Abstract

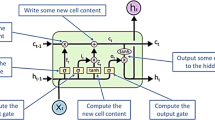

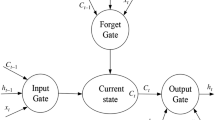

The stock market is an important part of the financial market, is closely related to economic development. Various analysis and forecasting problems of stock prices have always existed along with the establishment of financial markets. For this reason, this article uses the historical transaction data of the Shanghai A-share 50 as the research object to carry out forecasting and analysis of the closing price trend. Predict the stock price trend through ARIMA model and LSTM model. After empirical research, combined with error indicators and transaction performance to show the model's forecasting accuracy and forecasting effect, it is finally concluded that the deep neural network model based on the LSTM model has better forecasting accuracy. And by using a variety of deep learning methods, we can discover potential profit opportunities in the current market from historical transaction data in the financial market, and guide institutions and individual investors to make better investment behaviors.

Access this chapter

Tax calculation will be finalised at checkout

Purchases are for personal use only

Similar content being viewed by others

References

Ying H, Varatharajan R (2021) Research on influencing factors of stock returns based on multiple regression and artificial intelligence model. J Intell Fuzzy Syst 40(4)

Polamuri SR, Srinivas K, Mohan AK (2020) Multi model-based hybrid prediction algorithm (MM-HPA) for stock market prices prediction framework (SMPPF). Arab J Sci Eng (prepublish)

Wu JM-T, Li Z, Herencsar N, Vo B, Lin JC-W (2021) A graph-based CNN-LSTM stock price prediction algorithm with leading indicators. Multimedia Syst (prepublish)

Fazle RMd, Yazhou T, Imran HMd, Insup L, Maida AS, Xiali H (2021) Stacked LSTM based deep recurrent neural network with Kalman smoothing for blood glucose prediction. BMC Med Inform Decis Making 21(1)

Musa Y, Joshua S (2020) Analysis of ARIMA-artificial neural network hybrid model in forecasting of stock market returns. Asian J Prob Stat

Rahul P, Kanishk B, Aman S, Vikram R (2021) Stock trend prediction and analysis using LSTM neural network and dual moving average crossover algorithm. IOP Conf Ser Mater Sci Eng 1131(1)

Yadav A, Jha CK, Sharan A (2020) Optimizing LSTM for time series prediction in Indian stock market. Procedia Comput Sci 167

Moghar A, Hamiche M (2020) Stock market prediction using LSTM recurrent neural network. Procedia Comput Sci 170

Ding G, Qin L (2019) Study on the prediction of stock price based on the associated network model of LSTM. Int J Mach Learn Cybern (prepublish)

Bangru X, Xinyu M, Ruihan W, Xin W, Zhengxia W (2021) Combined model for short-term wind power prediction based on deep neural network and long short-term memory. J Phys Conf Ser 1757(1)

Ji L, Zou Y, He K, Zhu B (2019) Carbon futures price forecasting based with ARIMA-CNN-LSTM model. Procedia Comput Sci 162

Zhou K, Kun Z, Yong WW, Teng H, Huang WC (2020) Comparison of time series forecasting based on statistical ARIMA model and LSTM with attention mechanism. J Phys Conf Ser 1631(1)

Yin T, Jin yu Y, Jian C (2019) Comparative research on influencing factors of LSTM deep neural network in stock market time series prediction. Res Econ Manag 4(1)

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2022 The Author(s), under exclusive license to Springer Nature Singapore Pte Ltd.

About this paper

Cite this paper

Ding, W., Jin, C., Yang, S. (2022). Comparison of Two Models Based on Deep Neural Network Prediction. In: Atiquzzaman, M., Yen, N., Xu, Z. (eds) 2021 International Conference on Big Data Analytics for Cyber-Physical System in Smart City. BDCPS 2021. Lecture Notes on Data Engineering and Communications Technologies, vol 102. Springer, Singapore. https://doi.org/10.1007/978-981-16-7466-2_20

Download citation

DOI: https://doi.org/10.1007/978-981-16-7466-2_20

Published:

Publisher Name: Springer, Singapore

Print ISBN: 978-981-16-7465-5

Online ISBN: 978-981-16-7466-2

eBook Packages: Intelligent Technologies and RoboticsIntelligent Technologies and Robotics (R0)