Abstract

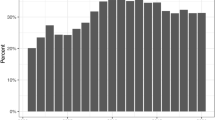

Contagion from Greece, together with domestic political uncertainty in Italy, caused interest rates on Italian sovereign debt to spike in the second half of 2011. As shown in Fig. 1, the risk spread above German bunds for 10-year Italian government bonds rose from 200 basis points in early July 2011, to a range of 300–400 basis points after the July 21 Greek package with its new emphasis on private sector involvement. There was a second surge to the 400–500 basis point range in November through January, following the October 27 Greek package that insisted on a 50 % reduction in private sector claims.

Access provided by Autonomous University of Puebla. Download conference paper PDF

Similar content being viewed by others

Keywords

These keywords were added by machine and not by the authors. This process is experimental and the keywords may be updated as the learning algorithm improves.

Contagion from Greece, together with domestic political uncertainty in Italy, caused interest rates on Italian sovereign debt to spike in the second half of 2011. As shown in Fig. 1, the risk spread above German bunds for 10-year Italian government bonds rose from 200 basis points in early July 2011, to a range of 300–400 basis points after the July 21 Greek package with its new emphasis on private sector involvement. There was a second surge to the 400–500 basis point range in November through January, following the October 27 Greek package that insisted on a 50 % reduction in private sector claims.Footnote 1

Italy 10-year bonds: interest rate and spread over German bunds (basis points) Source Datastream

Even after the improved prospects for implementation of fiscal adjustment under the new government of Mario Monti, on November 25 interest rates reached 6.5 % for six-month treasury bills, 7.8 % for two-year bonds, and 7.3 % for 10-year bonds.Footnote 2 By January 23, 2012, however, the short-term rate had fallen sharply (to 2.2 % for six-month bills) and the long-term rate had eased as well (to 6.1 %).Footnote 3 The decline in the short-term rate reflected the major European Central Bank (ECB) initiative in late December, lending €489 billion to euro area banks for 3 years at 1 % interest.Footnote 4

The decline in the long-term rate may reflect growing confidence that the Monti government will meet fiscal targets and also adopt growth-oriented reforms. Thus, on December 4 the government adopted a package of €20 billion in fiscal cuts designed to eliminate the deficit by 2013.Footnote 5 Then on January 20 the government adopted a set of reforms intended to spur growth. These included the opening of competition among lawyers, taxi drivers, pharmacies, and gasoline stations and liberalizing the markets for gas and electricity, insurance, and local public services.Footnote 6 Both the fiscal and growth reforms were in the form of decree laws that retain force unless rejected by parliament within 60 days.

The recent improvement in Italy’s borrowing conditions is by no means assured to continue. A breakdown in the Greek negotiations with private creditors could cause a new round of contagion. Importantly, monthly amortizations of medium- and long-term debt are to rise from zero in December 2011 and January 2012 to €36 billion in February and €27 billion in March and again in April (Tesoro 2011a). Presumably the government could roll over these maturing bonds with one- to three-year obligations if necessary, in order to take greater advantage of market ease toward the shorter-maturity end given the ECB’s lending program for the banks. Nonetheless, the heavy calendar of amortizations could again test whether and on what terms the government can access the bond market.

In its September 2011 World Economic Outlook (WEO), the International Monetary Fund projected a reduction in Italy’s public debt ratio, from 121 % of GDP in 2011 to 114 % in 2016 (IMF 2011a). This projection is premised on an increase in the primary surplus from 0.5 % of GDP in 2011 to 2.6 % in 2012, 4.1 % in 2013, and 4.5 % thereafter. The growth rates assumed are relatively low even for Italy: an average of 0.78 % annually in 2012–2016.Footnote 7 However, the September IMF projections assumed a relatively benign interest rate outlook. Thus, total net interest payments in 2012 implied an average rate of 4.5 % paid on the end-2011 gross stock of debt.Footnote 8

In contrast, with public debt at about 120 % of GDP, if the average interest rate were to reach 7.5 % the interest burden would reach 9 % of GDP, raising serious questions of sustainability. However, only a fraction of the lower-interest outstanding debt must be rolled over each year. Of about €1.79 trillion in outstanding medium- and long-term debt, only about €190 billion needs to be rolled over (although about €130 billion in short-term debt must also be rolled over annually). So even after several years the average interest rate would remain well below 7 % despite a marginal rate of 7.5 %.

