and the Chudik and Pesaran (2015) Dynamic CMG estimator (CMG1 and CMG2), which beyond parameter heterogenity, allow the unobservable process to have a different impact per country and per year (empirically accounted by augmenting Eq. (8) with the cross-sectional averages of the variables).

Once the heterogeneous models are estimated, we exploit the cross-country heterogeneity from the Mean Group-style estimators’ first stage to identify the effect of globalization on the labor share impact of the capital-output ratio. This is done following different country classifications, which will serve as a robustness check on our previous findings, and will provide us with further insights on the heterogeneities within the group of “non-OECD” countries.

5 Data and stylized facts

5.1 Data

Table 1 lists the variables used and offers a synoptic definition.Footnote 9 Labor shares, capital-output ratios, GDP per capita, and employment growth rates are obtained from the Extended Penn World Table (EPWT 4.0), developed by Adalmir Marquetti and Duncan Foley. From the World Development Indicators (WDI) we get the manufacturing share over GDP, a variable that tries to control for the sectoral economic composition. The proxy for globalization comes from the KOF index database, which accounts for social, economic, and political globalization (Dreher 2006); trade union density from the OECD; and national oil prices from the International Monetary Fund (IMF). The Polity II and TFP indices are obtained, respectively, from the Policy IV and PWT 8.0 databases. Finally, in order to control for the skill composition of the labor force, we include a human capital index from the PWT 9.0 database.

Karabarbounis and Neiman (2014) and Rognlie (2015) have recently emphasized the importance of the labor share and capital stock definitions for the analysis (including/excluding taxes, net vs gross, imputation of mixed income, etc...). The EPWT 4.0 draws information from different United Nations sources and measures the labor income share as the share of total employee compensation in the Gross Domestic Product with no adjustment for mixed rents. In turn, the numerator in the capital-output ratio is the real net capital stock calculated by the Perpetual Inventory Method (PIM) using the investment series from the PWT 7.0, whereas the denominator is the real Gross Domestic Product. In spite of some caveats surrounding investment data from the PWT, regarding their quality (Srinivasan 1995) or the impossibility of abstracting from residential structures (as there is no disaggregation by type of investment), we follow Young and Lawson (2014) and use this database on account of the nature of our analysis covering a large number of both developed and developing countries with yearly basis observations.

5.2 Stylized facts

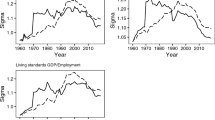

Figure 1 shows the evolution of our main variables of interest for both the OECD and the non-OECD countries. These trajectories are obtained as time dummy coefficients from a GDP weighted regression of the variable of interest against a set of time and country dummies. The initial value is normalized to 100 to facilitate comparisons.Footnote 10

Figure 1a uncovers a parallel falling trend in the labor income shares of the OECD and the non-OECD economies, the latter starting before and being steeper. It is, thus, a worldwide phenomenon with different intensities.

Labor income share, capital-output ratio, capital-labor ratio, KOF and TFP, 1970–2009. a Labor Income Share. b Capital-Output ratio. c Capital-Labor ratio. d KOF index of globalization. e TFP index. Notes: Own calculations obtained as year fixed effects from a GDP weighted regression including country fixed effects to control for the entry and exit of countries throughout the sample. Initial year is normalized to equal 100 in 1970, at the start of the sample period

Figure 1b shows the evolution of the capital-output ratio, which is more volatile in the non-OECD economies. It grows faster than in the OECD between 1970 and early 1980s, but it deteriorates quicker afterwards (by more than 20 pp) until the mid 1990s, to stay relatively flat thereafter. Overall, the ratio has increased by less than 15%, while the continuous positive trend in the OECD area since the late 1980s has led this ratio to grow by around 25%.

Figure 1c illustrates the different evolution of the capital-labor ratio. Whereas the OECD countries show a continuous (and constant) process of capital deepening (being today more than twice the one in 1970), the non-OECD group follows a more heterogeneous pattern. The increase in the ratio went mostly in parallel to the OECD one during the 1970s, but it was followed by an important decrease (40 pp) since then until mid 1990s, when capital gingerly started to rise again with respect to labor. The capital-labor ratio for the non-OECD countries is nowadays almost 1.5 times its value in 1970.

Regarding globalization, Fig. 1d displays a common and positive upward trend between 1970 and 1990. Then, the non-OECD economies experienced a faster exposure to globalization as shown by the much steeper path followed by the KOF index in this area until the Great Recession years. In spite of this faster growth, the degree of globalization in the non-OECD countries is around 20 pp lower than in the OECD countries (Figure A1c of “Online Appendix”).

With respect to technological progress, the pattern is quite different. There is a sort of constant (albeit not large) rate of progress in the OECD countries only crushed by the Great Recession at the end of the sample period. In contrast, the non-OECD countries suffered a severe collapse in the aftermath of the oil price shocks lasting until 1990 (with a 25% fall) to regain, afterwards, a positive trend, and end up 10% below the starting level in 1970.Footnote 11

Overall, the contrast in some of these developments call for a careful appraisal, by areas, on the value of \(\sigma\) and the influence exerted by globalization and technological progress.

6 Results

6.1 Homogeneous dynamic models

Table 2 presents our estimates of the empirical model represented by Eq. (6) by distinguishing between the OECD and the non-OECD countries.

