Abstract

Despite the presence of a large chunk of manufacturing firms in the informal sector in India, we know very little about their characteristics and evolution over time in a period when the Indian economy has been increasingly globalized. What constrains firm growth, productivity and wages in the informal manufacturing sector in India? How different are the characteristics of firms in the Indian informal manufacturing sector across the different types of firms that populate this sector, across household and non-household enterprises? How have firm characteristics including firm size and firm productivity changed in the 2000s, a period of rapid globalization in India? In this chapter, we attempt to address this gap in the literature by conducting a detailed investigation of informal manufacturing firms in India, using rich unit record data on these firms from the NSSO for the years 2000–01, 2005–06, 2010–11 and 2015–16. To be specific, we first look at the evolution of firm size across the three different categories of firms in the Indian informal manufacturing sector—own account manufacturing enterprises (OAMEs), non-directory manufacturing enterprises (NDMEs) and directory manufacturing enterprises (DMEs), first in the aggregate and then by state and industry. We then look at firm size and productivity by different sets of firms’ characteristics (location of the firm, age and gender and social group of the owner) to see if there are observable differences in firm size and productivity across firms of different characteristics. We note the presence of the ‘missing middle’ problem in Indian manufacturing. One important concern about firms in the informal sector is that they pay less wages to their workers than firms in the formal sector. We capture this by examining the differences in wages paid to workers by specific characteristics of firms—by firm type, ownership, social group of owner and firm size. Our findings suggest the need to enhance firm productivity in the Indian informal sector, as a means to improve the living standards of the workers employed in the informal sector. We also notice that there exist significant social and economic barriers to informal firms in increasing their productivity, which is a matter of major policy concern.

Access provided by Autonomous University of Puebla. Download chapter PDF

Similar content being viewed by others

Keywords

1 Introduction

One of the most remarkable features of India’s economic development in the past two decades is that in spite of rapid economic growth, the informal sector has not shown signs of withering away. While the informal sector tends to dominate in the services sector of many other low-income countries, in India, we have a large informal presence in the manufacturing sector as well. The informal manufacturing landscape in India is populated by both household enterprises, called own account manufacturing enterprises (OAMES) in the Indian context, and non-household enterprises. The OAMEs use only family labour and are often single-person establishments. The non-household enterprises are those that employ at least one hired labour and are further classified into two, non-directory manufacturing establishments (NDMEs) and directory manufacturing establishments (DMEs), based on the number of workers they employ. While NDMEs employ five or less workers, DMEs employ six or more workers.

In this chapter, we ask what we know about the informal manufacturing, using the most recent representative data on informal manufacturing firms available so far. We proceed as follows. We first look at the evolution of firm size across the three different categories of firms in the Indian informal manufacturing sector—OAMEs, NDMEs and DMEs—first in the aggregate and then by state and industry. We then look at firm size and productivity by different sets of firms’ characteristics (location of the firm, age and gender and social group of the owner) to see if there are observable differences in firm size and productivity across firms of different characteristics. One important concern about firms in the informal sector is that they pay less wages to their workers than firms in the formal sector. We capture this by examining the differences in wages paid to workers by specific characteristics of firms—by firm type, ownership, social group of owner and firm size. Throughout this chapter, we apply frequency weights provided by the National Sample Survey Organization (NSSO) to compute descriptive statistics, which is often advocated when estimating population averages from the sample data (Solon et al. 2013). This study overlaps with our earlier work (Raj and Sen 2016). But in this chapter, we have used the most recent data on the informal sector to see how those earlier findings have changed.

We use unit-rich unit record data on the informal sector firms drawn from the NSSO surveys on the unorganized manufacturing sector for four years, 2000–01, 2005–06, 2010–11 and 2015–16. We focus on these years as the Indian economy, partly due to the availability of firm-level data and partly because our interest is in understanding the behaviour of the Indian informal manufacturing sector in the post-reform period. The Indian government has enacted a far-reaching set of economic reforms since 1991. These reforms led to greater integration of the Indian economy with the rest of the world, especially its manufacturing sector. Given the importance of the informal sector in India’s economy, there has been relatively little scholarship on informal firms in an era of globalization (the exception is Raj and Sen 2016). This chapter attempts to address this limitation.

The NSSO surveys collect information on various aspects of the enterprises/units in the informal manufacturing sector quinquennially, using a stratified random sampling procedure. These are nationwide enterprise-level surveys covering all the Indian states and Union Territories (UTs) and are stratified by district. Since most informal enterprises are not registered with any government authority, the NSSO uses a block enumeration approach to ensure a representative sample of the informal sector in every district.

2 Evolution of Firm Size and Firm Productivity

This section examines the trends in size and labour productivity in the Indian informal manufacturing sector. First, we look at the temporal variations in average firm size and labour productivity across different enterprise types—OAME, NDME and DME. We then pore over these variations at the state and industry levels. Finally, we examine the variations in firm size and firm labour productivity by ownership and location of the firm.

2.1 Aggregate Trends

Using number of workers as the proxy for firm size, we present the trends in average firm size for all the three enterprise types for the periods from 2000–01 to 2015–16, in Fig. 2.1. Our estimates suggest a consistent but marginal decline in the size of an average OAME over time. An average NDME too witnessed a steady but marginal drop in its size after a slight increase between 2000–01 and 2005–06. The DMEs, on the other hand, saw their average size increasing between 2000–01 and 2015–16. However, after a steady expansion of size in the 2000s, there was a marginal decline in the size of an average DME in the last quinquennium of our study period. In terms of size, the DMEs are more than three times larger than the NDMEs, which are double the size of the OAMEs.

