Abstract

Major economic events, such as the global financial crisis, are episodes of identifiable duration that differ from other time periods. Using monthly data on the unemployment rate, labour force participation rate and employment for Australia for the period from 1978 to 2012, we estimate a Markov-switching SVAR model to examine the relationship between unemployment and labour force participation and the performance of the Australian labour market. Three distinct labour market regimes are identified. We find that the labour market switches between periods of low unemployment and high participation, prolonged periods of relative stability and short, sharp periods of high unemployment and low participation. A key finding is that, due to the behaviour of workers not in the labour force, the long-term effect of an upswing in labour hiring results in a lower unemployment rate and a lower labour force participation rate.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

The severe labour market deterioration in most developed countries caused by the global financial crisis (GFC) has refocussed attention on the unemployment rate as a key economic indicator. On the one hand, the fact that unemployment rates seemed to rise simultaneously with declining output growth, rather than with some considerable lag, is possibly another reason for this renewed interest (Fujita and Ramey 2009; Schwartz 2012). While most commentators point to the Lehman Brothers collapse as being the most noteworthy event and the unofficial marker for the onset of the GFC, the global recession was manifesting itself in most OECD labour markets well before September 2008.Footnote 1 On the other hand, high unemployment has been extremely persistent in many countries; the labour market seemingly has fallen into a bad regime. In some cases, whether this reflects a permanent structural shift or adjustment to cyclical factors is contentious (Lazear and Spletzer 2012).

While the timing of the onset of economic crises in most countries is usually clear, what is less certain is how vulnerable a country may be to a severe deterioration in its labour market. Claessens et al. (2009) argue that globally synchronised recessions are longer and deeper than other recessions. Moreover, Reinhart and Rogoff (2009) show that financial crises are associated with significant declines in output and employment; the unemployment rate rises an average of 7 % points over the downphase of the cycle, which lasts on average more than 4 years. In addition, the average duration of synchronised recessions tends to be a quarter longer than non-banking crises. Furceri and Mourougane (2009) show that unemployment rates usually surge in countries hit by a deep financial crisis by an average of 5 % points in 4 years. By contrast, episodes of softer crises are characterised by a much smoother increase in unemployment rates of about 1 % point in the 4 years following the start of a crisis. The expression “jobless recoveries” refers to periods of economic growth with little or no associated increases in employment. An important reason for the absence of a stronger synchronous relationship between the cycle and the unemployment rate is the behaviour of labour force participation. In a recent paper, using quarterly labour market data for ten OECD countries, Brückner and Pappa (2012) show that the unemployment rate and the labour force participation rate both increase in response to a fiscal expansion. They argue that this occurs because the (adverse) wealth effect associated with fiscal stimuli increases labour force participation, but that imperfect matching of new labour force entrants leads to larger increases in unemployment than employment.

In general, the link between movements in the unemployment and labour force participation rates is complicated and the least understood of labour market flows (e.g. see Yashiv 2007; Elsby et al. 2009 and Wasmer 2009). One complication is that the added worker effect and discouraged worker effect operate in opposite directions over the cycle. The latter effect describes the possibility that workers unable to find work in economic downturns become discouraged and leave the labour force. Accordingly, it serves to dampen any rise in the unemployment rate during recessions. The former effect involves workers, usually secondary earners in a household, entering the labour force when the primary earner loses their job. Both effects are discussed in detail in the next section.

In this paper, monthly data for the unemployment rate and labour force participation rate are used to examine the labour market performance of Australia. Both variables are not only key macroeconomic indicators, but also act as key political barometers. Changes in the unemployment rate are a gauge of the economic hardship experienced by the most vulnerable workers over the business cycle. The labour force participation rate is of interest because together with rate of technological progress and the growth of an economy’s endowments, labour force participation is a key determinant of living standards and the growth of real income. It also tells us something about labour market behaviour independently of solely focussing on the unemployment rate. For example, welcome news about a lower unemployment rate can be tempered by news that labour force participation has also fallen. In this paper, changes in the logarithm of employment are used to proxy labour demand. As in Blanchard and Katz (1992) and Debelle and Vickery (1999), our specification of the lag structure allows for shocks to labour demand cause immediate, as well as lagged, effects on the unemployment rate and labour force participation rate; but not vice versa.

An important consideration in modelling these labour market variables is to identify shocks that are informative about their actual behaviour. We model the labour market variables as Markov- switching processes, by treating the labour market as transitioning through phases of expansion, moderation and contraction. Since the breaks for these phases are unknown, we determine them using a regime-switching model. Hamilton (2005) credits Burns and Mitchell (1946) for pioneering this way of thinking. Major economic shocks can be identified as episodes of identifiable duration which differ from “normal” time periods for the labour market. The regime switching occurs due to an idiosyncratic set of domestic labour market institutions as well as any external economic shocks. This behaviour is captured by using transition probabilities that determine the frequency and duration of time spent in high-mean/high-variance or low-mean/low-variance regimes, for example.

The next section discusses the theoretical considerations underlying the relationship between the unemployment rate and labour force participation rate. Section 3 describes the empirical model used to classify the labour market outcomes into different regimes, and Sect. 4 presents the results. Section 5 concludes.

2 The relationship between unemployment and labour force participation

Consider a straightforward extension of the two-state model of labour market dynamics. Workers can be employed, \(e\), unemployed, \(u\), or not in the labour force (at ‘home’), \(h\). The transition probabilities between the states are as follows. The probability of a job separation is \(s\). An unemployed worker has a job finding probability of \(f^{U}\).Footnote 2 Of those not employed, a proportion \(n\) is not in the labour force, with remaining \(1-n\) ‘officially’ unemployed and actively searching for work. Notwithstanding, for those not in the labour force, the probability of finding work is \(f^{H}\). It is reasonable to assume \(f^{U}>f^{H}\).Footnote 3 The model is summarised in Fig. 1.

