Abstract

The nexus between foreign direct investment and economic growth has been widely debated in recent years. A fundamental challenge to the economies of developing countries in East Africa is how to achieve a sustainable increase in output over time. They have been attracting foreign direct investments to bridge the gaps between the domestically available supplies of savings and investment demands; generating foreign exchange; transferring technology; and enhancing job creation and human capital skills to achieve sustainable economic growth and development. This study examines the impact of foreign direct investment (FDI) on economic growth and its determinants in East African countries. Secondary data for 20 years for 14 Sub-Saharan Africa countries was collected from the World Bank’s World Development Indicator database, the World Governance Indicator and political Risk Services International’s Country Risk Guide database for the study. The study uses the dynamic generalized method of moment estimator for data analysis after conducting all the diagnostic tests. Empirical evidence shows that FDI has a positive and significant effect on economic growth in the region. The pairwise Granger causality test shows that there is unidirectional causality running from economic growth to FDI. However, while attracting FDI for promoting economic growth the countries need to take care of its nature and composition.

Access provided by CONRICYT-eBooks. Download chapter PDF

Similar content being viewed by others

Keywords

JEL Classification Codes

1 Introduction

In recent years, developing countries have acknowledged the significant role that FDI plays in their development agendas. In Africa in particular it is considered as an important ingredient in filling the gaps between domestically available savings supplies and investment demands; technology transfers; enhancing job creation; adding value to human skills; and increasing aggregate productivity of the host country (Todaro and Smith 2012).

Globally , the flow of FDI increased from US$13.3 billion in 1970 to US$1.76 trillion in 2015. At the same time developing countries ’ share of FDI increased from US$3.8 billion to US$0.8 trillion. Similarly, the inflow of FDI to Africa increased from US$1.8 billion in 1970 to US$57.2 billion and Eastern Africa’s share went from US$0.1 to US$15.7 billion. The growth rate of FDI inflows to Africa and Eastern Africa increased in absolute terms between 1970 and 2015. Eastern Africa has also been attracting a large number of foreign investors (UNCTAD 2016).

However, a major concern for developing countries including those in East Africa is how to achieve sustainable growth in output over a long period of time and improve the standard of living of the people. This fundamental question of achieving sustained economic development in Africa and Eastern Africa remains a serious challenge for the regional economies. The region is not meeting its investment demands due to capital constraints, low saving rates, poor regional infrastructure development , structural and institutional rigidities, political instability, high crime rates, continuous civil conflicts, droughts and famines and unclear and arbitrary decisions about land ownership (Anyanwu 2012).

On the other hand, FDI’s economic role in developing countries has not been supported unequivocally by all writers; it has both proponents and opponents. The proponents argue that FDI is an alternative source of capital which stimulates economic growth in the host economy, transfers technology and skill gains, increases production and trade networks, enhances socioeconomic development , promotes employment opportunities, helps in integration with global production networks and access to high quality goods and reduces disparities between revenues and costs (OECD 2008). However, the fruits of this can be harnessed under the condition that the host country has the right policy environment and minimum levels of educational, technological and infrastructure development (Borensztein et al. 1998).

Opponents of FDI argue that it has a negative or insignificant effect on the host economy and at worst it can also retard economic growth through its crowding-out effects on domestic infant industries, deteriorating balance of payments , exploiting local resources, repatriating profits to home countries, risks of political changes and opening the door to corruption by some public officials (Abadi 2011; Agrawal 2011; Alege and Ogundipe 2013). Several empirical studies have confirmed the negative effects of FDI on the economies of host countries. At an extreme FDI leads to modern day economic colonialism.

For sub-Saharan African countries considerable research findings show that FDI has had a positive impact on the economic growth of the region. For instance, Demelew (2014) examined the impact of FDI on the economic growth of 47 sub-Saharan African (SSA) countries. The study showed that FDI had a positive and significant effect on economic growth in the region. Similarly, a study by Zekarias (2016) confirmed a positive effect of FDI on economic growth in 14 East Africa countries. The study showed that FDI had spillover effects on economic growth in the region.

Besides the inconclusive empirical results about the impact of FDI on economic growth , clear causality between the two has not been established as yet in the Eastern African region. As a result, our study examines the causes and effects of these variables for the region. To provide up to date evidence in East African countries, we provide additional insights into the impact of FDI on economic growth in Eastern African countries. Moreover, we also examine political instability, problems of institutional quality, financial constraints, low saving rates, infrastructure development and other variables as the determinants of FDI inflows into the region.

The primary objective of our study is investigating the impact of FDI on economic growth in Eastern African countries and see the determinants of FDI in the region. Specifically, we address the following objectives:

-

Identifying FDI’s short run and long run contribution to economic growth in East Africa.

-

Examining the causal relationship between FDI and economic growth .

-

Investigating the effects of institutional quality and political stability in attracting FDI to the region.

2 Literature Review

Both theoretical and empirical literature on FDI abounds. Contending theories are available for the concepts, definitions, benefits and costs of FDI to the overall performance of an economy. Conceptually, FDI is one of the three components of international capital flows: portfolio investments, foreign direct investments and other flows like bank loans from developed economies to developing economies (Todaro and Smith 2012).

FDI is defined differently by various organizations. For instance, OECD (2008) defines FDI as establishing a lasting interest by a resident enterprise in one economy (direct investor) in an enterprise (direct investment enterprise) that is resident in an economy other than that of the direct investment. Lasting interest implies the existence of a long-term relationship between the direct investor and the direct investment enterprise with a significant degree of influence on the management of the enterprise. A significant degree of influence and a long-term relationship are key terms that distinguish FDI from portfolio investments which are short-term activities undertaken by institutional investors through the equity market. A ‘lasting interest’ in a foreign entity emphasizes the difference between FDI and other forms of capital flows and occurs in the form of know-how or the transfer of management skills. It also refers to a direct or indirect ownership of 10 percent or more of the voting powers of an enterprise residing in one economy (OECD 2008).

