Abstract

Agri-food firms, as enterprises in any other sector, have a series of tools at their disposition, based on international standards, which may be useful for the purposes of environmental management. System standards (such as ISO 14001 for Environmental Management Systems) are the most widely used, but a more suitable approach to environmental quality management in the agricultural and agri-food sectors is probably one based on using direct means of ensuring the environmental performance of products. In this chapter, new approaches centred on the product-orientation of environmental management systems are presented, also investigating their role in the improvement of economic and competitive performance. Finally, the path towards the definition of a Product-Orientation of Environmental Management Systems (POEMS) framework, specifically tailored to companies operating in the agribusiness sector, is described.

Sections 1.1, 1.2, 1.4, and 1.5 were written by Roberta Salomone and Giuseppe Saija, while Sect. 1.3 was written by Daniela Rupo.

Access provided by Autonomous University of Puebla. Download chapter PDF

Similar content being viewed by others

Keywords

1 Introduction: Management of the Environmental Variable in the Agri-Food Sector

In recent years, management of the environmental variable in the agri-food sector has been continuously expanding, mainly as a result of a few drivers raising companies’ awareness, such as the following:

-

the growing interest of the market in eco-sustainable agri-food products also connected to the awareness that the environmental impacts associated with the production and consumption of food and agricultural products are relevant; for example, the Environmental Impact of Products—EIPRO study (Tukker et al. 2006) conducted by the European Commission showed that among the products consumed in Europe, those which have the greatest environmental impacts, from a life cycle perspective, are foods and beverages, along with the private transport and the housing sector (buildings, furnishings, equipment, energy for residential use, etc.);

-

the need to increase the competitiveness of the food industry through the introduction of appropriate eco-innovations—indeed, even though the European food industry structure is particularly complex and articulated, with very different supply chains,Footnote 1 one element that connects all the different agri-food firms is the significant presence of SMEs, variously placed along the entire production chain, often competing in a globalised international market, heavily dominated by multinationals. For this reason, one of the target actions of the European Commission is to stimulate innovation (including eco-innovation) in SMEs, precisely in order to increase, in such a situation, the competitiveness of European enterprises. Additionally, in traditional sectors, such as the agri-food industry, margins of innovation may be more limited, and working on issues of environmental sustainability, including for example the introduction of organisational innovations, may be of strategic relevance;

-

the need to face this growing environmental awareness pushes agri-food companies to adequately manage all environmental impacts related to the processes and products included in the whole agri-food chain—consequently, these companies are called upon to govern the processes that extend beyond the limits of their own production sites, considering Life Cycle Thinking and Life Cycle Management approaches.

In this context, management of the environmental variable in the agri-food sector is mainly carried out through the use of voluntary standards. The high number of variables to be considered in the management of a firm in the agri-food sector certainly requires the adoption of an integrated management approach, encompassing system, product and process quality. In fact, agri-food firms, as enterprises in any other sector, have a series of tools at their disposition, based on international standards, which may be useful for the purposes of environmental management (Salomone et al. 2012a).

The standards considered to be most significant for single or integrated use for the management and assessment of environmental issues can be classified as “system standards” (such as ISO 14001 for Environmental Management Systems) and “product standards” (such as the ISO 14040 series for Life Cycle Assessment and ISO 14020 series for Environmental product labels and declaration). In fact, system standards, in general, are the most widely used, as they can be adapted to the real situation of each business, especially regarding management of contractual and mandatory aspects, as well as continual improvement processes; however, they have the significant disadvantage of being poorly perceived by final consumers. This is partly due to the low visibility of the relative acronyms, which can only be used on packaging with considerable limitations, so as not to create confusion among consumers regarding what is being certified (the organisation’s management system and not the product), whereas regulated certification logos (quality marks and organic products) can properly be given greater prominence. A more suitable approach to environmental quality management in the agricultural and agri-food sectors is probably one based on using direct means of ensuring the environmental performance of products; capable of guaranteeing and facilitating social acceptability on the one hand and, on the other hand, greater appeal in more environmentally aware markets, which are expanding.

In addition to these considerations, nowadays businesses are held responsible for the impacts of their activities (so-called extended producer responsibility) in every phase of the life cycle of the products they make; therefore, companies have to manage processes that extend beyond their factory gates. This push towards moving the emphasis from the environmental impacts of individual production sites to those associated with products can be seen from numerous aspects including, for example: in the EU Green Paper on Integrated Product Policy (IPP), in the EMAS III Regulation, in the revision of the ISO 14001 standard and in the indications emerging from businesses with experience of a possible integration of the previously separate system (Environmental Management Systems) and product (Life Cycle Assessment, Eco-design, ecological labelling) fields, with the development of positive synergies. Therefore, the boundaries between an organisation pursuing its competitive strategies and other actors in the economic system, as well as those between process management and product/service management, have proved to be permeable whenever businesses decide to make a concrete commitment to improving their environmental performance (Andriola et al. 2003), so new approaches centred on the product-orientation of environmental management have emerged.

2 Product-Oriented Environmental Management: Moving Outside the Boundaries of Traditional Environmental Management

Product-Oriented Environmental Management (POEM) can be defined as “an approach for organising and operating a firm in such a way that improving the environmental performance of its products becomes an integrated part of operations and strategy” (de Bakker 2002).

A brief history of product-oriented environmental management is presented in van Berkel et al. (1999): its birth could be dated to 1989 when the Netherlands Environmental Policy Plan (NEPP) defined an environmental policy not merely focused on production processes, but also on products, by taking a life cycle approach. In 1995 the Dutch government changed its environmental product policy (with the PMZ programme)Footnote 2 pushing producers into making environmentally responsible decisions so that companies started to work on products, pursuing the continual improvement of their environmental performances. A European policy based on life cycle thinking and with a product focus was created only in 2001 with the Green Paper on Integrated Product Policy (European Commission 2001a), which proposed a new strategy to strengthen and refocus product-related environmental policies and develop the market for greener products.