This policy brief examines the sensitivity of the Italian public debt outlook to a new higher-interest-rate environment, as well as to possible shortfalls from fiscal targets. The calculations apply a simple debt projection model (European Debt Simulation Model, or EDSM).Footnote 9

1 Baseline

Table 1 sets forth the relatively benign baseline used by the IMF in its September 2011 World Economic Outlook (IMF 2011a). As discussed below, subsequent updates (IMF 2011b; 2012a) show larger deficits and debt, but appear excessively pessimistic given private sector growth forecasts and recent fiscal measures. The reference baseline for this study thus remains the one used by the IMF in September 2011.

The first five rows in Table 1 show the macroeconomic assumptions in the baseline. Real growth rises to 1.2 % by 2016, but thereafter is set at the 2011–2016 average or 0.8 % per year. The GDP deflator rises at close to 2 % per year. The primary surplus follows the path described above (reverting to the 2011–2016 average of 3.5 % for 2017–2020, beyond the IMF projection period). Because the December 2011 fiscal package set a zero fiscal deficit for 2013 (corresponding to a primary surplus of about 5.5 % of GDP) and by implication beyond, the fiscal assumptions here may substantially overstate future deficits and thus err on the conservative side.

In the next block of the table, the first two rows show that the EDSM closely replicates the IMF’s baseline projection of the ratio of public debt to GDP.Footnote 10 The next three rows show three additional indicators of the debt burden: net debt relative to GDP, interest payments relative to GDP, and amortization (including short-term debt) relative to GDP. The IMF (2011a) places financial assets at €328 billion at end-2011, rising at about €5 billion annually.Footnote 11 After deducting these assets, net debt is about 20 % of GDP smaller than gross debt (end-2011).

The (IMF-based) baseline, with its moderate interest rates and sizable primary surplus target, brings the gross debt ratio down from 122 % of GDP in 2012 to 110 % of GDP by 2020. The interest burden peaks at 5.4 % of GDP in 2013 and then stabilizes at 5.3 % thereafter. Amortization is a relatively steady 15–20 % of GDP, of which about 40 % is annual rollover of short-term debt.

The elements contributing to the borrowing requirement are shown in the next section of the table. For reference, the amount of the primary surplus is first shown. The fiscal deficit is then shown, and is calculated as the amount of interest payments minus the amount of the primary surplus. The total net borrowing requirement equals the fiscal deficit, minus the amount of privatization receipts (absent in Italy’s case). As shown, net borrowing needs ease from €71 billion in 2011 to only €14 billion annually in 2014–2016. The next row shows, however, that annual amortization needs are high, at above €300 billion (including short-term rollover). Amortization on existing medium- and long-term (MLT) debt is from Tesoro (2011a). Amortization on new MLT debt after 2012 is assumed to be at a rate of 10 % of the previous year’s principal outstanding. The gross borrowing requirement is then the sum of net borrowing plus amortization plus increase in financial assets (with the latter set at the levels projected in the September WEO). The gross borrowing requirement for 2012 amounts to about €375 billion. For the 3 years of 2012–2014, the total gross borrowing requirement is €1.02 trillion.

The subsequent rows report total debt outstanding, once again distinguishing old MLT debt from new, and identifying short-term debt. For MLT debt, the year-end level is simply the previous year’s debt, minus amortization in the relevant debt category for the year in question, plus borrowing during the year in the category in question.

