Abstract

The significance of wood and paper products originating from certified sustainable sources has been increasing worldwide during the last two decades paralleling overall interest and concern for global sustainability issues. Forest certification is a voluntary verification tool that has been gaining importance not only as an independent verification tool in the wood processing industry but also as an influencer in private and public purchasing policies and as a component of emerging wood harvesting and trade legality schemes. There are two main types of certification, forest certification for forest management and chain-of-custody (CoC) certification which tracks certified wood through the manufacturing supply chain. This study focuses on the chain-of-custody component. A multinational survey of CoC certificate holders in Slovakia, Czech Republic, Poland, Slovenia, Croatia and Serbia was conducted to identify the general understanding of certification concepts as environmental, economic and social tools, to determine incentives for CoC certification implementation by companies, and to identify difficulties in existing certified wood product supply chains. Results indicate that respondents demonstrated a high level of understanding of the chain of custody certification concept. Respondents also link forest certification mainly to the issues of legality, tracing the origin source of supply and prevention from illegal logging. The main expected benefits are linked to the improvement of external company image followed by business performance factors such as penetrating new markets, increase of sales volume, expanded market share and the increase of profit margin. The key problems connected to certified supply chains relate to the overpricing of certified material inputs, while respondents reported none or minimum price premiums for their certified products over non-certified alternatives.

Similar content being viewed by others

Explore related subjects

Discover the latest articles, news and stories from top researchers in related subjects.Avoid common mistakes on your manuscript.

1 Introduction

The foundation of sustainable forest management is based on the concept of sustainable development and is premised on three integrated and equally important pillars: environmental soundness, social justice, and economic viability. The concept of sustainable development and the interrelationship of its three pillars were originally popularized in the Brundtland (1987) report, yet it was at the Rio Earth Summit in 1992 where the idea finally took hold. Non-legally binding Forest Principles (UNECED 1992) resulted in the birth of forest certification. Thus, forest certification was initially introduced as a voluntary mechanism by environmental groups to ameliorate the consequences of tropical deforestation and forest degradation (Rametsteiner and Simula 2003). This type of certification, based on third-party auditing of compliance with established standards, was quickly accepted as a means to promote sustainable forest management (Durst et al. 2006; Siry et al. 2005; Perera et al. 2007) and directly influenced forest management practices (Auld et al. 2008; Lewis and Davis 2015; Mac Dicken et al. 2015; Moore et al. 2012).

Forest certification is a process by which forest owners voluntarily submit their forests to inspection by an independent certification body to determine whether their management practices meet clearly defined standards, particularly those regarding sustainability (Peck 2001). Forest owners’ awareness of certification and decisions to participate in certification programmes can be positively influenced by receiving professional advice regarding their forestlands and having a written management or stewardship plan (Creamer et al. 2012). Cabarle et al. (1995) argue that the objective of certification is to link the informed consumer with products produced in an environmentally and socially responsible manner. Consumers often express their concerns about the ethical behaviour of companies by means of ethical buying and consumer behaviour (De Pelsmacker et al. 2005) and are increasingly demanding assurances that the production of goods conforms to standards of social and environmental responsibility (Fischer et al. 2005). Companies that can prove that they are environmentally responsible by being certified may benefit by differentiating their products, potentially increasing market share (Bigsby and Ozanne 2002) and gaining market advantage (Hayward and Vertinsky 1999).

Since their inception, forest certification schemes have evolved, improved and continually incorporated interrelated concepts and needs of society. Certification programs increasingly became an instrument of governmental procurement policies, obligatory requirements for awarding ecolabels, corporate policies of private companies, requirements for green building initiatives, and acceptance as a tool for proving the legality of timber origin.

For any certification system to be effective, it must be trusted by entities in the supply chain from the forest to consumers. Certification criteria, standards and prescriptions must be consistent with extant definitions of sustainable forest management and must include effective monitoring. Rewards (premiums) or advantages of market access must also offer sufficient incentives for suppliers to bear the costs of certification (van Kooten et al. 2005). Rickenbach and Overdevest (2006) state that the dominant model for understanding the effectiveness of certification views forest certification as a market-based incentive for forestry enterprises whereby firms that adopt certification practices expect direct market benefits. Other views, for example Ulybina and Fennell (2013) suggest certification is a signal to external stakeholders that enterprises are meeting high forestry standards or improving forestry practices and/or production. Takahashi (2001) described four potential motivational models to explain why firms participate in voluntary initiatives such as forest certification—market economic model, production economic model, social, and moral model. The market economic model assumes that firms are attracted by voluntary initiatives if they can generate economic benefits. The production economic model is premised on additional profits through improvements in efficiency. The social model states that companies expect social exchanges generated between firms and stakeholders, and the moral model suggests that firms participate in voluntary initiatives because of intrinsic ethical morality. Empirical results by Takahashi (2001) and Nakamura et al. (2001) revealed that the market economic and social models explained participation in forest certification.

In addition, perceived pressure from shareholders, firm size, financial health, past environmental performance, and regulatory threats have been linked to firms’ decisions to meet environmental standards voluntarily. For some certified companies the implementation of forest certification provides the satisfaction of supporting the sustainability of natural forest resources and society as a whole (WWF 2000). It may also serve to improve their corporate images and access to markets (Hansen and Punches 1999; Hubbard and Bowe 2004) or may be part of business system innovations (Gilani et al. 2016). Owari et al. (2006) found that for certified companies in Finland forest certification was considered important for indicating a company’s sense of responsibility, for keeping market share and for selling products in an existing market. Trishkin et al. (2014) explored attitudes and motivations associated with forest certification among forest industry companies in north-western Russia. Market demand was identified as a main driving force influencing development of forest certification; wood legality, company’s image and competitiveness of wood products were recognized as the most important benefits associated with forest certification. In spite of general positive attitudes toward forest certification, the study identified gaps in understanding certification principles leading to limited awareness, especially for non-certified forest industry respondents.

