Abstract

The purpose of this article is to apply a multivariate spatial statistics technique: cluster analysis or spatial agglomeration, in order to classify departments into groups based on behavior in the number of active, inactive electronic savings accounts and savings traditional active accounts, with database available as of September 2017 in the bank of Colombia. The selection of this type of accounts was due to the fact that the financial product with the highest penetration in the Colombian population in September 2017, continued to be the savings account; 73.5% of the population had this financial product. However, this percentage is far from the target of 84% proposed in the National Development Plan. The findings show that the departments where electronic accounts are most used are Cauca, Bogotá, Meta, Casanare, Arauca, Vichada, Huila, Amazonas, Guainía, Vaupés, Caldas, Chocó, Sucre, La Guajira, César, Norte de Santander, however, the levels of penetration of this type of product are very low yet in the Colombian territory.

Access provided by CONRICYT-eBooks. Download conference paper PDF

Similar content being viewed by others

Keywords

1 Introduction

Electronic participation is defined as the process of involving citizens in politics through ICT, for decision making processes that allow the public administration to be participatory, inclusive, collaborative, and deliberative for intrinsic and instrumental purposes. Electronic participation is a strategic factor to improve citizen participation in digital governance [1], to promote a more efficient society [2], and improve the competitiveness of firms [3]. Despite the above, there is a recurring problem called the “digital divide” which is generally known as “unequal diffusion” between different socioeconomic levels, or countries, gender, age [4, 5], race, region, or geography in terms of access or use [6, 7].

According to the information from “Banca de Oportunidades” [8], 79.1% of adults in Colombia had at least one financial product in a credit establishment, that is, 26.6 million Colombians, 1.8% more with respect to September 2016. Also, as of September 2017, 738,432 adults entered the financial system for the first time and had 106,701 points of access to the financial system, that is, financial offices or banking correspondents.

52% of the population with some financial product were women and the remaining 48% men. The financial product with the highest penetration in the Colombian population as of September 2017 continued to be the savings account, since 73.5% of the adult use this financial product. Within the modalities of savings account, there are deposits and electronic accounts. However, they still have a lower penetration, since, by September 2017, there were approximately 3 million adults with some electronic deposit and 2.8 million actively used them (92.5%).

Electronic savings accounts exist in Colombia since 2007, in accordance with the provisions of Law 1151 of 2007 [9], regulated by Decree 2555 in 2010 [10]. In accordance with the mentioned regulations, electronic savings accounts are aimed at people belonging to level 1 of the Identification System of Potential Beneficiaries of Social Programs -Sisben-, and displaced people registered in the Single Registry of Displaced Population, and meeting the following conditions:

-

Transactions may be made through cards, cell phones, ATMs or any other means and distribution channel that is agreed upon.

-

The entity recognizes an interest rate.

-

The credit establishments and the authorized cooperatives cannot charge the holders for the management of the account or for one of the means enabled for their operation. At least two (2) withdrawals in cash and a balance inquiry made by the customer per month do not cause any payment.

-

Clients must be informed of the benefits, the cost of transactions, or additional queries.

-

No minimum initial deposit nor minimum balance is required for opening accounts.

-

The debits cannot exceed the two (2) legal monthly minimum wages in force.

-

Only one (1) electronic savings account may be held in the financial system.

-

The accounts are not subject to any type of mandatory investment.

According to the above, the purpose of this paper is to apply a multivariate spatial statistics technique: cluster analysis or spatial agglomeration, to classify departments into groups based on behavior in the number of active electronic savings accounts, inactive, and active traditional savings accounts. The importance of addressing this issue lies in the fact that in Colombia, it was stated that based on statistics on cell phone use, the simplest form of banking for the population was the use of electronic savings accounts. Despite this, the figures indicate that it is a financial mechanism that has had low penetration and in most of the national territory it continues to prefer the traditional savings account.

2 Method

2.1 Data

In this work, the Banca de las Oportunidades reports (2018a, 2018b) are used as the primary source. The reports contain information at the departmental level, as of September 2017, on the total of electronic and traditional savings accounts1. The source of the statistics “Banca de las Oportunidades”, is a program of the Government of Colombia, administered by Bancoldex, whose main objective is to promote financial inclusion in Colombia, through access to financial services to families in poverty, small entrepreneurs, small and medium-sized companies and entrepreneurs. All this, in accordance with its mission, to reduce poverty, promote social equality and stimulate economic development in Colombia.

Table 1 shows the data, sources and units used for the following sections. The software used for calculating the models corresponds to Philcarto.

2.2 Spatial Autocorrelation

For the calculation of spatial autocorrelationFootnote 1 we use the univariate Global Moran index [13,14,15] for each of the variables in Table 1. Given the set of spatial entities and an associated attribute (variable), this index evaluates whether the pattern expressed is grouped, scattered or randomized. The index oscillates between −1 (strong negative spatial autocorrelation) and 1 (strong positive spatial autocorrelation), if it is close to 0 it indicates the absence of spatial autocorrelation. It is interpreted as moderate spatial autocorrelation from 0.3, up to 0.6 and thereafter a high spatial autocorrelation. The formula is in Eq. 1.

