Abstract

This chapter examines the nature of bank-Firm relationships in Japan by investigating firms’ cash holding behavior based on a panel dataset of Japanese firms for the 2000s provided by Teikoku Databank. This dataset has the virtue of identifying firms’ main bank(s) or financial institution(s) with which they have a close relationship. This information is used to characterize the cash holding behavior of firms with varying degrees of closeness in their relationships with banks. The findings indicate that having a main bank relationship helps client firms in their cash management in two important ways. First, firms need to hold less cash for precautionary motives because main banks are ready to provide them with liquidity on a rainy day. Second, main banks can cushion shocks to client firms, so that client firms can keep the adjustment of cash holdings to such shocks to a minimum. However, client firms pay a price for maintaining long-term, stable relationships with main banks, namely, the monopoly rent imposed by main banks on their client firms in the form of a higher effective borrowing rate.

Access provided by Autonomous University of Puebla. Download chapter PDF

Similar content being viewed by others

Keywords

1 Introduction

Cash is held by firms for a number of reasons. In his general theory, Keynes argues that cash is held for three reasons, namely, transaction, precautionary, and speculative motives. The transaction demand for cash has been further elaborated by Baumol (1952), Tobin (1956), and Miller and Orr (1966). Since then, a number of theoretical and empirical studies have focused on the cash holding behavior of firms. Opler et al. (1999) and Bates et al. (2009) provide comprehensive surveys of the demand for cash by firms. Two further motives for a firm’s cash holdings have been added to the traditional ones: tax and agency motives, as shown by Bates et al. (2009). Regarding agency motives, Jensen (1986) argued that entrenched managers retain cash when a firm has poor investment opportunities. Jensen’s argument is also supported by Dittmar et al. (2003), Dittmar and Mahrt-Smith (2007), and Pinkowitz et al. (2006). These authors all found that greater agency problems lead to larger cash holdings.

In Japan, agency cost problems are mitigated to a large extent by long-term, stable bank-firm relationships, known as the main bank system. A firm’s main bank is frequently defined as the bank that holds the largest share of that firm’s loans. However, main bank relations are not simply confined to lending relationships and cover a wide spectrum of dealings.Footnote 1 Main banks hold a large share of the loans of client firms, which gives them a strong incentive to collect information about firms’ prospects and to monitor them.Footnote 2 This helps mitigate problems with information asymmetry, which can lead to adverse selection and moral hazard. Main banks also often hold both client firm debt and equity, which in terms of the agency cost approach implies that one would expect Japanese firms to hold less cash. However, Pinkowitz and Williamson (2001) found that Japanese firms in fact hold more cash than U.S. or German firms.Footnote 3 They argued that the dark side of the main bank system, namely, rent extraction, is responsible for these larger cash holdings. When a main bank exerts its monopoly power, it forces client firms to hold more cash reserves in the main bank’s account. By doing so, the main bank can extract monopoly rent in the form of a higher effective borrowing rate by way of a compensating balance. Thus, two opposing forces are operating to affect cash holdings under the main bank system. This means that by examining firms’ cash holding behavior, it may be possible to illuminate the nature of bank-firm relationships in Japan. This is the main purpose of this chapter.

The strategy employed to examine the nature of bank-firm relationships is to estimate a demand equation for firms’ cash holdings. The estimation is based on a unique panel dataset of Japanese firms in the early 2000s provided by Teikoku Databank, Ltd. This dataset has the virtue of identifying the financial institutions with which a firm has transaction relationships in terms of loans, bills discounted, and time deposits. Using this dataset, it is possible to estimate separate demand equations for cash for different groups of firms in order to examine firms’ cash holding behavior and, based on this analysis, make inferences on the nature of bank-firm relationships in Japan.

The main findings of the analysis can be summarized as follows. The results suggest that firms that have close ties with their main bank tend to hold less cash and the cash flow sensitivity of cash is low. This implies that main banks act as a buffer by providing liquidity to mitigate external shocks to their client firms. However, the effective borrowing rates for these firms are significantly higher than the nominal borrowing rates and are positively related to the degree to which firms depend on their main banks (as measured by the share in total loans that the main banks account for). Thus, main banks extract monopoly rents from close client firms. In other words, having strong ties with a main bank allows firms to have lower cash holdings than would otherwise be the case but comes at the expense of a higher effective borrowing rate due to the monopoly rent extracted by main banks. In contrast, for firms with only weak ties to their main banks, cash holdings are not correlated with dependence on bank debt and the cash flow sensitivity of cash is high.