Flows between the labour market states

The working age population consist of two types, \(i = 1, 2\), i.e. \(P=P_1+P_2\). Type 1 represents the majority of workers who are either single, unmarried, married household heads or primary earners for their families. The other type of worker is secondary earners, typically thought of as married women, who only find or actively seek employment when their spouse loses their job (see Lundberg 1985). In other words, while they are usually out of the labour force, type 2 individuals are still marginally attached to the labour force. We distinguish the behaviour of the types by assuming that \(n_1 <n_2 \le 1\). That is, a higher proportion of the marginally attached workers, who are not employed, are out of the labour force rather than officially unemployed. We also add an \(i\) subscript to the separation rate to facilitate the discussion of the added worker effect below. To summarise, for \(i = 1, 2\),

Since \(e_{ it} +u_{ it} +h_{ it} =1\), the steady-state probabilities are

where \(\Delta _i =[s_i +n_i f^{H}+(1-n_i )f^{U}]\). Note that if \(f^{U}=f^{N}=f\), then we get the familiar two-state unemployment rate, \(u_i^*=s_i /(s_i +f)\) (e.g. Hall 2006; Shimer 2012). At the macroeconomic level, the unemployment rate and labour force participation rate are

The following Proposition contains the key results.

Proposition 1

-

(i)

An increase in the separation rate, \(s_i\), or a decrease in either hiring rate, \(f^{U}\) or \(f^{H}\), raises the unemployment rate and lowers the labour force participation rate;

-

(ii)

An increase in the rate of labour market withdrawal, \(n_i\), is associated with both a lower unemployment rate and lower labour force participation rate.

Proof

From Eq. (3), for \(i=1,2\), \((e_i+u_i)^{2}\Delta _i^{2}{ UR}_{ is_i } =(1-n_i )[n_i f^{H}+(1-n_i )f^{U}]>0\) and \(\Delta _i^{2}{ LFPR}_{ is_i} =-n_i [n_i f^{H}+(1-n_i )f^{U}]<0\); \((e_i +u_i )^{2} \Delta _i^{2}{ UR}_{ if^{U}} = (1-n_i)^{2}s_i >0\) and \(\Delta _i^{2}{ LFPR}_{ if^{U}}=-n_i (1-n_i )s_i <0\); \((e_i +u_i )^{2} \Delta _i^{2}{ UR}_{ if^{H}} =n_i (1-n_i )s_i >0\) and \(\Delta _i^{2}{ LFPR}_{ if^{H}} =-n_i^{2}s_i <0\). For part (ii), \((e_i +u_i)^{2}\Delta _i^{2}{ UR}_{ in_i } =-s_i f^{H}\Delta _i <0\) and \(\Delta _i^{2}{ LFPR}_{ in_i } =-s_i (s_i +f^{U})<0\). \(\square \)

Part (i) shows that a lower rate of job separation, or higher job finding rates, lowers unemployment and raises labour force participation. In contrast, part (ii) indicates that if non-employed workers spend less time looking for work, then the unemployment rate actually falls. This occurs due to the relatively larger impact on the denominator of the unemployment rate and is sometimes referred to as the “unemployment pool” effect.

For given \(n\), the theoretical expectation is that the unemployment rate and the labour force participation rate are inversely related over the cycle. However, if \(n\) is procyclical, then a stronger labour market, associated with higher employment growth, may exhibit a lower unemployment rate and a lower labour force participation rate. It needs to be noted that \(n\) may change for both types of worker if job finding and separation rates change. To gain an initial impression of the factors involved, note that job separations are essentially of two types: voluntary (quits) or involuntary (lay-offs). In terms of job separations, the flow of workers from employment to unemployment is driven by lay-offs and workers losing jobs.Footnote 4 In contrast, the flow of workers from employment to not in the labour force is likely to be dominated by quits and workers leaving jobs. Recall that \(n\) is defined as the proportion of workers not in work and no longer actively searching for work, i.e. \(n=h/(u+h)\). Accordingly, this can be approximated by the proportion of quits in total job separations. If quits are procyclical and lay-offs countercyclical, then \(n\) is procyclical. Davis et al. (2006) find this to the case for the USA. Specifically, the authors show (see p.21) that the lay-off–separation ratio is inversely related to net employment growth. The same appears to be the case for Australia as well. In the following, the ratio of job losers to all unemployed workers (i.e. job leavers and job losers) is plotted against net employment growth, \(\Delta \hbox { ln}({ EMP})\).Footnote 5

Procyclical behaviour of \(n\) is consistent with an added worker effect, i.e. workers enter the labour force in downturns and exit when the economy improves. Gong (2011) studies women’s labour market activities in Australia for the periods before and after their partners’ job loss and finds a significant added worker effect in terms of increased full-time employment and working hours. The added worker effect is also finds support with Brückner and Pappa (2012), who argue that the positive co-movement of the unemployment rate and labour force participation rate is driven by the influence of the wealth effect on labour market withdrawal. The added worker effect is attenuated if some workers, unable to find jobs, leave the labour force. The discouraged worker effect lowers labour force participation and places downward pressure on the unemployment rate (Figs. 2, 3).

Relationship between job losers–unemployed workers ratio and net employment growth. Note: for data source and definitions, see footnote 5

Relationship between job losers–(job losers \(+\) job leavers) ratio and net employment growth. Note: for data source and definitions, see footnote 5

To explicitly model these effects note that the added worker effect implies that \(n_2\) falls when \(s_1\) rises—type 2 workers enter the labour force when the labour market deteriorates for type 1 workers. The discouraged worker effect implies labour market withdrawal by type 1 workers, i.e. \(n_1\) falls when \(f^{U}\) falls. The next Proposition contains the results.

Proposition 2

Suppose \(n_{1f^{U}} <0\) and \(n_{2s_1 } <0\), then

-

(i)

(Discouraged workers) a fall in the job finding rate, \(f^{U}\), lowers the labour force participation rate, but has an indeterminate effect on the unemployment rate;

-

(ii)

(Added workers) an increase in the separation rate of type 1 workers, \(s_1\), raises the unemployment rate, but has an indeterminate effect on the labour force participation rate.