We depart from Bentolila and Saint-Paul (2003), but we extend their analysis by adding globalization and the interaction terms. Bentolila and Saint-Paul (2003) control for the capital-output ratio (k), real oil prices (OIL), total factor productivity (TFP), the employment growth rate (\(\Delta {n}\)), and labor conflicts. As a rough proxy of labor conflicts, due to data limitations we use trade union density (UNION), which is available for the OECD countries. In turn, for the non-OECD countries we account for the degree of democracy (DEM), since differences in this dimension may be specially relevant for these economies.

Given the nature of our data, we further introduce as additional controls the share of manufacturing production (\(MAN\_SHARE\)), in order to account for differences in the productive structure of the countries (Young and Lawson 2014); a human capital index (HC) to control for the labor force composition; and GDP per capita (RGDP) to control for the fact that our labor share measure does not adjust for self-employment incomes (Gollin 2002). This variable is also used by Jayadev (2007) as a proxy of economic development.

All models are estimated by Pooled OLS (POLS), Two-way Fixed-Effects (2FE) and System GMM (BB), and include time dummies. Our reference estimates are the ones obtained by System GMM estimation, and are presented in the last column of each block (OECD and non-OECD).Footnote 12

In the System GMM estimation, beyond controlling for the potential dynamic bias arising from the lagged dependent variable, we control for the potential endogeneity of k, TFP, \(\Delta {n}\), RGDP, DEM, and the interactions. Although we are aware that in a macroeconomic partial equilibrium model, such as the one we are estimating, all the variables could be considered as endogenous, econometric constraints force us to chose a group of variables for which the relationship with the labor share may be more exposed to reverse causality.

Regarding our main variables of interest, globalization is the only one considered as exogenous. The reason is that this phenomenon has triggered significant economic changes, at the same time that it is general enough to be independent from particular changes in the economic conditions of the countries.Footnote 13

To endorse the validity of our results, we conduct a series of specification tests. The AR and Hansen tests check for serial residual correlation and the validity of the instruments; the CD-test corresponds to Pesaran’s (2004) test, which examines the cross-section independence of the residuals; finally, the cross-sectional augmented panel unit root (CIPS) Pesaran’s (2007) test is used to analyze the residuals’ order of integration (Int).

We verify that all the equations are clean of residual autocorrelation, well specified, and deliver stationary residuals. In turn, although the equations for the OECD area show cross-section independence, this is not the case in the non-OECD group. This implies that we will have to be careful when interpreting the results for this area.

Based on the estimated coefficients presented in Table 2, we compute the marginal effects in order to evaluate the labor share impact of the capital-output ratio at a relevant range of values of the KOF index of globalization and the log of TFP. In particular, we analyze the range of values that fall within the 95% confidence interval given by a two standard deviation from the sample mean.Footnote 14

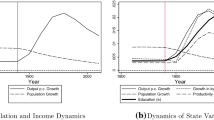

Figure 2 presents the estimated impact of the capital-output ratio on the labor share in the OECD and non-OECD areas respectively. Asterisks in these figures denote significance at the 90% confidence interval.Footnote 15

In Fig. 2a, b, the continuum of values of the KOF index is presented in the horizontal axis. Then, the impact of the capital-output ratio on the labor share along these values is evaluated in five levels of TFP comprising the minimum, maximum, and average values of technology, plus the upper and lower bounds computed as 1 standard deviation from the average.

In Fig. 2c, d, the effect of technology on the elasticity of the labor share with respect to the capital-output ratio is evaluated at selected levels of globalization. We have the continuum of values of the TFP in the horizontal axis, and 5 different trajectories of the KOF index ranging from one extreme case—a value 0% reflecting autarky—to the other extreme case—a country 100% globalized. In the intermediate scenarios, we consider KOF index values of 25, 50 and 75%.

For the OECD area (Fig. 2a, c), we find that the larger the degree of globalization is, the lower the impact of the capital-output ratio on the labor share independently of the countries’ technological level. To be more precise, if we take as reference the average value of TFP, an increase in the level of globalization alters the impact of the capital-output ratio on the labor share from a positive value (0.3 when \(KOF=40\%\)) to a negative one (\(-\,0.15\) when \(KOF=100\%\)).

Even though Eq. (2) shows that other factors could be affecting the SK schedule, this change in the sign can only be explained by a change in \(\sigma\) [recall expression (3)]. This implies that globalization enhances the substitutability between capital and labor, shifting \(\sigma\) from below to above unity. Further, it is a result that supports previous evidence according to which globalization processes (such as offshoring practices, or a larger market for intermediate inputs) allow companies to substitute easier away from labor in the case of an increase in its price (see, among others, Rodrik 1997; Slaughter 2001; Saam 2008; Hijzen and Swaim 2010).

With respect to technology, we find that the higher the technological level, the larger the impact of the capital-output is on the labor share for whatever value taken by the KOF index. Again, the sign change in the slope of the SK schedule implies a decrease in the degree of substitution between production factors (\(\sigma\)), which is compatible with the “capital-skill complementarity” hypothesis (Griliches 1969; Goldin and Katz 1996; Caselli and Coleman 2001) by which “new technologies tend to substitute for unskilled labor in the performance of routine tasks while assisting skilled workers in executing qualified work” (Arpaia et al. 2009, footnote 10). This assertion relies on the presumption that there is a larger share of high skill workers in the OECD economies (Krusell et al. 2000).Footnote 16

Marginal effects across varying levels of globalization and technology. a OECD. b Non-OECD. c OECD. d Non-OECD. Notes: *Results are significant at 10%

In the non-OECD countries (Fig. 2b, d), we find evidence that TFP has the opposite influence and increases the substitutability between production factors. Although our analysis is not able to identify the mechanism by which this occurs, one possible explanation could be the growing mechanization of industries exposed to trade, which are the ones that have received the bulk of FDI and are more subject to outsourcing and offshoring practices. In this sense, progressive substitution of traditional labor-intensive tasks by relatively more capital-intensive ones would explain the enhanced substitutability brought by technological progress in this area.