Different types of FDI have been identified on the basis of various criteria. Based on the strategic motive of an investment, FDI is classified as: market-seeking FDI, resource-seeking FDI, efficiency-seeking FDI and strategic asset seeking FDI. Resource-seeking investments seek to acquire factors of production that are more efficient than those obtainable in the home economy of the firm. Market-seeking investments aim at either penetrating new markets or maintaining existing ones. Efficiency-seeking investments target enhancing firms’ efficiencies by exploiting the benefits of economies of scale , scope and common ownership (Kinyondo 2012; UNCTAD 1998).

Foreign direct investment is also classified into horizontal and vertical FDI. Horizontal FDI refers to foreign manufacturing products and services similar to those produced in the home market. Vertical FDI refer to those multinationals that fragment production process geographically. It is called vertical because a multinational enterprise (MNE) produces a product that has multiple stages with different production activities (Beugelsdijk and Zwinkels 2008).

Further , FDI can be classified into Greenfield investments, brownfield investments and cross-border mergers and acquisitions. Greenfield investments refer to direct investments in new facilities or an expansion of existing facilities. Greenfield investments are a primary target of a host nation’s promotional efforts because they create new production capacities and jobs, transfer technology and knowledge and can lead to linkages to the global marketplace. In brownfield investments a company or government entity purchases or leases existing production facilities to launch a new production activity. It is one strategy for getting FDI. Mergers and acquisitions transfer existing assets from local firms to foreign firms and are common practices of this category of FDI (Kiyondo 2012; Solomon 2008; UNCTAD 2013).

Several theories of FDI have been postulated to explain its roles and effects including the product life cycle theory, exchange rates on imperfect capital markets theory, internalization theory and the eclectic paradigm of Dunning theory. The production cycle theory was developed by Vernon (1966) to explain four stages of production: innovation, growth, maturity and decline (Denisia 2010; Vernon 1966). The exchange rates on imperfect capital markets theory analyzes foreign exchange risk from the view of international trade along with the influence of uncertainty as a factor of FDI. The internalization theory was developed by Buckley and Casson (1976) and then elaborated by Casson (1983) and it explains the growth of transnational companies and their motivations for achieving FDI. The eclectic paradigm of Dunning theory was developed by Dunning (1973). This paradigm includes three different types of FDI: Ownership advantages, location-specific and internalization.

2.1 Evolution of FDI and Role of Institutional Quality in Attracting It

Developing countries as well as countries in transition have been attracting FDI and exploring ways of increasing its inflows. Buckley (1991) distinguished four phases in the history of growth of international private investments. The first phase (1870–1914) focused on the role of multinational enterprises (MNEs) as entrepreneurs and transfer of intangible assets in these 40 years. FDI during this period was transfer of resources between different countries and was used as a means of controlling the use of resources and complementary local inputs. The second phase (1918–1938) was followed by World War I where several challenges in levels, form and structure of international production were encountered. The war itself caused several European countries to aggressively sell some of their pre-war investments. There were also some challenges in its geographical distribution. The size of West European investments in central Europe and USA continued to attract more than two-third of the US direct investment stakes. There were a number of new MNEs which participated in the developing world in the inter-war years including new oil investments in the Mexican gulf, the Dutch East Indies and in the Middle East, copper and iron ore in Africa, bauxite in Dutch and British Guyana, nitrate in Chile, precious metals in South Africa and non-iron metals in South America.

The third phase (1939–1960), witnessed the increasingly important role of European, Japanese and some third world countries as international direct investors. Between 1960 and 1970 the world capital stock increased to US$18 billion of which USA accounted for 48 percent and West Germany and Japan for 18 percent.

Finally, the fourth phase (1960–1978) was a period when the rate of growth of international capital stock reached its peak in the late 1960s, reduced in the early and mid-1970s, UK and USA’s shares kept falling and there was an increase in the shares of West Germany, Japan and Switzerland. In the late 1970s regions such as Eastern Europe and China opened up. The growth in MNEs’ activities in different service sectors like banking, insurance, advertising and tourism and the increasing use of cross-border arrangements through multilateral agreements were some of the development indices during this time.

Several factors are responsible for increasing international flows of investments. Institution as a determinant of FDI was established in the distant past. The quality of institutions may matter in attracting FDI. Wei (2000) investigated the lack of institutional quality reflected in corruption by civil servants which generated mistrust and was unhealthy for the business community and for both domestic and foreign investors.

However, FDI has shown an increasing trend over time. In particular, the growth rate of FDI inflows to Africa and Eastern Africa increased in absolute terms between 1970 and 2015. Africa’s FDI share in developing countries fell from 33 percent in 1970 to 7.3 percent in 2013, but the share of East Africa in Africa as a whole rose from 6.3 percent in 1970 to 25.5 percent in 2013 and the total FDI inflows into Africa were approximately 12.6 percent in 2014 (AEO 2016).

To examine the role of FDI in economic growth , it is important to study its theoretical foundation. Its roles have been analyzed in a theoretical framework of the classical international trade theory of comparative advantage and differences in factor endowments between countries (Sala and Trivin 2014). Further , the importance of capital in an economy has been well stated in Keynesian, neoclassical and endogenous growth theories.

Most recently, the new growth theory acknowledged the importance of FDI in starting economic growth through financing new investments and technology transfers (Sala and Trivin 2014). Unlike previous theories, the new growth models emphasize the role of research and development , human capital accumulation and externalities in economic growth (Romer 1994).