Firm size by enterprise type, 2000–01 to 2015–16. Source: Authors’ estimates

Our rural-urban comparison of average firm size mirrors the pattern that we observed at the aggregate level (Fig. 2.2). However, these changes are more marked for firms in the rural areas than in the urban areas. For instance, the rural OAMEs and rural NDMEs exhibited a much larger decline in their average size as compared to their counterparts in urban areas. Our computations show that the size of an average OAME and an average DME in the rural areas declined 22 per cent and 9 per cent, respectively, compared to a decline of 17 per cent and 6 per cent, respectively, for their urban counterparts. Perhaps the most striking finding from our analysis is that the rural DMEs are larger in size than the urban DMEs. We had expected urban firms to be larger, given that products made by these informal firms would have a bigger market due to the higher population density in these areas. Additionally, the rural DMEs showed a faster growth in size compared to their counterparts in urban areas. While an average DME in rural areas grew by 11 per cent, the corresponding figure for the urban DME was 7 per cent. In absolute terms, the number of workers employed by an average rural DME has increased from 11 workers in 2000–01 to 13 workers in 2015–16. On the other hand, the average urban DME witnessed an expansion in size from nine workers in 2000–01 to ten workers in 2015–16. This minimal increase in the size of urban DMEs explains why there is only a marginal rise in the size of the average DME in the combined rural and urban sample over the period from 2000–01 to 2015–16.

Firm size by enterprise type and sector, 2000–01 to 2015–16. Source: Authors’ estimates

When we look at the labour productivity levels across different size categories (Fig. 2.3), we notice a consistent increase in productivity for all enterprise types over the period from 2000–01 to 2015–16 (Fig. 2.4). As expected, average labour productivity levels are found to be the highest among the DMEs, followed by the NDMEs and the OAMEs. This difference in productivity levels that we observed at the aggregate level is clearly evident for urban firms but not for rural firms. While the OAMEs are the least productive firms in rural areas, the NDMEs and the DMEs are equally productive.

Labour productivity by enterprise type and sector. Source: Authors’ estimates

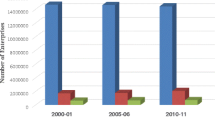

Histogram of frequency of firms for different size classes. Source: Authors’ estimates

We next examine histograms of frequency of firms and firm productivity across different size classes, for the years 2000–01, 2005–06, 2010–11 and 2015–16. To do this, we classify the firms into six size categories based on the number of workers employed by them. They are firms with 1–2 workers, those with 3–5 workers, those with 6–9 workers, those with 10–15 workers, firms with 16–19 workers and those firms that employ 20 or more workers. Over the period from 2000–01 to 2015–16, we notice a consistent increase in the number of firms in the smallest size category (1–2 workers, which are mostly OAMEs) and the largest size categories (16–19 and 20 and above). In contrast, the intermediate size classes (3–5 size category, which are mostly the NDMEs, 6–9 size category and 10–15 size category) registered a considerable decline in the number of firms. On the other hand, the productivity seems to be higher among the firms in the intermediate classes as compared to those in the lower and upper size categories. This inverted-U-shaped relationship between firm size and labour productivity is evident in all time periods. Figure 2.5 clearly shows that firm productivity increased steadily up to the 10–15 size category and then declined.Footnote 1

Histogram of firm labour productivity (in ‘00s) for different size classes, 2000–01, 2010–11 and 2015–16. Source: Authors’ estimates

Our discussion on firm size and productivity presents two possible developments occurring simultaneously in the Indian informal manufacturing sector: (a) the absence of transition from family firms to non-family firms with at least one hired worker, as apparent from the shrinking size of an average firm in the informal sector (from 2.15 in 2000–01 to 1.83 in 2015–16) and (b) the absence of upward progression of firms from the informal sector to the formal sector, as evident from the accumulation of firms in the border categories (at the unorganized/organized firm threshold—which is 10 workers for firms with power and 20 workers without power). Evidently, the transition within the non-household segment of the informal sector continues till they reach the unorganized/organized firm-size threshold as defined by the Factories Act, at which point few firms may be making the transition to the formal/organized sector. We explore this point further by combining the microdata from Annual Survey of Industries (ASI) with that from National Sample Survey Office’s surveys on unorganized manufacturing sector so that we have a continuum of firms from the very smallest (except the household enterprises) to the very largest. To be specific, we include informal sector firms with six to nine workers that employ mostly hired labour with the firms in the formal sector. Evidence from the merged data set lends support to our conjecture that very few small firms make the transition to larger firms. This is readily apparent from the firm size distribution in Fig. 2.6, which points to the presence of a dualistic structure with a bipolar distribution in firm size distribution in Indian manufacturing. Two prominent modes, one on the left (represented by 6–9 and 10–49 categories) and one on the right (represented by 500 and above) side of the employment distribution, with a striking trench in the share of employment in the intermediate size categories, from 50–499 workers, are noticed. This phenomenon, commonly referred to in the literature as ‘missing middle’, characterizes the presence of large number of small firms, some large firms, but very few medium-sized firms in Indian manufacturing. We also find that this pattern remains more or less unaltered during the ten-year period between 2000–01 and 2010–11. Evidence also points to the substantial economic distance between small and large firms in India. As evident from Fig. 2.7, the firms in the 500+ category are about 13 times more productive than firms in the 6–9-size category in 2010–11. Moreover, the gap in productivity has widened between 2000–01 and 2010–11, from 1:11 to 1:13. On the whole, we notice two significant characteristics of manufacturing sector in India: (a) the limited vertical progression of firms within the informal sector, from the household segment to the non-household segment and (b) the clustering of firms in the borderline categories, explaining the weak graduation of firms from large informal firms to formal sector firms. Our preliminary evidence also show why the presence of missing middle is a drag on the growth and productivity of Indian manufacturing sector. Though there are some sporadic attempts to locate the factors that might explain the presence of missing middle in Indian manufacturing, these are mostly suggestive and lack empirical evidence. Further research is needed to establish the relative importance of these factors in influencing limited firm transition, which is, however, beyond the scope of this study.