The remainder of this chapter organized as follows. Section 11.2 presents the hypotheses concerning the effects of bank-firm relationships on cash holdings within the framework of a firm’s demand equation for cash. Section 11.3 then explains the dataset used for the empirical analysis and presents some descriptive statistics on cash holdings. Next, Section 11.4 presents the estimation results, which allow inferences on the nature of bank-firm relationships in Japan. Finally, Section 11.5 concludes.

2 Bank-Firm Relationships and Cash Holdings: Formulation of Hypotheses

Firms’ relationship with their bank(s) affects firms’ cash holdings in a number of ways. Specifying a firm’s demand function for cash helps to clarify the channels through which such bank-firm relationships affect a firm’s cash holdings. Bates et al. (2009) classified a firm’s demand for cash into four motives: the transaction, precautionary, agency, and tax motive. This chapter primarily focuses on the first three motives and identifies explanatory variables corresponding to each motive.

The benchmark demand function for cash holdings is specified as follows:

where \({{v}_{i}}\): firm-specific term, and

\({{u}_{it}}\): disturbance term.Footnote 4

The dependent variable is the change in cash holdings (\(\Delta CASH\)) divided by total assets (TA). The explanatory variables are categorized into three groups to capture each of the motives mentioned above.

2.1 The Transaction Motive and Bank-Firm Relationships

This section explains the variables used to represent the transaction motive of cash holdings and how the transaction motive is affected by bank-firm relationships. The growth rate of real sales \((\Delta \log {{(SALES )}_{it}})\)represents a firm’s current activities as well as future investment opportunities.Footnote 5 Higher sales growth might be sustained by retaining more cash. Moreover, firms whose access to credit is constrained can use cash to make profitable investments in the future. Therefore, \({{\alpha }_{1}}\)is expected to be positive. Evidence suggests that there are economies of scale in holding cash (e.g., Mulligan 1997). Using the logarithm of real total assets to measure firm size, it is expected that the coefficient on this (\({{\alpha }_{2}}\)) will be negative.

A change in net working capital (NWC), defined as current assets minus current liabilities minus cash, is a substitute for cash and \({{\alpha }_{3}}\)is therefore expected to be negative. When a firm has a close relationship with its main bank, the bank will provide short-term loans when net working capital is scarce; thus, the firm does not have to keep liquidity by drawing out cash. That is, the absolute value of \({{\alpha }_{3}}\) will be smaller for a firm with a close relationship with its main bank.

2.2 The Precautionary Motive and Bank-Firm Relationships

Firms will save part of their cash flow for precautionary purposes. Thus, the propensity to save \({{\alpha }_{4}}\) will be positive. Almeida et al. (2004) demonstrated theoretically and empirically that the propensity to save is higher for financially constrained firms.Footnote 6 When the bank-firm relationship is strong, the client firm expects its main banks to provide liquidity on a rainy day, so that the firm does not need to save a lot from cash flow. Thus, the propensity to save from cash flow will be lower for a firm with close ties with its main banks.

The same argument holds for the effects of cash flow volatility on cash holdings. Han and Qiu (2007) extended the model of Almeida et al. (2004) to allow for a continuous distribution of cash flow and then theoretically showed that an increase in the volatility of cash flow increases cash holdings for financially constrained firms.Footnote 7 This implies that there is a positive relationship between the standard deviation of cash flow to total assets (SDCFRATIO) and cash holdings (\({{\alpha }_{5}}>0\)). When the relationship between a firm and its main banks is strong, the firm expects its main banks to provide liquidity in times of uncertainty; therefore, coefficient \({{\alpha }_{5}}\) will be smaller for firms with a close relationship with their banks.

2.3 The Agency Motive and Bank-Firm Relationships

When a firm’s debt reaches a certain level relative to equity, it faces a high risk of default and the cost of outside finance increases as a result. To avoid this situation, a debt-ridden firm will use cash to repay debt, so that the coefficient on the debt/asset ratio, \({{\alpha }_{6}}\), is expected to be negative.Footnote 8 When the firm has a close relationship with its main bank, the main bank performs a monitoring and disciplinary role, so that the cost of financial distress will be lower and the firm does not necessarily have to pay back debt using cash. Thus, the absolute value of \({{\alpha }_{6}}\) will be smaller for a firm with a close bank-firm relationship.