The benign outlook in the September 2011 WEO-based baseline suggests sustainability of the debt because of the gradual reduction in the debt to GDP ratio (from 122 % in 2012 to 113 % in 2016 and 110 % in 2020). Net debt declines from a peak of 101 % of GDP in 2012 to 91 % by 2020. Although there is a slight reduction in the interest burden (from a peak of 5.4 % of GDP in 2013 to 5.3 % in 2014 and thereafter, the interest burden is relatively high even at the end of the period. In comparison, for the G-7 as a group, interest payments on public debt in 2011 averaged only 2 % of GDP, and are projected to rise to just 2.9 % by 2016 (IMF 2011a).

As noted, in its January 2012 updates the IMF projected more pessimistic outcomes for growth and fiscal performance than in its September baseline. It placed growth at −2.2 % in 2012 and −0.6 % in 2013, instead of 0.32 % and 0.54 %, respectively (IMF 2012a). The Fund projected the fiscal deficit at 2.8 % of GDP in 2012 and 2.3 % in 2013 (IMF 2012b) instead of 2.6 % in 2012 and 1.2 % in 2013 as in the September WEO. However, private sector growth forecasts anticipate growth of −1.2 % in 2012 and 0.1 % in 2013 (Consensus 2012). The Monti government’s new fiscal program projects the fiscal deficit at 1.2 % of GDP in 2012 and zero in 2013 (Tesoro 2011b). As a result, by end-2013 the cumulative deficit would be 3.9 % of GDP smaller than in the January 2012 IMF projections, and 2013 GDP would be 1.7 % larger.

As a consequence, the January 2012 IMF estimate for the 2013 ratio of debt to GDP, 126.6 % of GDP (IMF 2012b), would be overstated by 3.9 % of GDP in the numerator and understated by 1.7 % in the denominator. Thus, if one applies private sector growth forecasts and the government’s latest fiscal projections, the debt to GDP ratio would stand at 120.6 % (applying the adjustments to the January 2012 IMF estimate for 2013). This level turns out to almost the same as projected in the IMF’s September 2011 WEO (see Table 1). On this basis, the analysis here simply uses that baseline as the reference path rather than adopting the more pessimistic outlook in the January 2012 IMF updates.

2 Impact of Higher Interest Rates

The projections are considerably less favorable if the high interest rates of November 2011 are assumed to return and persist. In the high interest rate (HIR) scenario shown in Table 2, the interest rate block places the rate for new long-term debt at 7.5 %, and for short-term debt at 6.5 %. All other assumptions of the model, including for growth and the primary surplus, remain unchanged. (Table 2 reports only the elements of Table 1 that are changed in the high-interest scenario.)

As shown in the third row of Table 2, the effect of higher interest rates is to reduce substantially the improvement in the debt to GDP ratio achieved in the benign baseline. Thus, the debt ratio by 2020 stands at 118 % of GDP, a modest improvement from 122 % in 2012 but considerably higher than the 110 % reached in the baseline. The net debt ratio shows almost no improvement, easing slightly from 101 % of GDP in 2012 to 99 % by 2020. There is a much higher interest burden, with interest payments rising from 5.2 % of GDP in 2012 to 6.9 % of GDP by 2020 instead of stabilizing at 5.3 % as in the baseline.

Suppose that Italy sought to stabilize the debt to GDP ratio at 110 %, the 2020 level in the benign baseline. With nominal GDP growth at 3 % (1 % real) and the interest rate at 7.5 %, the required long-term level of the primary surplus would be 5.0 % of GDP.Footnote 12 In principle, then, Italy could sustain public debt even at the high 7.5 % interest rate so long as it achieved a primary surplus not much higher than the target of 4.6 % of GDP in the IMF baseline (by 2016; Table 1). Even so, such a scenario would seem vulnerable to the risk of a self-fulfilling prophecy of unsustainability because market fixation on a still high debt ratio could cause further escalation in the interest rate, potentially causing a credit-rationing situation in which at some high interest rate the supply curve for capital would become backward-bending.