Proof

Part (i): \((e_1+u_1)^{2} \Delta _1^{2}{ UR}_{ 1f^{U}} =-e_1 [(1-n_1)^{2}s_1+(s_1 +f^{H})s_1 n_{1 f^{U}}]-u_1 [(1-n_1 )s_1+(f^{H}-f^{U})s_1 n_{1 f^{U}}]=-u_1 (1-n_1 )\Delta _1 -u_1 \Delta _1 f^{H}n_{1f^{U}}/(1-n_1 )\) is unsignable (nb., substituting \(e_1 =u_1 [n_1 f^{H}(1-n_1 )f^{U})]/(1-n_1 )s_1 )\); \(\Delta _1^{2}{\textit{LFPR}}_{1f^{U}} =-n_1 (1-n_1 )s_1 +s_1 n_{1f^{U}} (s_1+f^{U})<0\). Part (ii): noting that \(s_1\) affects \(e_2*,u_2*\hbox { and }h_2*\) through \(n_2\), the result follows directly from Proposition 1. \(\square \)

Part (i) shows that a lower job finding rate for unemployed workers, or more specifically \(f^{U}\) falling relative to \(f^{H}\), unambiguously lowers labour force participation. The precise effect on the overall unemployment rate is indeterminate because of the conflicting effects of lower job finding which raises UR and lower participation which lowers UR. Part (ii) indicates that UR definitely rises—type 1 workers lose their jobs and type 2 workers enter the labour force. The effect on the labour force participation rate reveals offsetting effects of some separated type 1 workers leaving the workforce and some type 2 workers entering the workforce.

Other factors affecting labour force participation and unemployment rates are also noteworthy. The first is the so-called shelter effect of education (Miller and Volker 1989), where faced with the prospect of prolonged unemployment, unemployed individuals enrol in further education. Moreover, other individuals may decide to defer entering the labour market by remaining at school when their job market prospects are poor (Dellas and Sakellaris 2003). Likewise, retirement decisions can be affected by the state of the business cycle. In Australia, the GFC resulted in many baby boomers and retirement age workers delaying retirement (O’Loughlin et al. 2010; Kendig et al. 2013). Also, there is the growing importance of various social insurance and expenditure programmes. In the USA, there has been a large increase in disability filings which is associated with exit from the labour market (Autor 2011). The effect has been prominent in Australia as well (Cai and Gregory 2003; Cai 2010). In Australia’s case, the effect of workers moving from being unemployed and actively searching to the disability support pension (DSP) programme, and no longer searching, places downward pressure on both the labour force participation rate and reduces the unemployment rate.

Another interpretation of the relationship between the added worker effect and labour force participation over the business cycle is provided by job search behaviour. Shimer (2004) constructs a model which shows that individuals with high job finding probabilities respond to adverse economic conditions by increasing their search intensity, i.e. \(n\) is procyclical. Workers who are less likely to find jobs become discouraged, reducing their search intensity and drop out of the labour force. Overall, search activity and labour force participation are likely to be countercyclical. Despite these considerations, the relation between the UR and LFPR is still considered to be ambiguous, which provides the opportune time to investigate their actual empirical relationship.

3 An MS-SVAR model of the labour market

3.1 Data

Most of the research in the area studies the USA, while this paper focuses on Australia. One reason why Australia has attracted attention since the GFC is that it has not experienced two consecutive quarters of negative real output growth (the official definition of a recession) since 1991. What also makes Australia relatively unique is the dramatic increase in its terms of trade since 2002, in large measure driven by China’s demand for resources. China’s impact on the price of energy and resources affected all economies. Most other developed countries experienced falling terms of trade. However, for a primary commodities exporter like Australia, the consequence has been historically high terms of trade. Average prices received by Australian non-rural commodity exporters increased by more than 60 % in the 2 years before the onset of the GFC. Associated with this were large increases in real income and reductions in unemployment, albeit with concerns about ‘Dutch disease’ and the ‘resources curse’ (Gaston and Rajaguru 2013).

Another feature of the paper is the use of monthly data. Cross-country panel studies of unemployment generally use annual or quarterly data. Not only are monthly data required for more timely assessments of the current state of the labour market, they are more informative for capturing the dynamics of labour market adjustment. (In principle, quarterly data could conceal up to 4 months of rising unemployment.) We use seasonally adjusted data for Australia from the Australian Bureau of Statistics (ABS) for the period 1978 to 2012 for estimation.Footnote 6

Employment is defined by the ABS as everyone who works for at least 1 hour or more for pay or profit is considered to be employed. This definition of ’one hour or more’—which is an international standard—means that ABS’ employment data can be compared with the rest of the world. Obviously, any hours of work cut-off point and the issue of underemployment are contentious. Commentators often refer to the rise in employment as the number of new jobs created each month. The ABS does not measure the number of jobs. Hence, if an employed person in the Labour Force Survey gains a second part-time job at the same time as their main job, this would have no impact on the employment estimate—the ABS’ Labour Force Survey does not count jobs, it counts people. This paper uses the natural logarithm of employment, ln(EMP). The unemployment rate, UR, is the percentage of people in the labour force who are unemployed. The size of the labour force is a measure of the total number of people who are willing and able to work. It includes everyone who is working or actively looking for work. The percentage of the total population who are in the labour force—either employed or unemployed—is known as the labour force participation rate, LFPR.

Over the 34-year sample period used in this paper, the average unemployment rate is 7.1 % with a standard deviation of 1.8 %. The maximum (minimum) unemployment rate was 11.2 (4.0) % in December 1992 (February 2008). The descriptive statistics are given in Table 1. The next section briefly discusses the empirical model used to classify the labour market outcomes into different regimes and presents the results. Section 4 concludes.

3.2 Unit root tests

The unemployment rate, UR, the labour force participation rate, LFPR, and the natural logarithm of employment, ln(EMP), can be modelled in either levels or differences depending on the unit root property of each series. As is well known, in the presence of structural breaks, standard unit root tests can be misleading as a stationary process can be misinterpreted as being non-stationary. In addition, unit root tests that do allow for structural breaks assume that the breaks are deterministic and exogenous. In this study, we use the unit root test proposed by Hall et al. (1999) and treat the breaks as being endogenous.

To proceed, we estimate the following ADF test regression where the constant term is allowed to switch between unobservable states, \(s\), i.e.

where \(\nu _t \sim iid\left( {0,\sigma _{s_t}^2}\right) \) and \(y\) represents one of the variables of interest, i.e. UR, LFPR, ln(EMP).Footnote 7 The state variable is assumed to evolve according to an \(m\)-state Markov chain whose transition probabilities are \(p_{ij}=Pr\left( {s_t =j|s_{t-1} =i} \right) \).