To measure a firm’s dependence on banks, the ratio of debt outstanding with banks (BANKDEBT) to its total debt (DEBT) is used. When this ratio is high, the firm is likely to have a strong relationship with its bank(s). Therefore, the coefficient on the bank dependence variable, \({{\alpha }_{7}}\), picks up the direct effect of bank-firm relationships on cash holdings. That is, a firm with strong ties to banks may hold less cash in the expectation that the banks will provide liquidity on a rainy day. In this case, \({{\alpha }_{7}}\) will be negative. At the same time, however, when bank-firm relationships are strong, the banks may extract monopoly rents by forcing client firms to keep a large amount of cash in their accounts. In this case, \({{\alpha }_{7}}\) will take a positive value.

Another variable employed is MAINDEP, the dependence of a firm on its main bank. The MAINDEP variable is defined as the proportion of borrowing from the main bank to total bank debt. Again, a strong main bank relationship may reduce a firm’s demand for cash holdings, since the firm expects its main bank to provide liquidity on a rainy day. In this case, \({{\alpha }_{8}}\) will be negative. On the other hand, the main bank might extract monopoly rents by forcing the client firm to keep a large amount of cash in its bank account. In this case, \({{\alpha }_{8}}\) will positive.

The final variable used is the lagged cash/asset ratio, which measures the adjustment speed of cash holdings toward the optimal target.Footnote 9 In addition, year dummies (YEARDUM) are included in the estimation to control for macro shocks common to all firms in the sample.

Table 11.1 provides a summary of the responses of cash to its determinants and how they are affected by bank-firm relationships. Section 11.4 provides an empirical investigation of these effects.

2.4 Bank-Firm Relationships and Effective Borrowing Rates

When a main bank makes loans to a client firm, the firm is sometimes required to deposit part of its loans into the main bank’s account. This practice raises the effective borrowing rate for the client firm. Specifically, denoting the nominal borrowing rate and the deposit rate by \({{r}_{L}}\text{ and }{{r}_{D}}\), respectively, the effective borrowing rate (\(r_{L}^{*}\)) when a firm borrows \({{B}_{L}}\)and deposits part of the borrowed money, say \(D(<{{B}_{L}})\), into its account with the main bank, is calculated as follows:

It is easy to show that \(r_{L}^{*}>{{r}_{L}}\) as long as \({{r}_{L}}>{{r}_{D}}\). In the empirical analysis in Section 11.4, the effective borrowing rate for each firm is calculated and the correlation between these effective borrowing rates and bank-firm relationship variables is examined.

3 Data Characteristics and Descriptive Statistics of Cash Holdings

This section explains the dataset used for the empirical analysis and provides descriptive statistics of cash holdings as well as major firm attributes.

3.1 Dataset Characteristics

The Teikoku Databank (TDB) database is a very unique and extensive dataset on Japanese firms. The dataset was constructed by a group of researchers involved in the Program for Promoting Social Science Research Aimed at Solutions of Near-Future Problems “Design of Inter-firm Network to Achieve Sustainable Economic Growth” in collaboration with Teikoku Databank, Ltd., the largest credit information provider in Japan. The dataset contains information on nearly 400,000 firms in Japan, including the financial transactions between firms and financial institutions as well as firms’ basic attributes and financial statements. A detailed explanation of the data from Teikoku Databank, Ltd. is provided in Uchida et al. (2011) and Ono et al. (2011).

The TDB dataset provides rich information on bank-firm relationships. First of all, the dataset makes it possible to identify a firm’s “main bank.” The main bank is defined as the financial institution with which the firm thinks it has the closest relationship.Footnote 10 Thus, the definition of a main bank is somewhat subjective. In addition, the amount of loans outstanding, bills discounted, and time deposits are also available for each bank-firm relationship.

The financial statements of firms are available from 2001 to 2009, although detailed information regarding bank-firm relationships is available only from 2007 to 2010.Footnote 11 Therefore, in the analysis here, firms’ cash holding behavior is examined for two periods: the whole observation period from 2001 to 2009 and the sub-period from 2007 to 2009, for which detailed information regarding bank-firm relationships is available.

For the empirical analysis, firms from non-profit-oriented industries and financial firms are excluded. Regarding the legal form of firms, the following types of firms are included in the sample: joint stock companies, closely-held limited liability companies, limited partnership companies, unlimited liability partnership companies, limited liability partnerships, medical associations, cooperative partnerships, and sole proprietorships.