2 Chain-of-custody certification

There have been many studies conducted regarding chain of custody certification (CoC) and its perception by forest products companies. As stated by Potkański et al. (2011), CoC becomes one of the factors in determining leadership position in the forest and wood-based sector, especially under economic crisis conditions. Empirical research carried out by Tuppura et al. (2016), among the world’s leading forestry companies, found out that incentives for adopting forest certification are more often external rather than internal, and more market driven than regulation driven. Immature markets, the indirect nature of most benefits, and certification being an unfamiliar concept are commonly cited reasons for a lack of manufacturer support or involvement (Jayasinghe et al. 2007).

In the early stages of certification, Vlosky and Ozanne (1998) examined the attitudes of U.S. wood manufacturers with regard to wood products certification focussing on willingness-to-pay a price premium for certified products They found that manufacturers were not willing to bear any cost of certification and pay any price premium for input material unless it was offset by higher prices of manufactured products received by their customers. Vlosky et al. (2003) examined attitudes of U.S. value-added wood products manufacturers with regard to current and potential participation in CoC certification. Results indicated that respondents did not have a very clear understanding of forest management or CoC certification. Studying the same sector in 2009, Vlosky et al. (2009) found that the number of respondents paying a price premium for certified inputs decreased and number of respondents receiving a premium for certified products increased between 2002 and 2008. Owari et al. (2006) found that certified wood products companies in Finland were not able to charge any price premium and certification did not help them to improve their financial performance. Tolunay and Türkoğlu (2014) examined the state of CoC certification in different forest product sectors in Turkey and the perspectives of companies to pay a premium for certified products. They found that CoC certification was known mostly by the companies operating in pulp, paper and paperboard sectors. The certification program most demanded was the Forest Stewardship Council (FSC) with a share of 15%; and Programme for the Endorsement of Forest Certification (PEFC) CoC was demanded by 2% of respondents.

Vidal et al. (2005) researched the status of CoC in Canada and the United States. They found that company size is an important variable to be considered when analysing the adoption of CoC certification by primary wood producers; larger companies are more likely to be certified than smaller ones. They also found that benefits of CoC included improved supply chain management performance, communications in supply chains, inventory controls, market knowledge, transparency, and profitability. Lower overall costs were also found to prevail (Miles and Covin 2000; PEFC 2017).

Nor Suryani et al. (2011) examined costs associated with implementation of CoC certification requirements in sawmills in Malaysia. There were three kinds of costs identified in relation to certification—standard implementation, initial audit, and surveillance audit cost. The standard implementation cost accounted for 96% of total cost. Hrabovsky and Armstrong (2005) examined experiences of U.S. hardwood exporters concerning certified hardwood products and certification. They found out that willingness-to-pay a premium was low and that only large companies owning their own forests did not have problems with certification such as supply or maintaining documentation. Bond et al. (2014) found that the main barriers to certification identified by forest products manufacturers in the state of Virginia in the U.S. were that certification systems do not add value to their products and the lack of certified raw material.

Regarding timber legality issues, CoC certificates are an acceptable measure for the legality verification of timber products required by European Timber Regulation (EUTR), in particular concerning risk assessment and risk mitigation procedures as a part of an operator’s due diligence system (European Commission 2016). As suggested by the European Forest Institute (EFI 2011), in order to make these systems fully compatible with EUTR requirements, there are only minor additional operator costs required. Therefore, implementing forest and CoC certification as an assurance for timber legality could contribute to reduced costs and administrative work for operators required to establish due diligence systems according to the EUTR. EUTR as a public policy may potentially have a positive effect on the acceptance of certification (Cashore and Stone 2012).

Holopainen et al. (2015) found out that EUTR is not likely to impact domestic timber producers and large importers with existing certification in Finland, while the impact will be on Small and Medium Enterprises (SMEs) importing timber from outside the EU without existing traceability systems. For Romanian companies, FSC certification is a useful source in providing information required by EUTR even though the certification standard does not explicitly refer to each of EUTR’s requirements; therefore FSC certification cannot be automatically considered to be in full compliance with the EUTR (Gavrilut et al. 2016).

By the end of 2015, the Forest Stewardship Council (FSC 2015) reported over 186 mil. ha and the Programme for the Endorsement of Forest Certification (PEFC 2015) 272 mil. ha of certified forests. According to UNECE (2015), the global certified area of 458.4 mil. ha included an estimated 7.5 million ha certified under both schemes with more than 80% of forest landowners with double certification in Europe and North America. By 2015, FSC had registered 29,801 and PEFC 10,744 CoC certificates to downstream manufacturers.

Despite research that has been carried out worldwide, there is limited information on CoC certification in Central and South Europe. There have been several studies focusing on the establishment and development of forest certification (Dudík and Riedl 2015; Paluš 2000; Paluš et al. 2014; Šupín 2006), but only few concentrating on the attitudes of certified companies towards forest and CoC certification (Paluš and Kaputa 2009; Halalisan et al. 2013).