Afterwards, many companies increasingly realised that environmental benefits can be achieved by assessing products and organising, together with partners, measures and activities for the reduction of environmental impacts of products (PricewaterhouseCoopers 1999). With a product-oriented environmental approach the focus shifts from the individual organisation to the entire product chain with a focus on the life cycle stages which imply the most important environmental impacts in the supply chain; indeed, these impacts often appear in parts of the chain other than in the organisation in question (Jørgensen 2008). Considering that environmental improvements of products can be gained in each part of the product life cycle phases, several companies in the product chain should look jointly at how environmental effects can be reduced and how this can be translated into commercial benefits (Klinkers et al. 1999). Thus, dialog throughout the product chain should be considered as a precondition of success (Schmidt et al. 2001). When a company decides to put this approach into practice the environmental condition of the products, business opportunities, strategic targets and stakeholders’ expectations should be evaluated (Schmidt et al. 2001). Indeed, by implementing a product-oriented approach, companies gain different benefits, such as (Brezet and Rocha 2001; Danish EPA 2002; Schmidt et al. 2001):

-

greater knowledge of products (including their financial aspects and price calculation);

-

closer coordination within the company and a better synergy between the environmental function and the firm’s other functions;

-

closer cooperation among firms thanks to better dialog and exchange of information with customers and suppliers;

-

improvement of the company’s strategic position in green markets;

-

reduction of environmental impacts.

In literature more than one term is used to indicate environmental management approaches, activities, procedures and/or structures that go beyond firms’ boundaries with a life cycle and/or a supply chain approach, often creating terminology that can be confused with the above mentioned definition of POEM. The most widely used terms cited in international literatureFootnote 3 are:

-

Product-oriented Environmental Care (PEC) is intended as an extension of environmental management aimed at allowing firms to control the environmental impact of their products anywhere in the chain and “product-oriented environmental management system could be regarded as a very promising solution to incorporating responsibility at the right places within the industry” (Klinkers et al. 1999). It can be specifically defined as “a systematically set up management system through which all efforts and activities within a company are structured in such a way that environmental effects of products or services within their product chain, under given preconditions (economically sound) are controlled, reduced and, where possible, prevented, in a continuous process” (PricewaterhouseCoopers 1999);

-

Inter-Organisational Environmental Management (IOEM) is an environmental management approach that “involves learning about the environmental impacts throughout the supply chain and the life cycle of products, and interacting with other firms or organisations in the supply-chain to reduce these impacts” (Sinding 2000);

-

Life-Cycle Oriented Environmental Management (LCOEM) is a form of environmental management that requires firms to examine environmental impacts throughout the life cycle of their products and that “can only be achieved through coordinated efforts of all parts of the organisation, its suppliers and its customers” (Sharfman et al. 1997);

-

Environmental Supply-Chain Management (ESCM) is a form of supply chain management that involves introducing and integrating environmental practises aimed at auditing and assessing suppliers on environmental performance metrics; at the same time, suppliers should undertake measures that ensure the environmental quality of their products (Darnall et al. 2008);

-

Green Supply Chain Management (GSCM)—for Srivastava, implementing GSCM means “integrating environment thinking into supply chain management, including product design, material sourcing and selection, manufacturing processes, delivery of the final product to the consumers, and end-of-life management of the product after its useful life” (Srivastava 2007);

-

Product-Oriented Environmental Management (POEM) is a management tool “in which by taking a systematic approach all processes and activities in a company can be organised such that the environmental impact along the product chain can be constantly controlled, minimised and avoided wherever possible” (Brezet et al. 2000);

-

Product-Oriented Environmental Management Systems (POEMS or P-EMS) or Product-Based Environmental Management Systems (PBEMS) are all synonyms that indicate an extension of traditional process-oriented Environmental Management Systems (or a stand-alone tool including EMS) in order to facilitate the integration of environmental product considerations into the process of continual improvement (Brezet and Rocha 2001; Donnelly et al. 2004; van Berkel et al. 1999).

Although this list may not be exhaustive, it refers only to cases directly or indirectly linked to environmental management practises, activities and tools that imply co-operation between a firm and suppliers and/or customers aimed at evaluating, controlling and managing environmental issues connected to a product. The above mentioned terms (which always embrace life cycle and/or supply chain approaches) are often synonyms, but in other cases their meaning may have a different scope. For example, POEM, IOEM and LCOEM are more general, indeed they are umbrella terms that may include ESCM, Life Cycle Assessment, Industrial Ecology, and other tools and practises that involve an inter-organisational efforts and a lifecycle perspective. On the contrary, POEMS, P-EMS and PBEMS specifically refer to Environmental Management Systems (EMSs) and always include this type of management structure in their framework. Therefore we can conclude that POEMS, P-EMS and PBEMS are systems that can be certainly included in the wider category of “inter-organisational environmental management” (IOEM) and of “life-cycle oriented environmental management” (LOESM) and are strongly related to Life Cycle Management (LCM) and Supply-Chain Management (SCM) approaches.

Without a doubt the growing interest shown by society in the environmental consequences associated with the whole product life cycle is a key pressure towards the diffusion of product-oriented environmental management approaches in firms; however, for their successful implementation systematic procedures need to be developed and inserted into a routine organisational activity, such as an EMS. Indeed, investigating the various above mentioned concepts, some authors (e.g., Ammenberg and Sundin 2005a; Donnelly et al. 2006; van Berkel et al. 1999; etc.) highlighted the important role that standardised EMSs may have in the pursuit of product-related environmental goals and in the implementation of product-oriented environmental management approaches; this role is explored here below, presenting a brief overview of the reasons for which standardised management structures should be used as a basis for product-oriented environmental practises.

2.1 Products in Environmental Management Systems

In the wide and diversified range of environmental management tools that firms can use in pursuit of sustainability goals, EMSs are certainly the most widespread in every different productive sector; indeed, at January 2007, more than 134,400 companies in the world had an EMS in compliance with ISO 14001 and/or EMAS Regulation (Corporate Risk Management Company 2012; Eurostat 2011).

The success of this environmental management tool is demonstrated by the fact that the number of certifications/registrations has grown steadily over time, however, considering the above mentioned product-related issues, its major limitation is the fact that EMS only cover the organisation itself, without considering the environmental aspect of the life cycle, thus limiting the organisation’s environmental improvement actions and the consequent market opportunities to be potentially exploited (De Lima Ottoni 2010; Kim 2008). Indeed, in industrial experiences, EMSs have a primarily internal orientation, usually being directed at site level (Klinkers et al. 1999) because companies mainly implement site-specific procedures aimed at reducing emissions through process improvements. In these cases, EMSs often lack a life-cycle perspective on products, so companies have a limited perception of the environmental impacts of their products (Ammenberg and Sundin 2005a, b), with the result that concentration on internal performance may be less effective since environmental impacts may go beyond firm boundaries (Sinding 2000).

