Abstract

The old age security system consists of three parts: pensions, endowment insurance and elderly care services. The pension system mainly includes public pensions (pillar 1), occupational pensions (pillar 2) and personal pensions (pillar 3). Among them, the public pensions, part of social endowment insurance, are financed on a pay-as-you-go basis and form the endowment system together with commercial endowment insurance. The occupational pensions and the personal pensions are actually designed for personal retirement savings purposes, which have no risk diversification mechanism among different enrollees, and therefore are not insurance. In China, the basic old age insurance (pillar 1) dominates the pension system, the enterprise (and occupational) annuities (pillar 2) develop slowly, and personal pensions (pillar 3) fail to come into shape. Other than that, China’s pension system is faced with problems such as a severe shortage of national pension assets reserve, imbalanced development of pension system, and enormous financing pressure in the long run. Therefore, it is imminent for China to speed up the establishment of the personal pension account system. In the process of developing pillar 3, we must take China’s national conditions into full consideration, put personal accounts at the core, and construct a mature system framework based on three stages of account opening, operating and cashing. At the same time, supporting mechanisms, including automatic participation, emergency withdrawal, investment consultancy, and the 2nd-pillar and 3rd-pillar account merging mechanisms, should be established to complement personal pensions system. Furthermore, feasible measures should be explored to separate pension pools and individual accounts of the basic pension system, integrate personal accounts into pillar 3, rationalize and optimize the pension system structure so as to promote the sustainable development of the pension system in China.

Access provided by CONRICYT-eBooks. Download chapter PDF

Similar content being viewed by others

Keywords

- Personal pensions

- Account system

- Tax deferral

- Investment diversification

- Separation of social pools and individual accounts

1 Definition of Pension and Related Terms

According to the UN criterion, an ageing society is defined as a country or region in which greater than ten percent of the population is over sixty years old or greater than seven percent is over the age of sixty-five. In 2000, those aged above sixty accounted for 10.2% of China’s total population, marking China’s entry into the ranks of ageing societies. By the end of 2015, there were 222 million people over the age of sixty in China, accounting for 16.1% of the country’s total population. By 2020, China’s population over the age of sixty will increase to about 255 million, 17.8% of the total population. By 2030, China’s elderly population will exceed 350 million, 25% of the total population.

On the other hand, China is getting old very fast. It took the US 30 years (from 1942 to 1972) for the percentage of those aged sixty-five to grow from seven percent to ten percent of the total population. In China, this process took fourteen years (2000–2014). With respect to development trend, China and the rest of the world simultaneously entered an ageing society in 2000. By 2050, population aged sixty-five and over will reach 30.81% in China, which is close to the expected 32.03% in developed countries while the world average is expected to stand at only 19.7%. In other words, in fifty years, our country will catch up with the degree of ageing in developed countries, which is bound to pose a great challenge for China’s pension system. Therefore, we must seize the time to improve the pension system when China is still able to maintain rapid economic growth and before the elderly population reaches its peak.

However, Chinese people have different understandings of old age security, pensions and endowment insurances in China. The theoretical definition of a concept is the basic premise for system design and policy making. The current misunderstandings and confusion about related concepts have affected the reforms and further development of systems related to old age security. As a result, it is necessary to define related concepts in order to lay a solid foundation for policy making.

1.1 Definitions of Old Age Security, Pension and Endowment Insurance

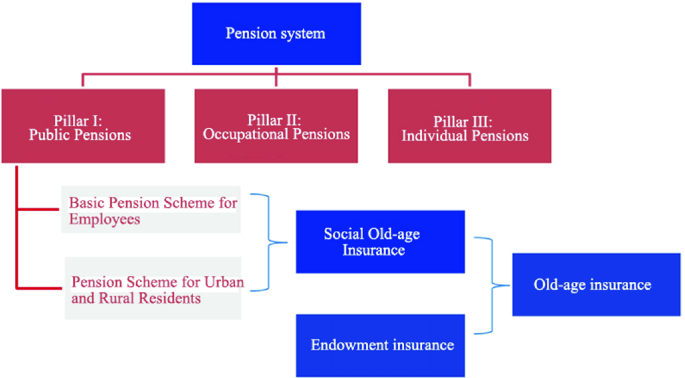

Old age security system refers to a comprehensive institutional arrangement covering pension money saving, diversification of old age risks, elderly care and other related fields, made by an economy to meet the various pension demands of the elderly. An old age security system consists of pensions, commercial insurance and elderly care services. Among them, the pension system aims to accumulate assets for old age care, the commercial insurance is designed to help prevent long-life risks, and elderly care services are to provide non-material support to the elderly. For its framework, see Fig. 5.1.

Relationships between old age security system and related concepts

Pension system refers to an institutional arrangement made by a state or society to provide economic support for citizens and help them maintain a reasonable standard of living after retirement through income redistribution or savings. The three-pillar system, consisting of the public pensions, occupational pensions and personal pensions, proposed by the World Bank in the 1990s has been widely adopted across the world for pension reform. In 2005, the World Bank expanded the three-pillar framework into a five-pillar framework by adding Pillar Zero which is a non-contributory, publicly financed and managed system that tackles retirement poverty and the 4th pillar of non-institutionalized solutions like informal support (family support, etc.). However, judging from the general international trend of pension development, the three pillars that assign pension responsibility to the government, employers and individuals still remain the core of modern pension systems.

Endowment insurance system Endowment insurance refers to institutional arrangements designed based on the law of large numbers and the principle of risk diversification to provide economic compensation for elderly members of a society to help them prevent and respond to age-related risks. An endowment insurance system consists of two parts: social endowment insurance and commercial endowment insurance, of which public pensions of the pension system belongs to social endowment insurance, and commercial endowment insurance is an insurance product provided by commercial entities to protect social members from age-related risks.