The bottom line is that if interest rates were to return to their late-November peak and persist at that level but rise no further, the result would be to thwart the bulk of the earlier potential progress in reducing Italy’s debt ratio over the medium-term, but not to provoke further increases in the debt ratio so long as fiscal adjustment targets were met (indeed there would still be a modest decline).Footnote 13 The downside risk to a fragile sustainability of this nature would be that interest rates (and thus debt) would instead spiral further upwards because of a vicious circle of growing market anxiety about an excessive debt level.

3 Impact of a Lower Primary Surplus

Table 3 reports the results of reverting to the benign interest rates of the WEO baseline but placing a ceiling on the primary surplus at 2.5 % of GDP. In this case the debt to GDP ratio stays virtually unchanged over the decade, ending at 123 % of GDP in 2020. The lower primary surplus thus has a more damaging effect than that in the scenario for higher interest rates. (Again, all elements not reported in Table 3 remain unchanged from the values shown in Table 1.)

Finally, Table 4 shows the effect of an adverse combination of interest rates and primary surplus. The interest rates are at their late-2011 high levels throughout (same as in Table 2), and the primary surplus does not surpass 2.5 % of GDP (same as in Table 3). The result is a severe worsening in the debt problem. The ratio of gross debt to GDP reaches 132 % by 2020.

Figure 2 shows the trends in the four debt indicators for the four scenarios. The graph of the debt to GDP ratio confirms at a glance the contrast between significant improvement in the benign baseline; much less improvement in the high interest case and stagnation in the low primary surplus case; and escalation to a substantially worse debt burden if high interest rates and the low primary surplus occur jointly. The same pattern is broadly shown by the net debt ratio. The amortization rates are much more similar across the cases but begin to show the corresponding dispersion toward the end of the period. Importantly, the interest burden of the debt shows substantial escalation of the debt burden even in the high-interest-only (HIR) case, and is the worst in the joint HIR and low primary surplus case (HIRLPS). The interest burden rises slightly in the low primary surplus case, and as noted above, even in the benign base case the interest burden over time remains almost unchanged at a relatively high level.

European debt simulation model, Italy (with short-term debt, as of end-September, 2011)

4 Risk of a Liquidity Squeeze

Even at its peak levels, the interest rate shock to Italian public debt that occurred in the fourth quarter of 2011 would not necessarily be fatal to Italy’s debt sustainability. Basically if it persisted it would prevent much of the improvement that otherwise would have occurred in the debt indicators as a consequence of fiscal adjustment aimed at a primary surplus over 4 % of GDP. However, at such interest rates, on the order of 7.5 %, there could be liquidity problems even if it were judged that Italy remained solvent at a debt ratio of slightly below 120 % that did not escalate over time. The fragile condition of the financial market for European sovereign debt in the wake of the Greek haircuts and the specter of possible exit of some economies from the euro means that it could prove difficult to avoid an upward escalation of the interest rate beyond late-November levels and even a failure to roll over debt coming due.

Monthly redemptions of short-, medium-, and long-term debt, which were €30.6 billion in November and €22.5 billion in December, eased temporarily to €15.2 billion in January, but then will surge to €53.1 billion in February and €44.2 billion in March (Tesoro 2011a). In the absence of a major policy change, it seems unlikely that ECB purchases through its Securities Markets Program (SMP) could provide a major part of the demand for the rollover financing. After virtually no net purchases in May through July, 2011, ECB net purchases in the program reached an average of €33 billion monthly in August–November 2011. However, the average fell to only about €7 billion in December 2011 and January 2012.Footnote 14 Even if the ECB were to return to the higher pace of purchases in August–November, with Italy accounting for 57 % of total debt of the five troubled periphery economies (IMF 2011a), its share in the purchases would amount to no more than €20 billion monthly, far below the February and March amortization totals.Footnote 15 Moreover, the ECB has emphasized that it sees even its recent SMP purchases as temporary, and has signaled strongly that it is not prepared to engage in much larger and prolonged purchases.