Employment by size groups in manufacturing firms in India. Source: Authors’ computations based on ASI and NSSO data. Note: Category 6–9 stands for firms with 6 to 9 workers, category 10–49 stands for firms with 10 to 49 workers and other categories have to be understood similarly

Labour productivity differential by size groups (labour productivity of 500+ = 100). Source: Authors’ computations based on ASI and NSSO data. Note: Category 1–5 stands for firms with 1 to 5 workers, category 6–9 stands for firms with 6 to 9 workers and other categories have to be understood similarly

3 State and Industry Differences in Firm Size and Productivity

The changes in the distribution of firm size and productivity at the industry and state levels are captured in this section. For brevity, we confine our analysis to the latest two time periods, 2010–11 and 2015–16. In line with the all-India trends, the average firm size has declined in most states, and it is evident across all the three enterprise types (Table 2.1). The OAMEs contracted in size in majority of the states—about four-fifth of the states witnessed shrinking OAMEs. The NDMEs and DMEs also declined in size in 21 of 35 states. The OAMEs, on average, are larger in size in the states of Uttar Pradesh, Odisha and Madhya Pradesh; in all these states, they have also shrunken in size. The biggest NDMEs, in terms of average size, are in Gujarat and Delhi. These too have witnessed size contraction. The biggest DMEs, by average size, are in the states of Uttarakhand, Assam, Jharkhand and Uttar Pradesh. In Uttarakhand and Assam, an average DME has expanded in size, while size contraction can be seen in Jharkhand and Uttar Pradesh. In Uttarakhand, an average DME has more than doubled in size: from 9 workers in 2010–11 to 19 workers in 2015–16, while in Assam its size has gone up from 9 workers in 2010–11 to 15 workers in 2015–16. The decline in size for DMEs in Uttar Pradesh was marginal, while in Jharkhand the average size almost halved.

At the industry level, too, we observe a trend similar to that found at the regional level. The average firm size has declined in majority of the industries, and the decline is evident across enterprise types (Table 2.2). The OAMEs experienced size contraction in 14 industries, and the NDMEs and the DMEs in 13 industries. A decline in firm size is reported for all enterprise types in the manufacture of tobacco products, textiles, petroleum products, metal products, electronic goods, furniture, other manufacturing products and repairs. The OAMEs, NDMEs and DMEs exhibited size expansion in beverages, chemicals and machinery goods. The OAMEs are, on average, bigger in size in the manufacture of mineral products, petroleum products and motor vehicles, which are the only industries where OAMEs employ two or more workers. The firm size of an average NDME is the highest in industries producing pharmaceuticals, rubber and plastics and mineral products. As for DMEs, the average number of workers is substantially higher in the manufacture of mineral products. An average DME in the mineral product industry employs about 19 workers. DMEs in other manufacturing products come next by employing, on average, about 14 workers each.

Do substantial economic differences between firms across industries, states and enterprise types exist over time? We investigate this in Tables 2.3 and 2.4, which report inter-state and inter-industry variations in labour productivity across enterprise types, over time. As expected, barring a very few cases, all industries and states have witnessed a significant surge in productivity levels between 2010–11 and 2015–16. The increase in productivity is visible across all enterprise types. Our evidence also points to the existence of considerable regional-level variations in productivity levels. At the state level, the productivity levels are found to the lowest in West Bengal and the highest in Delhi for OAMEs. In the case of NDMEs, Delhi and Gujarat reported the highest productivity levels and Odisha and Uttar Pradesh reported the lowest. The DMEs are relatively more productive in Gujarat and Delhi and less productive in Madhya Pradesh and West Bengal. For instance, our computations suggest that a DME operating in Gujarat is more than two times productive than an average DME from Madhya Pradesh. There are substantial industry-level variations in productivity too (Table 2.4). In the case of OAMEs, labour productivity ranged from 74 in paper products to 647 in the manufacture of electronic products. For OAMEs, it varied from a lowest figure of 224 for tobacco products to a highest figure of 1105 for machinery. When it comes to DMEs, the output per worker is highest in the manufacture of machinery goods and the highest in the manufacture of tobacco products. On the whole, we find that there has been a substantial increase in productivity across industries and regions over time in the informal manufacturing sector in India. Alongside, we also observe that the economic differences between sectors and regions have also widened during this period.

4 Firm Size and Ownership

We explore the difference in firm size across different ownership categories in this section.Footnote 2 Three ownership categories of firms are specified: Proprietary (Male), Proprietary (Female) and Partnership.Footnote 3 In proprietary firms, an individual is the sole owner of the enterprise, and they are mostly operated from the household. We classify these firms further into two based on the gender of the owner: Proprietary (Male) if the proprietary firms are male-owned and Proprietary (Female) if they are female-owned. The NSSO defines partnership as the “relation between persons who have agreed to share the profits of a business carried on by all or any one of them acting for all” (NSSO 2002). It is very much possible that the partners may be drawn from the same household or from different households. In our case, we pool them together into one category and call them ‘Partnership’.

The main objective here is to examine whether the average firm size varies across the three ownership categories defined above. We first capture the difference in firm size across the three enterprise types in each ownership category (Fig. 2.8). As expected, the size of an average OAME, NDME and DME is higher among the partnership firms. However, our estimates do not suggest a substantial difference in firm size between male-owned and female-owned proprietary firms. Whether an OAME, an NDME or a DME, the proprietary firm run by a female entrepreneur is marginally smaller in size as compared to a male-owned enterprise in the same category. Predictably, the argument that ‘the larger the firm size, higher will be the productivity’ survives the scrutiny of our analysis. Among all the ownership categories, the DMEs are the most productive, followed by the NDMEs and the OAMEs (Fig. 2.9). A comparison of the ownership categories reveals that the OAMEs and the NDMEs are more productive among male-owned proprietary firms, while the DMEs are more productive among the partnership firms.