1.2 Distinctions and Correlations Between Old Age Security, Pension and Old Endowment Insurance

-

(1)

An old age security system is a more comprehensive institutional arrangement than an old age insurance or pension system. It covers a more comprehensive and systematic package of arrangements of materials and services while pension and old age insurance systems focus on providing financial and material security for citizens. Improving pension and old age insurance systems can provide good economic support for the old age security system.

-

(2)

Commercial endowment insurance serves as an important supplement to the pension system, but it is not part of the system. Firstly, the concept of pension is introduced from western countries. In English-speaking countries, a pension system (not endowment insurance system) consists of public pension, occupational pension and individual pension. Secondly, the key function of the pension system is to accumulate pension assets while that of commercial endowment insurance is risk diversification, which demonstrates the stark differences of the purposes of two systems. Thirdly, the responsibility and involvement of the government is much more prominent and deeper in the pension system. The government finance and run the pillar 1, and regulate and provide tax incentives for the pillar 2 and pillar 3. In comparison, the government’s involvement in the commercial endowment insurance industry is much less since it is only responsible for regulating market behavior in the industry.

-

(3)

Despite differences, the pension system and the old age insurance system are related. In the pension system, the public pensions are financed on a pay-as-you-go basis. They are in essence insurance that provides mutual aid to members of society, such as China’s pay-as-you-go basic pension scheme for urban employees. Therefore, public pensions (pillar 1 of the pension system), together with endowment insurance, form the old age insurance system. However, the accumulative occupational pensions and personal pensions are personal retirement savings of individuals. They are part of the pension system but not insurance. For the distinctions and relationships between the pension system and the old age insurance system, see Fig. 5.2.

Fig. 5.2

Distinctions and relationships between the pension system and the old age insurance system

2 Urgency for Developing Pillar 3 Personal Pensions

2.1 Problems and Challenges Faced by China’s Pension System

-

(1)

China’s pension reserve is severely insufficient, exerting grave challenges to provide for the aged

Globally, with the ageing population growing larger and larger, countries across the world have taken precautions and attached great importance to accumulate pension assets. Global Pension Assets Study 2017 shows that the size of global pension assets increased from USD 26.50 trillion in 2010 to USD 36.44 trillion in 2016. The growth rate of pension assets is also higher than the GDP growth rate. During 2010–2016, the global average annual growth rate of pension assets was 5.45%, while the average annual GDP growth rate was 2.39%. In comparison, by the end of 2016, the total size of China’s pension assets, including basic pension, enterprise annuities and social security funds, stood at about RMB 6.8 trillion, accounting for less than 10% of China’s total GDP, which was RMB 74 trillion in 2016. On the other hand, China has the world’s largest population, which means the per capita pension assets are seriously insufficient and China’s pension system will face great challenges in the long run.

-

(2)

There is a growing gap between the contributions flowing into Pillar 1 and the benefits flowing out of it, creating a massive payment pressure in the long run

With respect to the size of China’s basic pension assets, taking out the factor of government subsidies, the annual gap between revenue and payout of China’s basic endowment insurance reached RMB 65.2 billion in 2014. Since then, the gap has been widening. In 2016, the gap reached RMB 435.4 billion and the system reported an annual surplus of RMB 0.3 trillion thanks to RMB 651.1 billion worth of government subsidies and an accumulated surplus of RMB 3.86 trillion. However, the number of payable months dropped from 19.7 months in 2012 to 17 months in 2016, reflecting the potential financing pressure on the basic pension fund in the future. Most scholars believe that China’s pension system will face a huge financing gap in the long run due to rapid population ageing and inadequate system design. A study conducted by Boyuan Foundation in 2012 shows that, by 2033, China’s pension gap will account for 38.7% of its GDP of that year; in 2050, that number will register 75% of that year’s GDP.

-

(3)

Pillar 2 occupational pensions only cover a small number of people and their role in supplementing the pillar 2 is thus limited

At present, occupational pensions in China include enterprise annuities for employees in urban enterprises and occupational annuities for employees from the public sector. Enterprise annuities were introduced in 2004, marked by the promulgation of The Trial Measures for Enterprise Annuities. An enterprise annuity is an accumulative fund contributed by an enterprise (employer) and its employees. After more than a decade of development, the pillar 2 has improved significantly but still has many problems. First of all, its size of assets remains insufficient. At present, the total amount of occupational pension funds represented more than 50% of GDP in 35 OECD member countries and less than 2% in China. Secondly, the pillar 2 only covers a small number of people. Most Chinese enterprises have not set up an enterprise annuity mechanism. That is why the aggregate size of occupational pension assets is rather small. According to the Report on China’s Enterprise Annuity Funds 2016 released by the Ministry of Human Resources and Social Security, by the end of 2016, only 76,300 enterprises in the country have set up an enterprise annuity and 23,247,500 employees were enrolled in the enterprise annuity system. Thirdly, the development of enterprise annuities is unbalanced. The development of enterprise annuities in the eastern part of China is faster than that in the central and western regions. The development of enterprise annuities among state-owned enterprises and foreign-funded enterprises with better economic returns is faster than that of private enterprises.

Occupational annuities are established for government employees to make up for the decline in the basic pension benefits after the merging of the dual tracks. Occupational annuities are accumulative pension funds contributed by employers and employees as well. The system of occupational annuities for employees of government agencies and public institutions came into force on October 1, 2014, making the sizes of it relatively small too. In the long run, occupational annuities can only cover over 30 million employees of government agencies at most, which means occupational annuities and enterprise annuities (pillar 2) will cover about 60 million people, accounting for only 17% of the population from the basic pension for urban employees in 2pillar 1. Such small coverage limited its role in supporting pillar 1.