Therefore “if managers wish to minimise their company’s impact on the natural environment, logic dictates that they look at all the effects, not just those specific to a single production or service process” (Sharfman et al. 1997), and to do so they need to move outside the boundaries of a traditional environmental management system, changing the focus from site-specific processes to the whole product-chain, implementing product-oriented approaches.

Indeed, despite this criticism of EMS, there are several aspects which indicate that products can be properly managed in the structures of the standardised EMS and that traditional EMSs are a useful starting point for product-orientation work with a life cycle and/or a supply chain approach:

-

several product-related issues are integrated into the EMS standards—the EMS standards require that companies pay attention not only to environmental issues regarding the production process, but also to their products and services, and product-related references are quite often cited in both the EMS reference documents—i.e., ISO 14001 (International organisation for standardisation 2004a) and EMAS Regulation (European Commission 2009) - with potential significant consequences in terms of management of product environmental issues, even if “it is uncertain to what extent normal EMSs encompass and influence the environmental load of products” (Ammenberg and Sundin 2005a);

-

the EMS framework is a useful support for the implementation of product-related strategies—indeed, some authors (e.g. Brezet and Rocha 2001; Ammenberg and Sundin 2005a) suggest that an EMS provides an adequate structure for helping a firm acknowledge its own product environmental problems, implementing product environmental improvement strategies, providing consistency through the allocation of resources, assignment of responsibilities and ongoing evaluation of practises, procedures and processes. Even though EMSs are not a guarantee of continual improvement of product environmental performances—which depends on effective strategic choices by companies (Brezet and Rocha 2001)—it is indubitable that EMS structure may be a significant starting point, albeit insufficient, for addressing and implementing product environmental improvement strategies. The fundamental aspect is to integrate the requisites and the additional activities “into strategic management and the daily operation of companies in a dynamic process of continuous environmental performance improvement” (Brezet and Rocha 2001) and this aspect can be ensured by the organisational structure of an EMS;

-

significant synergies exist between EMS and life cycle tools—life cycle management tools such as Life Cycle Assessment (LCA) can be used in EMS in order to evaluate environmental performance and to identify significant environmental aspects of an organisation’s products and services (Lewandowska 2011). ISO 14001 and EMAS do not specify the tools that should be used for the identification and assessment of environmental aspects, but ISO 14004 states that “there is no single approach for identifying environmental aspects and environmental impacts …” (International organisation for standardisation 2004b). Furthermore, EMS standards contain requirements that should be adapted to the real situation of the company applying them and third-party certification will check if the company satisfies the requirements, but the method used to meet them is optional. This means that LCA can be considered as a suitable tool in this context. Remaining on this subject, a survey conducted by Zobel et al. (2002) revealed that the identification and assessment of environmental aspects in an EMS context can differ considerably among different organisations and may be influenced by personal value judgements, with the result that the environmental managers interviewed felt that the most common improvements should be the use of more objective and similar methods among the different units of a company and LCA is suggested as the scientific method that can satisfy these requirements. Indeed, although an LCA study only allows the potential environmental impacts associated with a product to be identified, while EMS needs detailed impact modeling, LCA certainly enables a broadening of the review of environmental aspects with indirect aspects related to the whole supply chain, using a well-established impact assessment methodology, generating results scientifically relevant and reproducible (Lewandowska et al. 2011);

-

significant synergies exist between EMS and Green Supply Chain Management (GSCM)—GSCM is highly coherent with EMS, indeed, for organisations, GSCM involves measures oriented to requiring suppliers to undertake actions that ensure the environmental quality of their products; it also sometimes includes measures intended to inform buyers on how to reduce the environmental impact when they are using the product, so that practically organising management activities embracing the chain from suppliers to consumers. GSCM and EMS practises are strongly complementary: their measures and actions aim to reduce direct and indirect impacts of an organisation; they both rely on the Deming Cycle continual improvement model; EMS offers a management structure to support supply chain management decisions that affect the environment, etc.; but the great difference is, once again, the different perspective (the organisation in EMS and the whole chain in GSCM), so for an organisation, GSCM activities involve greater external contacts than EMSs and this may require additional skills outside the EMS framework (Darnall et al. 2008).

The similarities and potential synergies between EMS and other product-oriented tools and approaches (e.g. eco-design, eco-labelling, etc.) could be analysed in greater depth, but it is already clear that there are strong incentives to integrate product management into EMS, because the product life cycle perspective could enrich and broaden the scope of EMS (Ammenberg and Sundin 2005a) bringing benefits in terms of resolution of environmental pollution problems, better relations with the other actors involved in the supply chain, and market orientation of the environmental activities performed. So, even though traditional EMSs do not practically encompass products into their procedures, there is a growing need to incorporate life cycle perspective into the more general environmental management of an organisation and also to be able to manage the indirect aspects associated with product and services, within a structured framework, with a scientific method and with a supply chain focus. It is for all the above mentioned reasons that a growing number of organisations that pay great attention to environmental issues are therefore experiencing the need to integrate system standards (e.g. ISO 14001) with product standards (e.g. ISO/TR 14062 on Eco-Design, ISO 14040 series on Life Cycle Assessment, and ISO 14020 series on environmental labelling on products), progressively shifting attention from system/process to product/service.

In line with this orientation, during the 3rd Integrated Product Policy Expert Workshop on IPP (European Commission 2001b), some of the participants identified three types of EMS with a broader focus (Product-Oriented Environmental Management Systems—POEMS—which focus on products; Organisation-Oriented Environmental Management Systems—OOEMS—which focus on the site or organisation; Integrated Environmental Management Systems—IEMS—which integrate ISO 14001 and EMAS) and finally Product-Oriented Environmental Management System (POEMS) was indicated as the standardised management system useful for the integration of products into firms’ strategies and this work certainly influenced the ISO 14001 and EMAS revisions (Kim 2008). The importance of POEMS was then newly confirmed in the communication of the European Commission to the Council and European Parliament, with particular reference to its role in the development of the concept of product life cycle (European Commission 2003).

2.2 Product-Oriented Environmental Management System

POEMS is a new framework designed to bring together traditional environmental management systems and tools oriented towards improvement of the environmental performances of products. The abovementioned considerations highlight the increasing need for integration between system standards and product standards and, as a result of this, alongside management “tools” that are already widely used (ISO 14001 and EMAS), companies have started to appreciate other “tools” that are oriented more towards the management of environmental performances of products (Life Cycle Assessment, Eco-Design, ecological labelling).

