Abstract

Evidence from this study shows a significant relationship between growth and income inequality in which inequality creates a negative impact on the growth, but the impact of economic growth on income inequality is nonlinear. This result captures the Kuznets Hypothesis, finding the level of growth that can reduce unequal distribution of income in Thailand. Finally, this study also discovers a certain level of inflation that can help reduce income inequality effectively.

Access provided by Autonomous University of Puebla. Download conference paper PDF

Similar content being viewed by others

Keywords

1 Introduction

The relationship between income disparity and economic growth has been a critical issue in macroeconomics over several decades. Countries need economic growth to improve standard of living, reduce poverty, and also to survive in the modern economy. But in the meantime a rise in growth can also cause the inequality which may lead to a long-standing problem which in turn can become destructive to the growth.

While we seem to consider the inequality as a consequence of economic growth, some economists tend to argue that inequality may affect the growth at the same time and perhaps it is necessary to propel the growth. ‘Two sides of the same coin’ is what Ostry and Berg, IMF staff, used to define the effect of inequality on economic growth through their paper in 2011 [13]. They reckoned that the impact of unequal distribution of income is split into two sides. Inequality can influence the growth negatively and become a problem for society. For example, it can obstruct the human capital accumulation especially in education. That is because individuals having higher income can invest more in education than poor people can and have lots of choices in occupation. Recently, IMF has released one more discussion paper about inequality and growth entitled ‘Causes and Consequences of Income Inequality: A Global Perspective’ [5]. One part of this paper refers to a negative effect of inequality on growth and reckons that inequality can also leads to political and economic instability, resulting in corruption, resource misallocation, and nepotism. In contrast, inequality can also be good for economy since it provides incentives for people to invest and save for their future livelihood and also for entrepreneurs to run their businesses successfully [10]. Inequality does not instantly propel economy but without inequality economy is like socialism where the growth of economy hardly exists.

Trade-off between increasing growth and reducing inequality

While growth is needed, inequality still matters. Some economists suggest that an improvement in income distribution and economic growth can be achieved at the same time [2]. Simon Kuznets, an American economist who received the Nobel Memorial Prize in Economic Sciences in 1971, hypothesizes that as a country develops, the economic inequality would first increase and then later decrease [9]. This hypothesis is graphed as an inverted-U shape called ‘Kuznets Curve’ where the horizontal x-axis is income per capita and the vertical y-axis is economic inequality. This inverted-U shape curve implies that income inequality following the curve is gradually increased resulting from economic evolution. That is, at the initial level of low economic growth, income inequality is also low. Then, as countries seek to increase the rate of economic growth, industrial sector often plays a key role to achieve the goal. This event leads to a big gap between rich and poor, and hence income inequality increases. According to the Kuznets Hypothesis, the level of inequality keeps rising as long as the economic growth increases. However, according to the same hypothesis, inequality will be decreased after the growth reaches some certain level, a threshold, in which the economy is developed efficiently resulting in an increase in average income, an improvement in social welfare of society, higher educated populations, and so on.

Motivated by this reasoning, this paper aims to investigate whether the Kuznets Hypothesis holds in the case of some developing country like Thailand where Thai government has been trying to promote the economic growth and especially with a concern about inequality at the same time. This is crucially important because, if we could prove that the hypothesis holds and the result could illustrate the threshold accurately, it means we can find the proper rate of economic growth that will not hurt income distribution in the long term. Our findings should be useful for the Thai government and policy makers and can contribute to longer-run benefits for society.

2 Econometric Modeling Framework

Investigating the inverted U-shaped curve or the so-called Kuznets curve is a profoundly complicated problem and difficult to do in the real world because economic growth and income inequality themselves actually depend on many factors. Therefore, an appropriate tool for investigating this phenomenon with special concern in the real mechanism of growth and income inequality becomes so important. As in the literature, numerous studies failed to find the Kuznets curve, especially the empirical studies on time series (see, e.g., Gallup [6]). Therefore, this paper presents a novel tool of investigating the Kuznets curve that is the simultaneous kink equation (SKE) model. We employ the idea of Kink regression with unknown threshold as introduced in Hansen [7] for identifying the unequal effect of growth on the distribution of income.