5 Conclusion

In terms of long-term solvency, Italy is not close to a precipice and could keep its debt ratio from escalating even if the recent peak interest rates on its debt (about 7.5 %) were to return and persist for a long time (but rise no higher). However, there is a considerable chance that Italy would face a severe liquidity squeeze under these circumstances. It thus behooves the official sector in Europe and internationally to move quickly to provide some credible lender of last resort vehicle in the immediate future. So far the October 26 pledge of leveraging the financing capacity of the European Financial Stability Facility (EFSF) and alternative proposals of launching euro area bonds jointly or with partial guarantees have bogged down.

The December 9 EU commitment to lend €200 billion to the IMF, to be supplemented by lending from other countries (especially emerging market economies with large reserves) was a useful first step toward building a firewall. Similarly, the ECB’s large package of 3-year lending to the banks at end-2011 helped ease sovereign borrowing conditions. Nonetheless, further steps to expand the EFSF (and its successor European Stability Mechanism, ESM) or launch eurobonds should be pursued promptly, without lengthy procedural delay for institutional change. Constructing a credible lender of last resort would reinforce the momentum of recent improvement in Italian spreads, and go a long way to ensuring that a liquidity crisis does not provoke an Italian moratorium and thereby inflict severe damage on the Italian, euro-area, and world economies.

Notes

- 1.

Previously published as Policy Brief PB12-5, Peterson Institute for International Economics, Washington, February 2012. Reproduced by permission.

- 2.

Neil Dennis and Guy Dinmore, Italian short-term borrowing costs surge, Financial Times, November 25, 2011; and Datastream.

- 3.

By February 1–6 the 10-year rate had improved further, falling to an average of 5.7 %. Data are from Bloomberg and Datastream.

- 4.

Rita Nazareth, US Stocks Decline as ECB Lends Record Amount, Bloomberg, December 21, 2011.

- 5.

The measures included an increase in the minimum pension age, a new property tax, a potential increase in the value added tax by 2 percentage points by September 2012, and new taxes on luxury goods. Cash transactions exceeding €1,000 were banned in an attempt to curb tax evasion. Giuseppe Fonte, Italy PM unveils sweeping austerity package, Reuters, December 4, 2011.

- 6.

Guy Dinmore and Giulia Segreti, Monti unveils liberalization plans, Financial Times, January 20, 2012.

- 7.

Note that whereas the growth rates for 2012 and 2013 in the IMF baseline may be somewhat optimistic, because the government now expects a decline of GDP by 0.4–0.5 % in 2012 and zero growth in 2013, the fiscal assumptions are understated considering the new target of zero deficit by 2013 in the December fiscal package, in contrast to the 1.5 % of GDP deficit assumed in the IMF projections. Fonte, op. cit.

- 8.

Net interest payments are €80.7 billion (the difference between primary and total fiscal balance). With financial assets at €328 billion, and assuming earnings at 2 % on these assets, gross interest payments are €87.3 billion, or 4.5 % of end-2011 gross debt of €1.92 trillion (IMF 2011a).

- 9.

For a description of the model, see Cline (2011).

- 10.

The table presents an estimated decomposition of the debt into medium- and long-term (MLT) pre-2012; new MLT debt borrowed in 2012 and after; and short-term debt, assumed to be rolled over at the end-2011 level. The interest rate on pre-2012 debt is based on total interest payments after taking account of earnings on assets (at 2 %) and interest on short-term debt at a lower rate. For 2012 and after, the interest rate on new MLT debt is imputed at rates likely to have been applied at the time of the September WEO: a spread of 300 basis points above the German 10-year bund in 2012, 250 basis points in 2013, and 200 basis points thereafter. The bund rate is shown in the table as well, and is taken from IMF (2011c).

- 11.

The Organization for Economic Cooperation and Development (OECD 2011) places financial assets even higher, at €450 billion at end-2011.

- 12.

The debt-ratio-stabilizing primary surplus as a percent of GDP is: π = λ (r − g), where λ = debt/GDP, r is the interest rate, and g is the nominal growth rate; see Cline (2010).

