Abstract

Climate change, growing urbanization, and technological developments like digitalization and electrification (“diglectrification”) change societal requirements and customer preferences toward motility and mobility in the future, especially automotive mobility. The international automotive industry is under pressure because of these tectonic shifts. There is a strong societal and political push caused by the climate change issue and the strategies as well as measures mitigating the climate change.

Traditional OEMs are in a sandwich position between societal requirements and customer needs. Therefore “low-emission and zero-emission vehicles,” “connected car,” and “autonomous driving” have been on the agenda of the automotive industry since several years. The drivers of these trends are partly newcomers in the automotive industry, like Tesla Motors, Google, or Apple. The growing role of disruptive innovations is in the focus of politics, business, and academia.

The leading idea of this paper is to design a conceptual framework, whereby open and discrete innovation approaches as well as cost of ownership approaches as key elements are applied to strategies and measures for “diglectrical” disruptive innovations in the automotive industry.

Access provided by CONRICYT-eBooks. Download chapter PDF

Similar content being viewed by others

Keywords

- Diglectrification

- Game changer

- Discrete innovation approach

- Emotionalization

- Connected car

- Autonomous driving

1 Introduction

Climate change, growing urbanization, and technological developments like digitalization and electrification (“diglectrification ”) change societal requirements and customer preferences toward motility and mobility in the future, especially automotive mobility. The international automotive industry is under pressure because of these tectonic shifts. There is a strong societal and political push caused by the climate change issue and the strategies as well as measures mitigating the climate change. Bellmann and Khare (2008) give an overview of the CO2 reduction programs. Further on, they recommend an integrated approach including regulations, a changing customer behavior, and a new business development by OEMs to bid farewell from individual mobility as prerequisite of sustainable mobility. The IPCC (2007) favors a modal shift toward public mobility and motility. According to a Continental study (2015), 83 % of the interviewees in Germany and 94 % in the USA drive their own cars, underlining the high preferences toward individual mobility. In contrast, Winterhoff (2015b) forecasts a smaller interest of younger generation in owning a car switching to shared mobility solutions.

Traditional OEMs are in a sandwich position between societal requirements and customer needs. Therefore “low-emission and zero-emission vehicles ,” “connected car,” and “autonomous driving” have been on the agenda of the automotive industry since several years. The drivers of these trends are partly newcomers in the automotive industry, like Tesla Motors, Google, or Apple. The growing role of disruptive innovations is in the focus of politics, business, and academia.

The leading idea of this paper is to design a conceptual framework, whereby open and discrete innovation approaches as well as cost of ownership approaches as key elements are applied to strategies and measures for “diglectrical” disruptive innovations in the automotive industry.

2 Basics of Electrical and Digital Disruptive Innovations in the Automotive Industry

2.1 Disruptive Innovations

“Disruption” as a synonym for discontinuity and breakthrough (Dobbs, Manyika, & Woetzel, 2015, pp. 8, 35), “disruptive technological innovation ” (Christensen, 1997, p. xvi), “disruptive technologies” (Köhler & Wollschläger, 2014, p. 252), and “digital disruption ” (McQuivey, 2013, p. 9) are common terms to describe the transformation of market or industry and service sector by basic (transformational) innovations (Foster & Kaplan, 2001).

Dobbs et al. (2015) identify four disruptions which develop simultaneously and empower the effects to change “long-established patterns in virtually every market and every sector of the world economy—indeed, in every aspect of our lives” (Dobbs et al., 2015, p. 8). These disruptive forces are the urbanization; the responding to the challenges of an aging world; the greater global connections of trade, finance, people, and data; and the accelerating technological change (Dobbs et al., 2015).

These effects have also a huge impact on the automotive business and industry. The core technological trends, “electrification” and “digitalization,” in the automotive industry are in the focus of this paper. They have an increasing disruptive impact on the traditional industry sector (Roland Berger, 2015; Continental, 2015), because they can dissolve the discrepancy between societal requirements and customer preferences for sustainable mobility. But societal and customer requirements are still not congruent, which up to now is observable in the low attractiveness and demand of electric cars (EAFO, 2016).

2.2 Disruptive Electrical Innovations : Trends of Electrification in the Automotive Industry

In 1881 William Ayrton (1847–1908) and John Perry (1850–1920) invented in England the first roadworthy electric vehicle (tricycle) (Seiler, 2011), 5 years before Carl Benz (1844–1929), the vehicle with combustion engine. Over several decades there was a severe concept competition between vehicles with electric drive, combustion engine, as well as hybrid drive, invented in 1900 by Ferdinand Porsche (1875–1951) in cooperation with Ludwig Lohner (1858–1925) (Parr, 2001).

German Emperor Wilhelm II (1859–1941) stated during this contest that “the automobile is just a temporary phenomenon. I believe in the horse” (Wimmer, Schneider, & Blum, 2010, p. 231). Nevertheless, the combustion engine was the winner of this contest over 100 years, and the German automotive industry has won a strong reputation and a core competence with its combustion engine engineering.A turning point seems to be the Volkswagen scandal concerning the worldwide manipulation of more than 11 million vehicles with diesel engines, which finally was uncovered in September 2015 (Smith & Parloff, 2016). Rupert Stadler, CEO of Audi—a subsidiary of Volkswagen Group—stated in April 2016 (Freitag, 2016) that Audi would stop the new development of combustion engines in 2025. The revival of the zero-emission electric drive is observable, supporting strategies and measures mitigating climate change as societal goal. This trend is boosted by start-up OEM Tesla Motors, producer of battery electric vehicles (BEV ) , “a powerful statement of American startup ingenuity” (Consumer Reports, 2015, p. 3), and second in the US market of luxury vehicles in the first half of 2015 (Gerster, 2015).