2.1 Introduction to the SKE Model

This study deals with a simultaneous relationship between income inequality and economic growth and speculates some covariate variables can produce effects that would be considered both negative and positive. Therefore, Kink regression model with unknown threshold is applied to the simultaneous equation model in order to capture our considerations. What is the kink regression? Briefly, it is simply a regression discontinuity model. The regression function itself is continuous but the slope is discontinuous at a threshold point, thereby a kink [7]. With that in mind, we have the simultaneous kink equation (SKE) model as an econometric model for this work. The SKE model can take the form as:

The model above contains \( m \)-simultaneous kink equations where \( (y_{1,t} , \ldots ,y_{m,t} ) \) and \( (\varepsilon_{1,t} , \ldots ,\varepsilon_{m,t} ) \) are \( T \times 1 \) vector of dependent variables and error terms, respectively. \( X_{i,t} \) is a \( T \times k \) matrix of \( k \) exogenous regressors, and \( Y_{ - i,t} \) is a \( T \times G \) matrix of \( G \) endogenous regressors on the right-hand side of the ith equation. Note that exogenous and endogenous regressors can simply be viewed as independent variables of the model. The exogenous regressors refer to \( X_{i,t} \). The endogenous regressors refer to the dependent variable of other equations \( Y_{ - i,t} \) that also work as an independent variable for this ith equation. Therefore, this structure is called the simultaneous equation model. The term \( (\sigma_{1} , \ldots ,\sigma_{m} ) \) are the scale parameters of margin 1,…,\( m \) and \( (\varepsilon_{1,t} , \ldots ,\varepsilon_{m,t} ) \) are the margin errors that follow some distributions. Following Hansen [7], we generate negative and positive functions of real number \( a \) as \( (a)_{ - } = \hbox{min} (a,0) \) and \( (a)_{ + } = \hbox{max} (a,0) \), respectively, in order to separate the regressor variables into two regimes. For ith equation, the coefficients with respect to the right hand side variables are equal to \( (\beta_{1i}^{ - } , \ldots \beta_{mi}^{ - } ) \) for the values of \( Y_{ - i,t} \) less than certain values \( (r_{1i} , \ldots ,r_{mi} ) \), and \( (\phi_{1j}^{ - } , \ldots ,\phi_{mj}^{ - } ) \) for the values of \( X_{i,t} \) less than \( (r_{1j} , \ldots ,r_{mj} ) \). Conversely, the coefficients will be \( (\beta_{1i}^{ + } ,..,\beta_{mi}^{ + } ) \) and \( (\phi_{1j}^{ + } , \ldots ,\phi_{mj}^{ + } ) \) if the values of \( Y_{ - i,t} \) and \( X_{i,t} \) are larger than \( (r_{1i} ,..,r_{mi} ) \) and \( (r_{1j} , \ldots ,r_{mj} ) \), respectively, and yet the regression function is continuous in all variables [7].

2.2 Modelling Dependence with Copulas

In our SKE model, it is assumed to have a correlation between the errors across \( m \) - simultaneous kink equations; therefore a joint distribution or dependency is somehow needed. We are thinking about the term ‘Copulas’ which are the best way to give us a joint cumulative distribution function. Therefore, we employ the copulas to measure the nonlinear dependence structures with different marginal distributions as in the suggestions of Wichitaksorn et al. [18] and Pastpipatkul et al. [14]. The estimation of our proposed model ‘the Copula based SKE’ will be discussed later.