One of the most widely used definitions of POEMS to be found in the limited literature available is the one provided by Rocha and Brezet: “an environmental management system with a special focus on the continuous improvement of a product’s eco-efficiency (ecological and economic) along the life cycle, through the systematic integration of eco-design in the company’s strategies and practises” (Rocha and Brezet 1999). Another definition, which is more appropriate for the agri-food sector as it is not unequivocally tied to eco-design and is, thus, also applicable to companies that do not deal with product design, is the one coined by de Bakker (referred to the more general POEM): “a systematic approach to organising a firm in such a way that improving the environmental performance of its products across their product life cycles becomes an integrated part of operations and strategy” (de Bakker et al. 2002).

Currently, there are no prescriptive standards for POEMS and the only elements that can offer methodological references are the Spanish UNE 150.301 standard and the ISO 14006; the Spanish standard was used as a basic reference point for the ISO one and both relate to the insertion of eco-design into environmental management systems. Despite there still being no standard reference and few studies available in literature—mainly in manufacturing industries and only early attempts in the food processing industry (van Berkel et al. 1999) and in the agri-food sector (Ardente et al. 2006)—a growing number of organisations are experiencing the need to integrate environmental management system standards with those addressed to the environmental evaluation of products, shifting attention from system/process to product/service (Salomone et al. 2011).

Thus, within a context in which organisations are showing increasing interest in ways of integrating system standards and product standards, there is certainly great interest in being able to create a POEMS model that reflects the real needs of companies and their stakeholders, also considering the lack of a uniform and widely accepted methodology, exploring its benefits both in the environmental and in the economic dimensions. In particular, the role of economic benefits (e.g., cost savings through eco-efficiency, reduced risk, improvement of the firm’s/product’s image and market position, etc.), should be investigated in detail, because very little is written on how POEMS affects firm’s performances, and the drivers that may push companies to implement POEMS should be clearly identified, as they can vary depending on the sector of production and the specific organisational and strategic conditions in which a firm operates.

3 The Role of POEMS in the Improvement of Economic and Competitive Performance

The existence of a mutual benefit between environmental and economic performance is usually considered as a basic assumption of sustainable development. As mentioned in the previous section, the framework of POEMS itself is designed in order to support an environmental system focused on the continual improvement of both ecological and economic product eco-efficiency along the life cycle (Rocha and Brezet 1999).

This section is intended to focus attention on some relevant issues of the relationship between environmental and economic performance, regarding the implementation of POEMS in the agri-food sector:

-

the relevance of economic issues in the adoption of environmental management systems by firms;

-

the pros and cons of accounting for the environment, with regards to the integration of the economic variable into the accounting system in the Life-cycle approach;

-

the benefits of POEMS in the improvement of economic and competitive performance, at firm level and at supply chain level.

3.1 The Relevance of Economic Issues in the Adoption of Environmental Management Systems

Achieving sustainable development often represents a strategic business decision, which plays a key role for the competitive advantage of a firm. The reasons why firms are embracing sustainable development at a strategic level are both ethical and economic.

The size of the firm can probably explain the predominance of ethical or economic reasons underlying the choice to go green. There is evidence, in this regard, that economic benefits are not a relevant issue for SMEs, whose interest in environmental management systems more likely springs from the will to improve: organisational and managerial efficiency; continuous monitoring of compliance; corporate reputation (Biondi et al. 2000). Though there is general acceptance of the virtuous cycle embedding the three dimensions of sustainable development—economic, environmental and social results –, into the ongoing debate over the value relevance of environmental management systems, evidence points to different results in different contexts. Whether or not the choice to invest in environmental management systems is associated with the aim of pursuing economic benefit, and independently of the awareness of the economic implications of such decision making, significant economic benefits are always associated when optimising resource use. The lack of awareness of economic benefit is often the necessary consequence of the lack of information in financial and in management accounting. Green (or environmental) accounting is suggested to overcome this “information gap”, encompassing environmental benefits and costs into decision-making.

3.2 Accounting for the Environment: The Pros and Cons in the Life-Cycle Approach

3.2.1 The General Aspects of Environmental Accounting

The widely accepted view that financial and non-financial data are traceable to the same framework of knowledge, being complementary in supporting decision making, highlights the existence of an “overlapping area” between the two types of information.

With regard to environmental issues, assuming that the environmental accounting domain is independent of the accounting information system leads management to underestimate the economic and competitive implications of environmental choices. Based on the assumption that “if you can’t measure it, then you can’t manage it”, management accounting is the prominent area of interest of environmental accounting, aiming to measure (in monetary terms) the consumption of factors of production (costs) and the results associated with the incurrence of such costs. While the latter are characterised by a greater degree of uncertainty, since it is very difficult to correlate the value created for only one of its potential determinants, the former is affected by the typical arbitrariness and uncertainty of cost accounting (Rupo 2001). Nevertheless, companies who follow the path of eco-management, sooner or later, have to adapt their cost accounting systems for the identification and proper allocation of environmental costs to their activities, processes and products. Information systems in use often allow the recognition of only a few types of costs among those related to the environment. Traditional accounting systems usually include these costs among general expenses (overheads), and this makes it harder to identify what causes the cost to be incurred (cost-driver). This could be justified only if environmental costs are supposed to be low, with the result that environmental accounting proves to be relatively expensive. Otherwise, the increasing importance of environmental costs, and the need to balance ethical and economic objectives, encourages companies to change their cost accounting systems, in order to have reliable information for decision making in the environmental field.

The integration of the environmental variable into the accounting system is direct detection of the so-called “green bottom line”, by which we mean the impact on business outcomes resulting from the adoption of environmentally friendly policies. Authoritative doctrine in this field has focused on the main objectives of environmental-related management accounting, which can be summarised as follows: (a) demonstrating the impact on economic and financial performance associated with environmental management; (b) identifying opportunities for cost reduction and other improvement opportunities; (c) defining environmental priorities; (d) product-pricing and definition of product mix; (e) enhancing customer value; (f) supporting investment appraisal and other long-term decisions; (g) supporting sustainable business (Bennet and James 1998). In short, environmental accounting provides insight into the evaluation of environmental impacts and of the associated financial effect, hence being a suitable tool for strategic planning and management control (Burnett et al. 2007). Together with various standardised procedures, such as 14001 for EMS, ISO 14040 series for LCA and ISO 14020 series for environmental product labels and declaration, environmental accounting can assist companies in managing, measuring and improving the environmental effects of their products/services and processes.