Moreover, one can find vast empirical evidence on the nexus between FDI and economic growth . While there is consensus on the theoretical outcomes of FDI on economic growth , there is a disagreement in the empirical findings. There are mixed results from this perspective. Balasubramanyam (1996) analyzed the relationship between FDI and economic growth in developing countries using cross-sectional data and ordinary least squares . His findings showed that FDI had a positive impact in developing countries that had adopted export-oriented strategies but not in countries that had implemented import-oriented strategies.

Borensztein et al. (1998) examined the impact of FDI on economic growth by focusing on the role of technological diffusion in 69 developing countries . Their findings indicate that FDI was an important driving factor for transfer of technology, which eventually contributed more to economic growth than domestic investments . The study concluded that FDI had a positive impact on economic growth , but the amount of growth depended on the availability of human capital . DeMello (1999) extended Borensztein et al. (1998) study accounting for both developing and developed countries. The findings of this study showed the existence of a positive impact of FDI on economic growth for both developed and developing countries . The study found that FDI inflows had a positive impact on economic growth in countries with higher income levels and substantial privatization.

In contrast, some studies have found a negative relationship between FDI and economic growth . For instance , Herzer et al. (2008) indicate that the relationship between FDI and economic growth in selected sample countries was indeterminate. Apergis (2008) found that FDI had a negative effect on economic growth in countries that had lower income levels and ineffective liberalization policies.

Sukar and Hassan (2011) investigated FDI’s effects on economic growth in sub-Saharan African countries by using 25 years’ panel data over the period 1975–1999. They found that FDI had a positive effect on the economic growth of these countries. On the other hand, Alege and Ogundipe (2013) found a negative effect of FDI on economic growth in the ECOWAS region. Their study indicated that the negative effect got stronger with the level of under-development; the growth-stimulating effect of FDI depended on human capital , the quality of institutions, infrastructure and other country specific factors.

Sala and Trivin (2014) examined the relationship between trade openness , investments and economic growth in sub-Saharan African countries using the GMM estimation method to the dynamic growth model. They examined the existence of both conditional and unconditional convergence models. Their findings show that globalization (trade openness ) and FDI had a significant effect on economic growth in the past three decades.

Agrawal (2015) analyzed FDI’s impact on economic growth in BRICS economies using panel data. The study focused on integration and a causality analysis at the panel level, which indicated the presence of a long run relationship between FDI and economic growth in BRICS.

Existing empirical literature provides mixed results on the determinants of FDI inflows. Valeriani and Peluso (2011) examined the impact of institutional quality on economic growth in 69 developed and developing countries using the fixed effect model. Their results revealed that a country with better institutional quality had better economic growth and attracted more FDI inflows . Basemera et al. (2012) analyzed the role of institutions in determining FDI inflows to East Africa between 1987 and 2008 based on the Dunning eclectic paradigm using the fixed effects and random effects models. Their study found that economic risk rating, financial risk rating and corruption significantly influenced FDI inflows to East Africa. However, governance and law and order were insignificant in influencing FDI inflows.

Baklouti and Boujelbene (2014) explain the impact of institutional quality in attracting FDI in the Middle East and North America (MENA) region over the period 1996–2008 using fixed effects models of panel data in eight selected countries. Their result indicate that corruption and regulatory quality had a negative influence on FDI. Nondo et al. (2016) found an insignificant relationship between institutional quality and FDI inflows to 45 sub-Saharan African countries in 1996–2007 using the fixed effects estimation technique. Many sub-Saharan African countries scored very low on all dimensions of institutional quality. However, these findings should be interpreted very cautiously as they do not discount the importance of institutional quality in the sustainable development process in SSA. Accordingly, it is possible that institutional quality may affect FDI indirectly by stimulating other variables including human capital , infrastructure and the health of workers which in turn directly affect FDI. This study revealed that institutional quality was hindering foreign investors in most African countries.

A recent study by Zekarias (2016) investigated FDI’s impact on economic growth in 14 Eastern African countries using the GMM estimation method. The findings of the study indicate that FDI had a positive and marginally significant impact on economic growth in the region. However, the findings did not find any impact of political instability and institutional quality on economic growth in East African countries.

Hence, it can be seen that there is scant empirical evidence on FDI’s impact on economic growth in East Africa and even this evidence has mixed results which may justify further studies. Our study explores the determinants of FDI by filling the missing variables in Zekarias’ (2016) study. Our study thus contributes to existing knowledge by taking into account the impacts of political stability and institutional quality on economic growth and FDI flows in the region.

3 Data and Methodology

3.1 Types and Source of Data

We used secondary data to analyze FDI’s impact and its determinants in Eastern African countries. Panel data was collected from the World Development Indicator database of the World Bank, the World Governance Indicator (WGI) database of the World Bank and Political Risk Services International’s Country Risk Guide (PRS) database. The study used 20 years panel data (1996–2015) for 14 Eastern African countries.

3.2 Population and Sample

Based on the UNCTAD classification, Eastern Africa comprises of 18 countries: Burundi, Comoros, Ethiopia, Kenya, Madagascar, Malawi, Mauritius, Mozambique, Seychelles, Rwanda, Uganda, Tanzania, Zambia, and Zimbabwe, Djibouti, Eritrea, Somalia and South Sudan. However, we excluded the last four countries from our study due to data limitations. Data for these countries was missing in the indicated sources. Therefore, the first 14 countries were included in the econometric analysis .