The unit root test with the null of \(\rho =0\), against the alternative that \(\rho <0\), is based on the \(t\)-statistic, \(t_{\rho }\). According to Hall et al. (1999), the computed \(t\)-statistic is compared against the empirical critical value by simulating the model under the null. To proceed, we first obtain the maximum likelihood parameter estimates of the model in Eq. (4) and the residuals of the estimated model. Then, we generate 10,000 sets of disturbances with sample sizes equal to that of the data-generating process by bootstrapping the residuals for each regime. (We generate the data from \(N\left( {0,\sigma _{s_t}^2}\right) \), instead of bootstrapping from the original residuals and find that the results are the same for each of the three variables.) Thirdly, we determine the dates for the state variable based on the estimated transition probabilities in Eq. (4). Fourthly, we construct the artificial data for \(y\) based on the simulated residuals and state variables under the null of non-stationarity. Finally, we estimate the \(t\)-statistic \((t_{\rho })\) for the 10,000 replications to establish the critical values.

The optimal lag length, the number of regimes, \(t_{\rho }\) and the corresponding critical values for each variable are reported in Table 2. The optimal lag length and the number of regimes for each model are established by the Akaike information criterion (AIC), Hannan–Quinn information criterion (HQC) and Schwarz criterion (SC).Footnote 8 The results reveal that both the unemployment rate and labour force participation rate are stationary in levels, while ln(EMP) is non-stationary. In the following, we model UR and LFPR in levels and ln(EMP) in first differences (denoted by \(\Delta \hbox { ln}({ EMP})\)); this ensures that the residuals from the system of equations are stationary.

3.3 The MS-SVAR model

In this subsection, we discuss the Markov-switching structural vector autoregressive model (MS-SVAR). The means of the labour market variables as well as the variances and covariances of the residuals are assumed to be unknown for a number of distinct regimes. That is, we use the statistical properties of the data to provide the identifying information about the actual reactions of our set of labour market variables to unexpected exogenous innovations (Hamilton 1989; Krolzig 1997; Lanne et al. 2010).

Let \(s_{t}\) be a discrete latent variable that identifies which regime the labour market is in at time \(t\). Although the regime in which the labour market is in at time \(t\) is unidentified, we can identify the conditional probability that the labour market is in any regime. For example, if there are just two regimes, then \(s_{t}=1 (s_{t} = 2)\) may be the low-volatility (high-volatility) regime. Alternatively, the latent variable may simply represent periods of labour market tightness or slack. The regimes are characterised by different conditional distributions of each labour market variable. We estimate the following model.

This can be written more compactly as

where \(X_t =\left[ \begin{array}{ccc} { UR}_t&{ LFPR}_t&\Delta \hbox {ln}({ EMP})_t\end{array}\right] ^{\prime }\), \(\mu (s_t )^{\prime }=\left[ \begin{array}{ccc}\varvec{\mu }_1 (s_t )&\mu _2 (s_t )&\mu _3 (s_t )\end{array}\right] \) is the regime-specific mean, \(A=\left[ \begin{array}{ccc} 1&{} 0&{} -\phi _{13}^0\\ 0&{} 1&{} -\phi _{23}^0\\ 0&{} 0&{} 1\\ \end{array}\right] \), \(\varepsilon _t \sim N(0, \Sigma _{s_t})\) is the regime-specific residual for period \(t\) and the coefficient matrix for lag \(i\) is denoted by \(\varPhi _i\). \(\varphi _{jk}^i\) denotes the \(j\)th row and \(k\)th column of the coefficient matrix \(\varPhi _i\). The model allows each regime to have a different mean and covariance matrix. The regime-specific covariances are denoted by \(\Sigma _{s_t}\). The idea behind regime shifting is that the parameters of an SVAR process, the intercept and covariances depend upon an unobserved regime variable, \(s_{t}\). In our model, the intercept and the covariances depend on the state of the Markov chain.Footnote 9 The advantage of this model is its flexibility in modelling times series subject to regime shifts (Clements and Krolzig 1998).

The structure is a standard SVAR except that changes in total employment, \(\Delta \hbox { ln}({ EMP})\), simultaneously affect UR and LFPR. As noted, in connection with the results of estimating Eq. (4), UR and LFPR are modelled as stationary variables. Further adjustments to unemployment, employment and participation take place in subsequent periods. As Nickell et al. (2003, p. 396) note, “unemployment in both the short and long run is determined by real demand”. The inclusion of the contemporaneous shock to employment is consistent with a demand-side interpretation, an approach based on a dynamic model of the labour market developed by Blanchard and Katz (1992). Figure 7 plots the data for quarterly real GDP and monthly employment. It helps convey two ideas. First, that quarterly data may ignore important higher frequency information and, secondly, that the percentage changes in employment closely mirror the growth in real GDP.

The estimation procedure proposed by Lanne et al. (2010) is used to estimate the parameters of the model. Under the assumption of conditional normality, \(\varepsilon _t \sim N\left( {0, \Sigma _{s_t}}\right) \), maximum likelihood (ML) estimation is used to estimate the structural parameters of the model simultaneously. If conditional normality fails, then it produces pseudo-ML estimates. As we shall see below, normality is not a concern for our model.

In order to determine the optimal number of regimes, we use the AIC, HQC and SC as discussed in Psaradakis and Spagnolo (2003), Psaradakis and Spagnolo (2006), Herwartz and Lütkepohl (2011) and Lütkepohl and Netšunajev (2014). The results are reported in Table 6 of Appendix.Footnote 10 In all cases, we find that the optimal number of regimes is three.

The state variable is assumed to follow an ergodic first-order Markov process and is characterised by the matrix \(\Pi \), the elements of which are the transition probabilities from state \(j\) to state \(k\), \(p_{jk}\). That is,

Once the coefficients of the model and the transition matrix have been estimated, the probability \(\Pr (s_t =j|X_1, X_2, \ldots , X_T)\) of being in state \(j\), based on the knowledge of the computed series, can be computed for each date.Footnote 11 The series of probabilities are referred to as the smoothed probabilities of being in state \(j\) based on the information up to date \(t\). The filtered probabilities are also calculated. When \(t =T\), the smoothed probability is equal to the filtered probability.

The autoregressive order \(p\) is determined by the AIC, HQC and SC to ensure that the residuals are white noise. Both AIC and HQC suggest an optimal lag length of 6, while the SC suggests a lag length of 5. However, the residual diagnostics for white noise error (i.e. the correlogram) suggest that the autocorrelations at lag 12 are statistically different from zero for all three equations. Hence, we include lag 12 to account for this. Moreover, we omit lags 7 through and 11 for two reasons: parsimony and the fact that the parameters are not jointly statistically different from zero at a 5 % level of significance. The residual diagnostics for the best-fit model with the inclusion of lag 12 are reported in Table 3 below. Portmanteau tests for residual autocorrelation and the relevant \(p\) values suggest that the residuals from each equation are not autocorrelated. The errors from each equation are normally distributed at a 5 % level of significance.

