Abstract

This article presents the hypothesis that exogenous shocks in the electricity market, through variations in prices that are independent of changes in oil prices, may affect the business cycle of the Chilean economy in the short and medium term. The results of our research confirm this hypothesis: shocks of different signs that modify investment in power generation—delays or new investment in renewable energies—have played an important role in the fluctuation of the business cycle. For example, the comparison of different scenarios reveals that after a few years, delays could have caused losses of around 6.0% of GDP growth, because the price of electricity would have been far from its equilibrium value for a long time. Therefore, without the strong investment in renewables, among other technologies, the delays would have materialized, resulting in relevant costs to the economy. These results have important policy implications. Chile has been a leader in Latin America in terms of electricity market reform since 1982. Therefore, it is essential to study possible changes in the Chilean electricity market, to the extent that it could lead other countries to question the benefits of implementing similar market reforms, especially if negative shocks in the electricity generation sector are not compensated by new investments.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

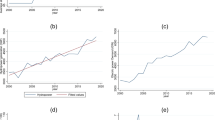

A few years ago, the development of new electricity power plants in Chile was subject to important delays and even cancellations, due to factors exogenous to the projects themselves. These factors are generally political in nature and have generated substantial obstacles in the project approval process. The time required to obtain environmental approvals by state agencies has almost doubled, on average, in the period of 1995–2011, as shown in Fig. 1 (Fuentes 2013). However, the electricity market reacted with strong investments in renewable energy, among other technologies, largely offsetting the potential negative effects of these delays and cancellations.

Source: Authors’ calculations

Average length of environmental processing of power stations per year in Chile.

These delays, in the period under analysis, could have caused electricity prices to rise for long periods of time. The resulting dynamic has created a new type of supply shock for the Chilean economy, similar to oil price shocks. In this paper, we show how strong changes in investment decisions in the construction of power plants are connected to the business cycle, through changes in the price of electricity which are independent of changes in the price of oil. The principal characteristic of electricity price dynamics in Chile is that, after a change, the level of this variable remains high and stable for several years. Thus, the primary concern of the study is to determine if this kind of change in the price level has a macroeconomic effect in Chile.

There is an extensive literature that connects the business cycle with fluctuations in the price of energy mainly through shocks in oil prices, since the early works by Rasche (1980) and Hamilton (1983) up to more recent works by Leduc and Sill (2007), Krey (2007), Kilian (2008b), and Oladosu (2009). According to Kilian (2008a), there are four reasons why the oil price has monopolized the attention of economists. First, oil prices have undergone strong and sustained increases and decreases. Second, the demand for oil is relatively inelastic. Third, changes in oil prices are exogenous—that is, they have external origins—and occur in the presence of important imperfections in labor markets characterized by sticky wages as in Blanchard and Galí (2007). Fourth, energy price hikes often happen in combination with major economic disruptions, such as recessions, unemployment, and high inflation. The literature pays much less attention to analyze the impact of the prices of natural gas and coal on the business cycle fluctuations, and some examples are the following studies Lutz and Meyer (2009) and Choi et al. (2010).

Ultimately, fluctuations in the price of electricity and their impact on the business cycle have only been explained by changes in the price of inputs to produce this energy—namely, oil, natural gas, and coal—and not by direct changes in the electricity sector, for instance Mohammadi (2009) and He et al. (2010).

We propose a direct methodology to measure the impact of investment decisions in the electricity market on the economy. First the electricity prices for different scenarios are simulated. The different electricity price scenarios are then introduced into a dynamic stochastic general equilibrium model, which is the standard methodology for analyzing the business cycle, where the macroeconomic variables are measured as log-deviations from the steady state. The contribution of electricity is incorporated explicitly in the macroeconomic model through a lumpy adjustment model, which is estimated using Bayesian estimation.Footnote 1 In particular, we try to measure whether a persistent and stable deviation in the electricity price from its steady-state value has a strong macroeconomic effect on other variables, such as GDP, investment, consumption, and employment.

We separate price determination in the electricity sector from macroeconomic modeling for the sake of simplicity. The incorporation of the sector’s capital and labor decisions would complicate the macroeconomic modeling, without providing further information about the aggregate impact of the price of this sector on economy. In this regard, we show evidence in this study that this assumption is valid for several countries (see Sect. 2).

By simulating different scenarios for a prolonged period—arbitrarily defined as thirteen years—, we estimate that the cumulative impact of delays in the construction of new power plants in Chile on GDP growth could have been around 6.0% in the period, with the consequent negative effect on private investment, domestic consumption, and employment. Therefore, without the strong investment in renewable energies, among other technologies, delays would have materialized, producing important costs for the Chilean economy. In addition, in June 2019 the connection of Chile’s two largest networks was completed, allowing the massive entry of renewable energy into the system. According to the premise of our study, this project should reduce the price of electricity, as also predicted in Bustos and Fuentes (2017) and Bustos and Fuentes (2016).