3.2 Descriptive Statistics

Table 11.2 presents descriptive statistics of the major firm characteristics (total assets, growth rate of real sales, debt/asset ratio, ratio of short-term and long-term bank debt to total debt, and return on assets (ROA)) in terms of median values for 2001 to 2009.Footnote 12 The median value of total assets is considerably smaller than the mean. For example, the median of total assets in 2001 was 227.7 million yen, while the mean was 4,145.2 million yen. This implies that the size distribution is skewed to the right. The sales growth rate exhibits an increasing trend up to 2006 and then falls sharply in 2009. The debt/asset ratio declined gradually during the observation period from 0.8161 in 2001 to 0.7611 in 2009. Dependence on bank debt, measured by bank debt to total debt, remained rather stable during the observation period, hovering around 0.57 to 0.58. The ROA exhibits an increasing trend in the first half of the 2000s, reaching a peak in 2006 and then declining thereafter.

Table 11.3 shows the median values of the annual cash/asset ratio during the observation period. The cash/asset ratio is defined as the ratio of cash and deposits to total assets. The cash/asset ratio remained relatively stable, ranging from 0.1532 to 0.1667, during the observation period. The third and fourth columns show the cash/asset ratio by firm size. Large firms consist of firms whose total assets are larger than the sample median and small firms of firms whose total assets are smaller than the sample median. Comparing the figures in the two columns shows that the cash/asset ratio of small firms throughout the observation period is about 3–6 % points higher than that of large firms, reflecting economies of scale in cash holdings. Next, in the fifth and sixth columns, firms are divided into those whose ratio of bank debt to total debt is above and below the sample median, with the former being considered to be bank dependent and the latter not dependent. The fifth column shows the cash/asset ratio of bank-dependent firms and the sixth column shows that of firms that are not bank dependent, and comparing the two columns shows that the cash/asset ratio is slightly smaller for bank-dependent firms. However, the difference is at most 1.2 % points, far less than the difference by firm size. Finally, the seventh and eighth columns show the cash/asset ratio dividing firms in terms of the volatility of their cash flow. Volatility of cash flow is measured in terms of the standard deviation of the ratio of cash flow to total assets over the current and past two years. Firms with a high volatility of cash flow are those whose standard deviation is larger than the sample median and firms with a low volatility are those whose standard deviation is smaller than the median. Throughout the period, the cash/asset ratio is 0.8–3.4 % points higher for firms with a higher cash flow volatility, reflecting a higher precautionary demand for cash.

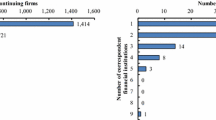

Next, let us look at some descriptive statistics regarding the link between bank-firm relationships and cash/asset ratios. Figure 11.1 shows a histogram of the number of main banks in 2008. Nearly two-thirds of firms in the sample have one main bank, while 7 % of firms have two main banks. It is surprising that 27 % of the sample firms do not have any specific main bank.Footnote 13 Table 11.4 shows the cash/asset ratio for six groups of firms categorized in terms of their number of main banks and whether they are classified as bank dependent or not. The cash/asset ratio is lowest for bank-dependent firms with one main bank (0.1364), while it is highest for firms that are not bank-dependent and have no main bank (0.1770). Note that the cash/asset ratio is rather high for firms that are not bank-dependent and have more than one main bank (0.1754).

Histogram of number of main banks: 2008

4 Bank-Firm Relationships and their Effect on Firms’ Cash Holdings: Empirical Evidence

Section 11.2 suggested that bank-firm relationships affect firms’ cash holdings in a variety of ways. Bank-firm relationships affect not only the level of cash holdings but also the way that cash demand responds to various factors. This section provides some empirical evidence on the impact of bank-firm relationships on firms’ cash holdings.

4.1 Estimation Results for the Whole Observation Period: 2001–2009

Table 11.5 shows the estimation results of the cash holdings equation for the whole observation period from 2001 to 2009. In the estimation, the top and bottom 1 % tails of the dependent and explanatory variables are trimmed. All explanatory variables in the baseline estimation for all firms have coefficient estimates consistent with theory and are statistically significant at the 1 % level. The level of bank debt relative to total debt (BANK DEBT) has a negative effect on cash holdings, implying that bank-dependent firms tend to hold less cash.

The next two columns of Table 11.5 report the results when estimating the cash holdings equation for bank-dependent firms and non-dependent firms separately. Again, all the coefficient estimates are significant and consistent with theory. Comparing the results in the two columns shows that cash holdings are less sensitive to net working capital, cash flow, and cash flow volatility for bank-dependent firms. This result suggests that bank-dependent firms seem to expect that financial institutions are ready to provide liquidity when needed.