Firm size by enterprise type and ownership. Source: Authors’ estimates

Average labour productivity by enterprise type and ownership. Source: Authors’ estimates

The differences in average firm size and productivity for rural and urban firms are also examined for the three ownership categories (Figs. 2.10 and 2.11). The average firm size is the highest in firms that operate on a partnership basis in both rural and urban areas. To be specific, the partnership firms are nearly twice larger than the proprietary firms owned by males—the next highest in firm size (Fig. 2.10). Strikingly, urban partnership firms are smaller than their counterparts in rural areas. We find that the huge difference in firm size between urban and rural DMEs explain the overall rural-urban firm size differential. According to our estimates, the rural DMEs are, on average, two times bigger than the urban DMEs. As expected, the urban firms are more productive in all ownership categories (Fig. 2.11). A comparison of productivity levels across the three categories, however, shows that it is the male-owned proprietary firms that produce more output per worker than the partnership firms and the female-owned proprietary firms. Perhaps the differences in endowments are likely to explain the performance differential between male-owned and female-owned firms. This is clearly evident when we look at the nature of labour input employed by firms run by men and women. Women-owned firms tend to employ far fewer paid workers, operating instead as single-person firms or with unpaid family workers. Available evidence in the literature points to the differences in motivation as the one possible reason for such differences, with male-owned firms driven by growth and profitability motives and female-owned firms by subsistence (Daymard 2015). The presence of paid workers in a firm is taken as an indicator to represent the profitability considerations of an entrepreneur as against the subsistence motive. At the same time, one cannot ignore the role of other factors such as social norms that influence the ability of women entrepreneurs to hire workers and is very important in the context of India. More research and better data are required to better understand the underlying reasons for the observed gap in performance between male-run and female-run firms, and their relative importance in influencing this gap.

Firm size by sector and ownership. Source: Authors’ estimates

Average labour productivity by sector and ownership. Source: Authors’ estimates

5 Location, Firm Size and Productivity

Does the choice of businesses influence their size and productivity? It is commonly believed that working from home detracts from doing business and hiring workers, lowering firm efficiency and the number of hours a firm normally operates (Amin 2010). In our data set, a majority of firms operate from within the household (72 per cent of firms in our data set), and also without fixed premises and permanent structures. It is argued that firms with fixed premises and permanent structures are likely to be more productive than those working out of temporary structures or Mobile-Street Vendors (Moreno-Monroy et al. 2014). Investment in permanent structures is expected to remove the uncertainty associated with temporary structures from, say, demolition by state agencies or the need to move from place to place in the case of mobile street vendors. Such uncertainties involved in businesses are likely to influence firm size and productivity. The analysis that we carry out next proposes to shed light on these conjectures.

To look at the relationship between location of firm, firm size and productivity, we classify firms into different categories based on the location of the firm. Four categories are defined: (a) firms operating from within the household (Within HH); (b) firms located outside the household premises and own fixed premises and permanent structures (OH-PERM); (c) firms located outside the household premises but have only temporary structures (OH-TEMP); and (d) firms that shift from market to market and street vendors (Mobile-Street Vendors). There is enough evidence in support of the role location plays in influencing firm size (Fig. 2.12). Our findings firmly point to considerable differences in size between firms operating from inside the household premises and those outside the household premises. The average firm size is substantially higher for enterprises that are located outside the household premises and carry out their operation (OH-PERM and OH-TEMP) as opposed to firms that operate from within the household (WithinHH). This is evident across all enterprise types and more apparent among the DMEs. For instance, a DME in the OH-PERM category is 1.25 times larger than a DME in the WithinHH category. However, compared to Mobile-Street Vendors, an average firm in the WithinHH category is substantially bigger in size in all three enterprise types.

Firm size by enterprise type and location. Source: Authors’ estimates

Next, we look at the role of location on firm productivity. The evidence that we draw from our analysis produces a mixed result on the relationship between location of the firm and firm productivity. On the one hand, there is enough evidence to suggest that firms that are bigger in size have derived significant productivity gains vis-à-vis small firms (Fig. 2.13). As anticipated, we also find that the firms that are located outside the household premises and owned fixed premises and permanent structures (OH-PERM) are the most productive ones among all the four categories of firms that were identified based on location. The average productivity of OH-PERM category in the OAME, NDME and DME enterprise types is 2.4 times, 1.7 times and 3.6 times higher than the least productive categories, respectively. However, to our surprise, the other category of firms that are located outside the household premises but operating from fixed premises and temporary structures (OH-TEMP) turned out to be the least productive firms. Does this imply that even if the firms operate from outside home, having fixed premises and permanent structure are essential for improving growth and productivity? Our findings fail to confirm this either, as the Mobile-Street Vendors where most firms are without fixed premises, are found to be the second-most productive category of firms across all the three enterprise types. To sum up, our conjecture that working within household premises would have detrimental effects on firm growth and productivity is not upheld. Further research may be required to establish the economic benefits of the location choice of small businesses in the informal sector.