The effect on GDP and the impact on employment depends crucially on some key parameters such as the persistence of the electricity price shock, the value of labor demand elasticity, and the adjustment of hiring inputs. Using Bayes’ factors, we confirm that the best model is one that has a high persistence in price shocks, a low elasticity of labor demand, and a high persistence in hiring labor. In other words, the values of the parameters that allow electricity price shocks to have a relevant effect on the economy, even though the electricity sector represents a low share of GDP.

The results obtained are relevant for both developing and developed countries that must delay important investment projects due to the associated negative externalities. This is often the case for projects in electricity generation, regardless of whether they involve renewable energies. There are at least two reasons why delays are likely to arise in these projects. First, the increasing empowerment of civil society in modern democracies makes decision-making processes more participatory and hence more complex, which can lengthen the time frame for defining the use of the available lands. Second, environmental issues are a growing concern, due to the lack of global solutions to the external effects of these large-scale projects. The resulting conflicts can translate into delays on electrical projects, beyond the mitigation policies and compensations that can be implemented in each case. Such delays increase the financial costs and ultimately prices, not only in terms of the costs considered in the initial plans, but also through unexpected costs that arise to mitigate the effects on society, if they were not included in the cost-benefit analysis.

The Chilean case is important because this country was an innovator in electricity market reform in Latin America, privatizing the electricity sector as early as 1982. Other countries followed suit in the early 1990s, including Argentina in 1991, Peru in 1992, Bolivia in 1995, Guatemala and El Salvador in 1996, Panama in 1997, and the Dominican Republic in 1998. All these countries implemented models with important similarities with the Chilean model, where private initiative plays a crucial role in the development of investment. While these countries implemented different pricing mechanisms, they took as a crucial element the role of private initiative in investment, as initially proposed in the region by Chile. As a result, Chile became a leader in market reforms that were adopted by other Latin American countries, which have closely followed the developments in this field in Chile over the years. Consequently, the possibility that the model implemented in Chile, and later replicated in multiple countries in the region, could converge in a specific period to a situation of stagnation due to delays in power plants is a key finding. Such a stagnation would not only have had relevant sectorial and macroeconomic implications for the Chilean economy, but could also call into question the benefits of market reforms in the electricity sector in other countries of the region, especially if negative shocks in the power generation sector are not compensated with new investments.

We organize the document as follows. Section 2 describes several aspects of the study: the introduction of electricity into the macroeconomic model, the calculation of electricity prices, the relationship of this price to investment in the electricity sector, and the calibration and estimation of the macroeconomic model. Section 3 analyzes the macroeconomic impact of shocks associated with investment in power plants in the business cycle. Finally, Sect. 4 presents the main conclusions of the study.

2 The main features of the macroeconomic model

To modelFootnote 2 the impact of the electricity sector on the economy, we must consider some stylized facts. First, the electric energy sector is small measured as a percentage of the GDP, averaging 2.24% for all OECD countries (see Table 1).

Second, regarding the production of electric energy, hydro and thermal power plants generated most of the electricity in OECD countries, including Chile (see Table 1). We, therefore, focus on these technologies to explain power generation in some of our simulations.

Third, the consumption of electric energy as a share of total energy consumption was approximately 22% in the OECD countries in 2013. However, the commercial and industrial sectors use this type of energy intensively: electric energy accounts for 32% and 52% of total energy consumption, respectively, in these sectors. Therefore, electrical power is essential to the production of output in the OECD countries.

Fourth, the electricity price followed its dynamic somewhat independently in the short term relative to other energy prices in the OECD countries (see Fig. 2). Therefore, oil price dynamics alone are not sufficient for understanding the energy situation. The price on the electricity market has its own behavior and thus its impact on the economy. We observe the same pattern for Chile in the period 2000:1–2011:3. Although the two prices followed a similar trend, the oil price fluctuated much more sharply over the period, while the electricity price increased in 2007 and then stayed at this higher level for the rest of the sample.

Source: IEA, Central Bank of Chile, and National Energy Commission, Government of Chile

Real energy prices indexes: OECD (1978–2014) and Chile (2000:1–2011:3).

2.1 Macroeconomic modeling

The macroeconomic model has the following sectors: households, which make decisions on consumption and labor supply; firms, which define the production of intermediate goods—by combining labor, capital, imported inputs, and oil-, investment goods, and commodity goods; private banks, which offer credit for the production of capital goods; a central bank, which sets the interest rate; the government, which determines public spending; and an external sector, which chooses imports (intermediate inputs and oil), capital flows (foreign debt), and exports (intermediate goods and commodities).

Considering the stylized facts discussed at the beginning of Sect. 2, we do not explicitly model the electricity sector in the macroeconomic model. We, therefore, focus only on the price effect of this industry on the economy, since the direct contribution of this sector to the economy as a whole is only marginal.Footnote 3

We diverge from the standard macroeconomic methodology in two ways.Footnote 4 First, we introduce electrical energy as an essential input in the production of intermediate goods.Footnote 5 Second, we restrict the model parameters proposing a simple lumpy adjustment model in hiring inputs such that an increase in the price of electricity causes a contraction in employment in the short term. As explained below, this last consideration is crucial for obtaining correct estimations.