Moreover, this effect is larger the higher the degree of globalization is (note that for higher levels of globalization the curve in Fig. 2d becomes steeper, so that the larger the decrease in the impact of the capital-output ratio on the labor share becomes with technological progress).

Regarding the effects of globalization, results are not unanimous. A first issue deserving attention is the presence of an inflection point around a value of 40% in the KOF index of globalization. Below this point (i.e. for relatively closed economies), the impact of the capital-output ratio is mainly irrelevant. In contrast, for relatively high levels of globalization (above 40%), the impact of the capital-output ratio on the labor share takes negative values (reflecting \(\sigma >1\)) when the technological level is relatively high. In this context, the more globalized a country is, the smaller the impact of the capital-output ratio on the labor share. This relationship, however, is the opposite at the lowest level of technology, in which case \(\sigma <1\) and the impact of the capital-output ratio on the labor share increases with globalization.

The inconclusive picture obtained for the non-OECD economies may be reflecting the existence of substantial heterogeneities among these countries. To explore whether this is a compelling possibility, next section will exploit country-specific coefficients to further investigate how globalization shapes the capital-output—labor share relationship.Footnote 17

6.2 Heterogeneities in the globalization effects on \(\sigma\)

This subsection presents estimates of Eq. (8) obtained by using different Mean Group-style estimators. Our aim is to check the robustness of our previous results for the developed group of countries, and further explore whether heterogeneities within the non-OECD countries are behind the inconclusive picture we have obtained. We do that by considering alternative classifications of countries including (i) the previous OECD/non-OECD division; (ii) a classification according to their income level (low, middle and high); and (iii) a grouping by world regions (Europe & Central Asia, East Asia & Pacific; Latin America & Caribbean; and Sub Saharan Africa).Footnote 18

Table 3 presents the results for the whole sample using both homogeneous and heterogeneous models. Given their standard use in the literature, and just as reference for comparison purposes, the first three columns present the estimation using the standard POLS and 2FE models, along with the pooled Pesaran (2006) Common Correlated Effects (CCEP). In turn, the last four columns present our preferred Mean Group-style estimators. We show results for the Pesaran and Smith (1995) Mean Group estimator (MG), the Pesaran (2006) Common Correlated Effects Mean Group estimator (CMG), and two versions of the Chudik and Pesaran (2015) Dynamic CMG estimator (CMG1 and CMG2). None of them show problems related to the integration order of the residuals, and just the MG estimator, which is not the central one, rejects the cross-sectional independence of the residuals.

We observe a positive impact of the capital-output ratio and globalization, but a negative one of the interaction, which is robust across the different Mean Group estimators. Given the presence of the interaction term, the corresponding marginal effects must be assessed for a relevant range of values. However, in contrast to Sect. 6.1, this time we compute the marginal effects by exploiting the country-specific coefficients along with the country-specific average level of globalization.Footnote 19

Figures 3, 4 and 5 show the impact of the capital-output ratio on the labor share (in the vertical axis) evaluated (in the horizontal axis) at the average level of globalization of each group (i.e. OECD/non-OECD; level of income; type of world region). To explore the potential existence of broad patterns, we fit the sequence of country observations with a fractional polynomial regression line. One standard deviation coefficient intervals are also added to help in the interpretation of the results.Footnote 20

6.2.1 OECD versus non-OECD countries

Figure 3a presents the results for the OECD countries. As a global pattern, we observe a positive impact of the capital-output ratio on the labor share across average levels of globalization. This implies an elasticity of substitution between capital and labor smaller than one.

Heterogeneous marginal effects: OECD versus non-OECD. a k impact coefficients, OECD sample. b k impact coefficients, non-OECD sample. Notes: Country-specific coefficients for the interaction term and the capital-output impact on the labor income share for an average level of globalization against the average level of globalization. Coefficients are taken from the first CMG stage using Stata’s rreg command to account for outliers. A fitted fractional polynomial regression line is added along with ± one standard deviation (shaded area). The fitted fractional polynomial regression line is obtained by using Stata’s fpfitci command

However, the key relationship regarding globalization is the declining impact of the capital-output ratio on the labor income share when globalization increases, a result that confirms this relationship as a robust finding (robust across estimation method in this case). Given that we are exploiting cross-section heterogeneities at the country-average level of globalization without considering different trajectories of the TFP, changes in the sign of the SK schedule are not expected to be observed. Still, these results are consistent with the ones obtained using homogeneous models where the larger the globalization level, the smaller the impact of the capital-output ratio on the labor share is, and the larger \(\sigma\).

In contrast, when looking at the non-OECD group of countries (Fig. 3b), we observe a negligible impact of the capital-output ratio on the labor share irrespective of the degree of globalization. This is the outcome of the large heterogeneity in countries whose average level of globalization ranges from 40 to 55%. With respect to our previous findings based on the estimation of homogeneous dynamic models, this result does not shed further light on the role (if any) played by globalization. Thus, we explore other possible classifications in search of new insights

6.2.2 Low, middle and high income groups

Unsurprisingly, given the substantial overlapping between the high income group and the OECD countries, Fig. 4a uncovers a positive impact of the capital-output ratio on the labor share for the group of high income economies. This group also shares the feature that this impact declines the larger the degree of globalization is, and confirms its robustness (robust across different classifications involving groups of “advanced” economies).