3.3 Model Specification

FDI is required for reducing the capital and income gap between developing and developed countries under endogenous growth . FDI impacts growth by improving the productivity of domestic and foreign capital. We estimated two models in our study. The first model was developed to examine FDI’s effects on economic growth and the second one was used for exploring the relationship between FDI and explanatory variables such as institutional quality and political instability. To find the impact of FDI on economic growth , we used a Solow-swan aggregate production (Solow 1956) from the augmented Cobb-Douglas production function as a theoretical foundation. The model is specified as:

Model one:

Where, Y is growth of output, Kd is domestic capital, Kf is foreign capital, L is labor force and E is the multiplier effect from FDI, \( \upalpha \) and \( \beta \) are the elasticity of labor and capital to output (Y) respectively and A refers to efficiency of production. The human capital augmented Lucas model (Lucas 1988; Romer 1994) divides labor into human capital (HC) and labor force (LF). Based on its productivity the rate of economic growth is affected by capital (K), the level of infrastructure (INFRA), inflation (INF), foreign trade (OPEN), political stability (POLSTA) and institutional factors. We used regulatory quality as a proxy for institutional quality. Using these variables, our modified model is:

where, Y is the GDP growth rate, FDI is foreign direct investment , GFCF is gross fixed capital formation (earlier known as domestic private investment), HC is human capital , LF is the labor force, INFRADEV is infrastructure development , OPEN is the value of foreign trade which is the sum of exports and imports, INF is the rate of inflation, POLSTA is political instability, INST is the institutional quality proxied by regulatory quality and \( \varepsilon \) is the general error term. Since the relationship between growth in output (dependent variable ) and the independent variables is non-linear, the explicit form of the model given in Eq. (2) is:

where, β1… β9 are respective factor contributions to growth and \( \varepsilon \) is the error term.

As panel models comprise both longitudinal and cross-sectional data they have dynamic dimensions across space, time and variables (Wooldridge 2005). In our study, there are 14 cross-countries, 20 years’ data and 13 variables. Therefore, Eq. (3) was further modified to include cross-sectional units and time. Thus, the dynamic cross-country growth model is given by:

where, i refer to cross-sectional units, that is, countries, t refers to time units in years (1996–2015) and \( \mathop \varepsilon \nolimits_{it} \) is the composite disturbance term. For computational convenience and easier understanding, the non-linear equation is converted into a linear equation through a logarithmic transformation as:

where, β0 is the intercept, β1, β2 … β9 are coefficients of the respective explanatory variables, Y it is growth rate of GDP which is the dependent variable , all the variables as explained earlier are transformed into a natural logarithm and \( {\text{U}}_{\text{it}} \) is the error term which is natural logarithm of \( \mathop \varepsilon \nolimits_{it} \).

Model two:

An alternative model was formulated to examine the determinants of FDI (Eq. 6). Institutional quality, political instability and human capital were used as explanatory variables.

where, FDI is foreign direct investment , INST is regulatory quality proxy for initutional quality, POLSTA is political stability to indicate the level of political instability and \( \mathop \varepsilon \nolimits_{it} \) is the error term.

3.4 Estimation Technique

To investigate FDI’s impact on economic growth in East Africa we used the generalized method of moments (GMM ) of dynamic panel data. GMM is a statistical method that combines observed economic data with information in population conditions to produce estimates of unknown parameters of the economic model (Zsohar 2012). The advantage of dynamic panel estimation methods like GMM is that they address the endogenity problem , work to eliminate the serial correlation and easily eliminate the hetroscedasticity problem. GMM is a general framework for deriving estimators that are consistent under weak distributional assumptions (Wooldridge 2001).

We used the Arellano-Bond dynamic panel estimator in our study. This method starts by transforming all regressors, usually by differencing and uses the generalized method of moments and is called difference GMM. The difference GMM estimator is designed for a panel analysis and embodies the assumptions about data generating of the dynamic model , with current realizations of the dependent variable which are influenced by past realizations but in this case there may be arbitrarily distributed fixed individual effects (Arellano and Bond 1991; Hansen 1982).

3.5 Diagnostic Tests

We conducted several diagnostic tests to confirm the appropriateness of the method and the adequacy of the variables among which are cross-sectional dependence , over-identification , autocorrelation and the panel unit root test . First, we tested the existence of cross-sectional dependence . DeHayos and Sarafidis (2006) have shown that if there is cross-sectional dependence in the disturbances all estimation procedures that employ the generalized method of moments such as Anderson and Hsiao (1981), Arellano and Bond (1991), and Blundell and Bond (1998) are inconsistent as N (the cross-sectional dimension) grows large for fixed T (the panel’s time dimension). As a result, our study also conducted a cross-sectional dependence test.

We also conducted the Sargan \( \overset{\lower0.5em\hbox{$\smash{\scriptscriptstyle\frown}$}}{\beta } \)and Hansen tests of over-identifying restrictions. Here the crucial assumption for the validity of GMM is that the instruments are exogenous. If the model is identified exactly, the detection of invalid instruments is impossible. Even when E(Źϵ) ≠ 0, the estimator will choose so that E(Źϵ) = 0. However, if the model is over-identified, a test statistic for the joint validity of the moment conditions falls naturally out of the GMM framework.

