Abstract

This study analyzes whether self-reported attitudes in economic risk taking predict experimentally revealed risk behavior, and how gender moderates the relationship between both measures. Prior research often finds women reporting higher risk averse attitudes than men and showing more risk averse behavior in observational or experimental studies. This study analyzes observations from 369 students who participated in two laboratory experiments and answered a survey about their risk preferences. The findings show that risk attitudes are not likely to predict risk behavior directly, but being female predicts risk averse behavior robustly. Most interestingly, the analyses show that in the experiments, women behave consistently to their self-reported risk attitudes, but men do not. Methodological and practical implications are briefly discussed.

I am very grateful for the support and valuable comments on this paper from Markus Tepe and Michael Jankowski. I wish to thank the participants of the 2018 Annual Meeting of the DVPW working group on decision theory for the fruitful discussion on a prior version of this paper, as well as the two anonymous reviewers for their thorough comments, which further helped to improve this work.

Access this chapter

Tax calculation will be finalised at checkout

Purchases are for personal use only

Similar content being viewed by others

Notes

- 1.

The computerized bidder plays a risk neutral bidding strategy, which is not revealed to the participants.

- 2.

Learning from feedback is explicitly allowed. Thus, participants are offered a table with their endowment, their own bid, the computer’s bid (only on output screen), the winning bid, and points won over all previous rounds. To diminish wealth effects, totals are only displayed after the input stage is finished.

- 3.

Arrow and Pratt (see Arrow 1971) defined the notion for Constant Absolute Risk Aversion (CARA) and Constant Relative Risk Aversion (CRRA) to measure the utility of risk. Thereafter CARA is measured as A(x) = −U"(x)/U'(x) and CRRA as xA(x) = R(x) = −xU"(x)/U'(x). The utility function U(x) = x1−r used in this study is based on Chakravarty et al. (2011). Solving the function leads to R(x) = r, why in this study CRRA is consistent with the utility of the expected payoff and measured as r = 1 − (valuation − bid)/bid.

- 4.

For across experiments comparison data need to be aggregated for each individual. Further, the CRRA scale needs to be transformed. Detailed information are given in Sect. 4.3.

- 5.

The full instructions are presented in the Appendix.

- 6.

The lottery choice treatment was played in a series of simple experimental games, like ultimatum and dictator game. To avoid spillover effects from these games all entry stages were separated from the outcome stages. After all experiments were played a random number determined which of the experiments was selected for payout. This procedure allows to create a one-shot situation environment. The winning points of the selected experiment were converted into Euro in the end of the laboratory session.

- 7.

For across experiments comparison data needed to be aggregated for both lotteries. Detailed information are given in Sect. 4.3.

- 8.

The full instructions are presented in the Appendix.

- 9.

To gain statistically reliable results 105 or 51 participants are needed for the experimental or the survey measure respectively. With the given sample size of 369 participants statistical power lies above 99% for the entire analyses. Statistical power is excellent for all analyses except for Model 1 in Table 3, which is below acceptable levels of reliability.

- 10.

After excluding extreme outliers.

References

Ajzen, Icek, and Martin Fishbein. 1977. Attitude-Behavior Relations: A Theoretical Analysis and Review of Empirical Research, Psychological Bulletin 84 (5): 888–918.

Arrow, Kenneth Joseph. 1971. Essays in the Theory of Risk-Bearing. Vol. 1. Markham Publishing Company Chicago.

Berg, Joyce, John Dickhaut, Kevin McCabe, and Vernon L. Smith. 2005. Risk Preference Instability across Institutions: A Dilemma, Proceedings of the National Academy of Sciences of the United States of America 102 (11): 4209–14.

Bohner, Gerd, and Nina Dickel. 2011. Attitudes and Attitude Change, Annual Review of Psychology 62: 391–417.

Bruhin, Adrian, Helga Fehr-Duda, and Thomas Epper. 2010. Risk and Rationality: Uncovering Heterogeneity in Probability Distortion, Econometrica 78 (4): 1375–412.

Byrnes, James P., David C. Miller, and William D. Schafer. 1999. Gender Differences in Risk Taking: A Meta-Analysis, Psychological Bulletin 125 (3): 367.

