Abstract

Companies included on a sustainability index meet several criteria based on an assessment of their economic, environmental and social practices. Each of these companies satisfies a different number of criteria and these standards can be quite different in quality and rigor. In this sense, RobecoSAM provides a Corporate Sustainability Assessment of the companies included in the Dow Jones Sustainable Index. The three proposed classes (Gold, Silver and Bronze) can be considered as social responsible (SR) ratings. Therefore, we examine the financial performance of portfolios composed of stocks according to these ratings. We assume that highly conscious SR investors could base their portfolio decision-making process on these SR ratings. From an extensive dataset, our results show that SR investments not only have no cost for investors but also outperform the market. Additionally, there are no significant differences among SR portfolios depending on the SR rating.

Access provided by CONRICYT-eBooks. Download chapter PDF

Similar content being viewed by others

Keywords

1 Introduction

Socially Responsible Investment (henceforth SRI) is an increasing finance trend, covering a great part of the upcoming literature, but, indeed, it has shaped how finance has developed over the past years, and probably how it will continue to do so.

SRI consists of selecting or excluding through investment screens based on environmental, social, or corporate governance criteria. Furthermore, engagement with local communities and shareholder activism is considered as out-standing criteria [1]. There are different ways of selecting SRI from the whole bunch of assets available in the market, investors can use negative, positive sustainability, or a combination between “sustainability” and shareholder activism [2].

The literature on the subject is focused on examining the performance of global SRI indices compared to conventional investments, the performance of companies grouped as homogenous because they are included in an ethical index or other SR benchmarks compared to conventional investments, and the performance of mutual funds or Ethical Investment Funds. Consensus has not been achieved.

The aim of this paper is to examine the role of corporate sustainable ratings as portfolio decision-making criterion for highly conscious SR investors. Some international investment companies have carried out sustainability assessments to build up SRI indices. This is the case of RobecoSAM, company which builds up the Dow Jones Sustainable Index (henceforth DJSI) and classifies SR companies in different levels or ratings based on the Corporate Sustainability Assessment (henceforth CSA). We assume that highly conscious SR investors could base their investment strategies on the three categories or CSA levels (Gold, Silver, and Bronze). In addition, we study is that SRI can be as good as conventional investments in terms of the financial performance, for which, an empirical analysis that measures financial performance of a different degree of sustainable companies versus non-sustainable companies has been carried out. This study contributes to the existing literature using a large sample period, reliable data to rank companies’ socially responsible performance and a wider range of performance measures. From the empirical analysis, we can conclude that SRI not only are not a cost for investors but also they outperform the market, having better performance than traditional diversified portfolios.

2 Relationship Between Socially Responsible Performance and Financial Performance

A branch of the literature on SRI is focused on examining the performance of global SRI indices compared to conventional investments, the performance of companies grouped as homogenous because they are included in an ethical index or other SR benchmarks compared to conventional investments, and the performance of mutual funds compared to EIFs. Consensus has not been reached either in the data base used neither the methodology. While some use liquidity ratios, other use risk-adjusted performance measures.

This study goes beyond this literature by examining portfolios that contain individual companies, but while distinguishing among different degrees of corporate sustainability involvement. Some authors [3,4,5,6] examine the performance of the own DJSI or the alternative FTSE4Good Indices or use being included in those indices as homogeneous Corporate Sustainability Performance (CSP). Other recent papers analyse companies that follows or publicly maintain that they use SBP [7,8,9]. We try to improve the methodology previously used by considering different degrees of CSR. We use the CSA, interpreted like a sort of CSR ratings, to examine separately the performance of portfolios of companies included in each category: Gold, Silver, and Bronze.

3 Portfolios Composition and Data Sample

Based on the yearly classification of the CSA provided by RobecoSAM, we look for companies also included in the Euro Stoxx 50, i.e., we match both datasets. We select manually companies that have been classified in one of the three main categories (Gold, Silver and Bronze) from The Sustainability Yearbook 2016, then the companies from the Eurozone need to be extracted from the list.Footnote 1

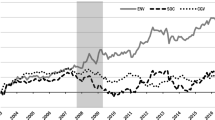

The study has been carried out so that the investor can build up different value-weighted portfolios depending on its SRI demand, i.e., depending on the “socially responsible ratings”. The portfolios would be Gold (3 stocks), Silver (9 stocks), Bronze (19 stocks), and Market portfolios. The last portfolio is the stock market portfolio Euro Stoxx 50, and is the benchmark or market portfolio, since it includes all the companies that are in each portfolio and the 50 leader companies of the euro zone.

The time horizon of this analysis is 15 years (January 2002–December 2016), calculating the weekly rates of return of each of the different portfolios. According to the volatility given by the VIX Index, the sample period has been divided into three different subperiods: pre-crisis and calm period (January 2002–June 2007), the financial crisis or market stress (includes the sovereign debt crisis in PIGS countries) (July 2007–June 2012), and bailout and economical overcome (July 2012–December 2016).