Arellano and Bond (1991, 1995) have developed a test for a phenomenon that would render some lags invalid as instruments due to the existence of autocorrelation in the idiosyncratic disturbance term, ν it . If ν it are themselves serially correlated of order one then yit–2 will be endogenous to νit–1 in the error term in differences, Δε it = ν it –νit–1 making them potentially invalid instruments. To test for autocorrelation aside from the fixed effects, we applied the Arellano-Bond test to the residuals in differences. To check for first-order serial correlation in levels or for second-order correlation in differences a test for correlation between the v it–1 in Δv it and the vit–2 in Δvit–1 is needed. The Arellano-Bond test for autocorrelation has a null hypothesis of no autocorrelation and is applied to the differenced residuals . The test for the AR (1) process in first differences usually rejects the null hypothesis (though not in our case), but this is expected since:

We also conducted the panel unit root test and the panel Granger causality test . Stationarity of individual variables has to be tested before estimating any model. A time series is said to be stationary if its mean, variance and auto covariance remain the same. If time series is non-stationary, the persistence of shocks will be infinite. As we used panel data the Hadri LM test was also done. This LM test has a null of stationary and is distributed as standard normal under the null (Hadri 2000). For each cross-sectional panel in i = 1… N, at time t = 1… T, suppose that:

where, Z it represents the exogenous variables in the model including any fixed effects or individual trends, T is time span of the panel, N represents the number of cross-sections, \( \alpha_{{i}} \) is the autoregressive coefficient and error term ε it is assumed to be mutually independent of idiosyncratic disturbances. Here if \( \left| {\alpha_{{i}} } \right| < 1 \), then Yit is said to be stationary. On the other hand, if \( \left| {\alpha_{{i}} } \right| = 1 \) and then Yit contains a unit root.

Further, we also tested the Granger causality. A variableY is said to Granger cause another variable X if at time t, Xt+1 can be better predicted by using past values of Y. Because panel data gives us more variability, degree of freedom and efficiency and also considering the time series individual regionally disaggregated we introduce panel techniques to improve the validity of our Granger causality test.

Finally, we specified and tested panel cointegration and vector error correction. The use of cointegration techniques to test for the presence of long run relationships among integrated variables has enjoyed growing popularity in empirical literature. Since the panel unit root tests presented earlier indicate that the variables are integrated of order one I (1) we conducted a test for cointegration using the panel cointegration test developed by Pedroni (1999). If two or more series are individually integrated (in the time series sense) but some linear combination of them has a lower order of integration then the series are said to be cointegrated. Besides, once we determined that the two variables were cointegrated we performed a panel-based vector error correction model (VECM) to conduct the Granger causality test to account for both short run and long run causality. We did this using Engle and Granger’s (1987) two-step procedure. In the first step, we estimated the long run model specified in Eq. (9) to obtain the estimated residuals ε it :

where, \( \alpha_{{i}} +\delta_{t} \) are fixed cross-section and trend effects respectively. We included them only when redundant fixed effects showed that this was necessary. Then we estimated the second stage using:

where, Δ is the first difference of the variable, k is the lag length, ECT is the error correction term which is estimated by residuals from the first stage and Uit are the residuals of the model. Here the significance of causality results is determined by the Wald F-test.

3.6 Definition of the Variables

The dependent variable for the first model is growth of national income denoted by Y. We used annual percentage growth rate of GDP at constant 2010 prices in terms of USD. In fact, a higher economic growth rate coupled with stable and credible macroeconomic policies attracts foreign investors (Onyeiwu and Shrestha 2004).

We also identified several variables as independent variables for the first model. Their definitions and expected signs are:

Foreign direct investment (FDI): the net inflows of FDI as a percent of GDP in the host country. It is the sum of equity capital, reinvestments of earnings, other long-term capital and short-term capital as shown in the balance of payments . This series shows net inflows (new investment inflows less disinvestment) in the reporting economy from foreign investors. We expect that FDI positively effects economic growth in East African countries.

Gross fixed capital formation (GFCF): earlier known as gross domestic private investment. Private investment covers gross outlays by the private sector on additions to its fixed domestic assets including land improvements (fences, ditches, drains); plant, machinery and equipment purchases; and the construction of roads and railways including schools, offices, hospitals, private residential dwellings and commercial and industrial buildings. It is measured as private sector investment as a percentage of GDP. It is also expected that this variable will have a positive effect on economic growth in the region.

Human capital (HC): is the aggregation of health, education, on-job training and social welfare . Human capital is one of the determinants of economic growth . Countries with good education and healthcare facilities also have developed economies. There is a positive correlation among economic growth , FDI and level of human capital . We used expenditure on education and health as a percentage of GDP as proxy to human capital . Human capital is expected to have a positive effect on economic growth and attract more FDI.

Institutional quality (INST): regulatory quality was used as proxy for institutional quality which reflects perceptions of people about the ability of the government to formulate and implement sound policies and regulations that permit and promote private sector development. Countries with good institutional quality have better economic development and attract more international investors to boost their economies.

Political stability (POLSTA): measures perceptions about the likelihood of political instability and/or politically motivated violence, including terrorism. A stable political situation leads to higher economic growth and attracting more FDI.

Infrastructure development (INFR): one of the well-recognized factors for economic growth and for attracting FDI. The main argument is that well-established infrastructure such as roads, airports, electricity, water supply, telephones and internet access reduce the cost of doing business and help maximize the rate of returns. It is suggested that the availability of good quality infrastructure subsidizes the cost of total investments and leads to increasing efficiency in production and marketing. To measure the overall infrastructural development of the region we used the number of mobile subscription per 100 population.

Trade openness (OPEN): is the sum of exports and imports as a percent of gross domestic product . A country’s openness can be expressed in different ways—trade restrictions, tariffs and foreign exchange control laws. As the openness of an economy is believed to foster economic growth and level of FDI, the more open an economy, the more likely it is to grow and attract FDI.

Labor force (LF): labor force participation rate is the proportion of the population aged 15–64 years, that is, economically active people who supply labor for the production of goods and services during a specified period.

Inflation rate (INF): inflation as measured by the consumer price index reflects the annual percentage change in costs for an average consumer acquiring a basket of goods and services that may be fixed or may change at specified intervals, such as yearly. A nation’s macroeconomic stability affects both economic growth and FDI flows.