Therefore, the main objective of the present research is to analyse the current state of CoC certification from the perspective of certified companies in the countries of Central and South Europe, with the focus of identifying any differences that may exist between the countries in terms of (1) understanding of concept and role of forest and CoC certification; (2) the expectations of companies following implementation of CoC certification; and (3) perceptions of any difficulties connected to certified supply chains and; (4) costs related to purchase and sales of certified raw materials and wood products, respectively.

3 The study-geographic scope

The Central and South European region plays an important role in terms of available forest resources. According to FAO (2016) timber produced in this region represents an important source of raw material not only for the domestic wood processing industry and energy production but also for export markets mainly to Western European Countries. For the purposes of this study data were collected in three Central European countries (Slovakia, Czech Republic, Poland) and three Balkan countries (Croatia, Slovenia, Serbia).

In all countries, there has been a significant participation of state forest enterprises in the initialisation of the process of forest certification and public entities represent major stakeholders implementing certification requirements. However, there are several differences regarding current and historical implementation of certification in these countries. While Croatian and Serbian forest owners use only the FSC certification scheme (2.04 mil. ha and 1.00 mil. ha, respectively), all other countries utilise both the FSC and PEFC programmes. Slovakia and the Czech Republic forests are predominantly certified by PEFC (1.25 mil ha and 1.77 mil. ha, respectively) with a small share of FSC certified forests (0.15 mil ha and 0.05 mil. ha, respectively). In Poland, with its area of almost 7 mil. ha of certified forests, more than 95% of the area is double certified. In addition to PEFC being recognised as the national system in Poland, Czech Republic, Slovenia, and Slovakia, there have also been national FSC standards developed in Poland, Serbia and Czech Republic. Past implementation of forest certification has influenced the structure and development of CoC certification in these countries. For example, FSC certificate holders are predominant in all countries (over 2300 FSC CoC vs. 540 PEFC CoC certificates) with the FSC Controlled Wood (CW) program being implemented more frequently in countries with available PEFC certified wood (e.g. 9 FSC CW in Croatia vs. 53 FSC CW in the Czech Republic).

4 Materials and methods

The study was carried out using an on-line email-based questionnaire survey. Companies selected for the survey were identified from international registries of CoC holders of the PEFC (PEFC 2015) and FSC (FSC 2015) certification schemes. A database of companies holding valid CoC certificates with available email addresses was constructed resulting in a total sample frame of 1916 companies surveyed.

Survey development and implementation was based on modified methods recommended by Dillman (2000) including a pre-notification email, as well as first and second survey emailings 3 weeks apart.

Data were collected in October and November 2015. English versions of the questionnaire were translated into the respective languages of each country and emailed to recipients by study cooperators in each country. A total of 881 (46%) responses were received, out of which 744 were suitable for analysis, thus giving the adjusted response rate of 38.8%.

The questionnaire consisted of a cover letter explaining the content and of a number of sections. The first section contained questions regarding the business profile of companies in terms of geographical location, company size, sector represented and certification scheme used. Recipient companies were categorised according to the European Commission (2003) classification into four size categories—micro (1–10 employees), small (11–50 employees), medium-size companies (51–250 employees) and large enterprises (over 251 employees). Twenty wood products and levels of trade activities were defined for companies to determine their main production and trade orientation. Respondents were grouped into one of three main sectors represented by primary processing, secondary processing and trade. Recipient companies were self-classified as PEFC, FSC or double (both PEFC and FSC) CoC certificate holders. The second section of the questionnaire contained questions examining company level of understanding of sustainable forest management and CoC certification determining the level of agreement with a number of certification-related statements. The researchers provided definitions of forest and CoC concepts to assure a consistent frame of reference for respondents.

The certification statements included the main objectives and purposes of having CoC certification, promotion/management of sustainable forest resources (Durst et al. 2006; Siry et al. 2005; Perera et al. 2007), traceability and confidence in sourcing certified raw materials and products (PEFC 2017), legality issues (Trishkin et al. 2014; Holopainen et al. 2015; Gavrilut et al. 2016), market access (Hansen and Punches 1999; Hubbard and Bowe 2004; van; Kooten et al. 2005), potential for improved communication (Owari and Sawanobori 2008), and possible improvements in internal efficiency of material flows, and effects on corporate management (Hubbard and Bowe 2004; Miles and Covin 2000).

In the third section, participants were asked to provide internal information on their involvement in the certification process, and expectations motivating them to enter certified products market. Factors included possible linkages of internal economic performance to increased sales and profit (Takahashi 2001; Miles and Covin 2000), diversification of product portfolios, market performance factors -increase of market share and penetration of new markets (Owari et al. 2006), commitment to the natural/forest environment (van Kooten et al. 2005), and improvement of company image (Trishkin et al. 2014; Vlosky et al. 2009; Hubbard and Bowe 2004). Additionally, questions were included that examined purchasing process, any difficulties in procuring certified wood, and costs to procure certified raw materials.

Another bank of questions identified any difficulties regarding the quality of delivered certified products, delivery terms, transportation, contracted price, profitability, and consistency of supply.

The final section of the questionnaire focused on price premiums paid for certified inputs and premiums received from customers for certified products (Vlosky et al. 2003, 2009).

Five-point Likert scales were used to measure many of the perception, motivations, and experiences items. They were anchored on: 1 = “strongly disagree” or “do not understand at all” to 5 = “strongly agree” or “completely understand”. In one bank of Likert-scale items, the mid-point was “somewhat understand” while the remaining item mid-points were “neither disagree nor agree” (a neutral mid-point). A reliability coefficient of 0.7 and above was considered and acceptable for item consistency level (Nunnaly 1978).