The fact that most middle and low income level economies do not belong to the OECD provides a first possibility of disaggregation for the non-OECD countries. As shown in Fig. 4b, the middle income level group reproduces the heterogeneous picture characterizing the analysis for the non-OECD, where no clear pattern can be observed.

In turn, the picture for the group of low income countries (Fig. 4c) is rather more promising, especially when combined with the information supplied in the “Online Appendix” where, as explained below when referring to the robustness checks, the same analysis is conducted with alternative measures of globalization (see Figures A11 and A14 of “Online Appendix”). Taken jointly, the inputs from this analysis point to a changing influence of globalization on the impact of the capital-output along a downward path, which moves from positive to negative when globalization attains 35–40%. Although featuring much lower globalization values, this result resembles the one obtained for the OECD economies.

Heterogeneous marginal effects: income groups. a High Income. b Middle Income. c Low Income. Notes: Country-specific coefficients for the interaction term and the capital-output impact on the labor income share for an average level of globalization against the average level of globalization. Coefficients are taken from the first CMG stage using Stata’s rreg command to account for outliers. A fitted fractional polynomial regression line is added along with ± one standard deviation (shaded area). The fitted fractional polynomial regression line is obtained by using Stata’s fpfitci command

6.2.3 World regions

Figure 5 displays four different figures corresponding to selected world regions. It is apparent that the only region displaying a significant pattern is Europe and Central Asia, which is remarkably similar to the ones observed first for the OECD countries, and then for the high income level group of economies.

Given this additional result, it seems safe to claim that the positive impact of the capital-output ratio on the labor share, together with its declining influence along with larger globalization levels, should be taken as a solid block of empirical evidence for the “advanced” economies. Considered along with the results from the homogeneous models, this evidence would be reflecting the increased possibilities of factor substitution achieved by these economies along with the development of the globalization process.

Heterogeneous marginal effects: regions. a Europe and Central Asia. b East Asia and Pacific. c Latin America and Caribbean. d Sub Saharan Africa. Notes: Country-specific coefficients for the interaction term and the capital-output impact on the labor income share for an average level of globalization against the average level of globalization. Coefficients are taken from the first CMG stage using Stata’s rreg command to account for outliers. A fitted fractional polynomial regression line is added along with ± one standard deviation (shaded area). The fitted fractional polynomial regression line is obtained by using Stata’s fpfitci command

In turn, Fig. 5b–d echo the results for the non-OECD countries, which appear to be impassive to globalization in terms of the influence exerted by the capital-labor ratio on the labor share. Two factors could explain this fact. First, income heterogeneity within groups, as tested in the previous subsection. Second, lack of significance due to the small number of countries in each group. Whatever the reason, though, these results would call for further research on these geographic areas and groups of countries.

6.2.4 Robustness checks

Our findings are robust to the type of estimation (whether conducted via homogeneous or heterogeneous models), and display a broadly consistent picture across different country clusters. However, there is still an issue related to globalization and its alternative empirical definitions.Footnote 21

As noted before, the KOF index of globalization provides a comprehensive measure involving the economic, social and political dimensions of this phenomenon. Hence, to check whether our results are robust to this particular definition of globalization, we have taken a sub-index of the aggregate KOF index which just accounts for the economic flows recorded as trade (exports and imports of goods and services), FDI, portfolio investment, and income payments to foreign nationals. All information related to any sort of trade restrictions (import barriers, taxes), and to social and political indicators of globalization, is thus excluded from this sub-index. In addition, we have gathered data on the degree of trade openness (exports plus imports as percent of GDP) from the Penn World Table 9.0, and performed the econometric analysis using these two alternative measures. The results are shown in Table A5 in the “Online Appendix”, and the corresponding marginal effects presented in Figures A10 to A15. They reveal a remarkable stability of the estimated relationships and clearly endorse our empirical findings.

All in all, these results reassert the conclusions reached in Sect. 6.1 for the OECD area, while the lack of a clear pattern found in the non-OECD countries looks like the main outcome from their heterogeneity. The fact that when we split the analysis by levels of income we observe a more clear pattern for the low income level countries is encouraging and should spur further research.

Next subsection further digs into these results by checking whether the departing point (i.e. from a relatively closed or open economy) is relevant for the effects that changes in globalization exert on \(\hat{\varepsilon }_{s_{L}-k}\).

6.3 Asymmetries

We check for the possibility of asymmetries on the influence of globalization on \(\hat{\varepsilon }_{s_{L}-k}\) by conducting a new evaluation of this influence at high and low globalization regimes. This analysis is based on Shin et al. (2014) and Eberhardt and Presbitero (2015), and requires the estimation of the following model:

where the globalization index is decomposed into partial sums above or below a specific threshold. For example, as explained in Eberhardt and Presbitero (2015), if we were to chose a threshold of 0 (i.e. we separate increases from decreases in globalization) we would have:

Given our will to preserve enough degrees of freedom, we use as (ad hoc) threshold the median level of globalization. In order to avoid imprecise coefficient estimations, we only consider countries where at least 10% of all observations are in one regime. We run three different regressions for the total sample (16 countries, threshold 59%), 19 OECD countries (threshold 78%) and 15 non-OECD countries (threshold 45%), and examine whether systematic differences in the interaction coefficients arise when globalization increases from relatively low or high starting levels.