Average labour productivity by enterprise type and location. Source: Authors’ estimates

We have also investigated whether the effect of location choice of businesses on firm size and productivity is different for rural and urban firms. When we look at the role of location choice on firm size, we fail to detect a clear pattern across the location categories (Fig. 2.14). While urban firms are larger in size in OH-PERM and WithinHH categories, it is the rural firms that are larger in size in OH-TEMP and Mobile-Street Vendors categories. We also notice that urban firms in the OH-PERM category and rural firms in the OH-TEMP category are the largest in terms of size. But when it comes to productivity, a clear pattern is discernible (Fig. 2.15). In all categories, urban firms are more productive than rural firms. As observed for the overall sector, firms in OH-PERM are the most productive ones in rural and urban areas, followed by firms in Mobile-Street Vendors category. Hence, our surmise that working from home is likely to have negative implications on growth and productivity is not confirmed.

Firm size by sector and location. Source: Authors’ estimates

Average labour productivity by sector and location. Source: Authors’ estimates

6 Sources of Funds

We now look at the sources of external funds for firms in the informal sector. An important feature of the changing financial landscape in India has been the decline in the importance of informal sources of finance over time, which fell from 70.8 per cent in 1971 to 39.6 per cent in 1991 as a share of total debt (Tsai 2004). This has been a consequence of the government requirement to banks to lend to small enterprises and agricultural households as well as the mandated branch expansion policy where the Reserve Bank of India required banks to open branches in under-banked rural and semi-urban areas.Footnote 4 Evidence presented in Table 2.5 also shows that there is less reliance on informal sources of finance by firms in the informal sector, and external funds sourced through institutional agencies appeared as the most common source of finance. In 2015–16, more than half of all loans to OAMEs were derived from institutional agencies, and the corresponding figure for NDMEs and DMEs was 73.2 per cent and 76.9 per cent, respectively (Table 2.3). Among the institutional sources, a major chunk of borrowing came from commercial banks. Though lesser in magnitude, money lenders still formed an important source of finance for firms in the informal sector, especially for OAMEs. About 22.4 per cent of total borrowings by the OAMEs came from money lenders. Firms have also sourced their finance through friends and relatives; however, the major beneficiary of finance originated through this source was OAMEs. Almost one-fifth of the borrowings for the OAMEs were derived from friends and relatives. On the whole, it can be seen that a significant proportion of external funds for informal firms originated from term-lending institutions such as commercial banks and other institutional agencies.

7 Capital Intensity and Firm Size

It is argued that the scope for using labour-saving machinery increases with size (Creamer and Bernstein 1954). We examine this in the context of informal firms in India. The evidence available to us supports this argument as we find that the amount of capital employed per unit of labour input increases with the size of the firm. Capital intensity is the highest for DMEs, followed by the NDMEs and the OAMEs (Fig. 2.16). Compared to OAMEs, the capital-labour ratio is 2.2 times higher in the NDMEs and 2.6 times higher in the DMEs in 2015–16. While the OAMEs experienced a 3.3 times increase in capital-labour ratio between 2000–01 and 2015–16, the corresponding increase in the NDMEs and the DMEs were 2.4 times and 2.6 times, respectively. Our analysis yields new insights into the relationship between size and capital intensity when we present the capital-labour ratio for different size classes using a histogram (Fig. 2.17). We find that the relationship between size and capital intensity follows an inverse U-shaped curve. Capital intensity does increase with firm size, but only up to a certain size threshold: beyond it, the capital intensity tends to decline. As is evident from Fig. 2.17, the capital-labour ratio displayed a steady progression up to the 10–15-size category and then declined. What may explain this puzzling relationship between size and labour intensity? We conjecture that as firms become larger in size and come close to the threshold size that would necessitate their registration with the formal authorities under the Factories Act, they are less keen to invest in fixed assets that they would need to do if they wanted to make the transition to the formal sector. We also examine the intensity separately for two components of fixed capital investment: investment in plant and machinery and investment in land and buildings. Our results show that DMEs are more intensive in plant and machinery (Fig. 2.18) and NDMEs more intensive in structure investment (Fig. 2.19). A detailed scrutiny of both components using histograms, however, mirrors the findings observed for overall intensity: rise in intensity up to the 10–15-size category and a decline thereafter. An interesting finding that emerges from the disaggregated analysis is that the share of investment in plant and machinery to total fixed capital investment is considerably lower for firms in the borderline categories as compared to other size categories and to their corresponding share in land and buildings.Footnote 5 This finding is in line with our conjecture that firms that are close to the threshold of size defined by the Factories Act are less likely to invest in costly plant and machinery as they are reluctant to make the transition to the formal sector, possibly due to the large costs of monitoring in the latter sector which they would like to avoid.

Capital-labour ratio by enterprise type and year (in 00s). Source: Authors’ estimates

Capital intensity by size groups in informal sector firms (in 00s). Source: Authors’ estimates

Mean plant and machinery to employment by enterprise type (in 00s). Source: Authors’ estimates

Mean land and building to employment by enterprise type (in 00s). Source: Authors’ estimates

8 Age, Size and Productivity

Do informal firms in India increase in size and become more productive as they grow older? The existing evidence for other countries suggests a negative relationship between age and growth (Sleuwaegen and Goedhuys 2002). Some studies have also found an inverse U-shaped relationship between age and productivity (Jensen et al. 2001; Van Biesebroeck 2005; Fernandes 2008). In the case of India, Deshpande and Sharma (2013) reported a negative association between age and firm growth. Using the latest two rounds of NSSO survey data, we test for the presence of relationship between firm age, firm size and productivity. The NSSO reports the year of initial operation of firms covered in their surveys. We exploit this information to compute firm age, which is defined as the number of years elapsed since the commencement of firm operation. Our findings fail to suggest any precise relationship between age of the enterprise and firm size. Given that the larger firms tend to survive longer, one would generally expect a positive relationship between the two and, hence, would see the average age increasing with firm size. In our case, the average age of the enterprise does not show any significant difference across enterprise types (Fig. 2.20). We explore this relationship further in Fig. 2.21 in a scatter diagram, where we capture the relationship between employment and age of the enterprise. The scatter plot, too, fails to suggest any precise relationship between age and size of the firm. We have also examined the role of age on productivity and capital intensity, and we found absence of any such relationship between firm age and productivity and capital intensity (Scatter Plots 2 and 3 in Fig. 2.21). As argued by Hsieh and Klenow (2014), this may stem from the barriers to productivity growth faced by large and old firms in India—such as “contractual frictions in hiring non-family labour, higher tax enforcement on larger firms, financial frictions, difficulty in buying land or obtaining skilled managers, and costs of shipping to distant markets”. However, more research is needed to precisely establish the reasons behind the absence of a relationship between firm age and productivity. Perhaps the distortions in the product and factor markets that large informal firms face could explain this lack of relationship.