What is Copulas? It is a parametrically specified joint distribution which is generated from any given marginal distribution [17]. The main advantage of using copulas is to separate the marginal behavior and dependence structure of variables from their joint distribution function [11]. This paper applies both bivariate Elliptical Copulas and Archimedean Copulas to model the dependence structure in the SKE model. Here, our model has two equations, the economic growth and the inequality equations, \( m \) = 2, in which \( u_{1} \) and \( u_{2} \) are the marginal distributions of \( \varepsilon_{1} \) and \( \varepsilon_{2} \), respectively. Let \( u_{1} = F(\varepsilon_{1} ) \) and \( u_{2} = G(\varepsilon_{2} ) \). According to Sklar’s Theorem (see Nelson [12]), the marginals can be inserted into any copula function C taken a form as \( C(u_{1} ,u_{2} ) = C(F(\varepsilon_{1} ),G(\varepsilon_{2} )) \), where \( u_{1} \) and \( u_{2} \) are uniformly distributed and bounded on [0,1].

Elliptical Copulas. Two common elliptical copulas considered here are the Gaussian and Student’s t. By considering the bivariate Gaussian Copula which is parameterized by the linear correlation coefficient \( \rho \), the function form can be defined as

where \( \Phi _{\rho } \) is the bivariate Gaussian distribution function and \( \Phi _{\rho }^{ - 1} \) is the inverse univariate Gaussian distribution function. Next, the bivariate Student’s t distribution is expressed in terms of

where \( T_{\kappa ,v}^{{}} \) is the bivariate Student’s t distribution function and \( T_{\kappa ,v}^{ - 1} \) is the inverse univariate Student’s t distribution function. Parameters \( v \) and \( \kappa \) are degree of freedom and dependence parameter, respectively.

Archimedean Copulas. Following Cherubini et al. [3], Archimedean copula can be defined as

where \( \Phi \) is a strictly generator with \( \Phi ^{ - 1} \) completely monotonic on [0, ∞). Let’s consider the bivarite Archimedean class consisting of Clayton, Gumbel, Frank, and Joe copulas.

-

1.

Clayton Copula. The Clayton copula is usually referred to in the bivariate case. It has an ability to capture lower tail dependence. The closed from of this copula is given by

$$ C_{\theta }^{Cl} (u_{1} ,u_{2} :\theta ) = (u_{1}^{ - \theta } + u_{2}^{ - \theta } - 1)^{ - 1/\theta } $$(5)where \( \theta \) is a degree of dependence, \( 0 < \theta < \infty \). If \( \theta \to \infty \) the Clayton Copula will converge to the monotonicity Copula with positive dependence, but if \( \theta = 0 \) then the marginal distributions become independence.

-

2.

Gumbel Copula. The Gumbel copula is employed to model asymmetric dependence of marginals. It is used to capture an upper tail dependence and weak lower tail dependence. The form of bivariate Gumbel copula is given by

$$ C_{\theta }^{G} (u_{1} ,u_{2} :\theta ) = \exp ( - [( - \log u_{1}^{{}} )^{\theta } + ( - \log u_{2}^{{}} )^{\theta } )^{1/\theta } ) $$(6)where the copula parameter \( \theta \) is restricted on the interval [1,\( \infty \)).

-

3.

Frank Copula. The Copula function of Frank Copula can be defined by

$$ C_{\theta }^{F} (u_{1} ,u_{2} ,\theta ) = - \theta^{ - 1} \log \left\{ {1 + \frac{{(e^{{ - \theta u_{1} }} - 1)(e^{{ - \theta u_{2} }} - 1)}}{{\text{e}^{ - \theta } - 1}}} \right\} $$(7)where the copula parameter \( \theta \) is restricted on the interval (\( - \infty \),\( \infty \)).

-

4.

Joe Copula. The Joe copula is defined by

$$ C_{\theta }^{J} (u_{1} ,u_{2} ,\theta ) = 1 - ((1 - u_{1} )^{\theta } + (1 - u_{2} )^{\theta } )^{1/\theta } $$(8)where the copula parameter \( \theta \) is restricted on the interval [1,\( \infty \)).