Slope of the marginal effects. a Total sample. b OECD sample. c Non-OECD sample. Notes: Interaction coefficients in the low and high globalization regimes. Coefficients are obtained from a CMG estimation of Eq. (9). x-axis represent the average level of globalization for the lower and higher regimes

Figure 6 presents the information obtained from the new estimation of the interaction coefficients \(\beta _4\) and \(\beta _5\) in Eq. (9). This estimation consists on a standard CMG model where only the dependent variable and the capital-output ratio introduce dynamics.

It is important to remark that the interaction coefficients (whose units are in the vertical axis) represent the slope of the relationship between the labor income share and the capital-output ratio studied in previous sections. This information is now presented taking the form of arrows, with left arrow tips reflecting the value of the interaction coefficient in a relatively low globalization scenario (\(\beta _5\)), and right arrow tips showing the interaction coefficient in a relatively high globalization scenario (\(\beta _4\)). The horizontal axis shows each country’s average level of globalization for these two globalization regimes.

To preview a simple case, let us assume that globalization has no impact on \(\sigma\) when changing in the low regime, but it decreases \(\sigma\) when changing in the high regime. In that case, Fig. 6 would deliver systematic negatively sloped arrows.

Looking at Fig. 6, however, we observe an eloquent absence of systematic behaviors. This holds irrespective of the sample under analysis (total, OECD, non-OECD), and fails to reveal the existence of inflection points in the influence exerted by globalization on the impact of the capital-output ratio on the labor share.

To complement this result, the left block of Table 4 provides the descriptive statistics corresponding to the interaction coefficients presented in Fig. 6. Interestingly, the standard deviation of the interaction coefficients is virtually the same no matter the regime. However, the rest of indicators (mean, minimum and maximum) reveal differences between the OECD and the non-OECD countries. While these indicators systematically increase in the OECD area, thus reflecting a decrease in the negative slope (or, in other words, a less negative impact of globalization on the SK schedule), exactly the opposite holds for the non-OECD group. In addition, information on the corresponding impact coefficients can be found in Figure A16 of “Online Appendix” and in the right block of Table 4. The main feature of these results is a larger dispersion of the impact of the capital-output ratio on the labor share for relatively high degrees of globalization.

Overall, we are unable to provide evidence of systematic patterns in the influence of globalization on the SK schedule when disaggregating by low and high starting globalization levels.

7 Conclusions

We use Bentolila and Saint-Paul’s (2003) framework to analyze the interplay between globalization, technology, and the elasticity of substitution between capital and labor (\(\sigma\)). In this context, we adopt, from Antony (2009a, b, 2010), the possibility that \(\sigma\) varies along with different relative factor intensities. It is through the role of globalization and technology as key determinants of relative factor intensities that we bring the study of their influence on a varying \(\sigma\).

We do so by estimating multiplicative interaction models to reappraise the impact of the capital-output ratio on the labor share when globalization and technology are allowed to influence this impact. The use of yearly data allow us to conduct separate analyses for the OECD and the non-OECD areas, as well as for alternative country classifications. These analyses are first performed through the estimation of homogeneous models, and then complemented via estimation of Mean Group-style estimators. In this way, we exploit the country-specific coefficients to check the robustness of our first set of results. The Mean Group-style estimators are used to reassess the results by the OECD and non-OECD countries, and obtain further evidence for alternative classifications by income level and world region. In addition, the possibility of asymmetries arising from different scenarios of small and large globalization levels is also considered.

Our findings provide a robust picture for the OECD countries, where we find a positive impact of the capital-output ratio on the labor share; a larger substitutability between production factors along with the globalization process; and, in contrast, a larger complementarity driven by technological progress. These results are in line, respectively, with the international trade literature (Slaughter 2001; Saam 2008), and the capital-skill complementarity hypothesis (Arpaia et al. 2009). Furthermore, it is a picture that remains essentially unchanged when looking at the the group of high income level countries, and at the Europe and Central Asia countries.

The results for the non-OECD area are mixed. On one side, we find evidence of an increase in the substitutability between capital and labor as a consequence of technological improvement. On the other side, we find a non-significant impact of the capital-output ratio on the labor share irrespective of the degree of globalization (which would be consistent with an average aggregate Cobb-Douglas technology). When checking alternative classifications, we confirm the lack of influence of globalization in the middle income level group of countries, and also in the East Asia and Pacific, Latin America and Caribbean, and Sub Saharan Africa regions. Only the results for the low income level group of economies somewhat detach from this picture and tend to resemble those for the OECD, although at much lower globalization levels.

One extra result of interest is the absence of evidence of an asymmetric relationship between globalization and the share-capital (SK) schedule. In other words, the fact that globalization may vary departing from a relatively low or high regime does not systematically alter the labor share response to changes in capital intensity.

The magnitude of \(\sigma\) is critical both for economic growth and factor income distribution. While it has been documented that a larger \(\sigma\) could boost potential growth, it could also put pressure on labor conditions by decreasing the workers’ bargaining power and rising functional inequality. It follows that the relevance of globalization and technological change as drivers of \(\sigma\) deserve further attention so as to avoid unexpected and undesirable effects from their continuous progress.

Further research should aim at clarifying the role of globalization in developing countries, where economic heterogeneities and difficulties in the access to long time series of high quality data hinder the analysis. With respect to the OECD, the natural step forward is to examine whether globalization and technology have the same influence across sectors and types of workers skilled/non-skilled. Such disaggregated perspective would help to clarify the mechanisms through which \(\sigma\) is affected by these major phenomena.