-

(4)

Pillar 3 personal pensions have received wide attention but related policy has not been developed

Early in 1991, China has proposed the idea of “gradually building an endowment insurance system consisting of basic endowment insurance, supplementary enterprise endowment insurance and personal savings.” This was the first time that 2pillar 3 was brought to the public’s attention in China. However, since the positioning of the pillar 3 remains unclear, no actual policy at the national level has been rolled out, only some relevant ministries and local governments have made some follow-up explorations. In 2007, Tianjin Binhai New Area attempted to carry out a program that allows up to 30% of an individual’s pre-tax salary paid for premiums of commercial endowment insurance products. However, the program failed eventually due to various reasons. In 2009, Shanghai proposed a pilot project to promote for-profit products of personal tax-deferred pension. In 2015, the Outline of the 13th Five-Year Plan proposed to “introduce tax-deferred pension” in which the word “for-profit” was deleted. The 13th Five-Year Plan of the Ministry of Human Resources and Social Security issued in July 2016 interpreted the concept as “the introduction to personal tax-deferred pension.” During the 2017 annual parliamentary sessions of China, dubbed as “two sessions”, the Ministry of Finance required that relevant departments conduct in-depth studies on policies and technical issues related to pillar 3 and rolled out relevant policy proposals.

2.2 Significance of Establishing and Improving Personal Pension System (Pillar 3)

China has already established a basic pension system (pillar 1) and an enterprise (and occupational) annuity system (pillar 2). However, the percentage of the pillar 1 assets to the aggregate assets in China’s entire pension system is too high. As the main provider for the aged, its replacement rate has maintained at about 45%, a relatively low protection for the elderly without the support from pillar 2 and pillar 3. On the other hand, the basic pension funds in the three northeastern provinces have already failed to meet the needs of their pensioners and many more provinces are expected to face the same fate in the future. As a result, it is imperative to improve the fairness and financial sustainability of the pension system. One of the key solutions is to build the pillar 3 as soon as possible to complement and upgrade the pension system.

-

(1)

Pillar 1 alone is unable to deal with pension crisis brought about by population ageing

Since China became an ageing society in 2000, its population ageing has gradually picked up pace. Judging from the trend of development, population ageing will dwell in China for a long period of time, reaching its peak around 2060 and then begin to decline. However, the total amount of elderly people will not drop with the decline of the total population, instead, the proportion of the elderly population aged 65 and above will remain relatively high (about 33%) for a considerable period till the end of the 21st century and the trend is irreversible (see Fig. 5.3).

Source United Nations, Department of Economic and Social Affairs, Population Division (2015). World Population Prospects: The 2015 Revision, custom data acquired via website

Changes in the population aged 65 and over in china and its proportion to the total population during 1950–2100.

The above demographic changes mean that the current dependency ratio of the existing pension system in our country will also continue to increase. In other words, the proportion of those who receive pension benefits will continue to increase while the proportion of those who contribute to the pension system will continue to decrease. If the existing pension system remains unchanged, China’s pension system will face a huge financing gap. Based on reform experience of the developed countries, most countries that have succeeded in achieving fairness, adequacy and sustainability in pension systems have mostly implemented a multi-pillar system that provides diversified pension benefits for their citizens. Pillar 2 and pillar that assign pension responsibility to employers and individuals play an increasingly important role during the reform. Pension systems rely solely on pillar 1 such as the pension system in Greece are unsustainable and have also led to sovereign debt crisis, proving that single-pillar pension system cannot cope with multifaceted challenges posed by demographic, economic and social changes.

-

(2)

Pillar 3 plays a bigger role than Pillar 2 in improving the pension system

The purpose of developing pillar 2 and pillar 3 is to perfect the pension system and split pension responsibility among the state, employers and individuals. However, after more than one decade of development, the enterprise annuities have failed to serve as an adequate supplement to the basic pension system in China. This is because pillar 2 is established by employers, and due to long-term excess of labor force, most enterprises are not motivated to establish enterprise annuities. Especially in recent years, as economic growth slows down and corporate profitability declines, the growth of enterprise annuities has been stagnant as well. By the end of 2016, only 844 new enterprise annuities were set up, up by only 1%. The number of employees enrolled in the new enterprise annuities stood at 85,300, merely up by 0.37%. Occupational annuities are designed only for over 30 million employees in government agencies. On the whole, the supplementary role of pillar 2 is very limited. In regard to pillar 3 personal tax-deferred pensions, employers’ voluntary participation and initiation is not required in that the government provides direct tax incentives to encourage individual participation. Thus, it is expected to cover a wide range of people and play a great role in China’s pension system by helping improving the system and reducing the financial burden on public pensions.

-

(3)

Pillar 3 can strengthen China’s ability to provide old age security and decrease financial burden on the government

The greatest driving force for pillar 3 is strong tax incentives provided by the government. In the United States, for example, up to about 12–15% of the average salary paid by individuals for premiums of pillar 3 can be exempted from personal income taxes. Such huge tax reduction greatly motivates individuals to accumulate pension assets during employment. Furthermore, reasonable and market-oriented investment and operation of pension funds which may last for several decades can preserve and increase their value; thus increasing the source of income for the aged and helping reduce the pressure on public pensions and the government.

