Abstract

Despite the importance of innovation in business performance, investigation into innovation in services is scanty and lacking consensus. In retailing, it is a topic that has been awakening considerable academic and business interest in recent years. In this study context, this work analyses innovation in retail experiences from two aspects—marketing innovation and technological innovation—to understand the role it exercises in satisfaction and subsequent recommendation. For that purpose, our objective is to investigate the direct and indirect influence of marketing and technological innovation on satisfaction and word of mouth through three core constructs: store image, consumer value, and store brand equity. On a sample of 820 retail customers of grocery, clothing, furniture, an electronics store and using SEM methodology, the results show that technological innovation is more important than marketing innovation in shaping image, value, and satisfaction. At the same time, store image is the variable that most influences customer satisfaction and that satisfaction is a very significant antecedent of word-of-mouth behaviour. Practical implications for retail managers and further research are presented.

Access provided by CONRICYT-eBooks. Download conference paper PDF

Similar content being viewed by others

Keywords

Introduction

Innovation in the services sector has received less attention (Djellal et al. 2013). Specifically in retailing, although retailers are one of the most influential actors in developed economies, the study of retail innovation from a conceptual and an empirical perspective is relatively poor compared to other sectors. Innovation refers to the generation of new ideas that stimulate economic performance in a company. It is based on creating and bringing into profitable use new technologies, new products, new services, new marketing ideas, new systems, and new ways of operating. One new research line is related to the activities and practices of marketing (Gil et al. 2014). There is still only scanty empirical evidence to relate this type of innovation with variables associated with satisfaction and loyalty. Furthermore, the rapid evolution of information and communication technologies (hereinafter ICT) has radically changed market conditions by providing new instruments to add value to customer experience. There is a consensus in the literature over the advantages of ICT use for firms such as cost reductions, more customer satisfaction, increased market share, more flexible jobs, and better competitive advantages (e.g., Gil et al. 2014). In this line, technological innovation in retailing is also a recent area of interest with challenges and debates still to be resolved (Renko and Druzijanic 2014).

Our work focuses on the study of retail innovation by exploring marketing innovation and technological innovation from the consumer perspective. To tackle this analysis, we investigate the direct and indirect effects of both types of innovation on satisfaction, as well as the influence of satisfaction on word-of-mouth (hereinafter WOM) behaviour. Three relevant variables were selected for this study from the retailing literature, which are also closely related to satisfaction and loyalty: store image, consumer value, and store brand equity. Firstly, image as a key strategic tool for achieving a competitive advantage, which is receiving particular attention nowadays (Kumar et al. 2014). Secondly, value because it has been found to be especially relevant in retail experiences in recent years (Yoon et al. 2014). And thirdly, brand equity which is an emerging area in the context of stores which requires greater in-depth study (White et al. 2013). Our aim, therefore, is to study the contribution of marketing and technological innovation on satisfaction and WOM behaviour through image, consumer value, and brand equity in retailing experiences. This analysis will enable us to detect differences in the effects of each type of innovation and further understanding of the relationship between innovation and customer satisfaction. These results can help commercial managers to design strategies and distribute resources oriented towards improving customers’ levels of satisfaction and their subsequent recommendations.

Theoretical Background

Marketing and Technological Innovation

Regarding marketing practices, attempts to define and classify marketing innovation in retail are still scanty. One of the most representative contributions is from Homburg et al. (2002), who consider that it refers to the degree of adoption of new ideas about merchandising or services. Most of the contributions are merely conceptual (e.g., Musso 2010), some are based on qualitative studies with a business focus (Hristov and Reynolds 2015), and there is a minority of quantitative works applied to the end consumer. In short, the study of marketing innovation in retailing presents major challenges and areas to be exploited.

Technological innovation, through the introduction and development of ICTs, has become consolidated in recent years as a long-term strategic investment, which can deliver competitive advantages by generating value for the end consumer. There are, however, clear opportunities for improvement for businesses in the sector, because according to the 2014 report of the Spanish National Observatory on Telecommunications and the Information Society (ONTSI 2015), retail commercial distribution is at intermediate levels of development and access to advanced ICTs. Technologies like radio-frequency identification (RFID) and self-scanning/self-payment for products and mobile applications are a genuine technological revolution which will be vital for the competitive improvement of those firms (Gil et al. 2014), but require further investigation.