To check the robustness of the results, the cash holdings equation is estimated using an instrumental variable (IV) approach. It is highly likely that the sales growth rate, net working capital, and cash flow are endogenous in the sense that common unobservable shocks simultaneously affect cash holdings and these variables. Therefore, the first-differenced cash equation is estimated using the IV method with the twice-lagged cash/asset ratio, sales growth rate, ratio of net working capital to total assets, ratio of cash flow to total assets, ratio of tangible fixed assets to total assets, ratio of intangible fixed assets to total assets, and ratio of inventory assets to total assets as instruments.Footnote 14 It turns out that some of the important variables such as the sales growth rate, the debt/asset ratio, cash flow, and the volatility of cash flow are insignificant, possibly because those variables are endogenous and the employed instruments are weak. The findings above suggested that changes in bank-dependent firms’ cash holdings are less sensitive to net working capital and cash flow. Thus, this result supports the finding above that bank-dependent firms appear to expect that their bank will shield them from an external shock by providing liquidity when needed.

In the following analysis, the discussion will be based on panel estimations rather than IV estimations, which may yield estimates with large standard errors due to the weak instruments problem.

4.2 Estimation Results for the Sub-Period: 2007–2009

Shortening the observation period to 2007–2009 means that detailed information on bank-firm relationships such as the number of main banks and main banks’ share of loans and time deposits are available, making it possible to add firms’ dependence on their main bank—represented by MAINBANK and defined as the main bank’s share in a firm’s total loans—as a variable in the estimation. Further, it also becomes possible to split firms based on the number of main banks and their dependence on bank debt to examine how the response of cash holdings to various factors varies across firms with different degrees of closeness to their bank. Starting with the results of the baseline estimation in Table 11.6, all the coefficient estimates (with the exception of those for the sales growth rate and the volatility of the cash flow ratio) are statistically significant and consistent with theory. The results show that firms with a higher level of bank debt to total debt have lower cash holdings, which supports the finding obtained for the observation period as whole. In addition, firms that are more dependent on their main bank tend to have lower cash holdings.

The third and fourth columns of Table 11.6 report the results when splitting the sample into bank-dependent and non-bank-dependent firms. The results indicate that cash holdings are less sensitive to net working capital, cash flow, and cash flow volatility in the case of bank-dependent firms.Footnote 15 Further, close bank-firm relationships play an important role in allowing firms to hold less cash as they know their bank will provide liquidity on a rainy day. Regarding the effect of main bank dependence on cash holdings, regardless of firms’ level of bank debt to total debt, firms whose main bank accounts for a higher share of loans tend to have a lower cash/asset ratio.

To examine how the main bank relationship affects a firm’s cash holdings, the sample is split into six groups of firms based on the number of main banks (none, one, and more than one) and the median of bank debt/total debt, and the cash holdings equation is then estimated separately for each group of firms. Table 11.7 reports the results, which show that the main bank relationship is closest when firms have only one main bank and the bank debt/total debt ratio is above the median. When the main bank relationship is very close, the coefficient estimates indicate that for this group of firms, cash holdings are least sensitive to the level of working capital, cash flow, and cash flow volatility. Moreover, only for this group of firms is the share of loans from the main bank associated with a significantly lower level of cash holdings. This implies that firms with close links with their main bank can keep their cash holdings at a minimum in the knowledge that if they are hit by an external shock that affects cash holdings their bank will help them out. Thus, main banks play a vital role in the liquidity management of their client firms.

Next, let us examine the cash holding behavior of firms that have the weakest ties with their main banks. These firms are the non-dependent firms with no main bank or with more than one main bank. The results indicate that the absolute value of the coefficient on net working capital is largest for non-dependent firms with no main bank, followed by non-dependent firms with more than one main bank. This implies that for these firms cash holdings and net working capital are close substitutes. The same observations hold for cash flow. The coefficient estimates for cash flow are 0.5382 and 0.4941 for non-dependent firms with no main bank and with more than one main bank, respectively. These firms save nearly half of their cash flow in the form of cash. Firms with the weakest or no main bank relationship have to rely on their own liquidity and hence their cash holdings are quite sensitive to changes in the determinants of cash demand.

Finally, it should be noted that the absolute value of the coefficient on the debt/asset ratio is largest for non-dependent firms with no main bank, reflecting that these firms have a strong incentive to use cash to redeem debt to lower the cost of external finance.

4.3 Monopoly Rents

As stated in Section 11.2, main banks can extract monopoly rent by requiring their client firms to deposit back part of their loans. To gauge the extent to which main banks extract monopoly rent, the effective borrowing rate is calculated in this section by taking this compensating balance practice into consideration. The monopoly rent can then be defined as the difference between the effective borrowing rate and the nominal borrowing rate. The results indicate that the monopoly rent thus calculated is statistically significant and that, moreover, bank-dependent firms with more than one main bank relationship pay higher monopoly rent when the share of borrowing from main banks gets higher.