- \( W_{y} \)::

-

It is the element of the matrix of special weights, corresponding to the \( \left( {i,j} \right) \)

- \( Y \)::

-

Average expected value of the variable \( y \)

- \( N \)::

-

Number of observations or sample size

- \( S_{o} \)::

-

Corresponds to: \( S_0 = \sum i\sum i W_{j} = \sum 2 W_{j} \).

2.3 Space Agglomeration

The purpose of this section is to apply a hierarchical ascending classification model (interdependence method), to identify which behaviors allow to create group clusters in conglomerates according to the number of electronic savings accounts, traditional savings accounts, and balances in millions of pesos. This in order to establish in which departments could be presented focalization programs that encourage the use of electronic accounts and improve the mechanisms of bancarization in Colombia.

Based on the data, an empirical study of the ex post facto type was carried out, using a cluster analysis (Gallardo, 2015, p. 1). The Minimum Distance strategy is used (Langrand and Pinzón, 2009 and Gallardo, 2015). In this way, when performing stage K, n-K clusters are obtained, and the distance between the clusters Ci (with ni elements) and Cj (with nj elements) would be:

In this case, the clusters Ci and Cj will be joined:

3 Results

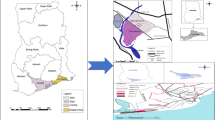

Figures 1, 2 and 3 show the departmental behavior of the use of traditional and electronic savings accounts. As shown in Fig. 1, the differences between traditional and electronic savings accounts are significant, especially in the western part of the country. Also, in the Figs. 2 and 3Footnote 2, it is evident that there is no degree of special autocorrelation between levels 1 and 7. For all cases, it is a random spatial distribution, considering the variables independently.

Comparison of electronic and traditional savings accounts

Distribution of active electronic savings accounts in Colombia

Distribution of traditional active savings accounts in Colombia

When applying the hierarchical ascending classification, the following results were obtained, using the Philcato software, specialized in cartographic analysis. The histogram shows that the significant number of classes is 6 for the 33 spatial units analyzed (departments), explaining 96.94% of the inertia. Figures 4 and 5 show the results of the departments grouping in 6 different significant classes. This grouping explains 96.94% of the data variability, which implies an excellent explanatory level. Figure 6 contains the spatial representation of the departments and is detailed in Table 2. The importance of this analysis lies on the fact that differentiated strategies can be applied, according to the characteristics of each statistically identified group, and not to a homogeneous policy.

Tree diagram of the clusters.

Diagram of average distance of each class with respect to the general average.

Spatial representation of the application of hierarchical ascending classification to the number of savings accounts in Colombia (September 2017).

In space units 1 and 5, given that electronic savings accounts have been more popular than in the rest of the country, it is worth focusing efforts with specific programs, which further encourage the use of this type of financial mechanisms. In groups 3 and 4 there is a clear preference for traditional savings mechanisms, which is striking, since most of these departments have good access to the Internet. Finally, it is important to note that in none of the cases is there a simultaneous behavior of being below the national average in electronic and traditional savings accounts. This indicates that at least some of the mechanisms are preferred and there is no evidence of a process of unbanking, at least in terms of saving.

4 Conclusions

In the departments of San Andrés and Providencia, Putumayo, Valle del Cauca, Quindío, Risaralda, Antioquia, Córdoba, Santander, Boyacá and Atlántico, the strategy of active electronic accounts as a financial inclusion mechanism has not been favored, since a preference for traditional accounts persists. For its part, the departments of Nariño, Caquetá, Guaviare, Cundinamarca, Tolima, Bolívar, Magdalena, are in an intermediate stage, since the number of traditional accounts is just a little higher than the average and the number of active electronic accounts, despite being below average, tend to increase.

On the other hand, the departments where the electronic accounts are most used are Cauca, Bogotá, Meta, Casanare, Arauca, Vichada, Huila, Amazonas, Guainía, Vaupés, Caldas, Chocó, Sucre, La Guajira, César, Norte de Santander. These findings are evidence of a breach within the country of the penetration of ICT and the use of alternative banking products such as electronic deposits.

The findings indicate that although it was proposed that electronic savings accounts were one of the mechanisms that would facilitate banking penetration, after 10 years of having been created by national legislation, they do not have a high penetration in the Colombian population, nor they have a homogeneous distribution in the national territory.

To reach the goal of 84% of the banking population in Colombia in 2018, more attractive mechanisms or programs are required for the population, which respond to the needs of users and whose costs are not so high.

Notes

- 1.

Spatial autocorrelation implies that the value of a variable is conditioned by the value assumed by that variable in a neighboring region [16].