4 Results and Discussion

4.1 Descriptive Statistics of Variables

Our study’s primary focus was examining FDI’s effect on economic growth in East African countries and the role of institutional quality and political stability in attracting FDI to the region. Country level descriptive data on GDP growth rate, FDI, GFCF, human capital , institutional quality, political stability, labor force, inflation rate, trade openness and infrastructure development for 14 East Africa countries for the period of 1996–2015 is presented in Table 1.

As can be seen from Table 1 during the past two decades, Seychelles attracted the highest share of FDI as percentage of its GDP in the region. For the stated period on average it attracted about 12.39 percent share of GDP with a variation of about 10.91. The share of FDI to GDP ranged from 3.95 to 54.06 percent for Seychelles. Mozambique was the second highest FDI recipient country in the region. On average, the country attracted about 11.87 percent FDI as a share of its GDP . Zambia was the third recipient of international investors (on average 5.71 percent). Burundi got the least among the East African countries during the study period (on average 0.61 percent).

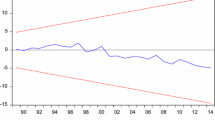

FDI inflows to the regions have been increasing over time. In particular, they have has shown an increasing trend internationally after the financial crisis (2008–2009). FDI flows were volatile depending on various shocks in the international economy. From Fig. 1 it can be seen that FDI inflows to the region were volatile. Seychelles followed by Mozambique attracted more foreign private investments than other countries in the region.

Net inflows of foreign direct investment (1996–2015)

4.2 Results of Diagnostic Tests

We conducted various diagnostic tests on each variable before running the actual model. First, we tested the stationarity of each variable. We used the Hadri Lagrange Multiplier (LM) test to conduct the panel unit root test . The results are given in Table 2.

The test statistics confirm that all the variables were not stationary at level. All the variables (GDP, gross capital formation , FDI, human capital , inflation rate, openness, political stability and institutional quality) become stationary at first difference.

Besides, we also conducted an autocorrelation test of the dynamic panel data using the Sargan test and Hansen statistic. The results are given in Table 3.

The test results provide sufficient evidence to reject the null hypothesis of autocorrelation . This indicates that there is no autocorrelation problem in our models as the probability of the Sargan and Hansen tests is greater than the 5 percent level of significance. We used the robust standard error to remove the problem of hetroscedasticity in the panel data. Moreover, Arreano-Bond AR (1) probability was greater than the 5 percent significance level. Therefore, there was no autocorrelation in our dataset.

We also tested a null hypothesis of the absence of cross-sectional dependence for which we used Pesaran ’s test of cross-sectional independence. The test results are given in Table 4 and these do not provide us sufficient evidence to reject the null hypothesis.

Therefore, our model has no problem of panel cross-sectional dependence .

Similarly, we did the cointegrated test using both Johansen and Fisher cointegration tests. The results of the Fisher cointegration test, which is system based are given in Table 5.

We can reject the null hypothesis of no cointegration between the variables of interest. Therefore, there is cointegration between the GDP growth rate and FDI inflows.

Finally, we estimated the panel vector error correction model to see the long run dynamics of the model.

As we can see from Table 6 the coefficient of C1 (error correction term ) is negative and significant. This indicates that there is long run causality from the independent to the dependent variable . There is long run causality from international private investments to GDP in the region.

4.3 Estimation Results of the Difference GMM

We used the difference GMM estimation method to examine the determinants of economic growth in East African countries. The results provide long run as well as short run effects of the covariates on the GDP growth rate. In particular, FDI had a positive and marginally significant effect on economic growth in the region. However, in the short run foreign private investments had a positive but insignificant effect on the GDP growth rate. Our results are consistent with some other studies (Demelew 2014; Zekariyas 2016).

As can be seen from Table 7, human capital and infrastructure development were negatively related to GDP growth. Since human capital and infrastructure are still poor in East Africa, our results justify the reality of the region. Despite the theoretical importance of human capital in growth and development, its practical contribution to Eastern African countries is not clear in the short run. There are many reasons for this including: (i) usually human capital development is gained through education, and it takes a long time to realize its returns, (ii) the cost of education and hence human capital is huge so that poor households may not be able to afford its cost in the short run and the government hardly provides the required education for all citizens at a time, (iii) brain drain is one of the serious challenges in the sub-region; competent productive forces are migrating to advanced economies, and (iv) the existing manpower may be placed in wrong positions which reduces the motivation and productivity of labor. Given these pitfalls of human resource utilization, our findings confirm the actual situation in East Africa.

Trade openness benefits small economies rather than large economies because small economies cannot affect world supply and hence world prices. This means their influence in world supply is insignificant and does not affect world demand and price levels. Small countries (Eastern Africa) are price takers in the global market. According to Krugman and Obstfeld (2006), a country gains from international trade at least in the form of a comparative advantage. Although most of these countries are too small to impact the world market, foreign trade has a positive effect on their economic growth .

Most of the time the sub-region faces trade deficit but the contribution of trade to growth is positive and insignificant. The reason for this could be that they import more capital goods (which induce investments and growth) than consumer goods. This signals how foreign trade integration is important for continuous economic growth in the sub-region. Empirically, Sala and Trivin’s (2014) work confirms our findings.

After examining FDI’s role in the economic growth of the region, we examined the determinants of FDI. FDI inflows to host countries are influenced by an array of factors which can be categorized as characteristics of the market (doing business), investment incentives and environmental policies. Characteristics of doing business encompass factors like economic and political stability, geographical position, factors of production (costs and quality), the institutional environment, technology levels, purchasing power of domestic demand and the business environment. Investment incentives include variables like tax policy and incentives and the trade policies of host countries. Contemporary development is facing stricter challenges from the environmental effects of development. As a result, several countries have formulated and implemented environmental policies. This to a larger extent is becoming a bottleneck for FDI. Therefore, the extent and strictness of environmental policies in host countries are important determinants of FDI. Our study was constrained by the availability of data for the selected countries and so it examined the effect of some of the determinants of FDI in East African countries. The results are given in Table 8.