We use a standard Cobb–Douglas production function that includes energy—oil and electricity—, as well as capital, labor, and imported inputs:

where \(Y_{t}^{P}\) is output, \(A_{t}\) is the level of technology, which is modeled as an AR(1) process with a parameter of persistence \({{\delta }_{A}}\), \(L_{t}\) is employment, \(K_{t}\) is the capital stock, \(M_{t}\) is imported inputs, MOIL\(_{t}\) is oil, \(EE_{t}\) is electricity, and \(\xi _{t+k}\) is a AR(1) shock to the quality of capital and provides a source of variation in the return to capital. We can then calculate the unit costs of producing one good in the intermediate sector:

where \(\mathrm{UC}_{t}\) is the unit cost of production, \(W_{t}\) is wages, \(Z_{t}\) is the rental price of the capital, \(SX_{t}\) is the nominal exchange rate, \(P_{t}^{*}\) is the price of imported inputs in dollars, \(\mathrm{POIL}_{t}\) is the international oil price in dollars, and \(\mathrm{PE}_{t}\) is the price of electricity in domestic currency. Therefore, a higher energy price on aggregate produces a direct increase in the unit costs of production (\(\mathrm{UC}_{t}\)), which is transferred directly to the inflation rate of intermediate goods. This can be seen directly from Eq. (2): an increase in PE\(_{t}\), which is dependent on \(1-\alpha _{1}-\alpha _{2}-\alpha _{3}-\alpha _{4}\), affects the \(\mathrm{UC}_{t}\).

The final impact on the economy of a change in the price of energy is more complex, however. It mainly depends on three key aspects included in the macroeconomic model:

-

i.

The substitution between energy and other production inputs (for example, the Cobb–Douglas production function in Eq. (1) explicitly assumes that the elasticity of substitution is one);

-

ii.

The degree of labor flexibility (if wages are very rigid, an energy shock will have a negative impact on aggregate employment); and

-

iii.

The central bank’s response to higher inflation (if an increase in the energy price is inflationary, then the central bank will raise its interest rate, producing a contraction in the economy).

A priori, higher energy prices are expected to have a stagflationary effect, both because production costs will be higher and because the shock will produce a contraction in GDP and, therefore, in employment. The first of these effects is obtained directly from Eq. (2), which shows a positive relationship between \(\mathrm{UC}_{t}\) and the energy price.

Modeling the second effect—namely, the contraction in employment—is more complex. Since an energy price shock makes labor relatively cheaper than electricity, firms could substitute cheap labor for expensive energy under the assumption of a Cobb–Douglas production function. This effect creates an expected paradox in the model: employment would rise instead of falling, which is a counter intuitive result.Footnote 6

In this context, we implement a more flexible and empirical approach for modeling the short-run dynamics of the demand for inputs while maintaining the benefit of having a Cobb–Douglas production function in the long term. First, we use a simple model of microeconomics lumpy adjustment in hiring inputs developed by Berger, Caballero, and Engel (2015) for when the number of agents is large. In the model, a firm abruptly adjusts the accumulated imbalances in its inputs j, and the probability of doing this is independent of the size of the imbalance. We define input\(_{j,i,t}\) as the effective demand for the input and input\(_{j,i,t}^{*}\) as the level that firm i chooses if it adjusts in period t. This depends positively on the level of activity \(y_{t}\) and the level of productivity \(a_{t}\) and negatively on the price of the input expressed in real terms, \(p_{j,t}^{R}\). Then the model is the following:

where \(\theta _{j,t}^\mathrm{input}\) is equal to one if firm i adjusts in period t.

We use Calvo (1983) assumption that the adjustment is independent of the size of the imbalance and therefore it allows us to replace \(\theta _{j,t}^\mathrm{input}\) with its expected value which is the parameter \(pmg\_\mathrm{input}_{j}\). As Berger, Caballero, and Engel (2015) explain, when the number of identical agents converges to infinity, the aggregate dynamic in hiring inputs can be represented as an Euler equation derived from a quadratic adjustment cost model which in linear terms is:

Second, we assume that the model must have an extra ingredient for labor demand. It must assume that the demand for labor is very inelastic to the real wage in the short term, that is, \(\theta _{j}\le 1\). In fact, we expect a low elasticity of substitution in the short term.Footnote 7 This last point is consistent with the above discussion: if employment can be expected to fall, then the effect that should prevail in the short term is the decline in the demand for intermediate goods, not the change in real wages. For the same reasons, we extend the assumption to the demand for fuel transport (see Eq. (6) in the next section).