Data were analysed using SPSS. The Pearson’s Chi square test for independence was used to measure differences in distribution of categorical variables. To test mean differences in a given set of factors between the six countries, MANOVA (multivariate analysis of variance) was used. This method applies to situations where there are two or more dependent variables (Warne 2014). By performing significance tests and obtaining a multivariate F value (Wilks’ λ) it was possible to test a null hypothesis that there are no differences between countries across a number of items. Corrected models with the results of between-subject effects test were constructed to determine significance of individual variables. For the ranked statements, Duncan’s multiple comparison test was applied to determine if there were significant differences between group (country) means. To eliminate unequal group sizes, the harmonic mean was used. Additionally, Chi square test was used to identify and highlight differences between responses based on company size, certification scheme used, and product sector.

5 Results

The number of companies contacted by country and respective adjusted response rates are shown in Table 1. Out of 744 respondents 57% were from Poland, 11% from Czech Republic and Slovenia, 8% from Serbia, 7% from Slovakia and 6% from Croatia. The number of responses is correlated to the number of CoC certificates holders in each country.

Most respondents were the primary wood processors (55%), followed by trading companies (25%) and secondary wood processing (20%) representing manufacturer of a variety of products including plywood, sawnwood, chips, pellets, pulp and paper, doors, windows, furniture, and wooden construction materials.

The number of respondent employees was used as an indicator of company size. Small companies (11–50 employees) represent 41% of respondents, followed by equal representation (27% each) of micro (1–10 employees) and medium-size companies (51–250 employees). Only 5% of respondents represented large companies (over 251 employees).

Two certification systems, FSC and PEFC, provided CoC certificates to respondents; FSC (56% of respondents) and PEFC (12%), with 32% being double certified. FSC certified companies held FSC Control Wood certificates.

All group distributions were tested for differences between countries. Using the Chi square test, there were significant differences identified between the countries in terms of company size (χ 2 = 93.045, p = 0.000), forest product sector (χ 2 = 54.192, p = 0.000) and certification scheme implemented (χ 2 = 293.199, p = 0.000). Regarding respondent level of understanding of sustainable forest management (SFM) and CoC certification,, there was better understanding of CoC (4.1 on a 5-point scale) than SFM (3.6 on a 5-point scale).

Attitudes of certified companies towards objectives and purposes of CoC certification, were examined (Table 2). The reliability of factors in this bank of questions using the Cronbach’s alpha coefficient was 0.857. Results show that the highest mean score (4.0) was for respondents belief that certification helps to ensure legal origin of wood. This is followed by the ability of CoC certification to trace the supply chain back to the origin source (3.9) and the consequent effect that certification has on the prevention from illegal logging (3.8). The least level of agreement respondents expressed is with the statements regarding improvement of internal efficiency from CoC certification.

Using multivariate analysis of variance (Wilks’ Lambda), a significant difference in levels of agreement for certification statements between countries were found at a 0.05 level of significance (Wilks’ λ = 0.384, F = 15.527, p = 0.000). Table 3 shows the corrected model with the results of the between-subject effects test; differences are significant except for the highest ranked statement “ensurance of legal origin of wood” where no differences were identified (F = 1.590, p = 0.161). Taking into account that this statement was identified by respondents as the highest ranked to explain the role of CoC certification, legality issues can be considered as strongly perceived by all respondents regardless of country. On the other hand, certification is not uniformly perceived between countries as a tool for improving corporate communication or internal efficiency of corporate management.

To explore expectations that motivated respondents to enter into the certified products market, several options of the benefits of certification found in the literature were provided (Table 4). The reliability of factors using the Cronbach’s alpha coefficient was 0.779. The highest ranked motive was the “improvement of external company image” (4.2/5-point scale). Next ranked items were linked to penetrating new markets (3.9) increasing sales volume (3.9), expanded market share (3.8) and increasing profit margin (3.7). Other issues, such as the environmental commitment (3.1) and diversification of products (2.5), were considered the least motivating factors.

Multivariate analysis of variance resulted in significant difference in levels of agreement for all certification motives between countries at a 0.05 level of significance (Wilks’ λ = 0.357, F = 24.425, p = 0.000) (Table 5).

To identify where between-country differences existed in responses to the statement “improvement of external company image”, a post-hoc test was applied. The test divided countries into two groups according to homogeneity (Table 6). The level of agreement of respondents in Slovenia (3.6) significantly differed from the rest of the countries (4.1–4.3). The low level of agreement in Slovenia may be due to a high proportion of micro-enterprise respondents (27%) compared to other countries as well as the fact that more than a half of respondents (52%) are in a primary wood processing sector supplying commodity and intermediate products to secondary wood processing companies and not the end-users of wood products.

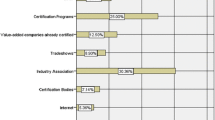

The incentives for respondents to initially become involved in certification were examined. Over 45% of respondents said they entered the certification arena to capture potential customers (Fig. 1). Certification can often be considered an option for companies to increase sales volume and expand market share. Using the Chi square test, there were significant differences identified between countries in terms of original incentives (χ 2 = 217.611, p = 0.000).