2.3 Estimation Technique

As we construct two-equation SKE model to represent growth and inequality, the bivariate copula is considered as a joint for these two equations. Prior to the model estimation, we need to check the stationary of the data so that we use the Augmented Dickey-Fuller unit roots test. The estimation technique we employ here is the maximum likelihood estimation where the log likelihood function of our model can be defined by

The terms \( \Theta _{1} = \left\{ {\alpha_{1} ,\beta_{1i}^{ - } ,\beta_{1i}^{ + } ,r_{1i} ,r_{1i} ,\phi_{1j}^{ - } ,\phi_{1j}^{ + } } \right\} \), \( \Theta _{2} = \left\{ {\alpha_{2} ,\beta_{2i}^{ - } ,\beta_{2i}^{ + } ,r_{2i} ,r_{2i} ,\phi_{2j}^{ - } ,\phi_{2j}^{ + } } \right\} \) and \( \theta \) are the estimated parameters of the growth equation, the income inequality equation, and copula parameter, respectively. In this study, we consider four different marginal distributions namely Normal, Student’s t, skewed Normal, and skewed Student’s t distributions. Copula families, i.e. Gaussian, Student’s t, Clayton, Gumbel, Frank, and Joe, are employed to join these two different marginals or to create a joint distribution function of a bivariate random variable with the univariate marginal distribution.

3 Simulation Study

We conduct a simulation study to explore the performance and accuracy of our proposed Copula based SKE model. The Monte Carlo simulation is employed to simulate dependence parameter for the Copulas. For the Elliptical copulas, we set the true value for the correlation coefficients \( \rho \) (Gaussian) and \( \kappa \) (Student’s t) equal to 0.5 and the additional degree of freedom parameter \( v_{c} \) equal to 4. Then, for the Archimedean copulas, the dependence parameter of Frank and Joe copulas are set as \( \theta \) = 2 and dependence parameter of Clayton and Gumbel copulas are set as \( \theta \) = 3. Then, the obtained uniform data are transformed to \( \varepsilon_{1,t} \) and \( \varepsilon_{2,t} \) using quantile function of marginal distribution choices in which \( \sigma_{1} \) and \( \sigma_{2} \) are equal to 1, the additional degree of freedom parameter of quantile function of the Student’s t distribution \( v \) is equal to 6 and the skewed parameter for skewed distribution is set as \( \gamma \) = 1. In this section, we are not going to examine all subsets of the cases in this simulation study; instead we are especially considering three comprehensive cases shown as follows:

- Case 1 ::

-

Copula based SKE with Normal and Student’s t margins

- Case 2 ::

-

based SKE with Skewed Student’s t and Student’s t margins

- Case 3 ::

-

Copula based SKE with Normal and Skewed Normal margins.

Thus, the simulation model takes the following form:

Prior to generate a dependent variable \( y_{1,t} \), we randomly simulate an independent variable \( X_{1.t} \) from N(15,10) and set the kink point \( r_{11} \) equal to 15, the true value for \( \alpha_{1} \) equal to 1. Moreover, the values for coefficients \( \phi_{11}^{ - } \) and \( \phi_{11}^{ + } \) are set to be −0.5 and 2, respectively. Similarly, to simulate \( y_{2,t} \) in the second equation, first, we have to generate the value of its independent variable, \( y_{1,t} \). However, as we are dealing with the simultaneous equations model, the dependent variable of the first equation also plays a role as an independent variable for the second equation at which \( y_{1,t} \) has been simulated already from the first equation. In addition, we set the value for the kink point \( r_{21} \) equal to 20, the true value for \( \alpha_{2} \) equal to 1, and for coefficients \( \phi_{21}^{ - } \) and \( \phi_{21}^{ + } \) equal to 0.1 and −2, respectively.