-

(4)

Pillar 3 can help optimize the structure of the financial system and stabilize capital markets in China

For a long time, due to the imperfect pension system and the lack of the third pillar, part of the national financial assets aimed at providing for the aged are invested in bank deposits and financing, which does not help China’s financial structural adjustment that strives to “reduce indirect financing and increase direct financing.” The financial system is seriously under-performing in converting savings into real investment. In the meanwhile, the government has no choice but obtaining low earnings that are below the average rate of return on investment in China. Apart from that, some pension fund assets will flow into the stock market disorderly through retail investors to capture short-term spread. These investors tend to hold winners and sell losers. As a result, the long-term attribute of pension money is not fully utilized and the flow of pension fund assets into the capital markets in this manner will also cause violent fluctuations in the capital market, which is unfavorable to the sustainability of pension funds. Setting up pillar 3 can separate the investment of pension funds from personal banking and stock investment and generate reasonable returns through specialized asset management institutions in the capital market, thus supporting the development of the real economy more effectively.

3 Positioning of Pillar 3 in China’s Pension System

3.1 Improving the Structure of China’s Pension System and Splitting Pension Responsibility Among the Government, Employers and Individuals

In 1991, the Decision of the State Council on the Reform of Enterprise Pension System proposed that China should gradually build an endowment insurance system consisting of basic endowment insurance, supplementary enterprise endowment insurance and personal savings and split pension responsibility among the government, employers and individuals. After several years of reform and practices, the government-financed basic pension system has significantly improved and the employer-financed occupational pension system has been established. However, privately-financed pillar 3 has not come into shape in China, which is not conducive to motivating citizens to save for retirement. Establishing and improving the pillar 3 is one of the important tasks in the overall strategy aimed to perfect the structure of China’s pension system and roll out a system that splits pension responsibility among the government, employers and individuals.

3.2 Motivating Individuals Through Preferential Taxation to Reserve Personal Pensions to Raise the Total Amount of Pensions

The primary objective of the pillar 3 is to further expand sources of income for the elderly and improve their self-supporting ability. Personal pensions are voluntary and accumulative, and they maintain and increase value through market-oriented investment. International experience shows that the most effective incentive for voluntary pensions is tax deferral. China should also issue an effective and powerful deferred taxation policy to increase the attractiveness of personal pensions and expand the coverage of pillar 3, especially among the vast number of employees who are not covered by enterprise annuities or occupational annuities, as well as self-employed persons with certain income. Expanding the coverage of pillar 3 can increase self-protection capability of enrollees and offer another source of income for the elderly in addition to basic endowment insurance.

3.3 Creating Supplementary Pension Accounts to Protect Enrollees’ Rights and Interests

So far, the transfer of basic pensions in China has been normalized. However, enrollees of pillar 2 may face pension transfer problems when they change jobs. In pillar 2, enterprise annuities are voluntarily established by corporate employers while occupational annuities, designed for employees from government institutions, are mandatory in nature. When an employee moves from an enterprise which has an occupational pension to a place without any occupational pension, the fund in his/her occupational pension account cannot be transferred, thus affecting the rights and interests of the insured. Concentrating on individuals themselves, pillar 3 opens personal pension accounts base on an individual’s own will. When a participant changes jobs or retires, he/she can transfer the fund in pillar 2 to his/her personal pension account of pillar 3, which is also a common practice across the world. Using the third pillar as the centralized account for supplementary pensions can increase the convenience of supplementary pensions and better protect the rights and interests of the enrollees.

3.4 Encouraging Long-Term Retirement Savings and Following Short-Term Capital Needs of Citizens

The third pillar of personal pensions is mainly designed through institutionalized rules to encourage individuals to start early in life, according to their own circumstances, sketch pension plans and provide sufficient economic support for themselves after retirement. Such pensions are accumulative and voluntarily contributed by individuals, and the pension assets are also owned by individuals. On the other hand, enrollees of pillar 3 do not have any need for pension benefits until retirement. The fund in their personal accounts gradually accumulates during their several decades of employment. In this accumulation process, they may have emergency capital needs, such as large emergency medical expenses, first-time home purchase, and children’s education. To meet the above capital needs and increase the attractiveness and flexibility of the system, Pillar 3 often allows individuals to apply for temporary withdrawal of pension assets accumulated in their personal accounts under special circumstances and repay the pensions withdrawn within a specified period. This mechanism takes into consideration both long-term pension accumulation and citizens’ short-term capital needs, making it a citizens’ personal pension account with comprehensive support functions.

4 Three Key Factors of the System Design for Pillar 3

Many countries in the world have established a multi-pillar pension system, among which the plan that the government provides tax incentives to encourage citizens to participate in the voluntary pillar 3 has grown rapidly and caught worldwide attention. Among them, the United States boasts the most well-developed and advanced pillar 3 in the world. As of the end of 2016, the pillar 3 assets in the United States reached USD 7.9 trillion, accounting for 30.3% of the assets in the three-pillar system, 2.8 times that of Pillar 1. Evolved after a series of reform, In the UK and Australia Pillar III has also been growing and evolving, albeit in different ways that are unique to each country. International experience shows that tax incentives, the account-based institutional framework, and investment diversification are the three key factors that affect the stability and growth of pillar 3.

4.1 Tax Deferral Is the Key Driving Force for Pillar 3 Development

(1) The principle of designing tax deferral mechanism is that it must ensure that the tax burden in the withdrawal stage should be smaller than the sum of tax concessions in the contribution and investment stages. Pillar 3 in most foreign countries follows the above principle. Although the tax rate of IRA withdrawals in the United States can reach as high as 20%, it is lower than the total tax burden on each individual in the contribution and investment stages. Therefore, tax incentives of Pillar 3 are attractive to most American citizens. American citizens are required to pay federal and state personal income tax during the contribution period and the minimum tax rate of federal personal income alone is as high as 15%. In the UK, the minimum tax rate of Pillar 3 is 20% during the contribution period, 25% of the pension during the withdrawal period is tax-free, and taxes will be deducted from the remaining part based on the personal income tax rate. Because the total amount of tax paid by enrollees in the withdrawal stage is significantly smaller than the sum of previous tax concessions, citizens are greatly motivated to participate in personal pension schemes.