Reason for initial certification involvement (n = 744)

In addition to certification stimulus and expected benefits, focus was also put on the perceived level of problems related to the procurement of certified input material. Several problematic areas were identified for respondents (Table 7). Overpricing of certified material is considered to be the most significant problem in the certified supply chain (3.8/5-point scale) followed by supply consistency (2.6) and its supply quantity (2.4). Issues related to negotiated contract terms were perceived as less problematic. The reliability of factors using the Cronbach’s alpha coefficient was 0.703. Differences in perceiving problems related to certified supply chain between countries (Wilks’ λ = 0.207, F = 34.707, p = 0.000) were significant in all examined factors (Table 8 ).

Given that high prices of certified raw materials were the highest ranked problem associated with purchasing inputs, cross-country differences were examined. Table 9 shows that this problem is perceived to be particularly onerous by Polish respondents (4.5/5-point scale) while for all other countries it is of lower significance (2.7–2.9). It is possible that the perceived high price of certified material in Poland is the result of market conditions characterized by a high share of micro and small wood processing enterprises (nearly 80%) and one dominant supplier of raw wood material represented by the State forest enterprise managing over 77% of total forest land in the country.

Respondents were probed further about prices of certified raw materials, specifically asking if they paid a price premium for input material. Almost 34% of respondents replied that they pay over 20% more for certified products compared to non-certified; however, on the other hand, 24.2% of companies pay no premium and 14.5% pay from 6 to 10% more (Fig. 2). There were also significant differences between countries regarding price premiums paid (χ 2 = 633.752, p = 0.000).

Price premiums paid by companies for buying certified inputs (n = 744)

On the sell side of the equation, 81% of respondents do not receive any price premium for the certified products they sell, with the remaining respondents say they receive a price premium up to 15% (Fig. 3). The highest price premium is achieved in Poland where 47% of respondents are able to receive between 1 and 5% premium and nearly 48% of companies receive between 6–10% price premium. Considering that almost 76% of respondents pay a premium for certified raw materials and only 19% receive a premium from customers, certification does not appear to be a profitable activity for respondents. At the very least, costs are being absorbed by many respondents.

Price premium received by companies for selling certified products (n = 744)

Finally, the influence of company size, forest product sector and certification scheme on the highest ranked statements and issues identified by respondents was examined. The Chi square test was used to determine significance of these differences (Table 10).

Double certified (95%) and FSC certified companies (83%) are more convinced that certification is a tool that can ensure legal origin of wood as opposed to PEFC certified companies (70%). Similarly, improvement of external image of company is more highly expected to be a benefit from double certified (96%) and FSC certified companies (85%) than PEFC certified companies (77%). As for the problems perceived regarding the certified supply chain, overpriced inputs are the most problematic.

Company factors (company size, certification scheme and sector) have significant influence on variability of responses. Sixty-two percent of small companies consider overpricing to be a very problematic issue compared to 17% of large companies. However, it should be mentioned that the share of large company responses was only 4.7%. PEFC certified respondents (34%) do not see high prices of inputs as problematic as those with FSC certification (61%). Although there were significant differences identified between the responses of forest products sectors, the percent of companies in each sector category that consider high raw material prices as very problematic varied between 60–70%.

6 Discussion

This study encompassed a broad range of issues related to CoC certification. The three main areas analysed were, the understanding of concept and role of certification, expectations of companies following from implementation of CoC certification and, difficulties connected to certified supply chain and cost related to purchase and sales of certified wood products.

When discussing and interpreting the results of this study it should be kept in mind that there are many factors that could be influencing the responses, either from cultural and socio-economic differences between the countries, but also differences related to the development and implementation of forest certification and availability of certified resources in a given country. These differences were subsequently reflected in the sample composition in each country. Moreover, van Kooten et al. (2005) mention a range of different factors, including those of non-economic nature that influence decisions to meet environmental standards voluntarily.

In particular, the two countries Serbia and Croatia use only FSC certification scheme; PEFC forest certification is prevailing in the Slovak and Czech Republic, and Poland is characterised by a significant area of double certified forests. Apart from the PEFC recognised national systems in Poland, Czech Republic, Slovenia, and Slovakia, there have also been national initiatives developing FSC standards in Poland, Serbia and Czech Republic. Moreover, there is a significant share of public forests certified in the region with the main role of the state forests in the process of development and implementation of forest certification. The distribution and areas of certified forests and, consequently the number of CoC certified companies in examined countries affected the structure of respondents with regard to certification scheme used. Some 88% of respondent were holders of FSC certificates, thought 32% were double certified using both FSC and PEFC scheme.

To understand the concept of certification means that companies are aware of the meaning, roles, function and goals, which forest certification should deliver as a tool supporting sustainable forest management and utilisation of forest resources. CoC certified companies demonstrated a high level of understanding of the CoC concept, nevertheless they reported also considerable awareness with the concept related to the sustainable management of forest resources. Forest certification is mainly connected to the issue of legality, tracing the origin source of supply and a tool that prevents from illegal logging.

However, legal compliance, which forms an essential component of many sustainable forestry definitions, should be a more achievable target, and a first step in progressing towards sustainable forest management (European Commission 2004). For the EU countries legality requirements for timber are defied by the European timber regulation (EUTR), which also recognises good practice in the forestry sector such as certification or other third party verified schemes that include verification of compliance with applicable legislation to be used in the risk assessment procedure (European Commission 2016). Criteria for legality are also part of timber procurement policies and cover issues such as legal use rights to the forest, payment of all relevant fees and taxes, compliance with all relevant local and national laws and with the requirements of CITES. In almost all cases they have been adjusted slightly to ensure consistency with the definition used in the EUTR (Brack 2014). Surveyed companies can utilise certification systems to prepare for and align with the EUTR requirements, in particular concerning risk assessment and risk mitigation procedures needed for due diligence system (Gavrilut et al. 2016). Double and FSC certified companies are more convinced that certification is a tool that can ensure legal origin of wood than PEFC certified companies. Moreover, there were no differences identified between countries in perceiving the role of legality within certification. Secondly, CoC certified companies also see the certification as a tool to promote sustainable forest management and sustainable utilisation of timber, which is in line with the results of WWF (2000). Even if both, FSC and PEFC CoC standards, incorporate minimum management requirements, companies do not consider them to be improving the efficiency of internal material flow, communication and corporate management.