To save the space, we decide to show the simulation result only for the first case that is the model with Normal and Student’s t margins. Table 1 shows the results of the Monte Carlo simulation investigating the maximum likelihood estimation of the Copula based SKE model. We found that our model can perform very well through simulation study. The mean parameters are very close to their true values with low and acceptable standard errors. For example, the mean value of the coefficient \( \alpha_{1} \) is 0.90 with standard error equals 0.13 while the true value is 1. This result demonstrates the accuracy of estimation and the same for the other cases. Overall, the Monte Carlo simulation suggests that our model ‘Copula based SKE’ is reasonably accurate.

4 Model Specification and Variables

To test a relationship between income inequality and economic growth, we use the following two equations which are modeled simultaneously. The first equation represents the economic growth and the second equation represents the income inequality which is measured by the best known index Gini coefficientFootnote 1. A key point of this model is that the growth equation contains Gini coefficient and the GDP growth is also entered into the Gini equation to find a direct link between these two factors.

At this stage, we construct this model and decide which economic variables should be included by combining a lot of information from expert advices and literatures. The first part of the growth equation includes change in nominal GDP lagged by one period and structural characteristic (\( Str_{t} \)), where \( \ln (Str_{t} ) = \ln (S_{t} )\, - \,\ln (n_{t} \, + \,0.75) \). The variables capturing structural characteristics were introduced by Sørensen and Whitta-Jacobsen in 2010 to include \( S_{t} \), the country’s average gross investment rate and \( n_{t} \), the growth rate of its average labor force [16]. In brief, they suggest this term is basically needed because growth has its own long run path which is defined by the basic structural characteristics of the country. The next variable is human capital accumulation (\( HC_{t} \)) in terms of education and training, health status, and experience which is found to have greatly positive impact on economic growth and induce sustainable growth. Also, institution should be considered as a cause of the long-run growth [1]. The institution in a society is commonly related to such social mechanisms as democracy, religion, property rights, and rule of law. It determines the incentives and creates constraints in the economy. The last included variable in the growth equation is change in government debt (\( \Delta Debt \)). We consider this term because the literature shows that debt also matters for economic growth.

Next, we will discuss about potential sources influencing income inequality. It is not easy to choose which factors should be included in the Gini equation because inequality is somewhat complicated and unclear to define. However, following the study of Kaasa [8], we are able to classify the factors affecting inequality into four groups as follows. The first group is economic growth and general development of a country where we select the growth in GDP (\( \Delta GDP_{t} \)) and GDP per capita \( (GDP_{t}^{pc} ) \) to represent this group and to describe a particular country’s development level. The second group refers to the political factors which are defined as privatization and the public sector [8]. Privatization is believed to cause wealth concentration which finally leads to income inequality. Therefore, the bigger share of private sector may imply the higher income inequality, thereby the variable \( PS_{t} \). The third group is macroeconomic factors. We especially consider inflation rate (\( Inf_{t} \)) and the number of unemployed people (\( Unemp_{t} \)) to represent this group. The last group is demographic factors. We focus especially on some part of demographic development that is education because education is greatly important for reducing uneven income [5], thereby a variable expenditure on education (\( Edu_{t} \)).

5 Exploring the Link Between Growth and Inequality Using Thailand’s Data

First of all, we’d better explain about data used in this study. We have a quarterly data set of all considered variables, spanning from 1993:Q1 to 2015:Q4. The economic growth data comprises GDP, a structural characteristics, human capital index, institution index, and government debt. In addition, the income inequality data consists of the Gini coefficient, GDP per capita, private sector share of GDP, inflation rate, government expenditure on education, and rate of unemployed labor. We collected all the data from Thomson Reuters DataStream, from Financial Investment Center (FIC), Faculty of Economics, Chiang Mai University, except the Gini coefficients which were collected from the National Statistical Office of Thailand. Additionally, we apply the Augmented Dickey-Fuller (ADF) unit roots test to the subsets of data to examine whether or not the data series contains a unit root, before we estimate the model. We do not show the result here but we found that all variables passed the test at level with probability equal to zero, meaning all of them are stationary.