-

(2) When designing a tax incentive program, it is more effective to make pension contributions tax-free up to a specific limit rather than offering tax deduction on a pro rata basis. Under such design, all enrollees are entitled to the same amount of tax concession regardless of the level of income. This kind of design is more suitable for pillar 3 because personal pensions, as part of the pension system, must balance incentives with fairness. If tax incentives are calculated at a specific percentage of earnings of enrollees, higher income earners will receive greater tax concessions, which will not be conducive to the income redistribution function of the social security system. As mentioned earlier, the tax deferral limit of pillar 3 in the U.S. is between USD 5500–6500 and the deferral limit of 401(k) plans is USD 17,500 per year. The aggregate deferral limit of pillar 3 and 401(k) reached over USD 25,000, which is nearly one half of the average annual salary of American people. In China, only four percent of salary contributed to enterprise annuities is exempted from personal income tax, a quite upsetting number for tax concessions, and another preferential tax policy allows citizens to pay a maximum RMB 200 a month from their pre-tax income to buy designated commercial health insurance products, which is barely satisfactory and less effective than expected too. Therefore, given the large scale of the national pension expenditure, to effectively motivate citizens, the government should increase tax incentives for pillar 3. Thus, it is advisable to set the upper limit of personal income tax deferral for personal pensions at RMB 1000 per month and gradually increase the deferral limit according to the level of social and economic development. In addition, greater tax incentives may be provided for adults near retirement age. For example, the government may allow those aged over 50 to defer another 20% taxable income contributed to their personal pension accounts.

-

(3) The government may create a link between tax incentives for pillar 2 and pillar 3. China has introduced a tax concession policy for enterprise annuities. However, because enterprise annuities are discretionary in nature, some companies may not have set up an enterprise annuity, thus their employees cannot contribute to enterprise annuity even if they are motivated. From the perspective of developing supplementary pensions and alleviating the pressure of public pensions, the government may offer tax incentives for setting up enterprise annuities and personal pension accounts. More specifically, the government can offer tax incentives to those who are not included in an enterprise annuity plan to increase the appeal of pillar 3 and encourage citizens to save for retirement.

-

(4) Pension benefits may be taxed as regular income to encourage retirees to withdraw their pensions in installments. Generally speaking, enrollees are not encouraged to withdraw their pensions in one lump sum after retirement because they are tempted to spend too much within a short term, leaving them short of money down the line. Therefore, in most countries, a higher tax rate is set for lump-sum withdrawal. As for withdrawals in installment, the government may tax them as regular income and set a tax-free base and progress tax rates to encourage long-term payments. This is because, for enrollees who have just crossed the tax threshold in the contribution stage, their income tax rates are lower, meaning they receive relatively less favorable tax incentives. If there is no tax-free base, their tax payment may be greater than the tax concession they have received in the contribution stage. According to related studies, if the government allows RMB 1000 from every monthly withdrawal of personal pensions to be exempted from income tax and tax the remaining amount at progress income tax rates, the tax liability due on pension withdrawals of all enrollees will be lower than their tax concessions in the contribution stage, thus creating an incentive and a positive correlation between the tax rate in the withdrawal stage and that in the contribution stage, which means the higher your income is, the higher a tax rate you pay. Under such circumstances as overall moderate tax rates, not only does this design create adequate incentives for all enrollees, increasing the participation rate, but also offers preferential tax treatment to those with lower income. Such policy transfers income from the rich to the poor and is conducive to achieve equality in financing old age care.

4.2 Personal Accounts Are the Cornerstone of a Pillar 3 System

As the specific foundation of pillar 3 system, personal accounts refer to special real-name accounts set up for personal tax-deferred pensions. Activities related to tax incentives and deferred levies, investment selection and right records are all carried out based on them.

-

(1)

The necessity to adopt personal accounts system in China

First, a personal account system can effectively realize the value transfer of accumulated pension benefits. As we all know, the basic pension system and enterprise (occupational) annuities adopt a typical personal account system. Therefore, it is natural for personal tax-deferred pensions to adopt a personal account system. At the same time, the creation of pillar 3 personal pension accounts is subject to no restrictions while Pillar II occupational pension accounts must be created by employers. When an individual moves from an enterprise with an occupational pension scheme to an enterprise without an occupational pension scheme, his/her pension rights cannot be transferred through his/her Pillar II account. In such events, personal pension accounts can be used to collect pension rights transferred from Pillar II and improve institutional flexibility.

Secondly, a personal account system is conducive to clarifying the responsibilities of all stakeholders and increasing citizens’ awareness of self-providing after retirement. Pillar 3 adopts the trust-based governance structure under the personal account system, which can help clarify pension responsibilities of the government and individuals and alleviate citizens’ over-reliance on the state and their employers. At the same time, special personal pension accounts can cultivate citizen’s perception of pension responsibilities and increase their awareness and participation in the pension system, strengthening their ability to provide from themselves after retirement.

Thirdly, a personal account system can make personal income more transparent and improve the taxation mechanism. Tax deferral at the account level generally requires enrollees to declare income. On the one hand, it helps the tax authorities to keep track of the real income of enrollees to further improve the personal income taxation mechanism. On the other hand, an accurate understanding of the actual income level of enrollees can also help the government determine the social insurance contribution base, promoting the accuracy in distributing social insurance contributions and payments.

