Abstract

There is a shift in focus from traditional accounting-based performance measures to the new value-based performance measures. With the rising focus on value-based performance measures which are derived from the long-term goal of wealth maximization as opposed to the short-term approach of profit maximization, EVA and FCF are promising indicators. Many past researches have shown that value-based performance indicators (especially EVA) are superior to traditional indicators like EPS, ROE, ROA, etc. Traditional indicators do not capture value creation and since they are accounting based, they can be manipulated by the managers. Therefore using them as firms’ performance measure is not in the best interest of the shareholders. The purpose of this study is to understand the various value-based performance measures and empirically verify the conceptual equivalence of free cash flow (FCF) and economic value added (EVA). For this, a sample of 30 firms listed in BSE SENSEX is taken and their FCF and EVA are calculated for the period of 5 years, from 2011 to 2015. The results of this calculation are analyzed using correlation and regression analysis. The descriptive analysis shows that there is a strong correlation between FCF and EVA. The regression analysis also shows that EVA and FCF are positively related which means that both EVA and FCF give similar results regarding firms’ performance. The discounting of appropriately defined cash flows (FCF) is conceptually equivalent to discounting economic profits (EVA) for performance and decision-making process. This study has empirically tested the conceptual equivalence of the two measures.

Access provided by CONRICYT-eBooks. Download conference paper PDF

Similar content being viewed by others

Keywords

34.1 Introduction

The paper discusses about value-based concepts: free cash flows (FCF) and economic value added (EVA) and their mathematical equivalence. The FCF is calculated by discounting cash flows and EVA is calculated by discounting appropriately defined economic profits. The central idea of both approaches is that operating profit after tax (NOPAT), derived by adding after-tax interest payments to net profit after taxes. The FCF approach focuses on the intermittent total cash flows calculated by deducing total net investment and adding net debt issuance to net operating cash flow, whereas the EVA mechanism requires defining the intermittent total investment in the firm. In a project valuation context, both FCF and EVA are conceptually equivalent to net present value. The FCF is important, the reason it enables the company to practice opportunities that enhance stakeholders’ value. The free cash flow reports the cash that a company is able to generate after laying out the money required to maintain or expand its asset base. Without cash, it’s difficult to develop new products, make acquisitions and takeovers, pay dividends, and reduce the liabilities.

The economic value added determines profit performance by taking into account direct cost, such as interest and cost of capital. Therefore, a company can formulate the profitable corporate strategy, business operations, and cost of capital. The EVA holds great potential; it does not show measurements by percentage term, unlike return on equity and return on assets, but with the monetary value that investors are well-known with. Investors get an insight on the corporate value at a glance and are able to compare how their profit surrounds the expected investors return.

The purpose of this article is to examine how FCF and EVA are actually calculated and empirically check whether both the approaches are actually mathematically equivalent or not. So data has been taken for the 30 firms listed on the Bombay Stock Exchange BSE SENSEX, and FCF and EVA values are calculated for the last 5 years.

34.2 Literature Review

The corporate finance has evolved over time shifting its focus from the traditional short-term approach of profit maximization to the modern long-term approach of wealth maximization, i.e., maximizing shareholder’s wealth. Shareholders aim to maximize the returns on their investments and for that they use financial data of firms to assess its current performance and predict future performance.

Chen and Dodd (1997) highlighted that there is no single accounting measure that accounts for the variability of shareholder’s wealth. They suggested that information from economic value added (EVA) helps in explaining stock returns (as a good accounting measures used to assess firm performance should). Traditionally performance was measured using net operating profit after tax (NOPAT), earnings per share (EPS), return on equity (ROE), return on assets (ROA), etc. Using these measures to assess the firm’s performance is not in the best interest of shareholders because these measures do not capture value creation. EVA and other value-based financial management have been preferred as performance indicators since then. Some of the important studies on value based performance measures are Burksaitiene (2015); Kaplan and Zingales (1997); Parvaei and Farhadi (2013); Ibendahl and Fleming (2003); Stewart III (1994); Unnisa and Janakiramudu (2014); Wells et al. (1995) and provides some intuitions to further investigate its relevance in the emerging corporate world.