5.1 Testing for a Kink (Threshold) Effect

This section is conducted to explore whether or not the kink (or threshold) exists with respect to our model. We employ the Likelihood ratio test (LR-test) to test the kink effect following a recommended algorithm of Hansen [7]. The kink effect on a relationship between response variable, y, and its covariate, xi, is examined as a single equation. This algorithm is kept using for each pair of the covariate and response variable. We assume the null hypothesis is linear regression and the alternative is kink regression. The results are shown in Table 2.

Assuming the null hypothesis is true, Table 2 shows that only the covariates \( \Delta GDP_{t} \) and \( \ln (Inf_{t} ) \) reject the null hypothesis of linearity at the 1 % level, and hence their outcomes are said to be in favor of the kink regression. The result implies that the kink test is conclusive regarding the question of whether or not there is a regression kink effect on the economic growth and income inequality due to these covariates. Therefore, the SKE model with specified kink effect can take the form as in the equations that follow. This model is set similarly to Eqs. (11) and (12) but the slope with respect to the GDP growth and inflation are discontinuous since they have a kink at \( \Delta GDP = r_{1} \) and \( \ln \left( {Inf_{t} } \right) = r_{2} \) where we treat the parameters \( r_{1} \) and \( r_{2} \) as the kink points which need to be estimated.

5.2 Selecting Copulas for SKE Model

This part is about selecting a Copula that is best-fit for the data. Given a set of Copula families, we then select the Copula using the Akaike Information Criterion (AIC) and Bayesian Information Criterion (BIC). Again, this paper is interested in some well-known families of Copula, i.e. Gaussian, Student’s t, Clayton, Gumbel, Frank, and Joe, as described in Sect. 5.2, and it assumes four different distributions for the marginals, namely Normal, Student’s t, skewed Normal, and skewed Student’s t distributions. Therefore, we have got sixteen cases for a pair of marginal distributions of the growth and inequality equations, respectively.

According to the results shown in Table 3, the minimum values of AIC and BIC are −796.8 and −741.3 (bold numbers), respectively, from which Gaussian Copula is chosen to be a linkage between normal margin of the growth equation and Student’s t margin of the inequality equation.

5.3 Estimates of Copula Based SKE Model

To explore the relationship between growth and income inequality in Thailand, Eqs. (13) and (14) are estimated by MLE and the results are presented in Table 4. In general, the model can perform well across the data sets and it can capture a nonlinear effect of some variables. Most of the parameters are rightly signed and statistically significant at the conventional levels. The estimation of the growth equation, shown at the beginning of Table 4, reveals that only some variables suggested by the empirical growth literatures, are significant in the case of Thailand. It is found that Thailand’s economic growth depends significantly on the structural characteristics and the Gini coefficient, but the impact of other variables on the economic growth are not significantly found.

The structural characteristic is an essential economic variable and needed for the economy to preserve an existence of convergence. Economists believe that the growth rates have to converge to some steady state equilibrium growth path, however, the convergence will occur due to some important condition that is a negative sign of a coefficient of the characteristics variable in order to let the conditional convergence occur [16]. Our result provides numerical evidence consistent with this condition, the coefficient is −0.0004 meaning that Thailand’s GDP growth converges significantly to a country-specific long run growth path with speed 0.0004. Importantly, we also found a negative relationship between growth and the Gini coefficient. The coefficient is equal to −0.1147, meaning that an increase in the income inequality – measured by Gini coefficient- leads to GDP growth decline in Thailand. In contrast, if we could reduce the Gini coefficient just by 1 %, Thailand’s economic growth could be boosted over 0.11 %.

As also reported in Table 4, income inequality in Thailand depends significantly on GDP growth, inflation, and unemployment. We found that GDP growth has both negative and positive impacts on income inequality, as well as the impacts of inflation. This happens due to the kink effect and we will discuss completely about this effect later. Unemployment is found to be positively correlated with income inequality. We found that the coefficient of unemployment is 0.0106, meaning that an additional 1 % of the growth rate of unemployed worker leads to 0.01 % increase in Gini coefficient. This estimate result confirms the previous works and also the empirical literatures as reported in Sect. 2. However, we failed to find significance for other important variables across this data set, such as GDP per capita, share of private sector, and expenditure on education.