Store Image

Store image management is a key strategic tool for achieving a competitive advantage. Currently, the concept is receiving considerable attention from academia and the business world (Kumar et al. 2014). Study of image management began in the 1950s, and the literature is very extensive. Most authors use Martineau’s classical conceptualisation (1958: 47) as their basis, according to which image is the way in which the shopper’s mind pictures the store, partly by its functional qualities and partly by its atmosphere of psychological attributes. Recently, Jinfeng and Zhilong (2009: 488) define it as perceptions of consumers on primary marketing activities of a store.

Therefore, image reflects the store’s identity or personality, because it is a combination of beliefs and perceptions based on tangible and intangible elements that consumers attribute to an establishment (Hartman and Spiro 2005). It is agreed that image is a subjective, consumer-centred concept and totally dependent on the context. Thus, a variety of variables have been recognised as contributing to image formation. The most common are quality, atmosphere, product display, services, convenience, prices, and assortment, although the variables mentioned are also made of emotions, accessibility and location, loyalty programmes, and payment methods (e.g., Kumar et al. 2014).

Consumer Value

Value has received special attention in recent years (Gallarza et al. 2011). The most commonly accepted conceptualisation of value was given by Zeithaml (1988: 14) who defined it as the consumer's overall assessment of the utility of a product based on perceptions of what is received and what is given. This get-versus-give perspective considers value as a global assessment consumers make in an exchange over the relationship between benefits and sacrifices. Additionally, value can easily be confused with satisfaction, but these constructs are different. Value takes into account the exchange sacrifices, whereas satisfaction does not. Value occurs at various stages of the purchase process, whereas satisfaction is a post-purchase evaluation (Oliver 1997).

Academic research has proposed many typologies of value (e.g., Holbrook 1999; Sweeney and Soutar 2001; Gallarza et al. 2011), which have given rise to different dimensions, from the most utilitarian and functional to the most hedonic. From the empirical perspective, retail studies have traditionally focused on more utilitarian aspects of the shopping process, but more recent literature indicates that consumers have motivations which go beyond the purchase of the product. Typologies of value can be grouped into the following four approaches: (1) benefits versus sacrifices, (2) transaction value versus acquisition value of the product, (3) utilitarian value versus hedonistic value, and (4) Holbrook’s (1999) typology. Among the different dimensions of value, economic value has traditionally been considered the main component of consumer-perceived value (Sullivan et al. 2012), and so we adopt this focus in this work.

Store Brand Equity

Brand equityFootnote 1 is an emerging concept in the retail distribution literature (White et al. 2013). It is based on the concept of brand equity that traditionally focuses on the product, refers to the added value derived from the existence of the brand, and occurs when consumers make favourable associations with a familiar brand (Yoo et al. 2000). One of the most outstanding contributions in the literature on brand equity is from Aaker (1991: 15) who defines it as a set of brand assets and liabilities linked to a brand, its name and symbol, that add to or subtract from the value provided by a product or service to a firm and/or to that firm’s customers.

Various authors recognise that the bases of brand equity can apply to the store, but with some variations (e.g., Pappu and Quester 2006). Contributions on store brand equity are somewhat limited and mainly highlight the power brand knowledge (Hartman and Spiro 2005) and added value that the store (Jinfeng and Zhilong 2009) has over the consumer. Most studies focus on the conceptual and dimensional aspects (e.g., Hartman and Spiro 2005), identifying research lines (e.g., Grewal and Levy 2007) or developing measures (e.g., Pappu and Quester 2006). Regarding the analysis of antecedents and consequences, whereas the literature on product-oriented brand equity is more extensive, works applied to retailing are fewer (e.g., Gil et al. 2013). The most recent studies indicate that empirical evidence is difficult to compare due to the diversity of variables, terms, and measures.