2.2 Strategy to measure electricity price shocks and to simulate the price of electricity

As we mentioned at the beginning of Sect. 2, the price of electricity \(pe_{t}\) shows a high persistence. Apart from the econometric discussion of whether this variable has a unit root, it is evident from Fig. 2 that this variable \(\rho ^{pe}\) is highly persistent. Thus, our primary concern is to determine whether this kind of change has similar macroeconomic effects in Chile as in other countries. Regarding the model, \(pe_{t}\) is expressed as the percentage deviation from the respective steady-state values \(pe_{t}^{*}\). We, therefore, measure whether a persistent deviation in the electricity price from its steady-state value in this way:

The value of the parameter \(\rho ^{pe}\) is crucial for measuring the relevance of the impact of the electricity price on the economy. On the one hand, if \(\rho ^{pe}\) tends to zero, then this impact is also zero; on the other, if \(\rho ^{pe}\) tends to one, then this impact could be relevant, depending on the other parameters of the model. To estimate Eq. (5), we assume that \(\rho ^{pe}\) can take different priors: namely, low, medium, and high persistence. We test these various alternatives using Bayes factor in Sect. 2.4.

The details of how \(pe_{t}\) is calculated are as follows. The operations model of the Chilean electricity sector establishes a centralized dispatch procedure based on a strict criterion of marginal costs of operation, so as to minimize the overall cost of short-term operations. The tariffication mechanism corresponds to a peak-load pricing model incorporating two different tariffs, one for energy and one for capacity (or power), and implementing a centralized dispatch ordered by increasing cost of operation in the short term. The energy tariff is established as the cost of operation of the last plant dispatched in every moment—that is, the plant with the highest variable cost of energy dispatched. Likewise, the capacity tariff, which is only applied to the consumer during the peak hours of demand for the period, corresponds to the marginal cost of capacity. Therefore, under Chilean regulations, the price of electricity will be relatively high or low depending on the conformation of generation capacity and the level of demand at any given time. In this way, any delays in the scheduled entry of new plants will result in higher spot prices than would be expected under the original timetable.

To illustrate the connection between investment and electricity price, we have made some simulations (see Table 2). For simplicity’s sake, we focus on the case of investment delays, as an example of a sharp change in the sector’s investments, although the opposite case of an increase in investments can be also analyzed. We define the following scenarios for \(pe_{t}\): the super-optimal scenario, which assumes that the electricity system operated without delays for thirteen years—an arbitrary period of time, but we consider it long enough for the investment decisions to have an effect on the price of the sector—; the optimal scenario, which assumes that the system operates without delays from period six onward; and the baseline scenario, which assumes that the current trend in delays continues through the thirteen years.

We use these scenarios to make two comparisons. First, we look at the difference between the super-optimal scenario and the baseline scenario. This comparison allows us to measure, regarding the price differential, the impact of delays that occur for thirteen periods. This is thus a measure of what could have been if delays had not occurred. Second, we compare the optimal scenario and the baseline scenario to measure, regarding the price differential, the effect of eliminating delays from period six onward.

It can also be seen from Table 2 that the effective price during these years moved from the base scenario in the early years to the super-optimal scenario in 2017. This is due to the strong investment made in renewable energy, which ultimately compensated for the delays in the construction of more traditional power plants.

2.3 Electricity versus oil

The other source of energy in the model is oil. This input was introduced into the model in two parts: first, it was included directly in Eq. (1), as an input in the production of intermediate goods MOIL\(_{t}\); second, it is one of the inputs in the intermediate goods distribution TOIL\(_{t}\), to capture the fact that before these goods are consumed or invested, they must be transported using oil:Footnote 8

Unlike electricity, an increase in the oil price has two independent transmission channels that affect the economy. There is an adverse effect on the production of intermediate goods—the same channel as electric energy—and an additional negative effect on the increase in transportation costs.

2.4 Calibration and estimation of the macroeconomic model

The estimation strategy of the macroeconomic model has two parts. First, all parameters related to the stationary state of the model are calibrated. The objective of the calibration is to replicate the stationary state or long-term balance of the Chilean economy, represented by shares over GDP, such as consumption over GDP, investment over GDP, and public expenditure over GDP. The calibrated parameters are only three: the depreciation rate (it is assumed that \(\delta \) is 2.5%), the shares of inputs (\(\alpha \) parameters from Eq. (1) and presented in Table 3), and the share of oil in the cost of transport (Eq. (6), \(\alpha _{P}\) parameter is 2%). All shares are obtained from national accounts data.

The calibration process requires accurate values for the parameters of the production function for intermediate goods (Eq. (1)). These parameters represent the shares of each input in the gross production of intermediate goods in the long term. The calibration of these parameters is based on information from the 2008 input–output matrix and on oil import data from the Central Bank of Chile. Table 3 shows the calibration results, where the share of electricity in the gross output of intermediate goods is around 3%.Footnote 9 Based on this calibration, the model yields a steady-state or long-run equilibrium that is consistent with the information available for the Chilean economy (see Table 3).Footnote 10

Second, we estimate the parameters that define the dynamic of the model with Bayesian estimation.Footnote 11 This decision in the estimation strategy allows us to reduce the problems that can arise from having a limited database. We are indeed using a quarterly database covering a very brief period (2000:2 to 2011:3) that was characterized by relevant delays in power plant construction. The data are in growth rates (multiplied by 100), except for interest rates, which are divided by four to be expressed on a quarterly basis.