Stewart (1991) demonstrated that “Earnings, EPS and earnings growth are misleading measures of corporate performance,” “The best realistic intermittent performance measure is economic value added,” and “EVA stands well out from the crowd as the single best measures of value creation on continuous basis.” Lovata and Costigan (2002) claim EVA reduces agency cost. Maditinos et al. (2006) suggested EVA is strongly associated with stock returns. Ferguson et al. (2005) concluded that EVA improves stock performance. Lefkowitz (1999) and Finegan et al. (1991) concluded that there is a high correlation between EVA and market value added (MVA) as compared to other performance measures like cash flows, EPS, capital growth, and ROE. Mann and Sicherman (1991) studied announcement of seasoned issues of common equity during years 1982, 1983, and 1984. The equities were selected from the Investment Dealer’s Digest of Corporate Financing. The equity of banks, bank holding companies, insurance companies, public utilities, limited partnerships, real estate investment trusts (REIT), and foreign-based firm industries and organizational forms was excluded from the sample. The study concluded that equity issues result in increase in free cash flow (FCF) available to managers and that these nonbonded funds carry agency costs and present evidence that shareholders do expect misuse of this FCF and condition their response to the firm’s acquisition history.

Shrieves and Wachowicz (2001) explored the relationship among EVA, free cash flow (FCF), and traditional net present value (NPV) methods from a valuation perspective. Beginning with cash budget identity, they showed that for valuation and decision-making purposes, with some accounting adjustments, discounting clearly defined cash flows with FCF approach is theoretically and rationally equivalent to discounting clearly defined economic profits under EVA approach. The difference among the two approaches is computational, that is, the FCF approach focuses on intermittent total cash flow, whereas EVA requires clearly defined intermittent total investment. Subatnieks (2005) empirically studied and calculated FCF of Latvian firms and also concluded the theoretical similarity of EVA, FCF, and NPV. Kaviani (2013) analyzed ten companies representing the automotive industry of Iran Stock Exchange for a period of 5 years from 2005 to 2009 to test the hypothesis that there is significant relationship between EVA and created value from FCF to firm and equity (i.e., FCFF and FCFE). The research concludes that EVA can serve investors and managers well to interpret and predict FCF.

There has not been a conformity on a single best performance measure in the literature. For example, O’Byrne (1996) suggested that earning measures have stronger involvement with share returns compared to EVA. Goetzmann and Garstka (1999) reported long-term performance of a firm is related to earnings and that earning per share (EPS) does a better job at explaining differences across firms and for predicting future performance. Turvey et al. (2000) examined a sample of 17 publicly traded food companies in Canada and could not find any correlation between EVA and MVA. Gunther et al. (1999) studied the German stock market and could not prove that value-based measures outperform traditional accounting-based measures. Worthington and West (2004) that showed using pooled time series and cross-sectional data on 110 Australian companies over the period 1992–1998 proved that earnings are more strongly connected to returns than FCF and EVA. Sharma and Kumar (2010) argue that EVA is not a better indicator of firm performance as compared to traditional performance measurement tools based on the sample taken from developed countries. Hence, it is essential to verify this notion for the emerging market like India. To explain the corporate performance, some more longitudinal studies are needed to validate the current status of EVA.

34.3 Data Sources and Empirical Model

The present study is based on the data collected from the financial statement of 30 firms. The data has been collected from Capitaline Databases maintained by Centre for Monitoring Indian Economy (CMIE). It provides data from firms’ financial reports and stock exchanges. The financial data is updated annually, whereas the shareholding details and share price data are updated quarterly and daily, respectively.

The data of 30 companies listed in BSE SENSEX (Sensitive Index) for the period of 5 years, from 2011 to 2015, has been used for the study. The BSE SENSEX, also called BSE30 or just SENSEX, is based on free-float market-weighted stock market index of 30 blue-chip Indian firms and financially sound firms across key sectors listed on Bombay Stock Exchange. The data collected includes profit before tax (PBT), tax, interest, depreciation, total net investment, total debt, total shareholder funds, and capital employed.