3.2.2 The Multi-Dimensional Notion of Environmental Cost and the Boundaries of the Accounting System

The scope of the environmental accounting system is related to the type of costs included in the system. Environmental costs have a wide range of meanings, corresponding to different theoretical approaches and practical purposes. Therefore, it is necessary to mark off the boundaries of the accounting system, distinguishing between internal (private) environmental costs, and external (societal) environmental costs. The former are costs incurred by the company, at its discretion or in accordance with legal rules, the latter represent the cost burden on society as a result of the business and which can be expressed by the depletion of resources and the consequent decrease in welfare and quality of life. It is well-known that the boundaries between internal costs and external costs are becoming more and more blurred, as a consequence of the growing pressure deriving from regulatory measures—enactment of laws, standard setting, threshold-parameters –, aimed at building the progressive internalisation of environmental costs, through the imposition of penalties for contraveners.

Another useful criterion in the definition of environmental costs is the reference to time. It must be clarified whether it is worth considering, in addition to costs already incurred, those costs which the company (or society) may incur in the future due to current or past choices. Despite the difficulties inherent in estimating future costs, companies should be aware of them, in order to set plans and programs on a rational basis.

Finally, but no less important, is the distinction between the costs incurred by actions to prevent, reduce or eliminate, the environmental impact, and the costs that the company is obliged to pay in order to repair environmental damage caused, in the form of fines, penalties or compensation for damage caused by past actions (environmental losses). It is quite evident that while the former are expected to produce future benefits, being the expression of the company’s commitment to the environment, the latter represent, at most, the reparation due for conduct contrary to the environment. Accepting the narrow meaning, which is coherent with the European approach to Financial Accounting, it is possible to uncover the environmental costs incurred by the company for activities intended to prevent, reduce or eliminate the environmental impact of products and processes, and the costs incurred to preserve environmental resources.

3.2.3 The Integration of the Economic Variable in the Life-Cycle Approach

LCA supports the evaluation of the potential environmental impacts associated with a product, process or service, allowing the identification of solutions for the environmental improvement of the system under study. Due to its nature, LCA handles only physical data and does not enable the identification of the most cost-effective means of making environmental improvements. On the contrary, Life Cycle Costing (LCC) is designed to compare the cost-effectiveness of alternative investments, enhancing consideration of the economic aspects of environmentally related decisions (Norris 2001). In its broader original meaning, LCC is designed to identify all the environmental costs—internal and external—associated with a product, process, or activity throughout all stages of its life (Epstein 1996). The objectives pursued are, as a matter of principle, to optimise the use of resources and reduce overall costs along the life cycle. LCC goes beyond the gate of the single firm, extending the analysis to the whole supply chain, and including the phase of consumption until end of life of the product. This configuration corresponds to the wider definition of environmental costs, embracing current and future costs, private and societal costs, associated with a product or process covered by the calculation, with the objective of evaluating the full life-cycle, encompassing each phase from raw material extraction to the end-of life phase of the product or process (from cradle to grave). In this perspective, the cost analysis integrates the LCA procedure, being focused on the economic impact (cost) rather than on the determination of physical inventory.

Therefore, the potential of LCA methodology to improve environmental performance of products/services can be emphasised through integration with accounting tools. The life-cycle assessment, as a domain of the accounting system, entails coupling a quantitative value (in monetary terms) to environmental impacts associated with a project or a product by assessing the potential environmental and social impact associated with identified inputs and releases, so as to support decision making.

It’s worth considering that, both in literature and in practice, the boundaries of LCC are defined in different ways, according to the approach adopted for the estimation of external and future costs. The subjectivity underlying the evaluation of such costs probably represents the most important limitations of LCC, emphasising the arbitrariness of any cost-accounting method. In fact, only the societal LCC includes societal costs and extends the time horizon to the long term. The more recent SETAC position, for example, is to encompass in the LCC all the costs incurred by firms operating in the supply chain, extending the analysis only to those external costs which are expected to be internalised in the decision relevant future. Given the difficulties incurred in the evaluation of all relevant costs for LCC, many firms prefer the adoption of partial LCC, especially in the pilot phase.

Realising the importance of monitoring economic effects of environmental management systems, an LCA procedure represents a necessary input for costs assessment, providing LCC with data for the cost inventory and subsequent allocation to cost types.

It is possible to argue that the greater the accuracy and reliability of LCA, the greater the reliability of cost accounting (and LCC) and the trustworthiness of information for decision making. Thus, the first step is to set up a suitable methodology for LCA, in order to properly assess environmental impacts; it is then worth encompassing economic implications in the decision making process, implementing adequate environmental cost accounting methods (such as LCC and Total Cost Accounting), as part of the same integrated information system.

3.3 The Benefits of POEMS in the Improvement of Economic Performance at Firm Level and at Supply Chain Level

A POEMS can assist uniform and widely accepted methodology in the improvement of environmental, economic and competitive performance, thanks to its following features:

-

a structure compatible with the flexibility of the accounting information system and/or with gradual implementation of economic/financial measures related to environmental performances;

-

the source of data gathered when implementing the product management system, which enables evaluation of the firm’s strategy, on the assumption that improving product environmental performance across product life cycles is bound to become a key factor in operations and strategy;

-

the potential benefits at the supply chain level, considering that adoption of EMS has impacts on the three pillars of the triple bottom line.

Once POEMS is implemented in firms, it is expected that variables to be included in the measurement of environmental performance will be developed, and then integrated within the accounting information system, in order to support a more comprehensive evaluation of firms’ performance. The availability of data from LCA, suitable to be processed for management decision making and for external reporting, provides a framework for testing the coherence of financial, social/environmental and competitive relapses of strategic planning and of voluntary and mandatory reporting.

Given the perspective adopted in a POEMS, its implementation will offer a good “test bed” for assessing the impact of sustainable operations on the triple bottom line both: at the firm level, in order to verify the profitability of alternative choices, given a certain priority in the environmental perspective, and at the supply chain level, in order to verify whether the adoption of collaborative practises with supply chain partners could have positive impacts on economic and social performance.