In relation to the prior values of the parameters that define electricity price dynamics and the impact of this price on the economy, we chose values based on Bayesian factors that are explained in detail below in this section (see Table 5). The rest of the parameters are estimated using prior values used in the literature (see Table 7). For example, see the studies by Smets and Wouters (2007), An and Schorfheide (2007), and García and González (2014) for the case of Chile.

Although we judge the fit of the model to the data by the observed growth rates, \(100\Delta \ln \left( x_{t}^\mathrm{observed}\right) \), we are interested in measuring the macroeconomic variables as log-deviations from the steady state, \(\left( \ln \left( x_{t}^\mathrm{model}\right) -\ln \left( {\bar{x}}_{t}^\mathrm{model}\right) \right) \), where \({\bar{x}}_{t}^\mathrm{model}\) is the steady state, after a shock in the price of electricity. Equation (7) shows the connection between the two types of variables \(100\Delta \ln \left( x_{t}^\mathrm{observed}\right) \) and \(\left( \ln \left( x_{t}^\mathrm{model}\right) \right. \) \(-\left. \ln \left( {\bar{x}}_{t}^\mathrm{model}\right) \right) \). In other words, given that the model fits data, we deduce the log-deviations from the steady state. The prior for the constant terms is the average growth rate observed in the sample:Footnote 12

In general, most of the values are in line with the values found in other studies using Bayesian estimation for macroeconomic models (for instance, García and González (2014)). Therefore, this section focuses on the parameters associated with the impact of electric energy on the economy (see Table 4). We find that the growth rate of electricity prices is very volatile (6.79%), although it is much lower than the growth rate of oil prices (14.34%). Also, our prior is that the growth rate of the electricity price is highly persistent, with an estimation of 0.88 (\(\rho ^{pe}\)).Footnote 13

As described in Sect. 2.1 (Eq. (4)), the parameters \(pmg\_\mathrm{input}_{j}\) and \(\theta _{j}\) measure the short-term sensitivity of the demand for each input to activity and prices, respectively. Table 7 (in “Appendix B”) and Table 5 show that the coefficients of \(pmg\_\mathrm{input}_{j}\) are between 0.3 and 0.7, which confirms the existence of important adjustment costs in hiring inputs in the short term. Besides, labor demand was inelastic to real wages in the short term (0.05), such that an increase in the energy price reduces employment in both the short and medium terms (see Table 4). This is the result of assuming a very low prior for the parameter \(\theta _{j}\) in labor demand and a small standard deviation for this parameter. We obtain a similar result for the case of fuel labor demand.

Regarding the central bank’s response to inflation, the model estimations are similar to other estimations for the Chilean economy and other countries, with a strong response of the interest rate to inflation (\(\phi _{\pi }\) of 2.39). This parameter is crucial in the study, since a negative energy price shock (electricity and/or oil) could have a second-round effect on the economy if the central bank decided to increase the interest rate to reduce the inflation rate.

In order to check if our priors and, therefore, the estimated values of the parameters are better than other alternatives, we test some of our hypotheses by directly comparing the following alternatives: (i) high, intermediate, and low persistence in the electricity price; and (ii) low elasticity of labor demand with hiring inertia versus unity elasticity of labor demand with no hiring inertia. The base model (BM) has high persistence, low elasticity of labor demand, and hiring inertia. We define the alternative models (AM) in Table 5. We follow Kass and Raftery (1995) in using Bayes’ factors to choose between the different models assuming that all of them are equally likely: if the base model has the largest marginal likelihood, then there is evidence against the alternative models. We consider that there is positive evidence if \(\left( Bayes\ factor\ AM-BM\right) \) is larger than one, strong evidence if it’s between one and two, and definitive evidence if it is larger than two.

As shown in Table 5, we have substantial evidence that the best model is the base model, that is, the model with high persistence in the electricity price, low elasticity of labor demand, and high adjustment costs in hiring this input.

3 Macroeconomic results for the different scenarios

This study only measured the impact of delaying the construction or alternatively entry into operation of power plants—for example, due to an increment in renewable energy investment—assuming no other shocks occurred simultaneously. The results must thus be interpreted using the impulse response functions, which show the trajectory of a variable over time after an exogenous shock. According to Fig. 3, an exogenous increase in the electricity price has a relevant and contractionary effect, especially on GDP, private investment, consumption, and employment. The shape of the impulse responses is standard for a negative supply shock: a contraction with higher inflation or stagflation. However, the reaction of the inflation rate and, therefore, the central bank’s response to increase the monetary policy interest rate are only moderate. Conversely, a shock that reduces the price of electricity produces impulse-response functions that have opposite forms to the images presented in Fig. 3.

Source: Authors’ calculations

Impulse response functions of a one-standard-deviation shock to electricity prices

Table 6 shows the simulations for eight years to for the three different macroeconomic scenarios (super-optimal, optimal, and baseline). These results, which were constructed directly from the impulse response functions, highlight the relevant impact of delaying investment in power plants on the Chilean economy. For the baseline scenario, the table shows the cumulative sum of various negative shocks, which represent delays that hit the economy over time (see Table 2). In contrast, we associate the other two scenarios with the cumulative sum of positive shocks from the absence of delays, that is, new power plants are entering the market at the scheduled time, thereby increasing the supply of electricity and systematically decreasing energy prices in the first period (see Table 2). Table 6 also shows the impact of actual prices on macroeconomic variables by using the macroeconomic model. As the price decreases, influenced by the introduction of new investments in renewable energies, all macroeconomics indicators show positive progress in relation to the baseline scenario.