Chakravarty, Sujoy, Glenn W. Harrison, Ernan E. Haruvy, and E. Elisabet Rutström. 2011. Are You Risk Averse over Other People’s Money?” Southern Economic Journal 77 (4): 901–13.

Charness, Gary, and Uri Gneezy. 2012. Strong Evidence for Gender Differences in Risk Taking, Journal of Economic Behavior & Organization 83 (1): 50–58.

Charness, Gary, Uri Gneezy, and Alex Imas. 2013. Explerimental Methods: Eliciting Risk Preferences, Journal of Economic Behavior & Organization 87: 43–51.

Cohn, Alain, Ernst Fehr, and Michel André Maréchal. 2017. Do Professional Norms in the Banking Industry Favor Risk-Taking?, The Review of Financial Studies 30 (11): 3801–23.

Croson, Rachel, and Uri Gneezy. 2009. Gender Differences in Preferences, Journal of Economic Literature 47 (2): 448–74.

Daruvala, Dinky. 2007. Gender, Risk and Stereotypes, Journal of Risk and Uncertainty 35 (3): 265–83.

Dohmen, Thomas, Armin Falk, David Huffman, Uwe Sunde, Jürgen Schupp, and Gert G. Wagner. 2011. Individual Risk Attitudes: Measurement, Determinants, and Behavioral Consequences, Journal of the European Economic Association, 9: 522–50.

Eckel, Catherine C., and Philip J. Grossman. 2002. Sex Differences and Statistical Stereotyping in Attitudes toward Financial Risk, Evolution and Human Behavior 23 (4): 281–95.

Eckel, Catherine C., and Philip J. Grossmann. 2008. Forecasting Risk Attitudes: An Experimental Study Using Actual and Forecast Gamble Choices, Journal of Economic Behavior & Organization 68 (1): 1–17.

Engel, Russell. 2011. First Price Auctions, Lotteries, and Risk Preferences Across Institutions, Journal of Business & Economics Research 9 (11): 9–27.

Fehr-Duda, Helga, Manuele de Gennaro, and Renate Schubert. 2006. Gender, Financial Risk, and Probability Weights, Theory and Decision 60 (2–3): 283–313.

Fellner, Gerlinde, and Boris Maciejovsky. 2007. Risk Attitude and Market Behavior: Evidence from Experimental Asset Markets, Journal of Economic Psychology 28 (3): 338–50.

Finucane, Melissa L., Paul Slovic, Chris K. Mertz, James Flynn, and Theresa A. Satterfield. 2000. Gender, Race, and Perceived Risk: The’white Male’effect, Health, Risk & Society 2 (2): 159–72.

Fischbacher, Urs. 2007. Z-Tree: Zurich Toolbox for Ready-Made Economic Experiments, Experimental Economics 10 (2): 171–78.

Gintis, Herbert. 2000. Game Theory Evolving: A Problem-Centered Introduction to Modeling Strategic Behavior. Princeton, NJ: Princeton University Press.

GSOEP. 2004. German Socio-Economic Panel. Berlin: German Institute for Economic Research (DIW).

Hainmueller, Jens. 2012. Entropy Balancing for Causal Effects: A Multivariate Reweighting Method to Produce Balanced Samples in Observational Studies, Political Analysis 20 (1): 25–46.

Halek, Martin, and Joseph G. Eisenhauer. 2001. Demography of Risk Aversion, Journal of Risk & Insurance 68 (1): 1–24.

Harrison, Glenn W., Eric Johnson, Melayne M. McInnes, and E. Elisabet Rutström. 2005. Temporal Stability of Estimates of Risk Aversion, Applied Financial Economics Letters 1 (1): 31–35.

Harrison, Glenn W., and E. Elisabet Rutström. 2008. Risk Aversion in the Laboratory, Research in Experimental Economics, 12: 41–196.

Holt, Charles A. 2007. Markets, Games, & Strategic Behavior. Boston, MA: Pearson Addison Wesley.

Holt, Charles A., and Susan K. Laury. 2002. Risk Aversion and Incentive Effects, The American Economic Review 92 (5): 1644–55.

Holt, Charles A., and Susan K. Laury. 2005. Risk Aversion and Incentive Effects: New Data without Order Effects, The American Economic Review 95 (3): 902–4.