Specifically, the effective borrowing rate based on Eq. (11.2) is calculated using the amount of time deposits held in the main bank’s accounts and the amount of loans outstanding from the main bank as collected by TDB. The nominal borrowing rate (BRATE) can be calculated from information in firms’ profit-and-loss and balance sheet statements. It is assumed that deposit rates (DRATE) are the same for all sample firms but depend on the amount deposited.Footnote 16

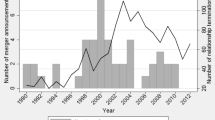

Figure 11.2 Presents histograms of the monopoly rent calculated for four different groups of firms classified in terms of the number of main banks (one and more than one) and their bank debt/total debt ratio.Footnote 17 The histogram of the monopoly rent of firms with a very close main bank relationship (bank-dependent firms with one man bank) resembles that of firms with a weak main bank relationship (non-dependent firms with more than one man bank). As for the descriptive statistics of the histograms, the median of monopoly rents is 27 basis points for the former group and 41 basis points for the latter. The proportion of firms for which monopoly rents are less than 50 basis points is 69.3 % for the former and 56.2 % for the latter.Footnote 18

Histograms of monopoly rent. (Source: Author’s calculation based on Teikoku Databank data.)

To further examine how monopoly rents are related to firm–bank relationships, the monopoly rent is regressed on a constant and the main bank’s share of loans for each of the four groups of firms. The results are reported in Table 11.8. The constant is significant for all groups except for bank-dependent firms with more than one main bank. The results thus indicate that statistically significant monopoly rents for these three groups of firms can be detected.

On the other hand, for bank-dependent firms with more than one main bank the coefficient on the main bank’s share of loans is significantly positive, which implies that the closer the main bank relationship is, the more monopoly rent the client firm has to pay.

Note that the existence of monopoly rents and lower cash holdings are not mutually exclusive. Consider, for example, the case where a firm holds a small time deposit, but the time deposit is exclusively held in its main bank’s account. The main bank can then extract monopoly rent from its client firm.

5 Concluding Remarks

The aim of this chapter was to illuminate the nature of bank-firm relationships in Japan by looking at the cash holding behavior of firms. The findings suggest that main banks help their client firms manage liquidity in two important ways. First, firms need to hold less cash for precautionary motives because main banks are ready to provide client firms with liquidity on a rainy day. Second, main banks can help to cushion unexpected shocks experienced by client firms, so that client firms can keep to a minimum the extent to which cash holdings are adjusted in response to an external shock. These are the advantages of establishing a long-term, stable relationship with a main bank.

However, client firms do pay a price for maintaining bank-firm relationships, namely the monopoly rent imposed on firms in the form of higher effective borrowing rates. Higher effective borrowing rates may lower firms’ fixed investment and R&D activities, which would otherwise enhance their productivity to attain higher growth.

Thus, an important question is whether the benefits of maintaining a main bank relationship exceed the costs. This is an issue of considerable interest for future research.

Notes

- 1.

Aoki et al. (1994) stressed five aspects of main bank relations: the lending relationship, client issuances of public debt, equity cross-shareholding, business settlement accounts, and the provision of information services and managerial resources.

- 2.

- 3.

A more recent empirical study on the cash holdings of Japanese firms is Hori et al. (2010). The firms in their panel dataset are listed firms.

- 4.

Subscripts i and t represent the firm and the year, respectively.

- 5.

In the literature, a widely used proxy to represent future investment opportunities is the market-to-book ratio. However, this ratio cannot be defined for unlisted firms, which make up a large part of the dataset used here.

- 6.

Riddick and Whited (2009) showed the opposite; they derived a negative relationship between cash flow and cash when current cash flow reveals future productivity shocks.

- 7.

Baum et al. (2008) also found that firms increase their liquidity when macroeconomic uncertainty or idiosyncratic uncertainty increase.

- 8.

That being said, Acharya et al. (2007) demonstrated that for constrained firms with high hedging needs the relationship between cash flow and debt as well as that between cash flow and cash holdings should be positive.

- 9.

Another potential determinant of the demand for cash holdings is capital expenditure. The reason that capital expenditure is not included as an explanatory variable here is that doing so would give the cash holding equation more the character of an accounting identity. R&D expenditure is also frequently used as a proxy of growth opportunities. However, R&D expenditure is not available for most of the small, unlisted firms in the dataset used here.