The analysis of the results in Table 6 is as follows, after eight years, the country would lose the equivalent of two years of growth because the super-optimal scenario did not materialize—this because the Chilean economy’s potential GDP is around \(3\%\). We obtain the result by comparing the difference between the super-optimal scenario and the baseline scenario, or \(6.15\% =4.72\% - (- 1.43\%)\). When we compare the optimal situation with the baseline scenario, the cumulative loss in GDP is much lower, at only 2.75% in the same period. As shown in Table 6, the economy’s loss is concentrated mainly in private investment. In the super-optimal scenario, private investment increases 12.79% compared with the base case. Employment also records a strong effect. Another key variable is consumption: under the super-optimal scenario the cumulative rate of growth is 6.63%.

4 Conclusions and policy implications

Our main conclusion is that strong changes in the construction and operation of new power plants have had a durable impact on the business cycle of the Chilean economy, mainly through the effects on GDP, investment, consumption, and employment. In other words, although the evolution of the Chilean economy is explained by a series of factors, we find that shocks in the energy market—excluding oil price shocks—are important elements in explaining not only the fluctuations of the business cycle but also in growth in the medium term.

First, under the counter factual scenario in which delays had not occurred for the entire simulated period of thirteen years—which we call the super-optimal scenario—, the cumulative growth rate for GDP would have been around 6.0% higher than under the baseline scenario. Private investment is the most strongly affected variable, with a cumulative growth rate of 12.79%. This result is relevant, considering that potential GDP growth in Chile is approximately \(3\%\).

Second, under the counter factual scenario in which delays do not occur from period six onward—which we call the optimal scenario—, the cumulative growth rate of GDP would be 2.75% higher than the baseline scenario. This last result indicates that, ceteris paribus, the loss for the Chilean economy would be irreversible in almost a decade due to delays in building new power plants. The important economic costs of these delays have only been avoided thanks to the strong growth in investment in renewable energies. In this respect, the two main forces driving the development of renewable energies—both characteristics of the electricity market—are technological change and greater empowerment of society, which have driven the market and its regulation in this direction.

These results are relevant from an economic policy perspective because Chile has been an innovator in the liberalization of the electricity market and the introduction of competition in the sector, and a number of countries in Latin America followed Chile’s example. The recent Chilean experience, showing the dramatic impact of investment in the electricity sector on the economy, could help other countries improve the competitive market reforms in their electricity markets, so as to avoid unexpected fluctuations in the business cycle. At the same time, the impact of these fluctuations on the economy could lead other countries to question the benefits of implementing competitive market reforms in their electricity markets.

Finally, one of the main limitations of our study is that, because our model is based on simulations of a stylized model, we did not consider the environmental and health costs of building new power plants. Nevertheless, our results highlight the importance of decisions related to the regulation and planning of the installed capacity of the electricity system, as well as environmental and energy policy, regarding their effect on the business cycle and economic growth.

Notes

To ensure consistency in our results, we use the Metropolis–Hastings algorithm based on two Markov chains, each with a large number of simulations: 150,000 replications to build the estimated distribution of the parameters (posterior). These simulations are implemented after searching for a proper starting point.

Nakov (2010) endogenizes the energy industry, when the impact of the aggregate value of this industry is also relevant for the economy.

For empirical evidence of a low elasticity of substitution between employment and energy, see Hamermesh (1993).

An alternative is to introduce this type of energy as an additional consumption good (Gavin et al. 2013).

Based on data from the Central Bank of Chile.

In “Appendix B” we present the estimation of the macroeconomic model.

For the interest rate: \((1/4)r_{t}^\mathrm{observed}=(1/4)\left\{ \left[ r_{t}^\mathrm{model}-{\bar{r}}\right] -\left[ r_{t-1}^\mathrm{model}-{\bar{r}}\right] +\mathrm{constant}_{t}\right\} \).

The model also imposed a high persistence in the growth rate of oil prices; the estimation was of 0.84 (\(\rho _{OIL}\)), see Table 7.

References

An S, Schorfheide F (2007) Bayesian analysis of DSGE models. Econ Rev 26(2):113–72

Berger D, Caballero R, Engel E (2015) Missing aggregate dynamics: on the slow convergence of lumpy adjustment models. Working papers 412. The University of Chile, Department of Economics

Blanchard OJ, Galí J (2007) The macroeconomic effects of oil shocks: why are the 2000s so different from the 1970s?” No. w13368. National Bureau of Economic Research

Brown SP, Yücel MK (2002) Energy prices and aggregate economic activity: an interpretative survey. Q Rev Econ Financ 42(2):193–208

Bustos J, Fuentes F (2017) Electricity interconnection in Chile: prices versus costs. Energies 10(9):1438