Satisfaction

Satisfaction is the main objective for retail managers and a concept of great interest in consumer research. It has been defined in the literature from a specific/cumulative approach to a cognitive/affective approach (Oliver 1997). Regarding the first approach, satisfaction with a concrete experience is an approach shared by many authors (e.g., Giese and Cote 2000). However, in the retailing context, satisfaction refers to a set of accumulated experiences. In the second approach, the cognitive perspective points out that satisfaction is a judgement on a pleasurable level of consumption-related fulfilment (Oliver 1997). In this line, store satisfaction refers to a subjective evaluation that the store meets or exceeds expectations. The affective perspective states that satisfaction is a summary of emotional responses of varying intensity (Giese and Cote 2000). Converging both approaches, Lovelock and Wirtz (1997: 631) define satisfaction as a person’s feelings of pleasure or disappointment resulting from a consumption experience when comparing a product’s perceived performance or outcome in relation to his or her expectations. Following the latter approach, we consider customer satisfaction with the store to be a cumulative, affective, and cognitive evaluation.

WOM Behaviour

One of the consequences of satisfaction is WOM behaviour or recommendations. This response is one of the most significant and recognised dimensions in the loyalty literature. Although it was originally studied in the 1960s, there has been a significant increase in academic investigation in recent years. There are different definitions of the WOM concept (e.g., Litvin et al. 2008). For example, according to the classic definition of Westbrook (1987: 261), WOM is all informal communications directed at other consumers about the ownership, usage, or characteristics of particular goods and services or their sellers. Significant aspects of WOM definitions should be highlighted. Firstly, it is direct and personal and contains an independent message from the company which is more real and credible than advertising or promotion (Litvin et al. 2008). Therefore WOM excludes formal communication from customers to companies (complaints or suggestions) and from companies to customers (promotional activities) (Mazzarol et al. 2007). Secondly, WOM is also both an antecedent (as a risk reduction strategy) and a consequence of consumers’ evaluations (to help, revenge, or reduce cognitive dissonance) (Halstead 2002).

WOM has been characterised traditionally as having a two-dimensional nature, with an evaluative dimension (valency or extent to which the information is positive) and a conative dimension (degree of diffusion to others) (Harrison-Walker 2001; Halstead 2002). More recent works have identified new WOM dimensions. For example, Gelbrich (2011) considers referral and activity as WOM dimensions. Referral is the degree to which customers praise and recommend an organisation and its products or services (Swan and Oliver 1989), and activity is the intensity of talking to others about the advantages and benefits (Harrison-Walker 2001). Gelbrich (2011: 212) argues both dimensions may become salient when customers experience particular emotions. Since consumer experiences in retailing have some hedonic and emotional content, we follow this approach in our context.

Hypotheses

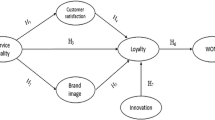

One of the areas of innovation which calls for more studies is the contribution of marketing innovation to satisfaction and other related constructs, like value and image. Various authors agree that the main objective of innovation is to create value for customers; otherwise innovation would be an expense. According to Sekhon et al. (2015), services innovation positively impacts on value excellence. Works like those by Weerawardena et al. (2006) highlight the importance of innovation in improving business image. In addition, the essence of innovation, from a marketing perspective, consists in offering customers something unique and different that satisfies their needs. Therefore, all marketing innovation should be oriented towards attracting and satisfying customers. In this line, Gil et al. (2014) find a significant direct relationship between satisfaction and innovation in the store. These empirical evidences indicate that consumers’ perceptions of innovation in the store’s marketing practices will have a positive effect on image, value, and satisfaction judgements (Fig. 1). Therefore, we posit the first group of hypotheses: H 1 —marketing innovation in retail experience has a positive impact on H 1a store image, H 1b consumer value, and H 1c satisfaction.

Proposed model

As already noted, the development of ICTs provides advantages in the form of value not only for consumers (Thiesse et al. 2009) but also through businesses by improving competitiveness (Gil et al. 2014). This increased competitiveness can be transferred to customers by improving consumers’ brand image (Yeh 2015) and reducing the price of the products. Following these contributions, we assume that the innovation perceived by customers in the technologies introduced in the store can have a positive effect on image and perceived value. Some works show that these effects lead to increased customer satisfaction stemming from the introduction of ICTs. In fact, as Renko and Druzijanic (2014) point out, technological innovation enables retail companies to understand customer needs better and so they can develop strategies to improve their satisfaction. This finding also suggests that perceived technological innovation will have a positive impact on satisfaction. Therefore, we posit the second group of hypotheses: H 2 —technological innovation in retail experience has a positive impact on H 2a store image, H 2b consumer value, and H 2c satisfaction.