As we can see from the results in Table 8, a one period lag of FDI had a positive and significant effect on FDI. This implies that the previous year’s inflow of FDI determined its inflows in the current year. This could be due to the fact that successful experiences of previous investors impacted others to come and invest in the area. A one period lag of institutional quality had a positive but insignificant effect in attracting FDI. A country with better institutional quality attracted more inflows from international investors and vice versa and there was a negative relationship between the two variables.

Political instability negatively affected foreign investment flows. The negative coefficient of a one period lag in political instability though insignificant signals this fact. Lack of good governance, civil conflict, unclearly defined land property rights and corruption reduced FDI flows and its effects on economic growth in the region. In the end, there was a positive correlation between gross fixed capital formation and FDI inflows. In the long run, gross fixed capital formation had a positive effect on FDI inflows to the region, though this was insignificant.

The coefficients of infrastructure development of a one period lag were negative. Infrastructure development affected international investments directly or indirectly. Empirical evidence shows that there was poor infrastructure development in the region. There were more international investors in a country that had suitable infrastructure development like roads, electricity, railways, airways, and so on. A one period lag of labor force had a negative and significant effect. Improved infrastructure provided attractive investment conditions, and may lead to more production, income and ultimately economic growth . Infrastructure was negatively related to the growth rate in the short run, but was positive and significant in the long run.

5 Summary and Conclusion

Our study analyzed the impact of FDI on economic growth in 14 East African countries using dynamic GMM estimators after conducting appropriate diagnostic tests. All the hypothesized variables were tested to be valid. First, FDI had a positive and marginally significant impact on economic growth in East African countries in the long run. However, institutional quality and political stability had an insignificant effect in attracting FDI to the region. This could raise questions about the nature of FDI flows to the region.

A pairwise Granger causality test indicated the existence of a unidirectional causality running from GDPGR to FDI inflows in the region. Hence, foreign investors came to a country which had a good economic performance. FDI is becoming significant for economic growth in the region. Eastern African countries need to attract more FDI by improving their investment environments, building key infrastructure, investing more in human capital , increasing regional integration, strengthening internal coordination and external relations, following up on export-oriented investments and doing careful impact evaluations. However, care should be taken about the composition of FDI and its maturity stage profit repatriation and low tax collection due to tax holidays to attract more FDI. A detailed study is needed to see the environmental effects of FDI in the region since this may undo its positive effects in economic growth in the region.

References

Abadi, B.M. (2011). The Impact of Foreign Direct Investment on Economic Growth in Jordan. International Journal of Recent Research and Applied Sciences, 8(2): 253–258.

AEO (2016). African Economic Outlook 2016: Sustainable Cities Structural Transformation. African Development Bank.

Agrawal, G. (2011). Impact of FDI on GDP Growth: A Panel Data Study. European Journal of Scientific Research, 57(2): 257–264.

Agrawal, G. (2015). Foreign Direct Investment and Economic Growth in BRICS Economies: A Panel Data Analysis. Journal of Economics, Business and Management, 3(4): 421–424.

Alege, P. and A. Ogundipe (2013). Sustaining Economic Development of West African Countries: A System GMM Panel Approach. MPRA Paper, 51702. Ota, Ogun: Covenant University.

Anderson, T.W and C. Hsiao (1981). Estimation of Dynamic Models with Error Components. Journal of the American Statistical Association, 76: 598–606.

Anyanwu, J.C. (2012). Why Does Foreign Direct Investment Go Where It Goes? New Evidence from African Countries. Annals of Economics and Finance, 13(2): 425–462.

Apergis, N. (2008). The Relationship Between Foreign Direct Investment and Economic Growth: Evidence from Transition Countries. Transition Studies Review, 15: 37–51.

Arellano, M. and S. Bond (1991). Some Tests of Specification for Panel Data: Monte Carlo Evidence and Application to Employment Equation. Review of Economic Studies, 58(2): 277–297.

Arellano, M. and O. Bover (1995). Another Look at the Instrumental-Variable Estimation of Error Components Models. Journal of Econometrics, 68(1): 29–52.

Baklouti, N. and Y. Boujelbene (2014). Impact of Institutional Quality on the Attractiveness of Foreign Direct Investment. Journal of Behavioral Economics, Finance, Entrepreneurship, Accounting and Transport, 2(4): 89–93.

Balasubramanyam, M.S. (1996). Foreign Direct Investment and Growth in EP and is Countries. The Economic Journal, 106(434): 92–105.

Basemera, S., J. Mutenyo, E. Hisali, and E. Bbaale (2012). Foreign Direct Investment Inflows to East Africa: Do Institutions Matter? Journal of Business Management and Applied Economics, 5. Available at: http://jbmae.scientificpapers.org.

Beugelsdijk, R.S. and R. Zwinkels (2008). The Impact of Horizontal and Vertical FDI on Host Country’s Economic Growth. International Business Review, 17: 452–472.

Blundell, R. and S. Bond (1998). Initial Conditions and Moment Restrictions in Dynamic Panel Data Models. Journal of Econometrics, 87: 15–143.

Borensztein, E., J. De Gregorio, and J.W. Lee (1998). How Does Foreign Direct Investment Affect Economic Growth? Journal of International Economics, 45: 115–135.

Buckley, P.J. (1991). Development in International Business Theory in the 1990s. Journal of Marketing Management, 7: 15–24.

Buckley, P. and M. Casson (1976). The Future of the Multinational Enterprises. London: Macmillan.