-

(2)

Suggestions for constructing personal account system of pillar 3 in China

First, the number of accounts. The comprehensive income taxation system is a widely adopted tax system across the world. An individual may open a personal pension account with a bank, mutual fund, insurance company or trustee. The account management agencies report citizens’ taxable income to the taxation authority so it can determine whether the total tax-free amount in all personal accounts of an individual has exceeded the specified cap. However, as China still implements a schedular system of taxation, the above method cannot be used to determine a specific tax concessional limit. Therefore, the Chinese government may consider setting up personal accounts based on citizens’ ID cards issued by the public security authorities. In that way, each citizen can only open a personal pension account to ensure the uniqueness of the account and facilitate tax deductions of an individual through one account.

Secondly, account custodians. To expand coverage, maximize the role of supplementary pensions, and provide a source of retirement income for citizens who are not covered by pillar 2, Pillar III personal pension accounts should allow for the voluntary participation of individuals. To this end, the account opening process should be convenient and flexible. Private pension funds may choose banks and securities agents as account custodians. On the one hand, banks and securities agents have many business outlets that can facilitate nationwide participation; on the other hand, banks and securities agents have extensive experience in account management and can handle big data efficiently.

Thirdly, the underlying account information platform. One of the key functions of a personal account system is to collect transaction information and levy personal income tax. China Securities Depository and Clearing Corporation Limited (CSDC) can serve as the underlying data recording and exchange platform for Pillar III, because the account platform of CSDC can ensure the uniqueness of personal tax-deferred pension accounts and are easy to connect the tax administration authority’s information management system. CSDC also has other advantages. Firstly, as a basic service provider in the capital market, CSDC has 170 million active securities accounts and extensive experience in account management. It can not only reduce the cost for setting up a special personal tax-deferred pension but also ensure stable and efficient operation of the pension account platform. Secondly, the business network of CSDC covers the whole country and can support both pilot implementation or nationwide implementation of the personal account system. Thirdly, CSDC also enjoys natural advantage in retirement verification and identity verification, so it is more convenient to supervise accounts, search for information and conduct other services through its platform.

4.3 Pillar III Must Diversify Its Investment Portfolios

Pillar III is in essence personal savings for retirement by individuals based on their own pension needs and risk appetites and are discretionary in nature. Diversifying pension products can meet the needs of different groups of enrollees and exemplify the attractiveness and flexibility of Pillar III. The following are some suggestions to increase the diversity of pension products in China’s third pillar:

Firstly, pension products offered by banks, funds and insurance companies to finance old age care may be included in the selection range. Pillar 3 is an accumulation system which will last for several decades. The key to its effective operation is to preserve and increase pension value through rational investment. Pillar 3 has a wide range of enrollees whose risk appetites and income levels vary considerably. For example, risk-averse enrollees may prefer bank savings, funds that generate steady yields or insurance products that provides stable support. Younger enrollees with a certain level of risk tolerance may choose equity funds to increase fund value through long-term investment and improve their ability to ensure financial security at old age. If personal investment choices are limited to a particular product category, it will undoubtedly affect the maximization of the utility of personal pension assets.

Secondly, standards should be formulated for product entry into the market. On the one hand, pillar 3 aims to meet the needs of citizens to ensure financial security at old age and the financial products they invest should match the attributes of pensions. On the other hand, there a wide range of financial products provided by banks, funds and insurance industries. In the context of an underdeveloped third-party investment advisory services industry, the lack of a market entry system may lead to a mismatch between risk appetite of enrollees and risk characteristics of products or irrational investment. Therefore, it is suggested that a market entry system for the pillar 3 should be set up by the relevant authorities. All products intended for pillar 3 should be assessed before entering the market so that enrollees are entitled to choose from regulated products freely.

Thirdly, default investment vehicles should be designated. In international communities, the pillar 2 and pillar 3 s allow individuals to choose investments for their pension contributions. However, it is difficult for some enrollees to make appropriate investment choices due to lack of financial knowledge or laziness, that is why many countries have established a default investment mechanism. For example, the United States introduced the QDIA system for 401(k) plans in its second pillar in 2006. QDIAs include target-date funds (TDFs), target-risk funds (TRFs), managed accounts and portfolios similar to balanced funds. If a participant fails to provide affirmative investment direction, his or her choice will be defaulted into a QDIA. Considering that most Chinese citizens lack financial knowledge and competent investment vision and that China’s third-party investment advice services industry is underdeveloped, many default investment products should be designated in the design of individual-oriented Pillar 3. Individuals may choose default investments when opening their personal pension accounts. Then if a participant fails to decide on how to invest the money in his/her personal pension account within a specified period of time, the money will be defaulted into a qualified default investment product selected by participant. For specific default investment alternatives, we may draw experience from the United States and Hong Kong where they mainly promote target-date funds, target-risk funds and other solution-based products with distinctive attributes of financing old age care. Besides, wealth management and insurance products that are specifically designed for old age care by banks can be designated as default investments, too.

5 Framework and Supportive Mechanisms of Pillar 3

5.1 Framework of Pillar 3 Personal Pension System

Personal accounts system is the core of designing a pillar 3 personal pension system, thus an institutional framework should be created to support account opening, management and pension withdrawal.

Account Opening Stage: Citizens submit account opening information to qualified account management institutions (i.e., designated commercial banks or securities agents) to apply for an account. Account custodians exchange information with taxation authorities through the platform of CSDC and obtain approval for contribution limits from taxation authorities. Such accounts should be created with identification numbers of enrollees and each participant may only have one account. Enrollees can check their contribution, investment and other products information through this account.