A recent empirical survey (Gimenez et al. 2012) shows that the implementation of internal environmental programmes produces positive effects on the components of the triple bottom line (social, environmental, economic). Environmental initiatives lead to lower manufacturing costs, through the optimisation of resource use and the reduction of reparation costs; at the same time, sustainable operations improve brand image and stakeholder relations. On the other hand, the results of the empirical study point out that supply chain collaboration has a significant impact on the triple bottom line, suggesting that the partnership approach should be preferable, since collaboration with suppliers and customers pays off in terms of improvement of environmental and social performance.

These results highlight that a firm engaged in POEMS implementation is expected to produce positive impacts on the various dimensions of its success (competitive, economic, social) other than it being desirable for environmental purposes. Finally, the adoption of collaborative schemes with suppliers and customers is considered the best way for implementing a sustainable initiative, while the exclusion of suppliers that fail to meet standard requirements could be unsuccessful.

4 A POEMS Framework for the Agri-Food Industry

Starting from the emerging interest in ways of integrating system standards and product standards described in the previous sections, the research project Eco-Management for Food (PRIN No.2008TXFBYT), co-funded by the Italian Ministry of Education, Universities and Research—MIUR (EMAF 2012), was designed in order to propose, test and, consequently, spread a model of POEMS, specifically tailored to companies operating in the Italian agribusiness sector, aimed at supporting these firms (mainly SMEs) in the introduction of organisational innovations that allow them to manage and continually improve the sustainability and competitiveness of their products/processes.

In the belief that the most appropriate definition of a POEMS model should be structured following a Life Cycle Management (LCM) approach, the main findings of the United Nations Environmental Programme (Remmen et al. 2007) were used as a starting point for the identification of the key elements of the POEMS. In particular, the POEMS model should be:

-

a product management system with a life cycle perspective and a chain vision—indeed “LCM is a product management system aiming to minimise environmental and socio-economic burdens associated with an organisation’s product or product portfolio during its entire life cycle and value chain…”(Remmen et al. 2007);

-

based on the continual improvement of product performances—indeed “LCM is making life cycle thinking and product sustainability operational for businesses through the continuous improvements of product systems…” (Remmen et al. 2007);

-

structured as a set of tools ensuring the most appropriate management of the main priorities of the firms that implement it—indeed “LCM is not a single tool or methodology but a management system collecting, structuring and disseminating product-related information from the various programmes, concepts and tools incorporating environmental, economic, and social aspects of products, across their life cycle…” (Remmen et al. 2007).

In order to specify which tools should be embedded in the POEMS model and to successfully apply this framework in agri-food firms, the first step was to identify the main sector-specific barriers to LCM implementation; then, the identified barriers were used as starting points for setting the success factors, the solutions to overcome barriers and achieve the success factors and, finally, the POEMS model tools that permit the identified solutions to be reached.

This path allowed the EMAF project partners to identify the tools that constitute the final framework of the POEMS model:

-

Integrated Quality and Environmental Management System (ISO 9001 and ISO 14001 or EMAS Regulation)—one of the most frequent obstacles encountered in the implementation of LCM approaches is the resistance to change that many organisations show when employees are asked to change their old ways of working. This barrier is mainly due to a lack of internal environmental awareness, so it should be dealt with by spreading an environmental cultural change and involvement through proper environmental training and dissemination activities, which are fundamental processes of Environmental Management Systems (EMS). Another specific barrier to LCM implementation is the dispersion of environment-related information, which should be dealt with through a structural and organised vision of the environmental aspects that the firm has to face. The structural organisation of EMS certainly offers a solution to this problem, but little attention is paid to product performances in EMS, while LCM strategies need to be targeted on products. The internalisation of product requisites within the environmental management structure can be ensured by the integration of EMS with a Quality Management System. All these considerations lead to the choice of an Integrated Management System as the most suitable tool for facing this group of barriers;

-

Simplified Life Cycle Assessment—a very common feature in agri-food firms (but also widespread in other production sectors) is the main focus on short-term problems and the lack of chain management responsibility. In order to contrast these aspects, the internalisation of a chain management vision and long-term value creation should be assured by implementing LCM and Life Cycle Thinking (LCT) approaches. These approaches require detailed knowledge of the environmental issues connected with the whole life cycle of the product. However, a lack of awareness of product life cycle environmental impacts usually affects firms in this field. Organisations that aim to identify their product life cycle environmental impacts may use the Life Cycle Assessment (LCA) methodology, but poor access to the large amount of life cycle data, the lack of in-house expertise and the costs associated with its implementation, make it highly necessary to define Simplified LCA approaches, in order to allow SMEs to perform environmental assessment by themselves using an easily understandable tool;

-

Guidelines for the Environmental Product Communication—although environmental awareness is constantly increasing in many businesses, environmental commitment is still not perceived as an opportunity, so the success strategy is represented by the ability to transform the environmental measures taken into commercial advantages, for example through accurate environmental product communication. The problem is that single firms encounter many difficulties in whole chain involvement, whereas product communication requires a life cycle perspective and a chain vision. The only solution is represented by spreading an external environmental cultural change and involvement throughout the supply chain with environmental training and external dissemination. In addition, the choice of the most suitable form of environmental message may be a complex and uncertain one for firms to make, so guidelines targeted at helping them in the identification of the proper environmental label declaration are absolutely necessary (Environmental Product Labelling and Declaration guidelines—EPLD).

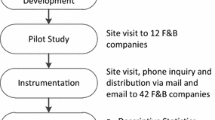

The above described path to the definition of a POEMS framework is summarised in Fig. 1.1; the path efficiency is enhanced by the fact that each tool can provide multiple solutions for overcoming several barriers.

The path towards the final POEMS model (Salomone et al. 2012b)

This book presents the individual environmental management tools of which the POEMS model is made up, with a description of their methodological structure and the main results of their implementation in different pilot agri-food companies, in order to verify their effective functioning and to highlight the strong and weak points of the POEMS model and of its individual fundamental elements.

Indeed, the innovative character of the POEMS model presented in the EMAF project has a double dimension connected to the fact that:

-

each environmental management tool included in the POEMS framework is individually developed in its methodological structure and then applied in pilot firms;

-

each environmental management tool can be observed both with a single and an integrated approach, offering agri-food organisations a “modular” format that refers to each tool separately and to the POEMS in general. In this way, whatever the starting point of the firms and whatever their targets, they will find an answer and a strategy via which they may formulate their own route to eco-compatibility.

This double dimension is also translated into a coherent structure of the book as described in Fig. 1.2.