4 Findings

The results from estimating Eq. (5) are in Tables 3 and 4. Using the testing procedure discussed in the previous section, we determine that there are three labour market regimes.Footnote 12 For UR note that regime 1 is the high-mean, high-variance regime; regime 2 is the moderate-mean, moderate-variance regime; and regime 3 is the low-mean, low-variance regime. It is noteworthy that this regime classification is statistically determined and that no restrictions are placed on the means and covariance matrices across regimes. For LFPR, regime 1 is the low-mean, high-variance regime; regime 2 is the moderate-mean, moderate-variance regime; and regime 3 is the high-mean, low-variance regime. Without further loss of generality, we refer to regime 3 as the strong labour market or good regime as it is characterised by (relatively) low unemployment and high participation as well as low volatility in both UR and LFPR. Likewise, regime 2 is referred to as the moderate regime and regime 1 as the severe recessionary or bad regime.Footnote 13

The variance–covariance matrices of the residuals for all three regimes are reported in Table 9 of Appendix. We find that the residuals from the UR and LFPR equations positively covary and are statistically significant for all regimes. These residual covariances explain the contemporaneous correlation between these two variables after controlling for all the lagged effects. On the other hand, the residuals from the \(\Delta \hbox {ln}({ EMP})\) equation are uncorrelated with the UR and LFPR equations at a 5 % level of significance.

For both UR and LFPR, there are large differences in the AR terms. For the LFPR equation, a higher unemployment rate in the previous two periods lowers labour force participation. This suggests that the effect of higher unemployment discourages worker participation. Additionally, this is consistent with the stylised fact that outflow rates from unemployment are procyclical (see Elsby et al. 2009, e.g.). The cross-effects in the UR equation are somewhat more complicated. When labour force participation rises, unemployment initially falls. This may occur due to increased job hiring rapidly pulling the most employable workers into jobs, many of whom are initially not in the labour force. However, as the effects of an initial rise in hiring dissipate, the larger number of workers attracted to the labour force leads to offsetting increases in the unemployment rate, i.e. due to the expansion of the pool of unemployed (see footnote 16 below).Footnote 14 As noted by Yashiv (2007, p. 84), the flow between being employed and being not in the labour force is the least understood and “murky” of all the potential flows in a three-state dynamic labour market model. In our case, these flows are more explicable when we look at the cumulative effects of impulse responses below.

Immediately apparent from Table 3 is the great deal of persistence of remaining in regimes 2 or 3. The probability of staying in a good regime is 98 %, and the duration of enjoying these good conditions is about 50 months. Similarly, the probability of staying in the moderate regime is 87.7 % and the duration of being in this regime is about 8 months. On the other hand, the duration of the labour market being in a bad regime—with high unemployment and low labour force participation—is about 2.4 months.Footnote 15 In the case of Australia, severe labour market downturns have been short and sharp.

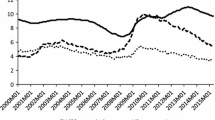

Table 4 shows that the labour market is in a bad regime about 5 % of the time. In terms of precise dates, the Australian labour market’s ‘golden’ period from the end of 1998 to December 2008 was more than 10 years long. In particular, the resources boom and rising terms of trade led to sustained and significant reductions in trend unemployment (Gaston and Rajaguru 2013). The recessions in the early 1980s and early 1990s were the worst times for Australia’s labour market. One curiosum is that 5 months in 1988 are also classified as being in the bad labour market regime. A possible explanation is that in 1988, and as part of a programme of ongoing and wide-ranging microeconomic reforms, the Australian government introduced the first of a series of phased reductions in tariffs across most industry sectors. In addition, there was a share market collapse at the end of 1987 which in all likelihood, and after some lag, contributed to adverse labour market conditions. On the other hand, note that the smoothed probability in the last column is quite small. Accordingly, Fig. 4 makes clear that this period is ‘close’ to being classified as belonging to regime 2.

State probabilities for three-state MS-SVAR (6) model for UR, LFPR and \(\Delta \hbox {ln}({ EMP})\). Note: the shaded bars represent official recessions for Australia (i.e. two quarters or more of negative real output growth)

The previous example highlights that an advantage of our modelling approach is that it can identify periods of severe labour market weakness, even when the data for output growth may indicate otherwise. This is borne out by the post-2008 data in Fig. 7. A further example is that, in the direct aftermath of the GFC, Australia did not experience two consecutive quarters of negative economic growth. In fact, unemployment was low and labour force participation high by (post-WWII) historical standards. However, the first months of 2009 are identified as belonging to regime 1. That is, even though the unemployment rate was low by historical standards, the labour market during those months is characterised as belonging to the bad regime. The severity of the GFC was important in this regard.Footnote 16

In terms of regime classification, Fig. 4 is very informative. With respect to duration, poor labour conditions are relatively infrequent and of short duration for Australia. The effects of the GFC have been quite muted, for example. We can also readily see that Australia’s recent labour market history can be broadly characterised by two distinct phases. The 1980s and the period up to 1998 are largely spent in regime 2—with moderate to high unemployment and moderate to low participation. With the exception of the GFC-influenced 3 months, the period from late 1998 to the present is in regime 3, with low unemployment and comparatively high labour force participation. These results highlight the different labour market dynamics in Australia compared to most other developed economies. For example, since the onset of the GFC in the USA, the spotlight has understandably been on the persistence of high levels of unemployment and the continuation of the secular decline in labour force participation (see e.g. Elsby et al. 2010).

A summary of the estimated coefficients is presented in Table 5. In this table, the figures quoted are for the sum of the lagged and contemporaneous coefficients. We also used the Granger causality test proposed by Billio and Di Sanzo (2006) for Markov-switching models in order to establish the causal link between UR, LFPR and \(\Delta \hbox {ln}({ EMP})\). The parenthesised figures in Table 5 are the \(p\) values for the Wald test to examine the Granger causality between the variables. In the model, each of the three variables is significant in explaining the cumulative effect on UR and LFPR.