Casson, M. (1983). Internalization as General Theory of Foreign Direct Investment. Cambridge: MIT Press.

DeHoyos, R.E. and V. Sarafidis (2006). Testing for Cross-Sectional Dependence in Panel-Data Models. The Stata Journal, 6(4): 482–496.

Demelew, T.Z. (2014). Foreign Direct Investment Led Growth and Its Determinants in Sub-Saharan African Countries. Masters thesis, Paper 1284. Available at: http://thekeep.eiu.edu/theses/1284.

DeMello, L.R. (1999). Foreign Direct Investment-Led Growth: Evidence from Time Series and Panel Data. Oxford Economic Papers, 51(1): 133–151.

Denisia, V. (2010). Foreign Direct Investment Theories: An Overview of the Main FDI Theories. European Journal of Interdisciplinary Studies, 3: 53–59.

Dunning, J.H. (1973). The Determinants of International Production. Oxford Economic Papers, 25: 289–336.

Engle, R.E. and C.W.J. Granger (1987). Cointegration and Error-Correction: Representation, Estimation, and Testing. Econometrica, 55(2): 251–276.

Hadri, K. (2000). Testing for Stationarity in Heterogeneous Panel Data. Econometrics Journal, 3: 148–161.

Hansen, L.P. (1982). Large Sample Properties of Generalized Method of Moments Estimators. Econometrica, 50: 1029–1054.

Herzer, D., S. Klasen, and D.F. Nowak-Lehmann (2008). In Search of FDI-Led Growth in Developing Countries: The Way Forward. Economic Modelling, 25: 793–810.

Kinyondo, M. (2012). Determinants of Foreign Direct Investment. Global Journal of Management and Business Research, 12(18): 20.

Krugman, P. and M. Obstfeld (2006). International Economics: Theory and Policy (9th ed.). English: Pearson Addison Wesley.

Lucas, R.E. (1988). On the Mechanics of Economic Development. Journal of Monetary Economics, 22(1): 3–42.

Nondo, C., M.S. Kahsai, and Y.G. Hailu (2016). Does Institutional Quality Matter in Foreign Direct Investment? Evidence from Sub-Saharan African Countries. African Journal Economic and Sustainable Development, 5(1): 12–30.

OECD (2008). OECD Benchmark Definition of Foreign Direct Investment. Paris: OECD.

Onyeiwu, S. and H. Shrestha (2004). Determinants of Foreign Direct Investment in Africa. Journal of Developing Societies, 20(1–2): 89–106.

Pedroni, P. (1999). Critical Values for Co-integration Test in Heterogeneous Panels with Multiple Regressors. Oxford Bulletin of Economics and Statistics, Special Issue: 653–670.

Romer, P.M. (1994). The Origins of Endogenous Growth. The Journal of Economic Perspectives, 8(1): 3–22.

Sala, H. and P. Trivin (2014). Openness, Investment and Growth in Sub-Saharan Africa. Journal of African Economies: 1–33.

Solomon, W.D. (2008). Determinants of Foreign Direct Investment in Ethiopia. Maastricht, The Netherlands: Maastricht University.

Solow, R.M. (1956). A Contribution to the Theory of Economic Growth. The quarterly Journal of Economics, 70(1): 65–94.

Sukar, A. and S. Hassan (2011). The Effects of Foreign Direct Investment on Economic Growth: The Case of Sub-Sahara Africa. South Western Economic Review, 34(1), 61–73.

Todaro, M.P. and S.C. Smith (2012). Economic Development (11th ed.). New York, San Francisco, and Upper Saddle River: Addison-Wesley.

UNCTAD (1998). World Investment Report 1998: Trends and Determinants. New York and Geneva: UNCTAD.

UNCTAD (2013). Global Value Chains: Investment and Trade for Development. World Investment Report. New York: United Nations.

UNCTAD (2016). World Investment Report 2016: Investor Nationality: Policy Challenges. New York: United Nations, UNCTAD.

Valeriani, E. and S. Peluso (2011). The Impact of Institutional Quality on Economic Growth and Development. Italy: University of Modena and Reggio Emilia.

Vernon, R. (1966). International Investment and International Trade in the Product Cycle. The Quarterly Journal of Economics, 80(2): 190–207.

Wei, S. (2000). How Taxing is Corruption on International Investors? Review of Economics and Statistics, 82(1): 1–11.

Wooldridge, J.M. (2001). Applications of Generalized Method of Moments Estimation. Journal of Economic Perspectives, 15(4): 87–100.

Wooldridge, J.M. (2005). Introductory Econometrics: A Modern Approach (2nd ed.). Thomson South-Western.

Zekarias S.M. (2016). The Impact of Foreign Direct Investment (FDI) on Economic Growth in Eastern Africa: Evidence from Panel Data Analysis. Applied Economics and Finance, 3(1): 145–160.

Zsohar, P. (2012). Short Introduction to the Generalized Method of Moments. Hungarian Statistical Review, Special Number 16.

Author information

Authors and Affiliations

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2018 The Author(s)

About this chapter

Cite this chapter

Bekere, B., Bersisa, M. (2018). Impact of Foreign Direct Investment on Economic Growth in Eastern Africa. In: Heshmati, A. (eds) Determinants of Economic Growth in Africa. Palgrave Macmillan, Cham. https://doi.org/10.1007/978-3-319-76493-1_4

Download citation

DOI: https://doi.org/10.1007/978-3-319-76493-1_4

Published:

Publisher Name: Palgrave Macmillan, Cham

Print ISBN: 978-3-319-76492-4

Online ISBN: 978-3-319-76493-1

eBook Packages: Economics and FinanceEconomics and Finance (R0)