Age by enterprise type. Source: Authors’ estimates

Relationship between age and firm size, productivity and capital intensity. Source: Authors’ estimations

9 Social Group of Firm Owner, Firm Size and Productivity

Recent years have seen a surge in studies that have attempted to relate the social group of the firm owner with size and productivity. Some studies have highlighted that enterprises owned by Scheduled Castes (SCs) and Scheduled Tribes (STs) are under-represented in the population of small and medium enterprises, and that these enterprises are smaller in size as compared to enterprises owned by other social groups (Deshpande and Sharma 2013; Iyer et al. 2013). The SCs and STs are also over-represented in occupations which have the highest rates of poverty (such as agricultural labour in rural areas and casual workers in urban areas), and there is mixed evidence on the degree of occupational mobility that these social groups have witnessed in recent years, especially in the post-reform period. For example, Hnatkovska et al. (2012) find significant convergence of occupation and wages of SC and ST groups towards non-SC/ST levels in the period 1983–2005, using quinquennial NSSO employment surveys. Similarly, Kapur et al. (2010) find clear mobility of SCs from being agricultural labourers to being owners of OAMEs using primary data from Uttar Pradesh. Gang et al. (2017) find evidence of occupational convergence among SCs towards non-SC/STs but not STs in rural areas. On the other hand, Newman and Thorat (2012) find social and economic discrimination significantly restricts the mobility of SCs, and their entry into ‘non-traditional’ occupations.

The recent NSSO surveys collected information on the social group of the owner of the informal firms, which enables us to investigate the firm size and productivity among the firms owned by entrepreneurs belonging to different social groups. Using this information from the NSSO data, we identified four categories of firms: (a) firms owned by those belonging to the general category (General); (b) firms owned by other backward classes (OBC); (c) firms owned by Scheduled Castes (SC); and firms owned by Scheduled Tribes (ST). We first examine whether there exist considerable differences in firm size across firms owned by various social groups. The results are in line with our expectations. Firms owned by general category, on average, employ more workers, followed by firms owned by OBCs, STs and SCs (Fig. 2.22). The size differential across social groups is more evident among the DMEs than in the OAMEs and the NDMEs. We notice more or less a similar pattern for labour productivity too. Firms owned by general social group category report the highest productivity levels, followed by firms owned by the OBCs, the SCs and the STs (Fig. 2.23). To sum up, the evidence points to the existence of clear divergence in size and productivity between the firms owned by different social groups, with the SCs (and STs, in the case of productivity) being the most disadvantaged, followed by the OBCs, while the firms owned by the general group (forward castes, along with non-Hindus) are the largest in size and the most productive. Our findings possibly point to the prevalence of social barriers to firm growth in informal manufacturing in India, which restrict the participation of socially disadvantaged groups in the growth process of the economy.

Firm size by enterprise type and caste. Source: Authors’ estimates

Labour productivity by enterprise type and caste. Source: Authors’ estimates

10 Education of Owner and Firm Size

Earlier studies on informal firms for other developing countries maintain that firms with educated owners tend to improve in size and productivity as compared to firms with less educated owners (Sonobe et al. 2011; Amin and Huang 2014). We examine this in the context of informal firms in India. To do this, we classify the firms into four categories based on the information available from the 62nd round of NSSO surveys on the unorganized manufacturing sector on the education level of the firm owners. The four categories are defined as follows: (a) firms owned by illiterates, (b) firms owned by entrepreneurs educated up to primary level, (c) firm owners who have an education up to higher secondary level, and (d) firm owners with post-graduation and above. If education indeed plays a positive role, one would expect firm size and productivity increasing with the level of education. Findings based on our analysis, however, do not produce any clear evidence on the positive role of education of firm owners on firm size (Fig. 2.24). Of course, we do find that average size is highest for firms which are owned by entrepreneurs with post-graduation and above. However, our results also show that the next category in terms of size is firms owned by illiterates. This pattern is visible across all enterprise types. On the other hand, we find that education is positively linked to productivity. When we relate educational qualification of the owner with labour productivity in Fig. 2.25, we find that labour productivity increases with levels of education. The productivity levels are higher for firms run by owners having a post-graduate degree and above, followed by firms where owners have education up to higher secondary level, those who have a primary education and at the bottom are those firms owned by illiterates. This suggests that human capital of the owner matters for firm productivity even in the informal sector, where the returns to education are likely to be low. Perhaps more surprisingly, returns to education also matter significantly for household enterprises, which are the least productive among the firms in the informal sector and employ most of the working poor in urban areas. Our findings perhaps point to the important role schooling might play in addressing the constraints to growth and productivity of all informal firms.