Impulse Responses: We follow the procedure proposed by Kilian and Park (2009) to derive the impulse responses by imposing a structural restriction in Eq. (5). Let \(e_t\) denote the reduced form VAR innovations such that \(e_t =A^{-1}\varepsilon _t\). The structural innovations are obtained from the reduced form innovations by imposing exclusion restrictions on \(A^{-1}\). We use the following identifying restrictions to derive the impulse response functions:

The reduced form innovations show that (i) the response of UR depends on the shocks from the unemployment rate and the change in employment, and (ii) the response of LFPR depends on the shocks originating from the participation rate and the change in employment.

Since each component of the reduced form innovations, \(e_t\), is not orthogonal, we derive the impulse response functions based on the orthogonal component of the structural innovations, \(\varepsilon _t\). That is, we rearrange Eq. (5) as

The impulse responses are obtained from the transformation matrix \(( {I-A^{-1}\sum \nolimits _{i=1_i}^p \Phi _i L^{i}} )^{-1}A^{-1}\), i.e. by transforming the VAR processes into vector moving average (VMA) processes of infinite order, so that UR, LFPR and \(\Delta \hbox {ln}({ EMP})\) are expressed in terms of the current and past values of the three shocks (i.e. \(\varepsilon _{ UR}, \varepsilon _{ LFPR}, \varepsilon _{\Delta \ln ({ EMP})}\)). Equation (8) can be expressed as \(X_t =A^{-1}\varvec{\upmu } (s_t )+\left( {\Psi _0 +\Psi _1 L+\cdots } \right) \varepsilon _t\), where \(\Psi _k\) denotes the impulse responses at lag k.

The response of UR to a participation shock and that of LFPR to an unemployment shock is in line with our discussion of Table 3 results above. While the relationship between the three variables, as reflected by the sign patterns, is informative, of most interest is the response of the unemployment rate and labour force participation rate to an innovation in employment demand. The cumulative effect of a positive demand innovation is to lower both the unemployment rate and the labour force participation rate. The effect on UR is unsurprising, while the effect on LFPR suggests the relative importance of the added worker effect. The positive co-movement of the unemployment rate and the labour force participation rate also appears in the cross-country study by Brückner and Pappa (2012), which they argue is explained by the wealth effect and imperfect labour market matching. Moreover, Fujita and Ramey (2009) show that if variation in the rate of job separations is strongly countercyclical, UR and LFPR both fall when employment rises.Footnote 17 The stylised model in Sect. 2 provides some rationale and further corroboration for this observed relationship.

Impulse responses for all three regimes are presented in Fig. 5.Footnote 18 The effect of a positive employment shock is to marginally lower both UR and LFPR. A one standard deviation negative shock to participation raises the unemployment rate. As discussed, this effect is expected since a fall in labour force participation reduces the denominator of the unemployment rate.

Impulse response functions. Response to one SD innovations \(\pm \) two SE Note: the confidence intervals are constructed using bootstrapping

The results seem small compared to the effects displayed in Table 5. However, recall that the tabulated results give the cumulative effects of an innovation to labour demand taking into account the entire lag structure of the estimated model. Figure 6 displays the cumulative impulse responses, with results readily comparable and consistent with the results in Table 5. Once again, UR and LFPR both fall in response to stronger employment demand.

Cumulative impulse response functions

5 Concluding comments

This paper investigated a feature of recessions and financial crises, by examining whether the labour market becomes mired in conditions characterised by high unemployment rates and lower labour force participation. We provided a statistically based analysis of this question by estimating a Markov-switching model of unemployment and labour force participation. The model treats the labour market as transitioning through different labour market phases or regimes. Specifically, major economic shocks, such as the GFC, are identified as episodes of identifiable duration which differ from other “normal” time periods. The regime switching occurs due to the idiosyncratic set of domestic labour market institutions as well as external economic shocks. This behaviour is captured by using transition probabilities which determine the frequency and duration of time spent in regimes with different mean and variance characteristics.

While research on unemployment (and to a lesser extent, labour force participation) understandably tends to focus on the role of specific determinants, research that uses high-frequency data for these variables and which has the ability to forecast the duration and severity of recessions and economic shocks on the labour market is also valuable and insightful. For Australia, we found little evidence to suggest that the labour market gets stuck in a bad regime. Poor labour market regimes may have been severe, but they have been of short duration in Australia, just 2.4 months on average. We also found that the 10 years between the end of 1998 and the end of 2008 were particularly good years for the labour market. Specifically, this ‘golden’ period had low unemployment and high labour force participation. As argued elsewhere, this is likely to have been attributable to the effects of ongoing labour market reforms and, more importantly, the effects of the China-fuelled resources boom (Gaston and Rajaguru 2013).

We were also able to shed light on the relationship between unemployment and labour force participation. The flow between the unemployed state and the not in the labour force state may be the least understood of all the potential flows in the three-state dynamic labour market model. Our results showed that the instantaneous effect of an increase in labour demand is quite small and reduces the unemployment rate and increases labour force participation. However, we were also able to confirm the results of previous research showing that the cumulative or long-term effect of an upswing in labour hiring results in a lower unemployment rate and a lower labour force participation rate.

Notes

Claessens et al. (2009) identify the quarter in which OECD countries entered recession. The USA, along with Ireland and Iceland, entered recession in the first quarter of 2008. Australia had just one quarter of negative output growth (the fourth quarter of 2008).

The job finding probability is closely (and positively) related to matching market tightness (Shimer 2005).

Monthly labour market gross flows data (for the period October 1997 to April 2013) reveal that the average values for \(f^{U}\) and \(f^{H}\) are 0.215 and 0.045, respectively. The fact that the two job finding rates for the USA are so different forms the basis for Flinn and Heckman’s (1983) observation that being unemployed and not in the labour force are behaviourally distinct labour market states. See also Hall (2006), who attributes the procyclicality of the job finding rate in large measure to the behaviour of those out of the labour force finding employment.

The ratio of job losers to job leavers among the ranks of the unemployed from the second quarter of 2001 to the second quarter of 2013 averages about 1.55. See the following footnote for the data source and definitions.