Notes

This type of production functions has also been used, among others, by Sato and Hoffman (1968) and Jones and Manuelli (1990). In addition to the VES production functions, Antony (2010) mentions the possibility of using flexible functional forms, such as translog or quadratic production functions. These flexible forms, however, share the problem of having a large number of parameters to be estimated or calibrated.

These production functions are based on the idea from de La Grandville (1989) of normalizing CES production functions.

A dual elasticity of substitution is chosen in this section for the sake of simplicity. The important fact is that changes in the capital-labor ratio can affect the value of \(\sigma\). Antony’s-type production functions do not have any structural model behind and do not provide clear indications about how increases in the capital-labor ratio affect \(\sigma\). Our paper, therefore, has to be seen essentially as an empirical exercise on the determinants of \(\sigma\) leaving the specific policy implications for further research.

Accordingly, both samples are estimated allowing for just four lags of endogenous variables and using the “collapse” instruments option available in the xtabond2 Stata command developed by David Roodman. Table A4 and Figures A8 and A9 in the “Online Appendix” present the results when 3 and 5 lags are used.

Tables A2 and A3 in the “Online Appendix” show the main descriptive statistics by group of countries. Given data availability, our analysis considers 24 OECD countries (621 observations) and 27 non-OECD countries (650 observations).

To complement this information, Figure A1 in the “Online Appendix” shows the evolution of the labor income share, the capital-output ratio and the KOF index taking as initial value the weighted average at 1970. TFP is not included in this figure, as its variation is within country (the index is equal to 1 for all the countries in 2005), thus making different values between groups uninformative.

To complement this general information, Figures A2–A4 in the “Online Appendix” present country specific correlation coefficients of the capital-output ratio, the KOF index of globalization, and TFP with respect to the labor income share (to provide the most global picture, these figures contain information for a wider sample than the one that we could actually use in the analysis due to data limitations). Clear pictures emerge in the first two cases, with worldwide positive and negative correlations across all economies. On the contrary, there is a much disperse result regarding TFP, with a negative correlation in most OECD countries, and a not so clear negative relationship in the non-OECD countries.

As a goodness check, note that the persistence coefficients obtained by the BB estimator lie between the ones estimated by POLS and 2FE (see Bond 2002). They are the largest ones under the POLS estimation (0.84 in the OECD and 0.96 in the non-OECD areas, respectively), the lowest ones under the 2FE estimation (0.66 and 0.79), and take a middle position when estimated by System GMM (0.72 and 0.82). We credit the latter and conclude that the labor share in the non-OECD area is more persistent than in the OECD countries.

The extent to which the process of globalization affects a particular country is certainly shaped by the trade policies and the institutional framework in which these policies are developed (which affect the costs and profits of economic activities). However, country-specific trade policies and the design of institutions are not forward looking but rather reactive to global and domestic changes. It is from this perspective that we consider globalization as an exogenous driver of the influence exerted by the capital-output ratio on the labor share. This interpretation is reinforced by the results presented in columns [2] and [6] in Table A4, and Figure A7 in the “Online Appendix”, which are robust when globalization is considered endogenous.

Figure A5 in the “Online Appendix” shows the Kernel density functions of the KOF and TFP indices in the OECD and non-OECD countries, with the shaded areas indicating the selected values. For the OECD economies, they range from 40 to 100% for the KOF index, and from \(-0.35\) to 0.18 for the TFP; for the non-OECD economies, they go from 22 to 68% for the KOF index, and range between \(-0.34\) and 0.38 for the TFP. Note that the wider interval in the non-OECD group implies a larger volatility of the TFP, and does not reflect at all a better technological level.

It is worth outlining the differences of significance between Table 2 and Fig. 2. While we find a significant impact of the marginal effects in Fig. 2, most of the coefficients in Table 2 are insignificant. For a benchmark model like \(Y=\beta _0+\beta _1X+\beta _2Z+\beta _3XZ+\epsilon\), Brambor et al. (2006) explain this result as follows: “even more important to remember is that the analyst is not directly interested in the significance or insignificance of the model parameters per se anyway. Instead, the analyst who employs a multiplicative interaction model is typically interested in the marginal effect of X on Y. In the case of [our model], this is \(\frac{\partial Y}{\partial X}=\beta _1+\beta _3Z\). As a result, the analyst really wants to know the standard error of this quantity and not the standard error of \(\beta _0\), \(\beta _1\), \(\beta _2\), or \(\beta _3\). The standard error of interest is:

$$\begin{aligned} \hat{\sigma }_{\frac{\partial Y}{\partial X}}=\sqrt{\mathrm {var}(\hat{\beta _1})+Z^2\mathrm {var}(\hat{\beta _3})+2Z\mathrm {cov}(\hat{\beta _1}\hat{\beta _3}) } \end{aligned}$$If the covariance term is negative, as is often the case, then it is entirely possible for \(\beta _1+\beta _3Z\) to be significant for substantively relevant values of Z even if all of the model parameters are insignificant.” (Brambor et al. 2006, p. 70.)

Given that Antony’s production functions lack an explicit transmission mechanism, it is worth noting that additional factors could also play a role on this relationship. Disentangling such factors is left for further research.

In the event of slow capital stock changes and a counter-cyclical behavior of the labor share, yearly data analysis could reflect a spurious positive correlation between the capital-output ratio and the labor income share. To exclude this possibility, Figure A6 in the “Online Appendix” shows the marginal effects for a 3 years average static model estimated by System GMM. It can be observed that our results are robust both for the OECD and the non-OECD countries and, thus, we can safely rule out the possibility of a spurious positive correlation.