How to read the book

Each single part of this book can be read independently from the others. Each part (except Part I—Background and concepts) is structured on three different levels of analysis (literature review, methodological structure and case studies in pilot firms) corresponding to three different chapters for each part:

-

part I describes background and concepts useful for understanding the field and the main topics covered in the other chapters;

-

part II describes the state-of-the-art of Integrated Management System, the methodological structure of a framework for agri-food SMEs and its application experience in a pilot firm of the tomato processing sector;

-

part III describes the state-of-the-art of Simplified Life Cycle Assessment approaches and tools, the methodological structure of a framework consistent with the needs of agri-food SMEs and its application experience in a pilot firm of the wine industry;

-

part IV describes the state-of-the-art of environmental labelling practises in the agri-food sector, the structure of Environmental Product Label and Declarations Guidelines tailored to the characteristics of agri-food SMEs and their application experience in a pilot firm in the pasta production sector;

-

part V describes the state-of-the-art of product-oriented environmental management systems, the methodological structure of a POEMS framework for agri-food SMEs, resulting from an integration of the previously described tools, and its application experience, with different levels of integration, in pilot firms in the olive oil production sector and in the roasted coffee production sector.

Moving from part II to part V, the environmental management standpoint gradually widens, progressively focusing on a process, product or supply chain perspective.

5 Conclusions

Ways of managing the environmental variable have changed a great deal since problems associated with pollution produced by human activities were first faced. Indeed, following the evolution of environmental policies, businesses have moved from a command-and-control approach towards a proactive approach and, consequently, a set of new tools for environmental management have been developed.

Nowadays, the majority of the EMSs implemented in firms are based on standards (e.g. ISO 14001) that allow improvements of the environmental performances of production processes in a flexible way; therefore, they are mainly oriented towards the internal operations of a company. However, growing interest in the environmental impacts of products along their life cycle opens the way to new scenarios. Indeed, the availability of product environmental tools and the development of IMS models enable the implementation of management systems that incorporate processes realised, partially or entirely, beyond the boundaries of a company, according to a supply chain logic. In such situation, a POEMS can play an important role, because it allows a company to manage both economic and environmental performances. The above considerations are valid for companies in any sectors, but they take on a special significance in the agri-food sector where the expectations of stakeholders are related to factors of food product quality (e.g. food safety), and of a cultural (e.g. tradition) and ethical-social nature (e.g. environmentally responsible behaviour). In conclusion, the development of a dedicated model can be an important aid for guiding agri-food SMEs in the implementation of a POEMS, in order to allow compliance with mandatory rules and specific customer requests, while improving economic and environmental performance and maintaining competitiveness.

Notes

- 1.

In this book the terms “supply chain” and “product chain” are indiscriminately used to refer to all actors (parties or organisations) involved in the creation of a product or a service, from the extraction of raw materials to production, consumption and end-of-life.

- 2.

See Sect. 11.2.1.1.

- 3.

For each definition just one reference is cited, which does not necessarily represent the most widely quoted definition in international literature.

References

Ammenberg J, Sundin E (2005a) Products in environmental management systems: drivers, barriers and experiences. J Clean Prod 13:405–415

Ammenberg J, Sundin E (2005b) Products in environmental management systems: the role of auditors. J Clean Prod 13:417–431

Andriola L, Luciani R, Sibilio S (2003) Esperienze di POEMS: sistemi di gestione orientati al prodotto. Unificazione&Certificazione 7:6–8

Ardente F, Beccali G, Cellura M, Marvuglia A (2006) POEMS: a case study of a winemaking firm in the South of Italy. Environ Manage 38:350–364

Bennet M, James P (1998) The green bottom line: environmental accounting for management, current practice and future trends. Greeleaf Publishing, Sheffield

Biondi V, Frey M, Iraldo F (2000) Environmental Management Systems and SMEs: Motiva-tions, opportunities and barriers related to EMAS and ISO 14001 Implementation. Greener Manag Int 29:55–69

Brezet H, Rocha C (2001) Towards a model for product-oriented environmental management system. In: Charter M, Tischner U (eds) Sustainable Solutions. Greenleaf Publishing, Shef-field

Brezet H, Houtzager B, Overbeeke R, Rocha C, Silvester S (2000) Evaluation of 55 POEM sub-sidy projects. Product oriented environmental management. Internal Report, Delf Technical University

Burnett RD, Hansen DR, Quintana O (2007) Eco-efficiency: achieving productivity improvements through environmental cost management. Acc Public Interest 7:66–92

Commission European (2009) Regulation No 1221/2009 of the European Parliament and of the Council of 25 November 2009 on the voluntary participation by organisations in a Community eco-management and audit scheme (EMAS). Official J Eur Union L342:1–45

Corporate Risk Management Company (2012) Worldwide number of ISO14001. http://www.ecology.or.jp/isoworld/english/analy14k.htm. Accessed 3 July 2012

Danish Environmental Protection Agency (2002) Manual on product-oriented environmental work. Environmental News 64

Darnall N, Jolley GJ, Handfield R (2008) Environmental management systems and green supply chain management: complements for sustainability? Bus Strategy Environ 17:30–45

de Bakker FGA (2002) Product-oriented environmental management: lessons from total quality management. J Industr Ecol 5:55–69

de Bakker FGA, Fischer OAM, Brack AJP (2002) Organising product-oriented environmental management from a firm’s perspective. J Clean Prod 10:455–464

De Lima Ottoni F (2010) Product-oriented environmental management: a system for product environmental performance communication. Master of Science Thesis, Royal Institute of Technology, Stockholm

Donnelly K, Salemink A, Blechinger F, Schuh A, Boehm T (2004) A product-based environ-mental management system. Greener Manag Int 46:57–72

Donnelly K, Beckett-Furnell Z, Traeger S, Okrasinski T, Holman S (2006) Eco-design implemented through a product-based environmental management system. J Clean Prod 14:1357–1367

EMAF (2012) Eco-management for food project. http://ww2.unime.it/emaf/. Accessed 3 Sep 2012

Epstein MJ (1996) Measuring corporate environmental performance: best practices for costing and managing an effective environmental strategy. Irwin Professional Publishing, Burr Ridge

European Commission (2001a) Green Paper on Integrated Product Policy COM(2001)68. http://eur-lex.europa.eu/LexUriServ/site/en/com/2001/com2001_0068en01.pdf. Accessed 9 July 2012