Regarding the potential effect of store image on satisfaction, many works recognised that this image plays an important role in these judgements (e.g., Yoon et al. 2014). One of the most representative works on the causality between image and satisfaction is the study by Bloemer and De Ruyter (1998). More recently, Thomas (2013) confirms that satisfaction mediates the relationship between image and loyalty. Therefore, we consider that the image consumers have of the store will have a positive and direct impact on satisfaction (Fig. 1), so we posit the following hypothesis: H 3 —Store image in retail experience has a positive impact on satisfaction.

The influence of consumer value on store brand equity is another relationship we attempt to test. In this area, various works dealing with the nature of brand equity have identified perceived value as one of its dimensions (e.g., Gil et al. 2014). There are, however, various empirical studies that confirm the impact of value or different dimensions of value, like price or perceived quality on store brand equity (e.g., Jinfeng and Zhilong 2009; Gil et al. 2013). In addition, the influence of value on brand equity can be explained by the “use of signals” theory proposed by Richardson et al. (1994), according to which consumers base their decisions on the elements of marketing-mix business designs. Given that value represents a cost-benefit comparison (Zeithaml 1988), this value can be a key indicator of the assessment of a brand (Teas and Agarwal 2000), can generate preference and positive attitudes, and therefore influence brand equity. Following this approach and taking into account the above evidence, we assume that if consumers perceive a store as providing higher value, thanks to investment in marketing actions (e.g., price reductions), they will show greater preference and consequently their perception of brand equity will improve. Therefore, we propose the following hypothesis: H 4 —Consumer value in retail experience has a positive impact on store brand equity.

In addition to the effect of image on consumer satisfaction, store brand equity can also play a significant role in those judgements. On this issue, several works have related brand equity with increased customer satisfaction. These contributions indicate that if brand equity represents the added value perceived by the consumer of the brand (Yoo et al. 2000), the associations, preferences, or positive attitudes customers may have about the store brand may condition their assessments of the shopping experience and therefore influence their level of satisfaction. So we posit the following hypothesis: H 5 —Store brand equity in retail experience has a positive impact on satisfaction.

Finally, as regards the satisfaction-WOM relationship, there are some contradictory results for the link between satisfaction and loyalty. However, many recent studies in retailing confirm the direct effect of satisfaction on WOM behaviour or intention (e.g., Nesset et al. 2011; Fuentes-Blasco et al. 2014). In addition, the relationship between satisfaction and WOM can be represented in the form of an inverted “U,” such that the most satisfied and dissatisfied consumers will provide the most comments on their experiences (Litvin et al. 2008). According to these results, we consider that satisfaction will have a positive impact on WOM (Fig. 1), and we posit the last hypothesis: H 6 —Satisfaction in retail experience has a positive impact on WOM.

Methodology

The empirical research was developed in the context of shopping experiences at grocery, clothing, furniture, and electronic product stores. Information was collected using a quantitative research method based on a structured questionnaire. The survey was developed with a set of scales carefully selected, tested from the most recent literature, and adapted to the retail context. A pilot test was carried out and some improvements were made in the wording of the items. A 7-point Likert-type scale was used to measure all the variables.

The marketing innovation scale (three items) is adapted from Homburg et al. (2002), which represents one of the few attempts to develop a measure of innovation in the retailing sphere. The technological innovation scale (four items) was taken from Wu et al. (2006). It is a scale which measures consumer perception of retailers’ use and development of ICTs. The image scale is made up of an atmosphere indicator and four convenience items (Chowdhury et al. 1998). To measure consumer value (four items), we adopt the economic focus (Sullivan et al. 2012) using the measure of value proposed by Sweeney and Soutar (2001). With regard to store brand equity scale (four items), some authors argue that this construct could be evaluated from purchase intention or the preference towards a specific store in comparison with a fictional store (Hartman and Spiro 2005; Yoo et al. 2000), using global brand equity measures adapted from product context. Following this approach, a scale from Yoo and Donthu (2001) is adapted to our research context. The satisfaction scale (five items) reflects the cognitive component (Nesset et al. 2011) and the affective component (Gelbrich 2011) based on Oliver (1997). Finally, WOM behaviour (six items) was measured according to Gelbrich’s (2011) proposal that differentiates WOM referral (Harrison-Walker 2001) and WOM activity (Swan and Oliver 1989).