Income and region classifications follows the World Bank system. Regarding income levels, we have created three groups in the following way: (i) high income \(=\) High Income OECD \(+\) High Income non-OECD, (ii) Middle Income \(=\) Upper Middle Income, and (iii) Low Income \(=\) Low Income \(+\) Lower Middle Income.

We are aware that some authors have warned against the study of country-specific coefficients in an isolated way (Pedroni 2007; Eberhardt and Teal 2013). For this reason, we will not focus on the specific information obtained for a given country, but on the existence of potential patterns across countries for different average globalization levels. In any case, let us note that our results are robust to the estimation method and no significant differences appear when we use the Chudik and Pesaran (2015) Dynamic CMG estimator (CMG1 and CMG2). We use the CMG estimates because of the larger number of countries included in this estimation.

The graphical analysis in this section is based on Eberhardt and Presbitero (2015). The replication files can be accessed at Markus Eberhardt’s personal website: https://sites.google.com/site/medevecon/publications-and-working-papers (by clicking “Replication data and do-files” below Eberhardt and Presbitero 2015).

Although we have tried to use alternative proxies for technological change, we have not found an alternative that covers enough sample to undertake a reliable robustness check.

References

Abel, A. B., & Blanchard, O. J. (1983). An intertemporal model of saving and investment. Econometrica, 51(3), 675–92.

Acemoglu, D. (2003). Labor and capital-augmenting technical change. Journal of the European Economic Association, 1(1), 1–37.

Acemoglu, D., & Guerrieri, V. (2008). Capital deepening and nonbalanced economic growth. Journal of Political Economy, 116(3), 467–498.

Antony, J. (2009a). Capital/labor substitution, capital deepening, and FDI. Journal of Macroeconomics, 31(4), 699–707.

Antony, J. (2009b). A dual elasticity of substitution production function with an application to cross-country inequality. Economics Letters, 102(1), 10–12.

Antony, J. (2010). A class of changing elasticity of substitution production functions. Journal of Economics, 100(2), 165–183.

Antràs, P. (2004). Is the US aggregate production function Cobb–Douglas? New estimates of the elasticity of substitution. Contributions to Macroeconomics, 4(1), 1–36.

Arellano, M., & Bond, S. (1991). Some tests of specification for panel data: Monte Carlo evidence and an application to employment equations. Review of Economic Studies, 58(2), 277–97.

Arpaia, A., Pérez, E., & Pichelmann, K. (2009). Understanding labour income share dynamics in europe. MPRA Paper 15649, University Library of Munich, Germany.

Barro, R., & Sala-i Martin, X. (2004). Economic Growth. McGraw-Hill Advanced Series in Economics. McGraw-Hill.

Bentolila, S., & Saint-Paul, G. (2003). Explaining movements in the labor share. The B.E. Journal of Macroeconomics, 3(1), 1–33.

Blundell, R., & Bond, S. (1998). Initial conditions and moment restrictions in dynamic panel data models. Journal of Econometrics, 87(1), 115–143.

Bond, B., Hoeffler, A., & Temple, J. (2001). GMM estimation of empirical growth models. Economics Papers 2001-W21, Economics Group, Nuffield College, University of Oxford.

Bond, S. (2002). Dynamic panel data models: A guide to micro data methods and practice. Portuguese Economic Journal, 1(2), 141–162.

Brambor, T., Clark, W. R., & Golder, M. (2006). Understanding interaction models: Improving empirical analyses. Political Analysis, 14, 63–82.

Caselli, F., & Coleman, W. J. (2001). Cross-country technology diffusion: The case of computers. American Economic Review, 91(2), 328–335.

Chirinko, R. S. (2008). \(\sigma\): The long and short of it. Journal of Macroeconomics, 30(2), 671–686. The CES Production Function in the Theory and Empirics of Economic Growth.

Chirinko, R. S., & Mallick, D. (2014). The substitution elasticity, factor shares, long-run growth, and the low-frequency panel model. CESifo Working Paper Series 4895, CESifo Group Munich.

Chudik, A., & Pesaran, M. H. (2015). Common correlated effects estimation of heterogeneous dynamic panel data models with weakly exogenous regressors. Journal of Econometrics, 188(2), 393–420. Heterogeneity in Panel Data and in Nonparametric Analysis in honor of Professor Cheng Hsiao.

Chudik, A., Pesaran, M. H., & Tosetti, E. (2011). Weak and strong crosssection dependence and estimation of large panels. Econometrics Journal, 14(1), C45–C90.

Coe, D. T., & Helpman, E. (1995). International R&D spillovers. European Economic Review, 39(5), 859–887.

de La Grandville, O. (1989). In quest of the slutsky diamond. American Economic Review, 79(3), 468–81.

Dreher, A. (2006). Does globalization affect growth? Evidence from a new index of globalization. Applied Economics, 38(10), 1091–1110.

Eberhardt, M., Helmers, C., & Strauss, H. (2013). Do spillovers matter when estimating private returns to R&D? The Review of Economics and Statistics, 95(2), 436–448.

Eberhardt, M., & Presbitero, A. F. (2015). Public debt and growth: Heterogeneity and non-linearity. Journal of International Economics, 97(1), 45–58.

Eberhardt, M., & Teal, F. (2011). Econometrics for grumblers: A new look at the literature on crosscountry growth empirics. Journal of Economic Surveys, 25(1), 109–155.

Eberhardt, M., & Teal, F. (2013). Structural change and cross-country growth empirics. Policy Research Working Paper Series 6335, The World Bank.

Falvey, R., Foster, N., & Greenaway, D. (2004). Imports, exports, knowledge spillovers and growth. Economics Letters, 85(2), 209–213.