Firm size by education and enterprise type, 2005–06. Source: Authors’ estimates

Labour productivity by education and enterprise type, 2005–06. Source: Authors’ estimates

11 Wages, Firm Size and Productivity

How do wages paid to workers differ by the type of firm? Do wages differ by firm ownership and social group of the owner and are the most productive firms paying the highest wages? In this section, we put together some stylized facts about wages in the informal manufacturing sector and examine whether wages paid to workers differ by type of firm, firm ownership and social group of the owner. Our measure of wages here includes wages and salaries payable in cash or in kind, and it excludes the value of social security contributions paid by the employer.Footnote 6 We use real wages, which are obtained by deflating nominal wages with consumer price index (CPI) for industrial workers at 1993–94 prices, and use monthly wages per worker to make the comparisons across different types of enterprises. We find clear evidence that the DMEs pay higher monthly wages, followed by the NDMEs and then the OAMEs. Our computations suggest that the DMEs pay monthly wages 1.5 times higher than those paid by the NDMEs, and 1.2 times more than the monthly wages paid by the OAMEs. This may be explained by the fact that large firms demand a higher quality of labour, defined by observable characteristics such as education, job tenure and a higher fraction of full-time workers, and hence end up paying higher wages. It is also partly due to the higher productivity and stability of the workforce in large firms. Our findings thus show how important it is for firms to make the transition from OAMEs to DMEs so as to better the living conditions of the workers employed in these enterprises (Fig. 2.26).

Monthly wages per worker by enterprise type (average for 2010–11 to 2015–16). Source: Authors’ estimates

As expected, the wages paid by partnership firms are much higher than the wages paid by firms owned solely by female and male proprietors (Fig. 2.27). Between male and female proprietorship firms, the average monthly wages are higher in the male proprietorship firms. Recall here that the partnership firms and male proprietary firms are larger in size and more productive than the proprietary firms owned by the females. We find that, among the DMEs, firms owned by the General social group pay the highest wages, followed by firms owned by OBCs, firms owned by STs and firms owned by SCs (Fig. 2.28). This is not a surprising finding, as we have already observed that DMEs owned by the General group are the most productive. When it comes to the NDMEs, the correlation between wages paid and the social group of the owner is less apparent. In the case of NDMEs, firms owned by the OBCs pay the highest wages, followed by firms owned by the general social group, firms owned by the SCs and firms owned by the STs. In the case of OAMEs, we observe more or less similar pattern as observed for the DMEs, except that firms owned by the STs pay higher wages than those owned by the SCs. Finally, the scatter plots presented in Fig. 2.29 shows strong evidence supporting the positive relationship between wages paid to workers and firm productivity, and wages paid to workers and firm size. The relationship between wages and firm productivity is particularly strong, indicating the importance of improving firm productivity in the Indian informal sector as a means to improve the living standards of the workers employed.

Monthly wages per worker by ownership (average for 2010–11 to 2015–16). Source: Authors’ estimates

Monthly wages per worker by social group of the owner and enterprise type (average for 2010–11 to 2015–16). Source: Authors’ estimates

Wages per worker, labour productivity and firm size. Source: Authors’ estimations

12 Concluding Remarks

In this chapter, we present some stylized facts about firms in the Indian informal manufacturing sector, using the most recent unit record data from the NSSO surveys of unorganized enterprises. Our analysis suggests that important changes have occurred in the Indian informal manufacturing sector in the era of globalization. Our results point to a consistent but marginal decline in the size of an average firm in the Indian informal manufacturing sector over time. The decline is more evident among the OAMEs and the NDMEs, while the decline in the DMEs is confined to the last quinquennium of our study period. These changes are more marked for firms in the rural areas than in the urban areas. As regards labour productivity, there is an apparent inverted-U relationship between firm size and firm performance: labour productivity increases up to a certain size threshold and experiences a decline thereafter. Productivity is highest among firms that operate from fixed premises with permanent structures; however, the evidence is not decisive on the role of fixed premises and permanent structures on driving up productivity.

Our attempt to understand the relationship between size and capital intensity throws up an interesting finding: the share of investment in plant and machinery to total fixed capital investment is considerably lower for firms in the borderline categories as compared to other size categories and to their corresponding share in land and buildings. Our further examination on the correlates of wages and productivity identifies firm size, gender and social group of the firm owner and location of the firm as important determinants. We find enough evidence to deduce that the most effective way to increase the wages of informal workers is to increase the productivity of the enterprises they work in, and that the larger these enterprises are, the more productive they are. However, our findings also point to the existence of social and economic barriers to informal enterprises in increasing their productivity—we find that firms owned by members of disadvantaged social groups such as the SC and ST, and female-owned enterprises are less productive than those headed by other social groups and by males. This suggests that targeted policies towards enterprises owned by marginalized groups are necessary to create a more inclusive development pattern in the informal manufacturing sector.

The missing middle problem is clearly seen in our analysis of firm size distribution with the strong presence of both small and large firms, with a conspicuous ‘missing middle’, and the markedly larger productivity differentials between small and large firms. They suggest that creating an institutional environment aiding the upward progression of small firms can lead to substantial increase in the growth and productivity of overall manufacturing sector. Raj and Sen (forthcoming) show that most important sets of institutions are the ones that could be termed ‘predatory’ institutions—the corruption that mid-sized firms face in their day-to-day interactions with the state. Thus, there is more attention that needs to be given to discipline lower level bureaucrats who engage in petty corruption and to make government procedures more transparent and accountable so that there is less scope for corruption.

Notes

- 1.

The only exception is 2015–16 period, during which the firms’ productivity increased up to the 16–19-size category and then declined.

- 2.

We did not find much difference in the pattern over time hence prefer to present the average from 2010–11 to 2015–16 for the figures that follow.

- 3.

Note that information on other forms of ownership (such as public limited companies) is not available in the data sets.

- 4.

However, Sen and Ghosh (2005) note that the share of lending to small enterprises in total bank lending to priority sectors may have declined over time.