The interviews were distributed on the basis of a series of representative shop formats in a Spanish city and its metropolitan area, taking into account the type of products offered and their positioning on the European and Spanish market (Interbrand 2014).Footnote 2 In the grocery sector, the interviews were conducted in Mercadona, Carrefour, Alcampo, Lidl, and Día. In the clothing sector, they were conducted in Zara, Mango, and H&M; in home furnishings in IKEA and El Corte Inglés, Hogar; and finally, in electronics, in Fnac, Media Markt, and Apple Store. Personal ad hoc questionnaires were used. Shoppers were intercepted on interviewer judgement as they left the establishments from Monday to Saturday mornings and evenings. A total of 820 valid questionnaires were collected. 36.6 % of individuals evaluated shopping experiences in grocery stores, 22 % in clothing stores, 22 % in electronic good stores, and 19.4 % in furniture stores. The sample has an average age of 41.4 years and in general most subjects are women (64.3 %) and are working (54.6 %).

Dimensionality and Reliability of Measurement Scales

The preliminary study on scale dimensionality was conducted through exploratory factor analysis using maximum likelihood estimation method and calculation of Cronbach’s alpha as reliability index. In terms of scale refinement, three items were eliminated because they considerably increased the alpha reliability indicator (one item from technological innovation scale, one item from store image scale, and one item from WOM activity). All the scales were one-dimensional except WOM scales that extracted two dimensions: WOM referral and WOM activity. Exploratory dimensionality was confirmed with a two-order measurement model estimation using robust maximum likelihood. The results show the multidimensionality of the WOM scale. Taking the significance of the Chi2 Sat−B statistic, the global fit indexes show that the variables converged towards the dimensions established. Internal consistency of the dimensions was evaluated considering two indicators: the composed reliability coefficient was greater than 0.7 and the average variance extracted was over 0.5 (Table 1).

Scale construct validity was analysed for the factors: (1) convergent validity was confirmed for one-dimensional scales as all the variables had significant and high standardised loadings (>0.6 and t-value > 2.58) (Steenkamp and Van Trijp 1991), and it was also confirmed for the multidimensional WOM because the covariances between the two dimensions—WOM referral and WOM activity—were significant at 0.01 and their loadings were significant when analysing a second-order measurement model (Anderson and Gerbing 1988); (2) discriminant validity was checked by linear correlation between each pair of dimensions. These values were less than the square root of the AVE in the scales (Table 1). This validity was analysed in depth with the Chi2 difference test between estimation of the model restricting the correlations between each pair of constructs to the unit and the unrestricted model following the indications in Anderson and Gerbing (1988). The statistical value Chi2 = 354.39 (df = 21) was significant at 99 % (p-value = 0.000).

Results

After studying the reliability and the dimensionality of the measurement scales, we proceeded to estimate the structural equation model in order to verify the hypotheses (Fig. 2). The fit indexes for the causal model, except the contrast associated to the robust Chi2 Sat−Bt = 1277.26 (df = 337), are adequate (RMSEA = 0.060; CFI = 0.944; GFI = 872: AGFI = 0.846; BB-NFI = 0.926; BB-NNFI = 0.938).

Structural model of the causal relationships

With regard to the estimated coefficients of causal relationships, the results show the significant effects of the marketing and technological innovation in retail experience on store image (γ 13 = 0.192** and γ 23 = 0.282**). However, technological innovation has a significant and positive impact on consumer value (γ 24 = 0.104**) and on satisfaction (γ 26 = 0.192**), but marketing innovation does not show these effects. Therefore technological innovation influences on store image, consumer value, and satisfaction, whereas marketing innovation only impacts on store image. These results lead to acceptance of the hypotheses H1a and the second group of hypotheses H2a, H2b and H2c. Consumer value significantly increases store brand equity (β 45 = 0.420**) and H4 is verified. The satisfaction construct, in addition to significant dependency on technological innovation, also depends on store image (β 36 = 0.432**) and store brand equity (β 56 = 0.457**), verifying hypotheses H3 and H5. Finally, WOM behaviour (evaluated from WOM referral and WOM activity dimensions) has a positive and significant dependency on satisfaction (β 67 = 0.788**). That is, most of the recommendations made by customers are due to their level of satisfaction. This result allows us to confirm the last hypothesis, H6.