- 10.

Financial institutions include both deposit-taking financial institutions and non-banks.

- 11.

For some firms, financial statements are available as far back as the 1990s.

- 12.

ROA is defined as the ratio of current net income to total assets.

- 13.

The histogram for 2009 is quite similar to that for 2008, while in 2007, 74 % of the sample firms have one main bank, 11 % have two main banks and 12 % have no main bank.

- 14.

The ratio of tangible fixed assets to total assets, the ratio of intangible fixed assets to total assets, and the ratio of inventory assets to total assets are used as instruments, since they are expected to be correlated with cash flow. The estimation results are not shown to save space, but are available from the author upon request.

- 15.

The coefficient estimate for cash flow volatility is significantly negative for bank-dependent firms, which is difficult to interpret.

- 16.

See the data appendix for more details on the way the nominal borrowing rate and the deposit rate are calculated.

- 17.

Note that we calculate the monopoly rent here by assuming that client firms are forced to hold all the time deposits. When parts of the time deposits are held at firms’ own initiative, the monopoly rent would be lower.

- 18.

The estimates of monopoly rents here are comparable to those obtained by Ono (1997). His estimates range from 20 to 80 basis points.

References

Acharya, V. A., Almeida, H., & Campello, M. (2007). Is cash negative debt? A hedging perspective on corporate financial policies. Journal of Financial Intermediation, 16, 515–554.

Almeida, H., Campello, M., & Weisbach, M. S. (2004). The cash flow sensitivity of cash. Journal of Finance, 59, 1777–1804.

Aoki, M., Patrick, H., & Sheard, P. (1994). The Japanese main bank system: An introductory overview. In M. Aoki & H. Patrick (Eds.), The Japanese main bank system: Its relevance for developing and transforming economies (pp. 1–50). UK: Oxford University Press.

Bates, T. W., Kahle, K. M., & Stulz, R. M. (2009). Why do U.S. firms hold so much more cash than they used to? Journal of Finance, 64, 1985–2012.

Baum, C. F., Caglayan, M., Stephan, A., & Talavera, O. (2008). Uncertainty determinants of corporate liquidity. Economic Modelling, 25, 833–849.

Baumol, W. J. (1952). The transactions demand for cash: An inventory theoretic approach. Quarterly Journal of Economics, 66, 545–556.

Dittmar, A., & Mahrt-Smith, J. (2007). Corporate governance and the value of cash holdings. Journal of Financial Economics, 83, 599–634.

Dittmar, A., Mahrt-Smith, J., & Servaes, H. (2003). International corporate governance and corporate cash holdings. Journal of Financial and Quantitative Analysis, 38, 111–133.

Han, S., & Qiu, J. (2007). Corporate precautionary cash holdings. Journal of Corporate Finance, 13, 43–57.

Hori, K., Ando, K., & Saito, M. (2010). Nippon kigyo no ryudosei sisan hoyu ni kansuru jissho kenkyu: Jojo kigyo no zaimu deta wo mochiita panel bunseki, (An empirical study on liquid asset holdings by Japanese firms: A panel analysis using financial data of listed firms). Gendai Finance (Modern Finance), 27, 3–24 (in Japanese).

Jensen, M. (1986). Agency costs of free cash flow, corporate finance and takeovers. American Economic Review, 76, 323–329.

Kang, J. K., & Shivdasani, A. (1995). Firm performance, corporate governance and top executive turnover in Japan. Journal of Financial Economics, 38, 29–58.

Kang, J. K., & Shivdasani, A. (1997). Corporate restructuring during performance declines in Japan. Journal of Financial Economics, 46, 29–65.

Kaplan, S. N., & Minton, B. (1994). Appointments of outsiders to Japanese corporate boards: Determinants and implications for managers. Journal of Financial Economics, 36, 225–258.

Keynes, J. M. (1936). The general theory of employment, interest and money. London: Harcourt Brace.

Miller, M. H., & Orr, D. (1966). A model of the demand for money by firms. Quarterly Journal of Economics, 80, 413–435.

Miyajima, H. (1998). Sengo nippon kigyo niokeru jyotai izonteki governance no shinka to henyo—Logit model niyoru keieisha kotai bunseki karano approach—(The evolution and change of contingent governance structure in the J-firm system—An approach to presidential turnover and firm performance). Keizai Kenkyu, 49, 97–112 (in Japanese).

Morck, R., & Nakamura, M. (1999). Banks and corporate control in Japan. Journal of Finance, 54, 319–339.