- 13.

A somewhat more optimistic conclusion is reached by Banca d ’Italia (2011: 14–15). In its baseline the debt to GDP ratio declines from 120.5 % in 2011 to 112.5 % by 2014. In its simulation increasing the interest rate on new borrowing by 250 basis points, there is still a decline in the debt ratio to 115.5 % of GDP by 2014. The difference reflects a more optimistic fiscal baseline (overall surplus of 0.2 % of GDP by 2014 instead of a deficit of 0.8 %, Table 1), and higher projected growth (an average of 0.9 % annually in 2012–2014 versus 0.55 %). The incremental impact of the higher interest rate scenario is broadly consistent with, albeit somewhat stronger than, that found here. A 2.5 % increase in the interest rate on new borrowing boosts the debt/GDP ratio by 2.9 % of GDP by 2014. In comparison, in the calculations here, an increase in the new borrowing interest rate by 1.7 % point above its baseline average of 5.4 % (MLT and short-term weighted average) raises the debt/GDP ratio by 1.2 % of GDP by 2014. The difference reflects the Bank of Italy’s use of summary elasticities of outlay with respect to the interest rate, in contrast to actual application to new borrowing projections in Table 2.

- 14.

Based on amounts outstanding in the weeks ending April 29, 2011 (€76 billion), July 29 (€74 billion), December 2 (€206.5 billion), and January 20, 2012 (€219 billion). ECB, Weekly Financial Statements, press releases. Available at www.ECB.int.

- 15.

Note further that the ECB’s SMP purchases are on the secondary market. Nonetheless, their effect should be broadly comparable to purchases in initial auctions.

References

Banca d’Italia (2011) Financial stability report no. 2. Rome

Cline WR (2010) A note on debt dynamics. Peterson Institute for International Economics, Washington

Cline WR (2011) Sustainability of Greek public debt. PIIE policy brief PB11-15. Peterson Institute for International Economics, Washington

Consensus (2012) Consensus forecasts. Consensus Economics, London

IMF (International Monetary Fund) (2011a) World economic outlook database. International Monetary Fund, Washington

IMF (International Monetary Fund) (2011b) Fiscal monitor: addressing fiscal challenges to reduce economic risks. International Monetary Fund, Washington

IMF (International Monetary Fund) (2011c) Greece: fifth review under the stand-by arrangement. Country report no. 11/351. International Monetary Fund, Washington

IMF (International Monetary Fund) (2012a) World economic outlook update. International Monetary Fund, Washington

IMF (International Monetary Fund) (2012b) Fiscal Monitor Update. International Monetary Fund, Washington

OECD (Organization for Economic Cooperation and Development) (2011). Economic outlook, no. 89. Organization for Economic Cooperation and Development, Paris

Tesoro (2011a) Departamento del Tesoro, Outstanding of public securities (breakdown by maturity). Ministero dell’Economia e delle Finanze, Rome

Tesoro (2011b) Relazione al Parlamento 2011. Presentata dal Presidente del Consiglio dei Ministri e Minstro dell’Economia e delle Finanze Mario Monti. Ministero dell’Economia e delle Finanze. Rome. Available at: http://www.dt.tesoro.it/export/sites/sitodt/modules/documenti_en/analisi_progammazione/documenti_programmatici/Relazione_2011_xPROTETTOx.pdf

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2013 Springer-Verlag Italia

About this paper

Cite this paper

Cline, W.R. (2013). Interest Rate Shock and Sustainability of Italy’s Sovereign Debt. In: Paganetto, L. (eds) Public Debt, Global Governance and Economic Dynamism. Springer, Milano. https://doi.org/10.1007/978-88-470-5331-1_19

Download citation

DOI: https://doi.org/10.1007/978-88-470-5331-1_19

Published:

Publisher Name: Springer, Milano

Print ISBN: 978-88-470-5330-4

Online ISBN: 978-88-470-5331-1

eBook Packages: Business and EconomicsEconomics and Finance (R0)