Conclusions and Further Research

The main aim of our work has been to go deeper into the study of retail innovation, both in marketing and technologies, and its direct and indirect effects on satisfaction and subsequent recommendation through store image, consumer value, and store brand equity. It is a new line of study, which is still fragmented and with little empirical evidence (e.g., Musso 2010; Djellal et al. 2013). Given this gap, our work presents, after a theoretical review of the variables, an empirical model which was tested on a sample of 820 consumers in different types of stores.

The results of this empirical work allow us to conclude that both technological innovation and marketing innovation enable improvements in consumer-perceived store image. The introduction of technologies also improves consumer value and customer satisfaction with the store. However, whereas marketing innovation does influence store image, its effect on consumer value and satisfaction is not significant. Therefore, in our case, customers perceive marketing innovation less significant than technological innovation. This difference may be partly explained by the difficulty in identifying marketing innovation with results that consumers can perceive because they may have more to do with the internal management of the commercial establishment. That is, marketing innovation refers to improvements in services and merchandising offered by the store. However, these improvements, which are easy to link to store image, are more difficult to relate to product prices (in the form of economic value) or to satisfaction with the purchase. Marketing innovation does have a significant indirect effect on satisfaction through store image. Thus, marketing innovation helps to improve store image and the said improvement increases customer satisfaction. The “consumer value store and brand equity satisfaction” chain has also been confirmed as the relationships between these variables are significant. The increase in consumer value improves customers’ perception of the brand, and the better this perception, the more satisfied the customer. Finally, our results confirm the final relationship between satisfaction and WOM behaviour, so that the more satisfied the customer with the retail experience, the more recommendations he or she will make.

These results enable us to make a series of recommendations for the management of retail firms. Firstly, firms should invest in innovation. Innovation is mainly linked to the industrial sector, but our work shows that innovation in the services sector can also improve firm competitiveness. In particular, it is especially important to invest in ICTs, because their results are more easily identifiable by consumers. Marketing innovation, understood as improvements in services and merchandising, can also offer competitive advantages, associated in particular with improved store image and consequently greater satisfaction and more recommendations. Firms should also focus their efforts on making customers aware of the improvements in marketing that have been introduced and how they affect their shopping experience, for example, by lowering prices, making shopping easier, reducing effort, and so on.

Finally, we propose a series of improvements for future studies. Firstly, the marketing innovation scale is too general, and a future analysis should use a scale that reflects different dimensions of this construct. For example, following Musso (2010), a differentiation could be made between innovation in technologies and in customer relations and structural or strategic innovations. Contemplating different types of innovation could shed light on possible reasons for the absence of marketing innovation impact on image and satisfaction. On the other hand, in future works new relationships can be analysed like the effect of marketing innovation on private label or on new product offering. Finally, given that this research was conducted in a geographical area, we propose extending the study to other provinces so the results can be generalised to the Spanish market. The study could also be replicated to other service contexts where marketing innovation is acquiring an important role in business strategy and in cross-channel retailing (physical vs. online channel).

Notes

- 1.

A wide variety of terms are used such as “customer-based store equity”, “retailer equity” or “store value”.

- 2.

References

Aaker, D. A. (1991). Managing brand equity. New York: The Free Press.

Anderson, J. C., & Gerbing, D. W. (1988). Structural equation modeling in practice: A review and recommended two-step approach. Psychological Bulletin, 103(3), 411–423.

Bloemer, J., & De Ruyter, K. (1998). On the relationship between store image, store satisfaction, and store loyalty. European Journal of Marketing, 32, 499–513.

Chowdhury, J., Reardon, J., & Srivastava, R. (1998). Alternative modes of measuring store image: An empirical assessment of structured versus unstructured measures. Journal of Marketing Theory and Practice, 6, 72–86.

Djellal, F., Gallouj, F., & Miles, I. (2013). Two decades of research on innovation in services: Which place for public services? Structural Change and Economic Dynamics, 27, 98–117.

Fuentes-Blasco, M., Moliner-Velázquez, B., & Gil-Saura, I. (2014). Effect of customer heterogeneity on the relationship satisfaction-loyalty. Revista Española de Investigación de Marketing ESIC, 18, 78–92.