The main expected benefits following from certification are linked to the improvement of external company image. This factor is related to the environmental communication activities of companies. Similarly Owari and Sawanobori (2008) observed on certified companies in Japan that certified companies perceive that they gain some benefits from certification in the aspects of environmental communication and consumer relations. Vlosky et al. (2009) also documented an increase in perceiving improvement of company image as a benefit following from entering the certification arena. In the present research, improvement of external image of company is more expected to be a benefit from double and FSC than PEFC certified companies. Other expectations following from certification were linked to business performance factors such as penetrating new markets, increase of sales volume, expanded market share and the increase of profit margin. This is in line with findings of Hansen and Punches (1999) or Hubbard and Bowe (2004) who argue that certification may serve to improve corporate image of companies and access to markets. The present results also indicate that companies expect these market benefits with the existing production patterns and there is no need to diversify products portfolio to meet the increasing demand for certified products.

The last but not least analysed area focused on difficulties connected to certification and related costs. In the certified supply chain the main problem seems to be overpricing of certified material followed by difficulties related to the consistency and quantity of supply. As for the problems perceived regarding the certified supply chain, the findings here suggest that overpriced inputs are more problematic for small and FSC certified companies. For companies one of the most important reasons for forest certification is the premise that customers are willing to pay a premium for products originating from well managed forest (Carter and Merry 1998; Hayward and Vertinsky 1999; Perera et al. 2007). The results confirm that almost all companies do not receive any (or minimum) price premium for their certified products. Similar results were revealed in many other regions of the world. In North America Hubbard and Brown (2005), Hrabovsky and Amstrong (2005) and in Japan Owari and Sawanobori (2008) identified little or no premium associated with certified products. In companies, the value of price premium is not able to cover the costs of CoC certification, and therefore the absence of premium is the most important reason why certification does not increase profitability and enhance business performance in the short term.

7 Conclusion

The study was aimed at examining the status of CoC certification in the countries of Central and South Europe, notably in Slovakia, Czech Republic, Poland, Croatia, Slovenia, and Serbia. In all surveyed countries forest certification has been implemented into forest management practices and there is a network of CoC certified companies utilising available certified wood resources. In particular, the understanding of concept and role of certification, expectations of companies following from implementation of CoC certification and difficulties connected to certified supply chain and cost related to purchase and sales of certified wood products were analysed. The following conclusions can be drawn:

-

there are differences between countries in terms of certified forest area, certification scheme used and number of CoC certified companies following from the development process of forest certification in particular countries,

-

CoC certified companies demonstrated a high level of understanding of the CoC concept, nevertheless they reported also considerable awareness of the concept related to the sustainable management of forest resources,

-

companies in all surveyed countries link forest certification mainly to the issues of legality, tracing the origin source of supply and prevention from illegal logging, rather than a tool to promote sustainable forest management and sustainable utilisation of timber,

-

expected main benefits following from certification are linked to the improvement of external company image followed by business performance factors such as penetrating new markets, increase of sales volume, expanded market share and the increase of profit margin.

-

main problem connected to certified supply chain relate to the overpricing of certified material inputs followed by difficulties associated with the consistency and quantity of supply. On the other hand, companies receive none or minimum price premium for selling their certified products.

-

compared to PEFC certified companies double certified and FSC certified companies tend to be more convinced that certification is a tool that can ensure legal origin of wood and improve external image of company.

-

high input material prices are considered to be the most problematic issue in the certified supply chain. In particular, small size and FSC certified companies regard overpricing as serious issue.

References

Auld G, Gulbrandsen LH, McDermott CL (2008) Certification schemes and the impacts on forests and forestry. Annu Rev Environ Resour 33:187–211

Bigsby H, Ozanne LK (2002) The purchase decision: consumers and environmentally certified wood products. For Prod J 52:100–105

Bond B, Lyon S, Munsell J, Barrett S (2014) Perceptions of Virginia’s primary forest products manufacturers regarding forest certification. For Prod J 64:242–249

Brack D (2014) Promoting legal and sustainable timber: using public procurement policy. Research paper. Chatham House Publishing. https://www.chathamhouse.org/sites/files/chathamhouse/field/field_document/20140908PromotingLegalSustainableTimberBrackFinal.pdf. Accessed 16 Jun 2016

Brundtland GH (1987) Our common future—report of the world commission on environment and development. Oxford University Press, Oxford

Cabarle B, Hrubes RJ, Elliot C, Synnot T (1995) Certification and accreditation: the need for credible claims. J For 93:1–12

Carter DR, Merry FD (1998) The nature and status of certification in the United States. For Prod J 48:23–28

Cashore B, Stone M (2012) Can legality verification rescue global forest governance? Analyzing the potential of public and private policy intersection to ameliorate forest challenges in Southeast Asia. For Policy Econ 18:13–22. https://doi.org/10.1016/j.forpol.2011.12.005