Bustos J, Fuentes F (2016) Economic effects of transmission expansions: the case of the regulated contract market in Chile. IEEE Latin Am Trans 14(4):1711–1716

Calvo G (1983) Staggered prices in a utility maximizing framework. J Monet Econ 12(3):383–98

Choi J, Bakshi BR, Haab T (2010) Effects of a carbon price in the U.S. on economic sectors, resource use, and emissions: an input-output approach. Energy Policy 38(7):3527–36

Davis SJ, Haltiwanger J (2001) Sectoral job creation and destruction responses to oil price changes. J Monet Econ 48(3):465–512

Energy National Commission (2009) Energy balance 2009. https://www.ariae.org/servicio-documental/balances-energeticos-de-chile-contiene-2009-2008-2007-2006-2005-2004-2003-2002. Accessed 6 Mar 2020

Fuentes F (2013) The Chilean electricity model at the crossroads. In: Jacob O, Perticara M, Rodriguez M (eds) The challenge of sustainable development in latin America. Konrad-Adenauer-Stiftung, Rio de Janeiro

Galí J, López-Salido D, Vallés J (2007) Understanding the effects of government spending on consumption. J Eur Econ Assoc 5(1):227–70

García CJ, González W (2014) Why does monetary policy respond to the real exchange rate in small open economies? A Bayesian perspective. Empir Econ 46(3):789–825

Gavin WT, Keen BD, Kydland FE (2013) Monetary policy, the tax code, and the real effects of energy shocks. In: Working paper 2013-019. Federal Reserve Bank of St. Louis

Gertler M, Karadi P (2011) A model of unconventional monetary policy. J Monet Econ 58(1):17–34

Hamermesh DS (1993) Labor Demand. Princeton University Press, Princeton

Hamilton JD (1983) Oil and the macroeconomy since world war II. J Polit Econ 91(2):228–48

Hamilton JD (2010) Nonlinearities and the macroeconomic effects of oil prices. No. 16186. National Bureau of Economic Research

He YX, Zhang SL, Yang LY, Wang YJ, Wang J (2010) Economic analysis of coal price-electricity price adjustment in China based on the CGE model. Energy Policy 38(11):6629–37

Kass RE, Raftery AE (1995) Bayes factors. J Am Stat Assoc 90:773–95

Kilian L (2008a) The economic effects of energy price shocks. J Econ Lit 46(4):871–909

Kilian L (2008b) Why does gasoline cost so much? A joint model of the global crude oil market and the U.S. retail gasoline market. CEPR discussion paper No. DP6919

Krey V, Martinsen D, Wagner HJ (2007) Effects of stochastic energy prices on long-term energy-economic scenarios. Energy 32(12):2340–49

Leduc S, Sill K (2007) Monetary policy, oil shocks, and TFP: accounting for the decline in US volatility. Rev Econ Dyn 10(4):595–614

Lutz C, Meyer B (2009) Economic impacts of higher oil and gas prices: the role of international trade for Germany. Energy Econ 31(6):882–87

Mohammadi H (2009) Electricity prices and fuel costs: long-run relations and short-run dynamics. Energy Econ 31(3):503–09

Nakov A, Pescatori A (2010) Monetary policy trade-offs with a dominant oil producer. J Money Credit Bank 42(1):1–32

Oladosu G (2009) Identifying the oil price-macroeconomy relationship: an empirical mode decomposition analysis of U.S. data. Energy Policy 37(12):5417–26

Rasche RH, Tatom JA (1980) Energy price shocks, aggregate supply, and monetary policy: the theory and the international evidence. Carnegie Rochester Conf Ser Public Policy 14(1):9–93

Sánchez M (2011) Oil shocks and endogenous markups: results from an estimated euro area DSGE model. IEEP 8(3):247–73

Schmitt-Grohé S, Uribe M (2003) Closing small open economy models. J Int Econ 61(1):163–85

Smets F, Wouters R (2007) Shocks and frictions in US business cycles: a Bayesian DSGE approach. Am Econ Rev 97(3):586–606

Vasconez VA, Giraud G, Mc Isaac F, Pham NS (2012) Energy and capital in a new-keynesian framework. halshs-00827666

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Agurto: SYNEX; Fuentes: Universidad Alberto Hurtado; García: Universidad Alberto Hurtado; Skoknic: SYNEX. We thank the editor and two anonymous reviewers for their suggestions and comments. Felipe Pinto and Gabriel Valenzuela provided excellent research assistance.