Gallarza, M. G., Gil, I., & Holbrook, M. B. (2011). The value of value: Further excursions on the meaning and role of customer value. Journal of Consumer Behaviour, 10(4), 179–191.

Gelbrich, K. (2011). I have paid less than you! The emotional and behavioral consequences of advantaged price inequality. Journal of Retailing, 87(2), 207–224.

Giese, J. L., & Cote, J. A. (2000). Defining customer satisfaction. Academy of Marketing Science Review, 1, 1–34.

Gil, I., Ruiz, M. E., Michel, G., & Corraliza, A. (2013). Retail brand equity: A model based on its dimensions and effects. International Review of Retail, Distribution and Consumer Research, 23(2), 111–136.

Gil, I., Ruiz, M. E., & Berenguer, G. 2014. Retail innovativeness: Importance of ICT and impact on consumer behaviour. In F. Musso & E. Druica (Eds.), Handbook of research on retailer-consumer relationship development (pp. 384–403). IGI Global. Hershey, PA, USA.

Grewal, D., & Levy, M. (2007). Retailing research: Past, present and future. Journal of Retailing, 83(4), 447–464.

Halstead, D. (2002). Negative word of mouth: Substitute for or supplement to consumer complaints? Journal of Consumer Satisfaction, Dissatisfaction and Complaining Behavior, 15(1), 1–12.

Harrison-Walker, L. J. (2001). The measurement of word-of-mouth communication and an investigation of service quality and customer commitment as potential antecedents. Journal of Service Research, 4(1), 60–75.

Hartman, K. B., & Spiro, R. S. (2005). Recapturing store image in consumer-based store equity: A construct conceptualization. Journal of Business Research, 58, 1112–1120.

Holbrook, M. B. (1999). Consumer value. A framework for analysis and research. London: Routledge.

Homburg, C., Hoyer, W. D., & Fassnacht, M. (2002). Service orientation of a retailer’s business strategy: Dimensions, antecedents, and performance outcomes. Journal of Marketing, 66(4), 86–101.

Hristov, L., & Reynolds, J. (2015). Perceptions and practices of innovation in retailing. International Journal of Retail & Distribution Management, 43(2), 126–147.

Jinfeng, W., & Zhilong, T. (2009). The impact of selected store image dimensions on retailer equity: Evidence from 10 Chinese hypermarkets. Journal of Retailing and Consumer Services, 16, 486–494.

Kumar, A., Gupta, S. L., & Kishore, N. (2014). Measuring retailer store image: A scale development study. International Journal of Business and Economics, 13(1), 25–38.

Litvin, S. W., Goldsmith, R. E., & Pan, B. (2008). Electronic word-of-mouth in hospitality and tourism management. Tourism Management, 29(3), 458–468.

Lovelock, C., & Wirtz, J. (2007). Services marketing: People, technology, strategy (6th ed.). Upper Saddle River: Prentice Hall.

Martineau, P. (1958). The personality of the retail store. Harvard Business Review, 36(1), 47–55.

Mazzarol, T., Sweeney, J. C., & Soutar, G. N. (2007). Conceptualizing word-of-mouth activity, triggers and conditions: An exploratory study. European Journal of Marketing, 41(11/12), 1475–1494.

Musso, F. (2010). Innovation in marketing channels. SYMPHONYA Emerging Issues in Management, 1, 23–41.

Nesset, E., Nervik, B., & Helgesen, O. (2011). Satisfaction and image as mediators of store loyalty drivers in grocery retailing. International Review of Retail, Distribution and Consumer Research, 21(3), 267–292.

Oliver, R. L. (1997). Satisfaction. A behavioural perspective on the consumer. London: McGraw Hill.

ONTSI. (2015). Análisis sectorial de la implantación de las TIC en la PYME española. Madrid: Ministerio de Industria, Turismo y Comercio. Retrieved October 19, 2015, from http://www.ontsi.red.es/ontsi/sites/default/files/informe_epyme14_analisis_sectorial_de_implantacion_de_las_tic_en_la_pyme_espanola_0.pdf.

Pappu, R., & Quester, P. (2006). A consumer-based method for retailer equity measurement: Results of an empirical study. Journal of Retailing and Consumer Services, 13, 317–329.