Feenstra, R., & Hanson, G. (2001). Global production sharing and rising inequality: A survey of trade and wages. NBER Working Papers 8372, National Bureau of Economic Research, Inc.

Feenstra, R. C., & Hanson, G. H. (1999). The impact of outsourcing and high-technology capital on wages: Estimates for the united states, 1979–1990. The Quarterly Journal of Economics, 114(3), 907–940.

Goldin, C., & Katz, L. F. (1996). The origins of technology-skill complementarity. NBER Working Papers 5657, National Bureau of Economic Research, Inc.

Gollin, D. (2002). Getting income shares right. Journal of Political Economy, 110(2), 458–474.

Griliches, Z. (1969). Capital-skill complementarity. The Review of Economics and Statistics, 51(4), 465–68.

Hijzen, A., & Swaim, P. (2010). Offshoring, labour market institutions and the elasticity of labour demand. European Economic Review, 54(8), 1016–1034.

Irmen, A. (2008). Comment on “On the openness to trade as a determinant of the macroeconomic elasticity of substitution”. Journal of Macroeconomics, 30(2), 703–706.

Jayadev, A. (2007). Capital account openness and the labour share of income. Cambridge Journal of Economics, 31(3), 423–443.

Jones, L. E., & Manuelli, R. E. (1990). A convex model of equilibrium growth: Theory and policy implications. Journal of Political Economy, 98(5), 1008–38.

Jones, R., & Kierzkowski, H. (1998). Globalization and the consequences of international fragmentation. In G. C. Rudiger Dornbusch & M. Obsfeld (Eds.), Money, factor mobility and trade: The Festschrift in honor of Robert A. Mundell. Cambridge, MA: MIT Press.

Karabarbounis, L., & Neiman, B. (2014). The global decline of the labor share. The Quarterly Journal of Economics, 129(1), 61–103.

Klump, R., & de La Grandville, O. (2000). Economic growth and the elasticity of substitution: Two theorems and some suggestions. American Economic Review, 90(1), 282–291.

Krusell, P., Ohanian, L. E., Ríos-Rull, J.-V., & Violante, G. L. (2000). Capital-skill complementarity and inequality: A macroeconomic analysis. Econometrica, 68(5), 1029–1054.

Madsen, J. (2010). Growth and capital deepening since 1870: Is it all technological progress? Journal of Macroeconomics, 32(2), 641–656.

Nickell, S. J. (1981). Biases in dynamic models with fixed effects. Econometrica, 49(6), 1417–26.

Pedroni, P. (2007). Social capital, barriers to production and capital shares: implications for the importance of parameter heterogeneity from a nonstationary panel approach. Journal of Applied Econometrics, 22(2), 429–451.

Pesaran, M. (2004). General diagnostic tests for cross section dependence in panels. Cambridge Working Papers in Economics 0435, Faculty of Economics, University of Cambridge.

Pesaran, M. H. (2006). Estimation and inference in large heterogeneous panels with a multifactor error structure. Econometrica, 74(4), 967–1012.

Pesaran, M. H. (2007). A simple panel unit root test in the presence of cross-section dependence. Journal of Applied Econometrics, 22(2), 265–312.

Pesaran, M. H. (2015). Time series and panel data econometrics. Oxford: Oxford University Press.

Pesaran, M. H., & Smith, R. (1995). Estimating long-run relationships from dynamic heterogeneous panels. Journal of Econometrics, 68(1), 79–113.

Raurich, X., Sala, H., & Sorolla, V. (2012). Factor shares, the price markup, and the elasticity of substitution between capital and labor. Journal of Macroeconomics, 34(1), 181–198.

Revankar, N. S. (1971). A class of variable elasticity of substitution production functions. Econometrica, 39(1), 61–71.

Rodrik, D. (1997). Has globalization gone too far?. Washington, DC: Peterson Institute for International Economics.

Rognlie, M. (2015). Deciphering the fall and rise in the net capital share. Brookings papers on economic activity, BPEA.

Roodman, D. (2009). How to do xtabond2: An introduction to difference and system GMM in stata. Stata Journal, 9(1), 86–136.

Saam, M. (2008). Openness to trade as a determinant of the macroeconomic elasticity of substitution. Journal of Macroeconomics, 30(2), 691–702.

Sachs, J. (2000). Globalization and patterns of economic development. Review of World Economics, 136(4), 579–600.

Sato, R., & Hoffman, R. (1968). Production functions with variable elasticity of factor substitution: Some analysis and testing. The Review of Economics and Statistics, 50, 453–460.

Shin, Y., Yu, B., & Greenwood-Nimmo, M. (2014). Modelling asymmetric cointegration and dynamic multipliers in a nonlinear ARDL framework. In W. Horrace & R. Sickles (Eds.), The Festschrift in honor of Peter Schmidt. New York, NY: Springer.

Slaughter, M. J. (2001). International trade and labor-demand elasticities. Journal of International Economics, 54(1), 27–56.

Solow, R. M. (1957). Technical change and the aggregate production function. The Review of Economics and Statistics, 39(3), 312–320.

Srinivasan, T. N. (1995). Long-run growth theories and empirics: Anything new? In Growth theories in light of the East Asian experience, NBER-EASE, Volume 4, NBER Chapters, pp. 37–70. National Bureau of Economic Research, Inc.

Young, A. T., & Lawson, R. A. (2014). Capitalism and labor shares: A cross-country panel study. European Journal of Political Economy, 33(C), 20–36.

Acknowledgements