Kahneman, Daniel. 1992. Reference Points, Anchors, Norms, and Mixed Feelings, Organizational Behavior and Human Decision Processes 51: 269–312.

Kraus, Stephen J. 1995. Attitudes and the Prediction of Behavior: A Meta-Analysis of the Empirical Literature, Personality and Social Psychology Bulletin 21 (1): 58–75.

Kelley, Matthew R., and Robert J. Lemke. 2015. Gender Differences When Subjective Probabilities Affect Risky Decisions: An Analysis from the Television Game Show Cash Cab, Theory and Decision. 78 (1): 153–70.

Knight, Frank H. 1921. Risk, Uncertainty and Profit. New York: Hart, Schaffner, and Marx.

Lemaster, Philip, and JoNell Strough. 2014. Beyond Mars and Venus: Understanding Gender Differences in Financial Risk Tolerance, Journal of Economic Psychology 42: 148–60.

Levin, Irwin P., Mary A. Snyder, and Daniel P. Chapman. 1988. The Interaction of Experiential and Situational Factors and Gender in a Simulated Risky Decision-Making Task, The Journal of Psychology 122 (2): 173–81.

Levin, Irwin P., Stephanie S. Hart, Joshua A. Weller, and Lyndsay A. Harshman. 2007. Stability of Choices in a Risky Decision-Making Task: A 3-Year Longitudinal Study with Children and Adults, Journal of Behavioral Decision Making 20 (3): 241–52.

Lönnqvist, Jan-Erik, Markku Verkasalo, Gari Walkowitz, and Philipp C. Wichardt. 2015. Measuring Individual Risk Attitudes in the Lab: Task or Ask? An Empirical Comparison, Journal of Economic Behavior & Organization 119: 254–66.

Maccoby, Eleanor E., and Nathan Maccoby. 1954. The Interview: A Tool of Social Science, Edited by Gardner Lindzey. Handbook of Social Psychology 1: 449–87.

Meier, Kenneth J., Laurence J. O’Toole Jr, and Holly T. Goerdel. 2006. Management Activity and Program Performance: Gender as Management Capital, Public Administration Review 66 (1): 24–36.

Milgrom, Paul R., and Robert J. Weber. 1982. A Theory of Auctions and Competitive Bidding, Econometrica 50 (5): 1089–122.

Morin, Roger, and A. Fernandez Suarez. 1983. Risk Aversion Revisited, Journal of Finance 38 (4): 1201–16.

O’Brien, Diana Z. 2015. Rising to the Top: Gender, Political Performance, and Party Leadership in Parliamentary Democracies, American Journal of Political Science 59 (4): 1022–39.

Pedroni, Andreas, Renato Frey, Adrian Bruhin, Gilles Dutilh, Ralph Hertwig, and Jörg Rieskamp. 2017. The Risk Elicitation Puzzle, Nature Human Behaviour 1 (11): 803–9.

Powell, Melanie, and David Ansic. 1997. Gender Differences in Risk Behaviour in Financial Decision-Making: An Experimental Analysis, Journal of Economic Psychology 18 (6): 605–28.

Schubert, Renate, Martin Brown, Matthias Gysler, and Hans Wolfgang Brachinger. 1999. Financial Decision-Making: Are Women Really More Risk-Averse?” The American Economic Review 89 (2): 381–85.

Von Neumann, John, and Oskar Morgenstern. 1947. Theory of Games and Economic Behavior. Princeton, NJ: Princeton University Press.

Wärneryd, Karl-Erik. 1996. Risk Attitudes and Risky Behavior, Journal of Economic Psychology 17 (6): 749–70.

Zizzo, Daniel John. 2010. Experimenter Demand Effects in Economic Experiments, Experimental Economics 13 (1): 75–98.

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Appendix

Appendix

Displayed instructions—Auction

In the following auction you will bet against a computerized bidder over 30 rounds. Your goal is to outbid the computer. If your bid is higher than the computer’s bid you have won the respective round. In the case of ties your bid does not win. In each round, you will have a new randomly chosen endowment with an amount between 1 and 100 points. The computer always bids between 1 and 50 points. All amounts are distributed equally.

Gain = endowment − bid

All the points you win are added, and converted into Euro with an exchange rate of

1 point = 0.01 €.