Appendices

Appendix A: Macroeconomic model

We assume a continuum of infinitely lived households indexed by \(i\in [0,1]\). Following Galí et al. (2007), a fraction of households, \(1-\lambda \), do not have access to capital markets, and thus neither save nor borrow. Their level of consumption is given by their disposable income. The remainder, \((\lambda )\), have access to capital markets and can smooth consumption. The Ricardian households maximizes expected utility, and we assume a separable utility function with habit persistence h:

where:

Subject to the budget constraint for each period k:

where \(C_{t+k}^{o}(i)\) is consumption, \(D_{t+k}^{o}(i)\) are dividends from ownership of firms, \(\Phi \) represents the country risk premium, where \(b_{t+k+1}^{o*}=SX_{t+k+1}B_{t+1}^{o*}/P_{t+k+1}\), \(SX_{t+k}\) is the nominal exchange rate, \(B_{t+k+1}^{o*}\) denotes private net foreign assets, \(W_{t+k}(i)\) is the nominal wage, \(N_{t+k}^{o}(i)\) is the supply of labor or labor force, \(B_{t+k}^{o}(i)\) is government debt held by households, \(R_{t+k}\) and \(R_{t+k}^{*}\) are the gross nominal return on domestic and foreign assets, which is modeled as a AR(1) shock with a parameter of persistence \({{\rho }_{R*}}\), and \(T_{t+k}\) are lump-sum taxes. The risk premium, \(\Phi \), depends on foreign debt, the value of the investment, GDP, and a risk premium shock \(u_{t+k}^{RK}\) (see Schmitt-Grohé and Uribe (2003) and García and González (2014) for details).

There are a continuum of firms indexed by \(j\in [0,1]\) that produce \(Y_{t+k}^{P}(j)\), by using capital \(K_{t+k}(j)\), labor \(L_{t+k}(j)\), imported goods \(M_{t+k}(j)\), oil MOIL\(_{t+k}(j)\), technology \(A_{t+k}(j)\), and energy \(EE_{t+k}(j)\) where \(\Lambda _{t,t+k}\) is the stochastic discount factor and \(\xi _{t+k}\) is a AR(1) shock to the quality of capital and provides a source of variation in the return to capital with a parameter of persistence \({{\rho }_{\xi }}\). Then, the objective function for the firm is:

where:

Additionally, we assume that there is a retailer that buys goods at price of \(P_{m,t+k}\) and receives a signal to optimally set a new price à la Calvo (1983).

where \(\delta _{D}\) measures the level of indexation, \((1-\theta _{D})\) is the probability that a given price can be re-optimized in any particular period, and \(\epsilon _{D}\) is the elasticity of substitution between any two differentiated goods. In parallel, we assume also that there are unions that act as wage setters in the labor market and wages are staggered à la Calvo (1983), in this case the parameters are \(\delta _{w}\), \((1-\theta _{w})\), and \(\epsilon _{W}\).

On the other hand, there are a continuum of firms indexed by \({\bar{j}}\in [0,1]\) that produce homogeneous capital goods and rent them to the intermediate-goods firms (the rental market for capital stock). Firms are owned exclusively by Ricardian households and invest the amount \(I_{t+k}^{o}({\bar{j}})\) to maximize profits.

where f is the adjustment cost such that \(f(1)=f'(1)=0\) and \(f>0\). Firms that produce capital obtain funds from intermediaries as in Gertler and Karadi (2011):

The demand for domestic exports from foreign countries is modeled as follows. There is a demand for each set of differentiated domestic goods, which by assumption depends on total consumption abroad, \(C_{t+k}^{D*}\), which is considered as a AR(1) shock in the estimations with a parameter of persistence \({{\rho }_{{{C}^{D*}}}}\), and on the home price of domestic goods relative to its price in the foreign country:

Nevertheless, we assume that in practice exports, \(X_{t+k}^{D}\), respond more slowly to real exchange rates and foreign demand. Additionally, we include natural resource exports (commodities), the total value of these products is \(SX_{t+k}P_{t+k}^{cu}Q\_c\), where \(P_{t+k}^{cu}\) denotes the international price of the commodity and \(Q\_c\) is production, both variables modeled as AR(1) processes with parameters of persistence \({{\rho }_{Q\_c}}\) and \({{\rho }_{{{P}^{CU}}}}\).

The central bank sets the nominal interest rate according to the following rule:

where:

where \({\bar{R}}\) is the steady-state nominal interest rate, \(\Pi _{t+k}\) the gross rate of inflation, \(\bar{\Pi }\) the gross rate of inflation in steady state (which is one in our model), \(YR_{t+k}\) is the GDP excluding natural resources, \({\bar{YR}}\) is its steady-state value, \({\bar{Q}}_{t+k}\) is the real exchange rate, and \({\bar{Q}}\) is its steady state level. Note that \({{Q}_{t+k}}\),\({{{\bar{Q}}}_{t+k}}\), and \(Q\_c\) are different concepts. These variables correspond to the capital value, real exchange rate, and production of commodity, respectively.

For simplicity, we assume that government expenditure follows a simple rule such that \(G_{t+k}\) depends negatively on public debt. We also assume that fiscal shock is modeled as an AR(1) process with a parameter of persistence \({{\rho }_{G}}\). Finally, aggregating over consumers and firms, the domestic equilibrium and the economy-wide budget identity can be expressed as:

where:

Appendix B: Bayesian estimation

Rights and permissions

About this article

Cite this article

Agurto, R., Fuentes, F., García, C.J. et al. The macroeconomic impact of the electricity price: lessons from Chile. Empir Econ 60, 2407–2428 (2021). https://doi.org/10.1007/s00181-020-01883-7

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00181-020-01883-7