The data are from the SuperTable files (UQ1) in Labour Force, Australia, Detailed, Quarterly (ABS cat. 6291.0.55.003) and for the second quarter of 2001 to the second quarter of 2013. Job losers are unemployed people who have worked for 2 weeks or more in the past 2 years and left that job involuntarily: that is, they were laid off or retrenched from that job; left that job because of their own ill-health or injury; the job was seasonal or temporary; or their last job was running their own business and the business closed down because of financial difficulties. Job leavers are unemployed people who have worked for 2 weeks or more in the past 2 years and left that job voluntarily—that is, because (for example) of unsatisfactory work arrangements/pay/hours; the job was a holiday job or they left the job to return to studies; or their last job was running their own business, and they closed down or sold that business for reasons other than financial difficulties. As in Davis et al. (2006), a quadratic polynomial is fitted to the data in both figures.

The use of seasonally adjusted data is standard in this literature (see, e.g. Schwartz 2012). The data used are for the period February 1978 to October 2012 and available from the Australian Bureau of Statistics at: http://www.abs.gov.au/AUSSTATS/abs@.nsf/DetailsPage/6202.0Jul%202012?OpenDocument.

We also considered other specifications that allow the autoregressive parameters to switch between regimes. However, these parameters were not significantly different from each other across the regimes for each of the variables. This subsequently reduced the univariate models to only switching between the regimes defined by differences in the intercept and variance of the residuals. Justification for a changing intercept for each regime is provided by Bianchi and Zoega (1998). For 17 OECD countries, they find shifts in the mean of the unemployment rate after large shocks and that the effects persist (measured as the sum of coefficients in the autoregressive process). Small shocks have no such effects. They argue that their findings are consistent with hysteresis models of unemployment.

See Psaradakis and Spagnolo (2003), Psaradakis and Spagnolo (2006), Herwartz and Lütkepohl (2011) and Lütkepohl and Netšunajev (2014) for the selection of the number of regimes. The tests for the number of regimes for each of the variables are not reported for the sake of brevity. We find that all three criteria suggest that the optimal number of regimes for all variables is three. We discuss this procedure in more depth in the next section, where we report the results for the multivariate model.

As for the univariate models, we also considered other specifications to allow the autoregressive parameters to switch between regimes. However, these autoregressive parameters were not significantly different from each other across the regimes in each equation. Thus, the models only switch between the regimes as defined by differences in the intercept and the variance–covariance matrices of the residuals.

For all the SVAR models (two regimes, three regimes and four regimes), the AR parameters are not statistically different from each other across regimes. The only difference observed is through the switching in intercept and covariances of the residuals across the equations. We report the results for the model with three regimes (which is statistically optimal) for the sake of brevity. We have also estimated each equations of the system independently to establish the number of regimes for each equation and find that the optimal number of regimes to be three. The results are not reported for the sake of brevity.

For details of the algorithm, see Krolzig (1997).

The equality of regime means is tested for each equation separately. The results are reported in Table 7 of Appendix. The results show that intercepts for the regimes are different from each other at a 5 % level of significance for all three equations. The equality of means is also examined pairwise and further confirms that there are at least three regimes for our analysis. In addition, the equality of regime variances was also tested for each equation separately to make sure that the covariance matrices are different between the regimes. The results are reported in Table 8 of Appendix. The results show that the variances for the regimes are different from each other at a 5 % level of significance for all three equations. Similar testing conducted on a model with four regimes found that the intercept and variances for the fourth regime are not statistically different from the third regime at a 5 % level of significance for all three equations, confirming that three regimes are the optimal number for our analysis.

As we shall see below, the moderate regime could also be classified as a moderate to mild recessionary regime.

The results from estimating a two equation model with UR and LFPR reveal that the same relationship exists between those variables. These results are available in a separate “Appendix” available from the authors.

The expected length of remaining in a particular regime is calculated as \(1/(1 - p_\mathrm{ii})\).

Job losses are countercyclical, and job finding rates are procyclical, i.e. when economic activity contracts and employment falls, job losses increase and job finding decreases. From the perspective of gross flows, the pool of the unemployed shrinks. Fujita and Ramey (2009) show that this “pool size effect” outweighs the effect of increases in the job finding rate. This effect is further reinforced because while the job loss rate reacts almost simultaneously with respect to movements in the cycle, the impact of the job finding rate and gross hiring reacts with some lag. This is a possible explanation for the ‘jobless recoveries’ phenomenon. Similarly, Shimer (2013) shows that the share of inactive workers rises during recessions as some of the large pool of unemployed workers drop out of the labour force. The underlying developments are subject to debate in the USA and Australia. In Australia’s case, Dixon et al. (2005) argue that increases in unemployment are driven by job separations (with greater flows from employment to both unemployment and not in the labour force), while Ponomareva and Sheen (2010) argue that increases in the unemployment rate are driven by lower job finding rates and diminished flows from unemployment to employment.

See Krolzig (1997) for a detailed discussion of impulse response functions for MS-VAR models with regime-invariant VAR matrices. Since the final model switches between the three regimes for the intercept and variances of the residuals, the impulse responses are similar across the three regimes.

References

Autor DH (2011) The unsustainable rise of the disability rolls in the United States: causes, consequences, and policy options. Working paper no. 17697, National Bureau of Economic Research

Bianchi M, Zoega G (1998) Unemployment persistence: Does the size of the shock matter? J Appl Econom 13(3):283–304

Billio M, Di Sanzo S (2006) Granger-causality in Markov switching models. Department of Economics Research Paper Series 20WP, University Ca’Foscari of Venice

Blanchard OJ, Katz LF (1992) Regional evolutions. Brook Pap Econ Act 1:1–75

Brückner M, Pappa E (2012) Fiscal expansions, unemployment and labor force participation: theory and evidence. Int Econ Rev 53(4):1205–1228

Burns AF, Mitchell WC (1946) Measuring business cycles. National Bureau of Economic Research, New York

Cai L (2010) The relationship between health and labour force participation: evidence from a panel data simultaneous equation model. Labour Econ 17(1):77–90

Cai L, Gregory RG (2003) Inflows, outflows and the growth of the disability support pension (DSP) program. Aust Soc Policy 2002(03):121–143

Claessens S, Kose MA, Terrones ME (2009) What happens during recessions, crunches and busts? Econ Policy 24(60):653–700

Clements MP, Krolzig H-M (1998) A comparison of the forecast performance of Markov-switching and threshold autoregressive models of US GNP. Econom J 1:C47–C75