Renko, S., & Druzijanic, M. (2014). Perceived usefulness of innovative technology in retailing: Consumers' and retailers' point of view. Journal of Retailing and Consumer Services, 21(5), 836–843.

Richardson, P. S., Dick, A. S., & Jain, A. K. (1994). Extrinsic and intrinsic cue effects on perceptions of store brand quality. Journal of Marketing, 58, 28–36.

Sekhon, H. S., Al-Eisawi, D., Roy, S. K., & Pritchard, A. (2015). Service excellence in UK retail banking: customers’ perspectives of the important antecedents. International Journal of Bank Marketing, 33(7), 904–921.

Steenkamp, J. B. E., & Van Trijp, H. C. (1991). The use of LISREL in validating marketing constructs. International Journal of Research in Marketing, 8(4), 283–299.

Sullivan, P., Kang, J., & Heitmeyer, J. (2012). Fashion involvement and experiential value: Gen Y retail apparel patronage. The International Review of Retail, Distribution and Consumer Research, 22(5), 459–483.

Swan, J. E., & Oliver, R. L. (1989). Postpurchase communications by consumers. Journal of Retailing, 65(4), 516–533.

Sweeney, J. C., & Soutar, G. N. (2001). Consumer perceived value: The development of a multiple item scale. Journal of Retailing, 77, 203–220.

Teas, R. K., & Agarwal, S. (2000). The effects of extrinsic product cues on consumers’ perceptions of quality, sacrifice, and value. Journal of the Academy of Marketing Science, 28(2), 278–290.

Thomas, S. (2013). Linking customer loyalty to customer satisfaction and store image: A structural model for retail stores. Decision, 40(1–2), 15–25.

Weerawardena, J., O’Cass, A., & Julian, C. (2006). Does industry matter? Examining the role of industry structure and organizational learning in innovation and brand performance. Journal of Business Research, 59(1), 37–45.

Westbrook, R. A. (1987). Product/consumption-based affective responses and postpurchase processes. Journal of Marketing Research, 24(3), 258–270.

White, R. C., Joseph-Mathews, S., & Voorhees, C. M. (2013). The effects of service on multichannel retailers’ brand equity. Journal of Services Marketing, 27(4), 259–270.

Wu, F., Yeniyurt, S., Kim, D., & Cavusgil, S. T. (2006). The impact of information technology on supply chain capabilities and firm performance: A resource-based view. Industrial Marketing Management, 35(4), 493–504.

Yeh, H. (2015). Effects of ICT’s innovative applications on brand image and customer’s purchase intention. The International Journal of Organizational Innovation, 7(4), 31–47.

Yoo, B., & Donthu, N. (2001). Developing and validating a multidimensional consumer-based brand equity scale. Journal of Business Research, 52, 1–14.

Yoo, B., Donthu, N., & Lee, S. (2000). An examination of selected marketing mix elements and brand equity. Journal of the Academy of Marketing Science, 28(2), 195–211.

Yoon, S., Oh, S., Song, S., Kim, K. K., & Kime, Y. (2014). Higher quality or lower price? How value-increasing promotions affect retailer reputation via perceived value. Journal of Business Research, 67, 2088–2096.

Zeithaml, V. A. (1988). Consumer perceptions of price, quality, and value: A means-end model and synthesis of evidence. Journal of Marketing, 52, 2–22.

Acknowledgment

The authors greatly acknowledge the financial support of the Spanish Ministry of Economy and Competitiveness (ECO2013-43353-R) for this research.

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2017 Academy of Marketing Science

About this paper

Cite this paper

Fuentes-Blasco, M., Moliner-Velázquez, B., Servera-Francés, D., Gil-Saura, I. (2017). Role of Marketing and Technological Innovation on Satisfaction and Word of Mouth in Retailing. In: Rossi, P. (eds) Marketing at the Confluence between Entertainment and Analytics. Developments in Marketing Science: Proceedings of the Academy of Marketing Science. Springer, Cham. https://doi.org/10.1007/978-3-319-47331-4_79

Download citation

DOI: https://doi.org/10.1007/978-3-319-47331-4_79

Published:

Publisher Name: Springer, Cham

Print ISBN: 978-3-319-47330-7

Online ISBN: 978-3-319-47331-4

eBook Packages: Business and ManagementBusiness and Management (R0)