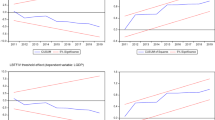

A specific capability of our method allows us to preserve the nonlinear impacts of GDP growth and inflation on income inequality. The impacts are split into two groups based on kink points. In Fig. 1 (a) we display the relationship between Gini coefficient and GDP growth through a regression line, on which the vertical axis is GDP growth and the horizontal axis is income inequality measured by the Gini coefficient. We can see that the regression shows a small positive slope for low GDP growth with a significant kink around 0.0074 (0.74 %), displayed as the blue dot, switching to a negative slope for GDP growth beyond that kink value. This means GDP growth displays a positive impact on the Gini coefficient when the growth is below 0.74 % per quarter. The coefficient of this positive part is 0.0501, meaning that an additional 1 % of GDP growth leads to 0.05 % increase in Gini coefficient. On the other hand, the same Fig. 1 (a) also shows a negative impact on the Gini coefficient when the growth is over 0.74 % per quarter. The coefficient of GDP growth in the negative trend is 0.0206, meaning that an increase in GDP growth by 1 % can cause a reduction in Gini coefficient by 0.02 %.

Plot of Gini coefficient and its covariates estimated by Copula based Kink regression (Color figure online)

In Fig. 1 (b) we illustrate the relationship between Gini coefficient and inflation through another regression line. We can see that the regression shows a steeply positive slope for low inflation with a significant kink around 3.2419 (3.24 %), displayed as the blue dot, switching to a smaller positive slope for the inflation beyond that kink value. The result observes the positive relationship between inflation and income inequality, in which the higher inflation the more income inequality. However, our work can do more than that; we find a salient result that the impacts of inflation on inequality are split into two levels based on the kink point. In the first stage, at any level of inflation below 3.24 %, an additional 1 % of inflation leads to 0.013 % increase in Gini coefficient. But in the second stage, the effect is much less than the first stage. We found that an additional 1 % of inflation just leads to 0.005 % (0.0047) increase in Gini coefficient. This result is consistent with the finding of Crowe [4], CEP researcher and IMF’s officer who first mentions about positive relationship between inflation and inequality that should be separated into two levels.

But, from our opinions, we think it is true that the greater inflation may cause the higher income inequality; but what we suggest here is to use the proper level of inflation to reduce income inequality in the case of Thailand. Our experiment found that in the first stage, under the kink value 3.24 %, the elasticity of the Gini coefficient with respect to the inflation is low; therefore a small decrease in the inflation rate results in a large decrease in the Gini coefficient. In contrast, the elasticity is much higher in the second stage, meaning that even the central bank provides a big decrease in the inflation rate; we can observe just a minor decrease in the Gini coefficient. Hence, it is reasonable to preserve the inflation rate below that kink value.

6 Conclusion

This study attempts to explore the relationship between income inequality and economic growth with special focus on Thailand. We propose Copula based simultaneous kink equations (SKE) model to investigate this relationship. The estimate results show that Thailand’s economic growth depends significantly on the structural characteristics and the Gini coefficient. For income inequality, it is found that the Gini coefficient depends significantly on GDP growth, inflation, and unemployment, in which the first two variables create the kink effects on the Gini coefficient.

Let us explain about our considerable issue, income inequality and growth. We found that the Gini coefficient creates a negative impact on the growth; on the other hand, the growth can create both negative and positive impacts on the Gini coefficient due to the kink effect. This result is corresponding to the Kuznets Hypothesis finding the level of growth that could reduce income inequality. From this data set, we experimentally found that the growth beyond the kink value, 0.74 % per quarter, can reduce income inequality in Thailand. But more than that, we also discover an alternative way to reduce income inequality that is the inflation. Our study found that at any level of inflation under the kink value 3.24 %, a small decrease in the inflation rate results in a large decrease in the Gini coefficient. Therefore, it is reasonable to preserve the inflation rate below that kink value.