For the analysis and comparison of FCF and EVA, statistical tools like descriptive statistics and regression analysis have been used. Descriptive analysis is done for annual net operating profit after tax (NOPAT), FCF, and EVA. To evaluate the effect of FCF on EVA, we develop a regression model with EVA as dependent variable and FCF as independent variable. The regression is done separately for individual years from 2011 to 2015 (see Table 34.3) for the 30 companies listed in BSE SENSEX. The data collected is used to calculate required variables using the following relationships:

where

NOPAT: net operating profit after tax

NPAT: net profit after tax

t: tax rate, calculated as the fraction of PBT (profit before tax) paid as tax:

WACC is the weighted average cost of capital and is calculated as follows:

where

k d : cost of debt

k e : cost of equity

w d : weight of debt, calculated as debt capital/capital invested

w e : weight of equity, calculated as equity share capital/capital invested

and finally,

The following regression model is used:

where

β 0: intercept

β 1: coefficient of FCF

ε: classical error term

34.4 Empirical Results and Discussion

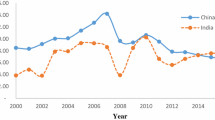

In this section we present the empirical relevance between free cash flow and the economic value added. The results are presented in the form of summary statistics, covariances, and regression for sections of years. First, we summarize descriptive statistics of FCF and EVA for the previous 5 years (see Table 34.1). The mean, median, standard deviation, standard error, and maximum-minimum values for 30 companies from BSE SENSEX have been calculated for each year from 2011 to 2015. The data presented is in ten million rupees. Graphical representations of FCF and EVA are also shown for better understanding of the readers (see Fig. 34.1). We can see that minimum mean FCF and EVA are in the year 2015 and the maximum in the year 2011.

Change in average FCF and EVA with time

This section discusses how the two variables, FCF and EVA, are correlated. Correlation has been calculated for every year from 2011 to 2015 for 30 companies included in BSE SENSEX. It is found that FCF and EVA exhibit strong positive correlation with each other (as can be seen in Table 34.2). The strong correlation between EVA and FCF suggests that with increase in one of the factor increases the other and vice versa. The correlation is strongest in the year 2011 and weakest in 2014 with given covariances. The average correlation over the 5 years is 0.798. The significant correlation measures imply that over a period of time, the free cash flow and economics value added remain similar; this happen due to theoretical mathematical equivalence of EVA and FCF. To test this equivalence, we developed the regression model as mentions in the previous sections, and the results are presented in Table 34.3.

This section discusses the relationship between the FCF and EVA of the 30 companies included in BSE SENSEX from year 2011 to 2015. The following model has been used for linear regression between the two variables: the equation \( \mathrm{E}\mathrm{V}\mathrm{A}={\beta}_0+{\beta}_1\mathrm{F}\mathrm{C}\mathrm{F}+\varepsilon \) and the hypothesis \( {H}_0:{\beta}_1\ne 0\kern1em {H}_A:{\beta}_1=0 \). Regression has been carried out independently for each year for 30 data points pertaining to the 30 companies of the sample. Regression results for the 5 years show that EVA and FCF are positively related to one another, and these results are highly significant as null hypothesis is not rejected even at 99.5 % confidence interval. This positive relationship comes from the fact that both are positively related to NOPAT. Table 34.3 shows the empirical output for years through 2015–2011; the slope of each years’ FCF appears to be positive and statistically significant. The accounting profit reported annually based on the fiscal year and the estimated slope of the FCF indicate that in all the period, the intermittent free cash flow explains the current years’ economic value additions.

34.5 Conclusion

With the rising focus on value-based performance measures which are derived from the long-term goal of wealth maximization as opposed to the short-term approach of profit maximization, EVA and FCF are promising indicators. Many past researches have shown that value-based performance indicators (especially EVA) are superior to traditional indicators like EPS, ROE, ROA, etc. Traditional indicators do not capture value creation and since they are accounting based, they can be manipulated by the managers. Therefore, using them as firms’ performance measure is not in the best interest of the shareholders. The discounting of appropriately defined cash flows (FCF) is conceptually equivalent to discounting economic profits (EVA) for performance and decision-making process. This study has empirically tested the conceptual equivalence of the two measures. The high correlation and the regression analysis suggest that both EVA and FCF give similar results. The regression analysis also shows that EVA and FCF are positively related which means that both EVA and FCF give similar results regarding firms’ performance. This positive relationship comes from the fact that both are positively related to net operating profit after tax.