Mulligan, C. B. (1997). Scale economies, the value of time, and the demand for money: Longitudinal evidence from firms. Journal of Political Economy, 105, 1061–1079.

Ono, A. (1997). Wagakuni kinyukikan no yotai kinrizaya—tei spread no haikei to sono taiousaku- (Spread between lending rate and deposit rate in Japanese financial institutions: Background and measures against low spread). Fuji Soken Ronsyu, IV, 1–30 (in Japanese).

Ono, A., Uchida, H., Kozuka, S., Hazama, M., & Uesugi, I. (2011). Current status of firm-bank relationships and the use of collateral in Japan: An overview of the Teikoku databank data, Working Paper Series No. 4, Research Center for Interfirm Network, Hitotsubashi University.

Opler, T., Pinkowitz, L., Stulz, R. M., & Williamson, R. (1999). The determinants and implications of corporate cash holdings. Journal of Financial Economics, 52, 3–46.

Pinkowitz, L., & Williamson, R. (2001). Bank power and cash holdings: Evidence from Japan. The Review of Financial Studies, 14, 1059–1082.

Pinkowitz, L., Stulz, R. M., & Williamson, R. (2006). Do firms in countries with poor protection of investor rights hold more cash? Journal of Finance, 61, 2725–2751.

Riddick, L. A., & Whited, T. M. (2009). The corporate propensity to save. Journal of Finance, 64, 1729–1766.

Sheard, P. (1994). Bank executives on Japanese corporate boards. Bank of Japan Monetary and Economic Studies, 12, 85–121.

Tobin, J. (1956). The interest elasticity of the transactions demand for cash. Review of Economics and Statistics, 38, 241–247.

Uchida, H., Ono A., Kozuka, S., Hazama, M., & Uesugi, I. (2011). Current status of interfirm relationships in Japan: An overview of the Teikoku databank data, Working Paper Series No. 3, Research Center for Interfirm Network, Hitotsubashi University.

Acknowledgements

This research was financially supported by a Grant-in-Aid for Scientific Research (#22330068) from the Japanese Ministry of Education, Culture, Sports, Science and Technology. The author would like to thank Arito Ono, the discussant Masahiro Hori, and participants at the HIT-TDB-RIETI International Workshop on the Economics of Interfirm Networks for their helpful comments and suggestions. Makoto Hazama provided excellent assistance in constructing the dataset for the empirical analysis. Finally, the author would like to thank Teikoku Databank, Ltd. for kindly supplying the data. Any remaining errors are the sole responsibility of the author.

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Appendix

Appendix

This appendix explains how the variables used in the regression analysis were constructed.

-

1.

CASH: cash and deposits.

-

2.

TA: total assets.

-

3.

\(\Delta \log (SALES )\): growth rate of real sales. Real sales are obtained by dividing nominal sales by the GDP deflator classified by economic activity.

-

4.

NWC: net working capital, defined as current assets minus current liabilities minus cash.

-

5.

CASHFLOW: cash flow, measured by current net income.

-

6.

SDCFRATIO: conditional standard deviation of the ratio of cash flow to total assets based on the current value and the value of the past 2 years.

-

7.

DEBT: total debt.

-

8.

BANKDEBT: short-term and long-term bank debt.

-

9.

MAINDEP: dependence on main bank(s), measured by the ratio of borrowing from main bank (or banks) to total loans outstanding.

-

10.

BRATE: borrowing rate defined as interest paid and discount expenses divided by the sum of short-term loans, long-term loans, bills discounted, and bonds.

-

11.

DRATE: interest rate on time deposits. Three annual interest rates on deposits are used, namely the rate on deposits of more than 10 million yen, on deposits between 3 and 10 million yen, and on deposits of less than 3 million yen.

Rights and permissions

Copyright information

© 2015 Springer Japan

About this chapter

Cite this chapter

Ogawa, K. (2015). What do Cash Holdings Tell us About Bank-Firm Relationships? A Case Study of Japanese Firms. In: Watanabe, T., Uesugi, I., Ono, A. (eds) The Economics of Interfirm Networks. Advances in Japanese Business and Economics, vol 4. Springer, Tokyo. https://doi.org/10.1007/978-4-431-55390-8_11

Download citation

DOI: https://doi.org/10.1007/978-4-431-55390-8_11

Published:

Publisher Name: Springer, Tokyo

Print ISBN: 978-4-431-55389-2

Online ISBN: 978-4-431-55390-8

eBook Packages: Business and EconomicsEconomics and Finance (R0)