Notes

- 1.

The Gini coefficient is a number on a scale measured from 0 to 1, where 0 represents perfect equality and 1 represents total inequality [15].

References

Acemoglu, D., Johnson, S., Robinson, J.A.: Institutions as a fundamental cause of long-run growth. In: Handbook of economic growth, vol. 1, pp. 385–472 (2005)

Boonyamanond, S.: Can equality and growth be simultaneously achieved? Chulalongkorn J. Econ. 19(2), 135–160 (2007)

Cherubini, U., Luciano, E., Vecchiato, W.: Copula Methods in Finance. Wiley, Chichester (2004)

Crowe, C.W.: Inflation, Inequality, and Social Conflict (No. 6-158). International Monetary Fund (2006)

Dabla-Norris, M.E., Kochhar, M.K., Suphaphiphat, M.N., Ricka, M.F., Tsounta, E.: Causes and consequences of income inequality: a global perspective. International Monetary Fund (2015)

Gallup, J.L.: Is there a Kuznets curve. Portland State University (2012)

Hansen, B.E.: Regression kink with an unknown threshold. J. Bus. Econ. Stat. (just-accepted) (2015). doi:10.1080/07350015.2015.1073595

Kaasa, A.: Factors influencing income inequality in transition economies. University of Tartu Economics and Business Administration Working Paper Series (18) (2003)

Kuznets, S.: Economic growth and income inequality. Am. Econ. Rev. 45(1), 1–28 (1955)

Lazear, E., Rosen, S.: nRank order tournaments as optimal salary schemeso. J. Polit. Econ. 89(5), 841 (1981)

Mahfoud, M., Michael, M.: Bivariate Archimedean copulas: an application to two stock market indices. BMI Paper (2012)

Nelson, R.B.: An Introduction to Copulas, vol. 139. Springer Science & Business Media, New York (2013)

Ostry, J.D., Berg, A.: Inequality and unsustainable growth: two sides of the same coin? (No. 11/08). International Monetary Fund (2011)

Pastpipatkul, P., Maneejuk, P., Wiboonpongse, A., Sriboonchitta, S.: Seemingly unrelated regression based copula: an application on thai rice market. In: Huynh, V.-N., Kreinovich, V., Sriboonchitta, S. (eds.) Causal Inference in Econometrics, pp. 437–450. Springer International Publishing, Switzerland (2016)

Ray, D.: Development Economics. Princeton University Press, Princeton (1998)

Sørensen, P.B., Whitta-Jacobsen, H.J.: Introducing Advanced Macroeconomics: Growth and Business Cycles. McGraw-Hill higher education, New York (2010)

Trivedi, P.K., Zimmer, D.M.: Copula Modeling: An Introduction for Practitioners. Now Publishers Inc., Hanover (2007)

Wichitaksorn, N., Choy, S.T.B., Gerlach, R.: Estimation of bivariate copula-based seemingly unrelated Tobit models. Discipline of Business Analytics, University of Sydney Business School. NSW (2006)

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2016 Springer International Publishing AG

About this paper

Cite this paper

Maneejuk, P., Pastpipatkul, P., Sriboonchitta, S. (2016). Economic Growth and Income Inequality: Evidence from Thailand. In: Huynh, VN., Inuiguchi, M., Le, B., Le, B., Denoeux, T. (eds) Integrated Uncertainty in Knowledge Modelling and Decision Making. IUKM 2016. Lecture Notes in Computer Science(), vol 9978. Springer, Cham. https://doi.org/10.1007/978-3-319-49046-5_55

Download citation

DOI: https://doi.org/10.1007/978-3-319-49046-5_55

Published:

Publisher Name: Springer, Cham

Print ISBN: 978-3-319-49045-8

Online ISBN: 978-3-319-49046-5

eBook Packages: Computer ScienceComputer Science (R0)