References

Burksaitiene D (2015) Measurement of value creation: economic value added and net present value. Econ Manag 14:709–714

Chen S, Dodd JL (1997) Economic value added (EVATM): an empirical examination of a new corporate performance measure. J Manag Issues JSTOR 318–333

EVA SBG (1994) Fact and fantasy. J Appl Corp Financ 363–652. Cited as G. Bennett Stewart III (1994), EVA™: Fast and fantasy. J Appl Corp Financ 7(2):71–84

Ferguson R, Rentzler J, Yu S (2005) Does economic value added (EVA) improve stock performance profitability? J Appl Financ Fall/Winter Vol. 15, 101–113

Finegan PT et al (1991) Maximizing shareholder value at the private company. J Appl Corp Financ 4:30–45

Goetzmann WN, Garstka SJ (1999) The development of corporate performance measures: benchmarks before EVA

Günther T, Landrock B, Muche T (1999) Profit versus value-based performance measures. Unpubl. Work. Pap. Dresden Univ., pp 1–27

Ibendahl G, Fleming R et al (2003) Using economic value added (EVA) to examine farm businesses. In: Annu. Meet. South. Agric. Econ. Assoc. Mobile, Alabama, February

Kaplan SN, Zingales L (1997) Do investment-cash flow sensitivities provide useful measures of financing constraints? Q J Econ JSTOR 112(1):169–215

Kaviani M (2013) Study of information content economic value added in explain new models based on free cash flow (CVFCFF and CVFCFE). Int J Account Financ Report 3:277

Lefkowitz SD (1999) The correlation between EVA and MVA of companies. MBA Diss. Calif. State Univ

Lovata LM, Costigan ML (2002) Empirical analysis of adopters of economic value added. Manag Account Res 13:215–228

Maditinos ID, Sevic Z, Theriou NG (2006) The introduction of economic value added (EVA) in the corporate world. Southeuropean Rev Bus Account 4:1–11

Mann SV, Sicherman NW (1991) The agency costs of free cash flow: acquisition activity and equity issues. J Bus JSTOR 64(2):213–227

O’Byrne SF (1996) EVA{®} and market value. J Appl Corp Financ 9:116–126

Parvaei A, Farhadi S (2013) The ability of explaining and predicting of economic value added (EVA) versus net income (NI), residual income (RI) & free cash flow (FCF) in Tehran stock exchange (TSE). Int J Econ Financ 5:67

Sharma AK, Kumar S (2010) Economic value added (EVA)-literature review and relevant issues. Int J Econ Financ 2:200

Shrieves RE, Wachowicz JM Jr (2001) Free cash flow (FCF), economic value added (EVA™), and net present value (NPV): a reconciliation of variations of discounted-cash-flow (DCF) valuation. Eng Econ 46:33–52

Stewart GB III (1991) The quest for value. New York

Subatnieks K (2005) Concept of cash flow and assessment of cash flow ratios of Latvian companies. Organ Vadyb Sist Tyrim 36:163

Turvey CG, Lake L, Van Duren E, Sparling D (2000) The relationship between economic value added and the stock market performance of agribusiness firms. Agribusiness 16:399–416

Unnisa N, Janakiramudu P (2014) Is EVA a superior measure of shareholder value? Evidence from CNX Nifty Constituent Firms. Asian J Financ Account 6:388–401

Wells BP, Cox LA, Gaver KM (1995) Free cash flow in the life insurance industry. J Risk Insur JSTOR 62(1):50–66

Worthington AC, West T (2004) Australian evidence concerning the information content of economic value-added. Aust J Manag 29:201–223

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2017 Springer International Publishing AG

About this paper

Cite this paper

Shaikh, I. (2017). On the Examination of Value-Based Performance Measures: Evidence from Indian Firms. In: Tsounis, N., Vlachvei, A. (eds) Advances in Applied Economic Research. Springer Proceedings in Business and Economics. Springer, Cham. https://doi.org/10.1007/978-3-319-48454-9_34

Download citation

DOI: https://doi.org/10.1007/978-3-319-48454-9_34

Published:

Publisher Name: Springer, Cham

Print ISBN: 978-3-319-48453-2

Online ISBN: 978-3-319-48454-9

eBook Packages: Economics and FinanceEconomics and Finance (R0)