European Commission (2001b) Environmental management systems (including product-oriented environmental management systems). Summary of Discussion at the 3rd Integrated Product Policy Export Workshop, Brussels

European Commission (2003) Communication from the Commission to the Council and the European Parliament. Integrated Product Policy. Building on Environmental Life-Cycle Thinking. COM (2003)302 final. http://eur-lex.europa.eu/LexUriServ/LexUriServ.do?uri=COM:2003:0302:FIN:en:PDF. Accessed 9 July 2012

Eurostat (2011) Organisations and sites with EMAS registration, 2003–2010. http://epp.eurostat.ec.europa.eu/statistics_explained/index.php?title=File:Organisations_and_sites_with_EMAS_registration,_2003-2010.jpg&filetimestamp=20111116135320#filelinks. Accessed 3 July 2012

Gimenez C, Sierra V, Rodon J (2012) Sustainable operations: Their impact on the triple bottom line. Int J Prod Econom (in press)

International organisation for standardisation (2004a) ISO 14001 Environmental management systems—Requirements with guidance for use. ISO, Geneva

International organisation for standardisation (2004b) ISO 14004 Environmental management systems— General guidelines on principles, systems and support techniques. ISO, Geneva

Jørgensen TH (2008) Towards more sustainable management systems: through life cycle management and integration. J Clean Prod 16:1071–1080

Kim N (2008) New model of component-based product-oriented environmental management system (C-POEMS) for small and medium-sized enterprises. PhD Thesis. Brunel University School of Engineering and Design. http://bura.brunel.ac.uk/bitstream/2438/3492/3/0324979NakyungKim_Thesis.pdf.txt. Accessed 8 June 2012

Klinkers L, van der Kooy W, Wijnen H (1999) Product-oriented environmental management provides new opportunities and directions for speeding up environmental performance. Greener Manag Int 26:91–108

Lewandowska A (2011) Environmental life cycle assessment as a tool for identification and assessment of environmental aspects in environmental management systems (EMS) part 1: methodology. Int J Life Cycle Assess 16:178–186

Lewandowska A, Matuszak-Flejszman A, Joachimiak K, Ciroth A (2011) Environmental life cycle assessment (LCA) as a tool for identification and assessment of environmental aspects in environmental management systems (EMS) part 2: case studies. Int J Life Cycle Assess 16:247–257

Norris GA (2001) Integrating life cycle cost analysis and LCA. Int J Life Cycle Assess 6:118–121

PricewaterhouseCoopers (1999) Guidelines for product-oriented environmental care. Environmental management in the product chain. Utrecht (Available on request at the Ministry of Housing, Spatial Planning and the Environment P.O. Box 20951 2500 EZ, The Hague tel. +31 70 3395050)

Remmen A, Jensen AA, Frydendal J (2007) Life Cycle Management. A business guide to sus-tainability. United Nations Environment Programme. http://www.unep.fr/shared/publications/pdf/DTIx0889xPALifeCycleManagement.pdf. Accessed 3 Sep 2012

Rocha C, Brezet H (1999) Product-oriented environmental management systems: a case study. J Sustain Prod Des 10:30–42

Rupo D (2001) La variabile ambientale nella comunicazione d’impresa. Giappichelli, Torino

Salomone R, Clasadonte MT, Proto M, Raggi A, Arzoumanidis I, Ioppolo G, Lo Giudice A, Malandrino O, Matarazzo A, Petti L, Saija G, Supino S, Zamagni A (2011) Product-oriented environmental management system (POEMS): A sustainable management framework for the food industry. Paper presented at the Life Cycle Management Conference 2011, Berlin, Germany, August 28–31

Salomone R, Saija G, Ciraolo L (2012a) The role of eco-management for sustainable agricultural production. In: Gorawala P, Mandhatri S (eds) Agricultural research updates, vol 4. Nova Sciences Publishers, USA

Salomone R, Clasadonte MT, Proto M, Raggi A, Arzoumanidis I, Ioppolo G, Lo Giudice A, Malandrino O, Matarazzo A, Petti L, Saija G, Supino S, Zamagni A (2012b) Improving life cycle management (LCM) tools for the food industry: a framework of Product-Oriented Environmental Management System (POEMS). Abstract book of the 6th SETAC World Congress 2012, 20-24 May 2012, Berlin, Germany, 294. http://berlin.setac.eu/scientific_programme/download_the_abstracts_book/?contentid=582&pr_id=403&last=435. Accessed 9 Aug 2012

Schmidt K, Møller Christensen F, Øllgaard H (2001) Product orientation of environmental work. Corp Environ Strat 8:126–132

Sharfman M, Ellington RT, Meo M (1997) The next step in becoming ‘green’: life-cycle oriented environmental management. Bus Horiz 40:13–22

Sinding K (2000) Environmental management beyond the boundaries of the firm: definitions and constraints. Bus Strat Env 9:79–91

Srivastava SK (2007) Green supply-chain management: a state-of-the-art literature review. Int J Manag Rev 9:53–80

Tukker A, Huppes G, Guinée J, Heijungs R., de Koning A, van Oers L, Suh S, Geerken T, Van Holderbeke M, Jansen B, Nielsen P (2006) Environmental Impact of Products (EIPRO). Analysis of the life-cycle environmental impacts related to the final consumption of the EU-25. Summary of the final report. European Commission: DG Environment e DG JRC

van Berkel R, van Kampen M, Kortman J (1999) Opportunities and constrains for Product-oriented Environmental Management Systems (P-EMS). J Clean Prod 7:447–455

Zobel T, Almroth C, Bresky J, Burman J-O (2002) Identification and assessment of environ-mental aspects in a EMS context: an approach to a new reproducible method based on LCA methodology. J Clean Prod 10:381–396

{kind=link}

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2013 Springer Science+Business Media Dordrecht

About this chapter

Cite this chapter

Salomone, R., Rupo, D., Saija, G. (2013). Innovative Environmental Management Tools for the Agri-Food Chain. In: Salomone, R., Clasadonte, M., Proto, M., Raggi, A. (eds) Product-Oriented Environmental Management Systems (POEMS). Springer, Dordrecht. https://doi.org/10.1007/978-94-007-6116-2_1

Download citation

DOI: https://doi.org/10.1007/978-94-007-6116-2_1

Published:

Publisher Name: Springer, Dordrecht

Print ISBN: 978-94-007-6115-5

Online ISBN: 978-94-007-6116-2

eBook Packages: Business and EconomicsBusiness and Management (R0)