Creamer SF, Blatner KA, Butler BJ (2012) Certification of family forests: what influences owners’ awareness and participation? J For Econ 18:131–144

De Pelsmacker P, Driesen L, Rayp G (2005) Do consumers care about ethics? Willingness to pay for fair-trade coffee. J Cons Aff 39:363–385. https://doi.org/10.1111/j.1745-6606.2005.00019.x

Dillman DA (2000) The tailored design method. Wiley. New York

Dudík R, Riedl M (2015) The possibilities of using C-O-C certifications in the czech republic. In: Wood processing and furniture manufacturing challenges on the world market and wood-based energy goes global, proceedings of scientific papers, Woodema, Zagreb. WoodEma Publishing. http://www.woodema.org/proceedings/WoodEMA_2015_Proceedings.pdf. Accessed 17 June 2016

Durst PB, Mckenzie PJ, Brown CL, Appanah S (2006) Challenges facing certification and eco–labelling of forest products in developing countries. Int For Rev 8:193–200

EFI (2011) Support study for development of the non-legislative acts provided for in the Regulation of the European Parliament and of the Council laying down the obligations of operators who place timber and timber products on the market. Final report. http://ec.europa.eu/environment/forests/pdf/EUTR-Final_Report.pdf. Accessed 10 Apr 2017

European Commission (2003) COMMISSION RECOMMENDATION of 6 May 2003 concerning the definition of micro, small and medium-sized enterprises (2003/361/EC). EUR-Lex Publishing. http://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:32003H0361&from=EN. Accessed 19 Jun 2016

European Commission (2004) Briefing note No. 04. FLEGT Briefing Notes. Forest Law Enforcement, Governance and Trade. Why the focus on legality, not sustainability? European Commission Publishing. https://ec.europa.eu/europeaid/sites/devco/files/publication-flegt-briefing-note-4-200404_en.pdf. Accessed 19 June 2016

European Commission (2016) Regulation (EU) No 995/2010 of the European Parliament and of the Council of 20 October 2010 laying down the obligations of operators who place timber and timber products on the market. EUR-Lex Publishing. http://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:32010R0995&from=EN. Accessed 16 June 2016

FAO (2016) Forestry production and trade. http://www.fao.org/faostat/en/#data/FO

Fischer C, Parry I, Aguilar PJ (2005) Corporate codes of conduct: is common environmental content feasible? Discussion paper 05–09, Resources for the future. Resources for the Future Publishing. http://www.rff.org/files/sharepoint/WorkImages/ Download/RFF-DP-05-09.pdf. Accessed 13 Jun 2016

FSC (2015) http://info.fsc.org/certificate.php. Accessed 27 Jun 2016

Gavrilut I, Halalisan AF, Giurca A, Sotirov M (2016) The interaction between FSC certification and the implementation of the EU timber regulation in Romania. Forests 7:3–5

Gilani HR, Kozak RA, Innes JL (2016) The state of innovation in the British Columbia value-added wood products sector: the example of chain of custody certification. Can J For Res 46:1067–1075

Halalisan AF, Marinchescu M, Popa B, Abrudan IV (2013) Chain of Custody certification in Romania: profile and perceptions of FSC certified companies. Int For Rev 15:305–314

Hansen E, Punches J (1999) Developing markets for certified forest products: a case study of collins pine company. Forest Prod J 4:30–35

Hayward J, Vertinsky I (1999) High expectations, unexpected benefits—what managers and owners think of certification. J Forest 97:13–17

Holopainen J, Toppinen A, Perttula S (2015) Impact of European Union Timber regulation on forest certification strategies in the finnish wood industry value chain. Forests 6:2879–2896

Hrabovsky EE, Armstrong JP (2005) Global demand for certified hardwood products as determined from a survey of hardwood exporters. For Prod J 55:28–35

Hubbard S, Bowe S (2004) Putting value on certified forest products: views from Wisconsin. Wood Wood Prod 57–62

Hubbard SS, Bowe SA (2005) Environmentally certified wood products: perspectives and experiences of primary wood manufactures in Wisconsin. For Prod J 55:33–40

Jayasinghe PS, Allen D, Bull GQ, Kozak RA (2007) The status of forest certification in the Canadian value-added wood products manufacturing sector. For Chron 83:113–125

Lewis RA, Davis SR (2015) Forest certification, institutional capacity, and learning: an analysis of the impacts of the Malaysian timber certification scheme. For Policy Econ 52:18–26

Mac Dicken KG, Sola P, Hall JE, Sabogal C, Tadoum M, Wasseige C (2015) Global progress toward sustainable forest management. For Ecol Manag 352:47–56

Miles MP, Covin JG (2000) Environmental marketing: a source of reputational, competitive, and financial advantage. J Bus Ethics 23:299–311

Moore SE, Cubbage F, Eicheldinger C (2012) Impacts of forest Stewardship Council (FSC) and sustainable forestry initiative (SFI) forest certification in North America. J For 110:79–88

Nakamura M, Takahashi T, Vertinsky I (2001) Why Japanese firms choose to certify: a study of managerial responses to environmental issues. J Environ Econ Manag 42:23–52

Nor Suryani AG, Mohd Shahwahid HO, Ahmad Fauzi P, Alias R, Vlosky RP (2011) Assessment of Chain-of-Custody certification costs for sawnwood manufacturers in Peninsular Malaysia. J Trop For Sci 23:159–165