Operation Stage: Securities, insurance and banking regulatory authorities should be responsible for reviewing funds, insurance, savings and wealth management products respectively, and design investment vehicles for financing old age care in a unified way. At the same time, a link should be created between designated investments and personal accounts so that enrollees may select among designated investment products based on their own risk appetites and needs. Meanwhile, a default investment vehicle system should be introduced for if enrollees fail to choose investment category on time, the money in their personal pension accounts will be defaulted into the default investment. Account custodians are responsible for submitting contribution, transaction and investment returns and other information to the system of CSDC in a timely manner. Apart from that, the information system of CSDC should be connected to the national tax information system so that taxation authorities can keep track of contributions, investment and returns of pension accounts, providing references for tax concession and deferral.

Withdrawal Stage: Based on the information from taxation authorities and CSDC’s deferred personal pension account, during the withdrawal stage, enrollees withdraw pension benefits from their personal pension accounts opened in banks or securities companies while taxation authorities withhold deferred income taxes on pension withdrawals based on relevant information.

5.2 Supportive Mechanisms

-

(1)

Cohesive mechanism between Pillar II and Pillar 3

Pillar 3 is based on a flexible personal account system consisting of independent personal accounts which can be easily transferred when a participant changes jobs. Occupational pensions (Pillar II) also adopt a personal account system but its establishment and function are only visible when sponsored by employers. When an employee moves from a company with an occupational pension scheme to another one without an occupational pension scheme, the pension assets in the employee’s Pillar II account cannot be transferred. In this regard, China may draw from the experience of other countries and create a cohesive mechanism between pillar 2 and pillar 3. In that way, when an individual changes jobs, his/her Pillar 3 personal pension account can be used to receive pension funds transferred from Pillar II, increasing the flexibility of pension system, which is also conducive to labor mobility.

-

(2)

Emergency borrowing mechanism

The purpose of personal pension accounts is to use tax deferral policies to encourage individuals to save and invest for retirement. In some special cases, personal pension accounts can also have other functions. For example, enrollees may be allowed to take an emergency loan from their personal pension accounts if the money is used to pay for health care, family education or a first-time home, which helps elevate the flexibility of pillar 3 personal pension. However, enrollees must comply with strict requirements to make emergency withdrawals and repay the borrowed money within a specified period of time. Should a participant fails to repay borrowed money in a timely manner, he/she will be subject to a penalty in addition to income tax.

-

(3)

Pension investment consultancy

The funds in pension accounts of pillar 3 account are long-term capital and should be invested in a reasonable manner to preserve and increase the value of pension assets. As China’s financial industry is still at an early development stage and most Chinese citizens have a relatively low level of financial literacy, professional investment consultants play an important role. Therefore, improving the general level investment advisory industry for enrollees to seek help from investment advisors when making decisions relating to investments.

-

(4)

Regulatory mechanism

Pillar 3 is an important institutional arrangement concerning the standard of living of citizens after retirement. The operation of the system involves many stakeholders and therefore must be supervised and regulated by different authorities. The implementation of contribution and benefit payment policies should be developed and supervised by human resources and social security authorities. As for taxation, the Ministry of Finance should be responsible for formulating preferential taxation policies for supplementary pensions. The State Administration of Taxation is responsible for reviewing qualifications and supervising and enforcing preferential tax policies. In this stage, the role of other financial regulatory bodies should be highlighted much more, so CBRC, CSRC, CIRC and other financial regulators should fully utilize their roles and shoulder the responsibility of supervising and regulating investments of pension assets.

6 Suggestions for Transferring Individual Accounts of the Basic Pension System to Pillar 3

6.1 Necessity of Separating Social Pools and Individual Account of the Basic Old Age Insurance System

-

(1)

The current system that combines social pools and individual accounts fails to achieve the goals of the pension reform

China’ current basic pension system combines social pools with individual accounts. The social pooling part is operated on a pay-as-you-go basis and redistributes income through transfers of funds among citizens. Funds in individual accounts are completely accumulative, which are designed to encourage enrollees to save for financing old age care. An efficient combination of social pools and individual accounts should be able to achieve inter-generational redistribution and provide incentives, reflecting the rule of combining collective mutuality and individual responsibility. However, since there is no specific institutional design for transformation reform costs and invisible debts, when the social pooling contributions are insufficient to pay current benefits, the Chinese government has to “borrow” from individual accounts to pay the benefits promised to current retirees. This is widely called the problem of “empty accounts.” This means, in reality, China’s basic pension system is operated on a pay-as-you-go basis and has failed to achieve the original goals of the pension reform.

-

(2)

“Empty accounts” severely affects the sustainability of China’s basic pension system

Due to accelerated population ageing and the continued increase in the number of retirees, the pay-as-you-go social pooling portion of the basic pension system is under increasing pressure. In recent years, because the social pooling contributions are insufficient to pay current benefits, the overwhelming majority of contributions to individual accounts have in fact been borrowed by the Chinese government to pay the benefits promised to current retirees. Although the government has been exploring ways to finance deficit in personal accounts, shortfalls in personal pension accounts continue to increase (see Table 5.1). By the end of 2015, the amount of money “borrowed” by the Chinese government from citizens’ personal basic pension accounts reached RMB 4387 billion. On the one hand, this “empty accounts” problem causes personal loss for individuals; on the other hand, the huge debt will put tremendous strain on future pension payments and become a major impediment to the sustainable development of the basic pensions system.

6.2 Rationale for Integrating Pillar 3 into the Personal Accounts of the Basic Old Age Insurance System

-

(1)

The ownership of both personal accounts of the basic old age insurance system and Pillar 3 vests in individuals

The fund in personal accounts of the basic old age insurance system is entirely contributed by employees and thus owned by employees. Personal pensions of pillar 3 are also private property, making the integration of two accounts possible and feasible. Furthermore, personal accounts from the basic old age insurance system are used only for employees after retirement and are in fact mandatory personal retirement savings, while pillar 3 is also in essence voluntary personal retirement savings. Therefore, the two can be integrated.