4 Empirical Analysis

In this section, we compute different risk-adjusted performance measures to our SRI portfolios constructed from three different levels of exigency of social responsibility: only Gold stocks, Gold and Silver stocks, and Gold, Silver, and Bronze stocks. From weekly discrete rates of returns, we compute basic statistical metrics and the performance measures to test the hypotheses previously exposed.

Both sets of performance measures show that the three sustainable portfolios outperform the market for the whole period (January 2002–December 2016). Summarizing results obtained by our analysis of the risk-adjusted performance measures, the three portfolios could be sorted into a clear order according to the values of all the performance indices: first the Silver portfolio, second the Bronze, and third the Gold.

We now try to check if this apparent result is statistically significant for the full sample period and for each particular subsample. This analysis makes sense from a statistical point of view and thus portfolios can be compared between each other to state which one is superior to the other. Using 6-month non-overlapping windows during the period 2002–2016, we test the equality of mean, and two non-parametric tests, the sign test (binomial test) and the Wilcoxon signed-ranked test to test the null hypothesis of equality of median, and the Levene statistic.

This analysis shows that the only statistically significant difference between portfolios appear in the case of the Sharpe ratio. For the full sample period, the Gold portfolio systematically performs below the Silver and above the Bronze portfolios. For the rest of the analysed performance measures, their mean, median, and variance are statistically similar. No differences are observed from the performance analysis based on these measures of the three portfolios constructed with different CSA categories.

5 Conclusion

This study delivers a new point of view to the existing literature. We examine whether investing in SRI has a cost in terms of lower rates of return or underperformance. Literature has not come to an agreement about the relationship between being socially responsible and financial performance, this study aims to fill the gap. The empirical background of this study, as far as we know, is the first analysis within which different portfolios are constructed depending on a ranking that classify SRI in different levels. These “socially responsible ratings” consider the number and quality of the SBP that the companies meet. This fact added to the long sample period analysed, which covers large periods of calm and turmoil, and the reliable data used to measure the companies’ SR performance, obtained from one of the most reliable databases in the world, gives a new outlook to the literature.

This study has been mainly developed with the aim of checking a relevant hypothesis: the performance of the portfolio is different depending on the “socially responsible rating” achieved. For which, it can be concluded that there are not significant differences between portfolios depending on their “socially responsible ratings”, then SRI is not a cost for investors, even, they can outperform the market.

Notes

- 1.

The stock prices have been obtained from Yahoo Finance, the market capitalization of each company has been obtained from ElEconomista website. As a risk-free asset, we use the daily series of the 1-week Euribor obtained from the European Money Markets Institute (EMMI).

References

Renneboog, L., Ter Horst, J., Zhang, C.: Socially responsible investments: institutional aspects, performance, and investor behavior. J. Bank. Financ. 32(9), 1723–1742 (2008)

Ward, S.: Socially Responsible Investment. Directory of Social Change Publication, London (1991)

Collison, D.J., Cobb, G., Power, D.M., Stevenson, L.A.: The financial performance of the FTSE4Good indices. Corp. Soc. Responsib. Environ. Manag. 15(1), 14–28 (2008)

Oberndorfer, U., Schmidt, P., Wagner, M., Ziegler, A.: Does the stock market value the inclusion in a sustainability stock index? An event study analysis for German firms. J. Environ. Econ. Manag. 66(3), 497–509 (2013)

Perez-Calderon, E., Milanes-Montero, P., Ortega-Rossell, F.J.: Environmental performance and firm value: evidence from Dow Jones Sustainability Index Europe. Int. J. Environ. Res. 6(4), 1007–1014 (2012)

Ziegler, A.: Is it beneficial to be included in a sustainability stock index? A panel data study for European firms. Environ. Resour. Econ. 52(3), 301–325 (2012)

Brammer, S., Brooks, C., Pavelin, S.: Corporate social performance and stock returns: UK evidence from disaggregate measures. Financ. Manag. 35(3), 97–116 (2006)

Callan, S.J., Thomas, J.M.: Corporate financial performance and corporate social performance: an update and reinvestigation. Corp. Soc. Responsib. Environ. Manag. 16(2), 61–78 (2009)

Godfrey, P.C., Merrill, C.B., Hansen, J.M.: The relationship between corporate social responsibility and shareholder value: an empirical test of the risk management hypothesis. Strateg. Manag. J. 30(49), 425–445 (2009)

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2018 Springer International Publishing AG, part of Springer Nature

About this chapter

Cite this chapter

Díaz, A., Garrido, G. (2018). Socially Responsible Investment, Should You Bother?. In: Corazza, M., Durbán, M., Grané, A., Perna, C., Sibillo, M. (eds) Mathematical and Statistical Methods for Actuarial Sciences and Finance. Springer, Cham. https://doi.org/10.1007/978-3-319-89824-7_60

Download citation

DOI: https://doi.org/10.1007/978-3-319-89824-7_60

Published:

Publisher Name: Springer, Cham

Print ISBN: 978-3-319-89823-0

Online ISBN: 978-3-319-89824-7

eBook Packages: Mathematics and StatisticsMathematics and Statistics (R0)