- 5.

For brevity, the histograms of intensity for these two components are not presented in the chapter but are available from authors upon request.

- 6.

The caveat here is that own account manufacturing Enterprises (OAMEs) mostly use family labour, so these include only wages and benefits for working owners.

References

Amin, Mohammad. 2010. “Gender and Informality.” Enterprise Note Series No.16. Washington, DC: The World Bank.

Amin, Mohammad, and Xie Huang. 2014. “Does Firm-size Matter in the Informal Sector?” Enterprise Note Series No.28. Washington, DC: The World Bank.

Creamer, Daniel, and Martin Bernstein. 1954. Capital and Output Trends in Manufacturing Industries, 1880–1948. Occasional Paper 41. Studies in Capital Formation and Financing. New York: National Bureau of Economic Research.

Daymard, Arnaud. 2015. Determinants of Female Entrepreneurship in India. OECD Economic Department Working Papers, No. 1191: 01–38. http://www.oecd.org/officialdocuments/publicdisplaydocumentpdf/?cote=ECO/WKP(2015)9&docLanguage=En. Accessed on June 12, 2018.

Deshpande, Ashwini, and Smriti Sharma. 2013. “Entrepreneurship or Survival? Caste and Gender of Small Business in India.” Economic and Political Weekly 28(28): 38–49.

Fernandes, Ana. 2008. “Firm Productivity in Bangladesh Manufacturing Industries.” World Development 36(10): 1725–1744.

Gang, Ira N., Kunal Sen, and Myeong-Su Yun. 2017. “Is Caste Destiny? Occupational Diversification among Dalits in Rural India.” European Journal of Development Research 29(2): 476–492.

Hnatkovska, Viktoria, Amartya Lahiri, and Sourabh Paul. 2012. “Castes and Labor Mobility.” American Economic Journal: Applied Economics 4(2): 274–307.

Hsieh, Chang-Tai, and Peter Klenow. 2014. “The Life Cycle of Plants in India and Mexico.” Quarterly Journal of Economics 129(3): 1035–1084.

Iyer, Lakshmi, Tarun Khanna, and Ashutosh Varshney. 2013. “Caste and Entrepreneurship in India.” Economic and Political Weekly 48(6): 52–60.

Jensen, J. Bradford, Robert H. McGuckin, and Kevin J. Stiroh. 2001. “The Impact of Vintage and Survival on Productivity: Evidence from Cohorts of U.S. Manufacturing Plants.” Review of Economics and Statistics 83(2): 323–332.

Kapur, Devesh, Chandra Bhan Prasad, Lant Pritchett, and Shyam Babu. 2010. “Rethinking Inequality in Uttar Pradesh in the Market Reform Era.” Economic and Political Weekly 46(35): 39–49.

Moreno-Monroy, Ana I., Janneke Pieters, and Abdul Azeez Erumban. 2014. “Formal Sector Subcontracting and Informal Sector employment in Indian manufacturing.” IZA Journal of Labor and Development 3(22): 1–17.

National Sample Survey Organisation (NSSO). 2002. “Unorganised Manufacturing Sector in India, 2000–2001.” National Sample Survey Office, Ministry of Statistics and Programme Implementation, Government of India, New Delhi.

Newman, Katherine, and Sukhadeo Thorat. 2012. Blocked by Caste: Economic Discrimination in Modern India. New Delhi: Oxford University Press.

Raj, Rajesh S.N., and Kunal Sen. 2016. Out of the Shadows? The Informal Manufacturing in Post-Reform India. New Delhi: Oxford University Press.

Raj, Rajesh S.N., and Kunal Sen. forthcoming. “The “Missing Middle” Problem in Indian Manufacturing: What Role Do Institutions Play? Economic and Political Weekly.

Sen, Sunanta, and Soumya Kanti Ghosh. 2005. “Basel Norms, Indian Banking Sector and Impact on Credit to SMEs and the Poor.” Economic and Political Weekly 40(12): 1167–1180.

Sleuwaegen, Leo, and Micheline Goedhuys. 2002. “Growth of Firms in Developing Countries, Evidence from Côte d’Ivoire.” Journal of Development Economics 68(1): 117–135.

Solon, Gary, Steven J. Haider, and Jeffrey M. Wooldridge. 2013. “What Are We Weighting for?” The Journal of Human Resources 50(2): 301–316.

Sonobe, Tetushi, John E. Akoten, and Keijiro Otsuka. 2011. “Growth Process of Informal Enterprises in Sub-Saharan Africa: A Case Study of a Jua Kali Cluster in Nairobi.” Small Business Economics 36(3): 323–335.

Tsai, Kellee S. 2004. “Imperfect Substitutes: The Local Political Economy of Informal Finance and Microfinance in Rural China and India.” World Development 32(9): 1487–1507.

Van Biesebroeck, Johannes. 2005. “Firm Size Matters: Growth and Productivity Growth in African Manufacturing.” Economic Development and Cultural Change 53(3): 545–583.

Author information

Authors and Affiliations

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2019 The Author(s)

About this chapter

Cite this chapter

Raj S. N., R., Sen, K. (2019). What Do We Know About Firms in the Informal Manufacturing Sector in India?. In: Shyam Sundar, K.R. (eds) Globalization, Labour Market Institutions, Processes and Policies in India. Palgrave Macmillan, Singapore. https://doi.org/10.1007/978-981-13-7111-0_2

Download citation

DOI: https://doi.org/10.1007/978-981-13-7111-0_2

Published:

Publisher Name: Palgrave Macmillan, Singapore

Print ISBN: 978-981-13-7110-3

Online ISBN: 978-981-13-7111-0

eBook Packages: Economics and FinanceEconomics and Finance (R0)