-

(2)

Pillar 3 can manage personal accounts of the basic old age insurance system

As mentioned earlier, it is imperative to separate personal accounts from the basic old age insurance system by transferring them to pillar 2 or pillar 3. Mainly sponsored by enterprises, occupational pensions can only cover a small number of people into the service of enterprise annuities and occupational annuities, about 60 million or so. Many employees are not covered by occupational pensions. Compared to pillar 2, the basic pension system has covered 380 million employees. If personal accounts of the basic old age insurance system are transferred to pillar 2, the majority of enrollees of pillar 1 will not have a pillar 2 account to receive pension benefits transferred from pillar 1 unless all companies are required to establish enterprise annuities, which is obviously unrealistic. In contrast, pillar 3 personal pensions are voluntary personal savings which are not sponsored by employers, meaning there are no institutional barriers to the transfer of personal accounts of the basic pension system from pillar 1 to pillar 3. In addition, if personal accounts of the basic pension system are merged to pillar 3 as a compulsory component, the number of enrollees covered by pillar 3 will increase by more than 300 million. The effect is similar to an automatic participation mechanism of supplementary pensions.

6.3 Key Suggestions for Transferring Personal Accounts of the Basic Old Age Insurance System to Pillar 3

-

(1)

Separate social pools with individual accounts after personal accounts are funded

In 2016, the total shortfall of personal accounts of China’s basic pension accounts exceeded RMB 4.7 trillion. If the current system of combining social pools and individual accounts remains unchanged, the shortfall will further increase. In particular, the new nominal rate formation mechanism for personal accounts introduced in 2017 links basic pension interest rates to salary growth. Under the new nominal rate mechanism, the nominal interest rate in 2016 reached as high as 8.31% while the GDP growth rate in the same year was only 6.7%. The actual rate of return on investment for corporate annuities and social security funds in 2016 was only 3.03 and 1.73% respectively. Obviously, the new mechanism will further increase the shortfall of personal accounts, putting further strain on basic pension system.

Therefore, it is necessary to fund personal accounts through various channels as soon as possible and separate the social pooling portion from individual accounts. An important way to make up the shortfall in personal accounts is to transfer state-owned assets to those personal accounts. At present, the market capitalization of Chinese state-owned companies listed in China and overseas markets exceeds RMB 20 trillion and the amount of funds required to make up the shortfall in individual accounts is less than RMB 5 trillion. In other words, this method is feasible. Moreover, transferring shares in state-owned firms to repay government debts is inherently reasonable and will not increase Chinese government’s current financial burden. It should be pointed out that after separating personal accounts from pillar 1, the social pooling contributions of the basic pension system may be insufficient to pay current benefits, compelling governments at all levels to fund and invest in social pooling contributions to head off the coming payment challenge.

-

(2)

Merge personal accounts of the basic old age insurance system into Pillar 3 as its mandatory component

Individual accounts separated from social pools of the basic old age insurance system may be merged into Pillar 3 as its mandatory component, whereas voluntary retirement savings serve as the voluntary component of Pillar 3. On the one hand, both personal accounts of the basic pension system and personal retirement savings of pillar 3 are private property, so it is feasible to merge accounts of the basic pension system into pillar 3 personal pension accounts. On the other hand, the transfer will quickly expand the coverage of pillar 3. Furthermore, the accumulative Pillar 3 after the merger will consist of a mandatory part and a voluntary part and the value of its assets can be preserved and increased through reasonable investment, thus increasing the ability of enrollees to ensure financial security at old age and reducing the government’s financial burden.

-

(3)

Implement existing tax exemption policy for personal accounts of the basic old age insurance system after the transfer

Since contributions to individual accounts of the basic old age insurance system are tax-free before the transfer, they should not take up the tax concession quota for personal retirement savings after they are incorporated into pillar 3. In addition, both pillar 2 and pillar 3 are private pensions. Pillar 2 is designed for employers with proper jobs and is generally given greater tax incentives than pillar 3. However, as indicated earlier, the number of people participating in enterprise annuities and occupational annuities in China is small. Therefore, tax concession quota of pillar 3 may be combined with tax credits of Pillar II. For those who have not participated in Pillar II or have not used up tax concession quota of Pillar II, their Pillar II tax concession quota or unused part thereof may be transferred to pillar 3 but the aggregate tax incentives not exceed the upper limit of tax incentives set for the two pillars. The purpose of such design is to encourage citizens to participate in personal pensions and promote the rapid development of Pillar 3.

References

Dong, K., and Yao, Y. (2016). Annual Report on the Development of China’s Financing Old Age Care (2016). Beijing: Social Sciences Academic Press (China).

Zheng, B. (2016). China Pension Report 2016—Deepening the Annuity Reform of Pillar II. Beijing: Economy & Management Publishing House.

The Investment Company Institute. (2017). ICI Fact Book 2017.

Department of the Treasury International Revenue Service: contributions to IRA & Distributions from IRA, 2015.

Author information

Authors and Affiliations

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2018 Social Sciences Academic Press and Springer Nature Singapore Pte Ltd.

About this chapter

Cite this chapter

Dong, K., Sun, B. (2018). Development Path of Pillar 3 Personal Pensions in China. In: Dong, K., Yao, Y. (eds) Annual Report on Financing Old Age Care in China (2017). Springer, Singapore. https://doi.org/10.1007/978-981-13-0968-7_5

Download citation

DOI: https://doi.org/10.1007/978-981-13-0968-7_5

Published:

Publisher Name: Springer, Singapore

Print ISBN: 978-981-13-0967-0

Online ISBN: 978-981-13-0968-7

eBook Packages: Economics and FinanceEconomics and Finance (R0)