Nunnaly J (1978) Psychometric theory. McGraw-Hill, New York

Owari T, Sawanobori Y (2008) Market benefits of chain of custody certification, perspectives of Japanese suppliers. For Resour Manag Math Mod 7:121–132

Owari T, Juslin H, Rummukainen A, Yoshimura T (2006) Strategies, functions and benefits of forest certification in wood products marketing: perspectives of Finnish suppliers. For Policy Econ 9:380–391

Paluš H (2000) Review on certification of non-industrial private forests in Europe. In Marketing 2000: marketing at break of the millenium. Technical University in Zvolen, Zvolen. Alfa Print Publishing. https://www.tuzvo.sk/files/DF/katedry_df/ kmosl/veda_a_vyskum/zborniky/mao_2000.pdf. Accessed 28 Jun 2016

Paluš H, Kaputa V (2009) Survey of attitudes towards forest and chain of custody certification in the Slovak Republic. Drewno 52:65–81

Paluš H, Maťová H, Križanová A, Parobek J (2014) Prieskum znalosti značiek lesných certifikačných schém na výrobkoch z dreva a papiera (A survey of awareness of forest certification schemes labels on wood and paper products). Acta Facultatis Xylologiae Zvolen 56:129–138

Peck T (2001) The international timber trade. Woodhead Publishing Ltd., Cambridge

PEFC (2015) http://www.pefc.org/find-certified/certified-certificates. Accessed 26 June 2016

PEFC (2017) PEFC chain of custody certification. The key to sell certified products. https://www.pefc.org/images/documents/brochures/PEFC_Chain_of_Custody_Certification.pdf

Perera P, Vlosky RP, Hughes G, Dunn M (2007) What do Louisiana and Mississippi nonindustrial private forest landowners thing about forest certification? South J Appl For 31:170–175

Potkanski T, Wanat L, Chudobiecki J (2011) Leadership in time of crisis or crisis of leadership? Implications for regional development. Intercathedra 27:45–52

Rametsteiner E, Simula M (2003) Forest Certification—an instrument to promote sustainable forest management? J Environ Manage 67:87–98

Rickenbach M, Overdevest C (2006) More than markets: assessing Forest Stewardship Council (FSC) certification as a policy tool. J For 104:143–147

Siry JP, Cubbage FW, Ahmed MR (2005) Sustainable forest management: global trends and opportunities. For Policy Econ 7:551–561

Šupín M (2006) Forest and wood products certification influence on strategies for entering and developing international markets. Intercathedra 22:166–169

Takahashi T (2001) Why firms participate in environmental voluntary initiatives: case studies in Japan and Canada. The University of British Columbia, Vancouver

Tolunay A, Türkoğlu T (2014) Perspectives and attitudes of forest products industry companies on the chain of custody certification: a case study from Turkey. Sustainability 6:857–871

Trishkin M, Lopatin E, Karjalainen T (2014) Assessment of motivation and attitudes of forest industry companies toward forest certification in northwestern Russia. Scand J For Res 29:283–293

Tuppura A, Toppinen A, Puumalainen K (2016) Forest certification and ISO 14001: current state and motivation in forest companies. Bus Strat Environ 25:355–368

Ulybina O, Fennell S (2013) Forest certification in Russia: challenges of institutional development. Ecol Econ 95:178–187

UNECE (2015) Forest products annual market review 2014–2015. United Nations, Geneva

UNECED (1992) Non-legally binding authoritative statement of principles for a global consensus on the management, conservation and sustainable development of all types of forests. In: Proceedings of the UN conference on environment and development, Rio de Janeiro. UN Publishing. http://www.un.org/documents/ga/conf151/ aconf15126-3annex3.htm. Accessed 9 Jun 2016

Van Kooten GC, Nelson HW, Vertinsky I (2005) Certification of sustainable forest management practices: a global perspective on why countries certify. For Policy Econ 7:857–867

Vidal N, Kozak R, Cohen D (2005) Chain of custody certification: an assessment of the North American solid wood sector. Forest Policy Econ 7:345–355

Vlosky RP, Ozanne LK (1998) Environmental certification of wood products: The U.S.manufacturers’ perspective. Forest Prod J 48:21–26

Vlosky RP, Gazo R, Cassens D (2003) Certification involvement by selected united states value-added solid wood products sectors. Wood Fiber Sci 35:560–569

Vlosky RP, Gazo R, Cassens D, Perera P (2009) Changes in value-added wood product manufacturer perceptions about certification in the United States from 2002 to 2008. Drvna Industrija 60:89–94

Warne RT (2014) A primer on multivariate analysis of variance (MANOVA) for behavioral scientists. Practical assessment. Res Eval 19:1–10

WWF (2000) The forest industry in the 21st century. Report prepared by the WWF’s forests for life campaign. Branksome House, Godalming

Acknowledgements

The authors are grateful for the support of the Scientific Grant Agency of the Ministry of Education, Science, Research and Sport of the Slovak Republic, and the Slovak Academy of Sciences, Grant No. 1/0473/16, “Dynamics and determinants of wood based products market in the Slovak Republic” and the Slovak Research and Development Agency, Grant APVV-14-0869 “Research of the utilization of wood as a renewable raw material in the context of a green economy”.

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Paluš, H., Parobek, J., Vlosky, R.P. et al. The status of chain-of-custody certification in the countries of Central and South Europe. Eur. J. Wood Prod. 76, 699–710 (2018). https://doi.org/10.1007/s00107-017-1261-0

Received:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00107-017-1261-0