- 2.

The Jenks algorithm is used to calculate classes, which is characterized by maximizing the difference between classes and making groups more homogeneous [17].

References

Sanford, J., Rose, C.: Characterizing participation. Int. J. Inf. Manag. 27(6), 406–442 (2007)

Sæbø, Ø., Rose, J., Skiftenes Flak, L.: The shape of eParticipation: characterizing an emerging research area. Gov. Inf. Quart. 25(3), 400–428 (2008)

Ortega Ruiz, C.: Inclusión de las TIC en la empresa colombiana. Suma de Negocios 5(10), 29–33 (2014). https://www.sciencedirect.com/science/article/pii/S2215910X14700060

Selwyn, N.: Literature Review in Citizenship, Technology and Learning. Cardiff University, Cardiff (2006)

Wagner, N., Hassanein, K., Head, M.: Computer use by older adults: a multi-disciplinary review. Comput. Hum. Behav. 26(5), 870–882 (2010). https://doi.org/10.1016/j.chb.2010.03.029

Tsatsou, P.: Digital divides revisited: what is new about divides and their research? Media Cult. Soc. 33(2), 317–331 (2015)

Dennis, C., Papagiannidis, S., Alamanos, E., Bourlakis, M.: The role of brand attachment strength in higher education. J. Bus. Res. 69(8), 3049–3057 (2016). https://doi.org/10.1016/j.jbusres.2016.01.020

Banca de las Oportunidades: Reporte Trimestral de Inclusión Financiera - Septiembre 2017. Bogotá: Banca de las Oportunidades (2018). http://bancadelasoportunidades.gov.co/sites/default/files/2018-01/REPORTE%20TRIMESTRAL%20INCLUSION%20FINANCIERA%20SEPTIEMBRE%202017%20VF_31%20Ene%202018.pdf

Ministerio de Hacienda y Crédito Público. Decreto 2555 de 2010. Diario Oficial 47771. Bogotá: Imprenta Nacional (2010). http://www.alcaldiabogota.gov.co/sisjur/normas/Norma1.jsp?i=40032#12.2.1.1.4

Congreso de la República de Colombia. Ley 1151 de 2007. Diario Oficial 46700 de julio 25 de 2007. Bogotá: Imprenta Nacional (2007). http://www.alcaldiabogota.gov.co/sisjur/normas/Norma1.jsp?i=25932

Banca de las Oportunidades: Cuentas de ahorro electrónicas - Septiembre 2017 [Base de datos] (2018a). http://bancadelasoportunidades.gov.co/es/cuentas-de-ahorro

Banca de las Oportunidades: Cuentas de ahorro tradicional - Septiembre 2017 [Base de datos] (2018b). http://bancadelasoportunidades.gov.co/es/cuentas-de-ahorro

Lis-Gutiérrez, J.-P., Macías Rojas, S., Gaitán-Angulo, M., Moros, A., Viloria, A.: Analysis of concentration, dominance and symmetry in bank deposits in Colombia. J. Eng. Appl. Sci. 12(1), 2831–2834 (2017). http://docsdrive.com/pdfs/medwelljournals/jeasci/2017/2831-2834.pdf

Zárate-Arévalo, A.-F., Lis-Gutiérrez, J-P., Gaitán-Angulo, M., Laverde, H., Viloria, A.: Perception of trust and commitment in the financial sector in Bogotá (Colombia). J. Eng. Appl. Sci. 12(11), 2835–2837 (2017). http://docsdrive.com/pdfs/medwelljournals/jeasci/2017/2835-2837.pdf

Moran, P.A.P.: The interpretation of statistical maps. J. R. Stat. Soc. B 10, 243–251 (1948)

Anselin, L.: Spatial Econometrics: Methods and Models. Kluwer Academic, Dordrecht (1988)

Smith, M., Goodchild, M., Longley, P.: Univariate classification schemes en Geospatial Analysis. (2015). http://www.spatialanalysisonline.com/HTML/index.html?classification_and_clustering.htm

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2018 Springer International Publishing AG, part of Springer Nature

About this paper

Cite this paper

Lis-Gutiérrez, JP., Gaitán-Angulo, M., Lis-Gutiérrez, M., Viloria, A., Cubillos, J., Rodríguez-Garnica, PA. (2018). Electronic and Traditional Savings Accounts in Colombia: A Spatial Agglomeration Model. In: Tan, Y., Shi, Y., Tang, Q. (eds) Data Mining and Big Data. DMBD 2018. Lecture Notes in Computer Science(), vol 10943. Springer, Cham. https://doi.org/10.1007/978-3-319-93803-5_28

Download citation

DOI: https://doi.org/10.1007/978-3-319-93803-5_28

Published:

Publisher Name: Springer, Cham

Print ISBN: 978-3-319-93802-8

Online ISBN: 978-3-319-93803-5

eBook Packages: Computer ScienceComputer Science (R0)