Davis SJ, Faberman RJ, Haltiwanger J (2006) The flow approach to labor markets: new data sources and micro-macro links. J Econ Perspect 20(3):3–26

Debelle G, Vickery J (1999) Labour market adjustment: evidence on interstate labour mobility. Aust Econ Rev 32(3):249–263

Dellas H, Sakellaris P (2003) On the cyclicality of schooling: theory and evidence. Oxf Econ Pap 55(1):148–172

Dixon R, Freebairn J, Lim GC (2005) An examination of net flows in the Australian labour market. Aust J Lab Econ 8(1):25–42

Elsby MWL, Hobijn B, Şahin A (2010) The labor market in the Great Recession. Brook Pap Econ Act Spring, 1–48

Elsby MWL, Michaels R, Solon G (2009) The ins and outs of cyclical unemployment. Am Econ J Macroecon 1(1):84–110

Fujita S, Ramey G (2009) The cyclicality of separation and job finding rates. Int Econ Rev 50(2):415–430

Furceri D, Mourougane A (2009) Financial crises: past lessons and policy implications. OECD Economics Department working paper no. 668

Gaston N, Rajaguru G (2013) How an export boom affects unemployment. Econ Model 30(1):343–355

Gong X (2011) The added worker effect for married women in Australia. Econ Rec 87(278):414–426

Hall RE (2006) Job loss, job finding and unemployment in the U.S. economy over the past 50 years. NBER Macroecon Annu 2005 20:57–101

Hall SG, Psaradakis Z, Sola M (1999) Detecting periodically collapsing bubbles: a Markov-switching unit root test. J Appl Econom 14(2):143–154

Hamilton JD (1989) A new approach to the economic analysis of nonstationary time series and the business cycle. Econometrica 57(2):357–384

Hamilton JD (2005) What’s real about the business cycle? Federal Reserve Bank of St. Louis Review, July/August, pp 435–452

Herwartz H, Lütkepohl H (2011) Structural vector autoregressions with Markov switching: combining conventional with statistical identification of shocks. Economics Working Papers ECO2011/11, European University Institute

Kendig H, Wells Y, O’Loughlin K, Heese K (2013) Australian baby boomers face retirement during the global financial crisis. J Aging Soc Policy 25(3):264–280

Kilian L, Park C (2009) The impact of oil price shocks on the U.S. stock market. Int Econ Rev 50(4):1267–1287

Krolzig H-M (1997) Markov-switching vector autoregressions: modelling, statistical inference, and application to business cycle analysis. Lecture notes in economics and mathematical systems, issue 454. Springer, Berlin

Lanne M, Lütkepohl H, Maciejowska K (2010) Structural vector autoregressions with Markov switching. J Econ Dyn Control 34(2):121–131

Lazear EP, Spletzer JR (2012) The United States labor market: Status quo or a new normal? Working paper no. 18386, National Bureau of Economic Research

Lundberg S (1985) The added worker effect. J Labor Econ 3(1):11–37

Lütkepohl H, Netšunajev A (2014) Disentangling demand and supply shocks in the crude oil market: how to check sign restrictions in structural VARs. J Appl Econom 29:479–496

Miller P, Volker P (1989) Socioeconomic influences on educational attainment: evidence and implications for the tertiary education finance debate. Aust J Stat 31(1):47–70

Netsunajev A (2013) Reaction to technology shocks in Markov-switching structural VARs: identification via heteroskedasticity. J Macroecon 36:51–62

Nickell S, Nunziata L, Ochel W, Quintini G (2003) The Beveridge curve, unemployment and wages in the OECD from the 1960s to the 1990s. In: Aghion P, Frydman R, Stiglitz J, Woodford M (eds) Knowledge, information, and expectations in modern macroeconomics: in honour of Edmund S. Phelps. Princeton University Press, Princeton, pp 394–431

O’Loughlin K, Humpel N, Kendig H (2010) Impact of the global financial crisis on employed Australian baby boomers: a national survey. Aust J Ageing 29(2):88–91

Ponomareva N, Sheen J (2010) Cyclical flows in Australian labour markets. Econ Rec 86(Special Issue):35–48

Psaradakis Z, Spagnolo N (2003) On the determination of the number of regimes in Markov-switching autoregressive models. J Time Ser Anal 24(2):237–252

Psaradakis Z, Spagnolo N (2006) Joint determination of the state dimension and autoregressive order for models with Markov regime switching. J Time Ser Anal 27(5):753–766

Reinhart CM, Rogoff KS (2009) The aftermath of financial crises. Am Econ Rev 99(2):466–472

Schwartz J (2012) Labor market dynamics over the business cycle: evidence from Markov switching models. Empir Econ 43(1):271–289

Shimer R (2004) Search intensity. Unpublished manuscript, University of Chicago

Shimer R (2005) The cyclical behavior of equilibrium unemployment and vacancies. Am Econ Rev 95(1):25–49

Shimer R (2012) Reassessing the ins and outs of unemployment. Rev Econ Dyn 15(2):127–148

Shimer R (2013) Job search, labor force participation, and wage rigidities. In: Acemoglu D, Arellano M, Dekel E (eds) Advances in economics and econometrics: Tenth World Congress, Vol 2, Econometric Society Monographs (Book 50). Cambridge University Press, Cambridge, pp 197–234

Wasmer E (2009) Links between labor supply and unemployment: theory and empirics. J Popul Econ 22(3):773–802

Yashiv E (2007) US labor market dynamics revisited. Scand J Econ 109(4):779–806

Author information

Authors and Affiliations

Corresponding author

Additional information

Noel Gaston and Gulasekaran Rajaguru: The comments of Felix Chan, Phillip Chindamo and two anonymous referees are gratefully acknowledged. The authors are also grateful to Lance Fisher and Jan-Egbert Sturm for feedback on an earlier version of the paper. As customary, the authors bear the responsibility for all errors and omissions.

Appendix

Appendix

See Tables 6, 7, 8, 9 and Fig. 7.

Plot of quarterly real GDP growth against monthly employment growth. Note: The shaded bars represent official recessions for Australia (i.e. two quarters or more of negative real output growth)

Rights and permissions

About this article

Cite this article

Gaston, N., Rajaguru, G. A Markov-switching structural vector autoregressive model of boom and bust in the Australian labour market. Empir Econ 49, 1271–1299 (2015). https://doi.org/10.1007/s00181-015-0920-4

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00181-015-0920-4