For each bid helpful information is provided (see Fig. 2 of the paper instructions). The following data can be displayed as often as you wish:

Expected payoff: Outcome in points in the case of winning

Expected payoff = endowment − bid

Winning probability: Probability of winning the auction with the actual bid. The value ranges from 0 to 1. The higher the value, the higher is the probability to win. 0 = sure no win, 0.5 = same probability of winning or not winning, respectively, 1 = sure win

Expected value = expected payoff * winning probability

Example:

With an endowment of 59 points you bid 27 points, and have a winning probability of 0.5 (i.e. 50%). The computer’s bid is 13 points. Yor bid is higher than the bid of the computer, thus you are the winner of the auction. In this round you are winning

59 − 27 = 32 points * 0.01€ = 0.32 €.

As soon as you have decided on your bid, please select the appropriate row and click the button “submit bid”.

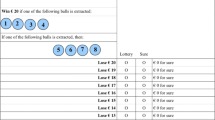

Displayed instructions—Lottery

Structure

In this game you choose between alternative lotteries.

You will decide 10 times. Each time you choose between option A and option B.

Each option can lead to two events. The probability and the gain in points of each event will be displayed in a table.

Please notice that only one of your decisions will determine your earnings.

Previously you will not know which lottery will be played.

When the time for input expired the computer will calculate two random numbers.

The first random number (between 1 and 10) determines which lottery will be played.

The second random number (between 1 and 10) determines your gain in points depending on your choice for option A or B.

Depending on the option you chose (A or B) the respective amount in points will be added to your account.

Example

Notice the example on the following screen. Please click “Forward”.

Lottery number | Option A | Option B | Your decision (A or B) |

|---|---|---|---|

1 | 40 of 10% or 32 of 90% | 77 of 10% or 2 of 90% | |

2 | 40 of 20% or 32 of 80% | 77 of 20% or 2 of 80% | |

3 | 40 of 30% or 32 of 70% | 77 of 30% or 2 of 70% | A |

4 | 40 of 40% or 32 of 60% | 77 of 40% or 2 of 60% | |

5 | 40 of 50% or 32 of 50% | 77 of 50% or 2 of 50% |

Example

If the first random number is 3, the lottery number 3 will be played. We assume you chose Option A in lottery number 3. Option A in lottery number 3 provides “40 of 30% or 32 of 70%”. In other words Option A in lottery number 3 offers a 30% chance to win 40 points and a 70% chance to win 32 points. If you would have been chosen Option B in lottery number 3 you had have a 30% chance to win 77 points and a 70% chance to win 2 points. The second random number determines which event actually occurs. Imagine a 10-sided die. If the throw of the 10-sided die in Option A of lottery number 3 is smaller than or equal 3 you win 40 points. If the throw of the 10-sided die in Option A of lottery number 3 is greater than 3 you win 32 points. Choose one of the options in each of the 10 lotteries. There are two runs of this game each with different amounts of points.

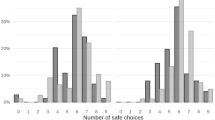

Appendix (Tab. 4, 5, 6, 7, 8 und 9; Fig. 4)

(Note: Based on full OLS regression model, 90% confidence intervals, from left to right: Predicted values of CRRA by gender; AME of gender on the relationship between risk attitudes and gender; AME sizes of stated risk preferences on risk behavior by gender)

Gender effect on the attitudes-behavior relationship, all risk attitudes.

Rights and permissions

Copyright information

© 2019 Springer Fachmedien Wiesbaden GmbH, ein Teil von Springer Nature

About this chapter

Cite this chapter

Prokop, C. (2019). Risk Attitudes, Gender, and Risk Behavior: Evidence from Two Laboratory Experiments. In: Debus, M., Tepe, M., Sauermann, J. (eds) Jahrbuch für Handlungs- und Entscheidungstheorie. Jahrbuch für Handlungs- und Entscheidungstheorie. Springer VS, Wiesbaden. https://doi.org/10.1007/978-3-658-23997-8_6

Download citation

DOI: https://doi.org/10.1007/978-3-658-23997-8_6

Published:

Publisher Name: Springer VS, Wiesbaden

Print ISBN: 978-3-658-23996-1

Online ISBN: 978-3-658-23997-8

eBook Packages: Social Science and Law (German Language)