What Is Electrification?

Electrification in the automotive industry is defined as the provision of infrastructure with grid and storage to guarantee the electric power supply inside and outside the vehicle .

The core trends of vehicle electrification focus on the electric drive and the driver assistance systems. Core topics are the electric drive by battery and by fuel cell. The battery concept is still realized by several automotive companies in the volume as well as in the premium sector. The battery concepts are already in serial development and production, e.g., Tesla Model S, Toyota Prius Hybrid, and the Porsche Panamera S Hybrid. Different grades of electrification of the power train by battery are possible (see Table 9.1).

Tesla Motors is a pioneer and the game changer in the industrial sector. Tesla Motors also vertically integrates the installation of destination chargers and battery charging stations in key markets like the USA and Germany. For example, in Manhattan, a borough of New York City, Tesla Motors owns 100 battery charging stations and there are still 40 classical gas stations left (Vetter, 2016).

In contrast, the fuel-cell concept is still in the pre-serial development phase, despite the Hyundai ix35 Fuel Cell and the Toyota Mirai presented at the International Motor Show 2015 in Frankfurt (Eck & Weigel, 2015). The expansion of the fuel-cell concepts also heavily depends on the very expensive hydrogen distribution infrastructure, which does still not exist in the industrial countries (Schatzmann, 2015).

The two electric drive concepts have different strengths and weaknesses concerning costs, range, performance, and availability, but the battery drive now is in the lead of market acceptance (Evannex, 2016). The focus of this paper is therefore on the battery electric vehicles.

Driving assistance systems in the automotive industry start with the introduction of the speed control system, invented in 1948 by R. R. Teetor (1950). These are additional devices and items to assist the driver in conducting the vehicle during specific driving situations, e.g., acceleration and braking of the vehicle. These systems belong to the car IT. Over the decades more and more (electrical) driving assistance systems have enlarged the product program of the automotive industry, which range , e.g., from the traditional speed control system to anti block system (ABS), electronic stability program (ESP) , adaptive cruise control (ACC), and tire-pressure monitoring system (TPMS) (Schöne, 2013). Some of these systems already work semiautonomous and are a prerequisite to the development of a digital car. Driving assistance systems are a focus of first-tier suppliers like Bosch, Delphi Automotive, and Continental.

2.3 Disruptive Digital Technologies: Trends of Digitalization in the Automotive Industry

McQuivey (2013) focuses on the digitalization and its impact on disruption, where often low financial and intellectual input generates high leverages of financial output and global access to customers. The rising relevance of the digitalization is strongly connected with the development of the information and communication technologies (ICT ). The driving assistance systems and the communication systems are prerequisites for the digitalization of the vehicles.

What Is Digitalization?

Digitalization in the automotive industry is defined as the transfer of analog data into a digital form with support by ICT inside and outside of a vehicle .

The forerunner industry was the photographic film industry, which disruptively changes the business models of traditional silver halide photographic film producers like the Eastman Kodak Company (Christensen, 1997).

Digitalization in the automotive industry has the following three core topics (Köhler & Wollschläger, 2014) (see Fig. 9.1):

Core topics of digitalization in the automotive industry (Köhler & Wollschläger, 2014)

-

1.

Connected car

-

2.

Internet of things

-

3.

Autonomous driving

Big data and analytics as well as cloud computing are considered a supportive issue in contrast to Köhler and Wollschläger (2014). Winterhoff (2015a) identifies automation, digital data, connectivity, and digital customer interface as determinants of digitalization.

2.3.1 Connected Car

Connected car (see Fig. 9.2) is about the interconnectedness of vehicles with the environment (Car-to-X Communication (C2X)) (Schöne, 2013), specifically with:

-

Other vehicles (Car-to-Car Communication (C2C))

-

Traffic infrastructure and other components of infrastructure (Car-to-Infrastructure Communication (C2I))

The interconnectedness of vehicles with other infrastructure components enables OEMs to use diagnosis tools for after-sales and maintenance services “by air” and to upgrade product items “by air” (Kieler, 2015) according to the pay-as-you-upgrade principle.

A study by Continental (2015) underlines that the acceptance of connected car-based services in Germany ranks the improvement of traffic management before the integration of black boxes documenting driving data followed by the service and maintenance based on vehicle data. In the USA the service and maintenance based on vehicle data ranks before the integration of black boxes and the improvement of traffic management .

2.3.2 Internet of Things

The electronic interconnectedness of things (Internet of things ) is an integral part of the upcoming sharing economy combined with the approaches of “smart city” and “smart home” (Köhler & Wollschläger, 2014) (see Fig. 9.3). According to the pay-as-you-drive principle, car owners can rent their car to others including a separated insurance service, which typically in average “remains unused for 23 of the 24 hours in a day” (Winterhoff, 2015b, p. 14). The application of the pay-as-you-use principle is suited for renting the own garage or the parking space management in conurbations, for example. But in the USA and Germany, only 1 % of the interviewed persons use car-sharing services (Continental, 2015). It is just a small niche business with low expectations of profitability (Köhler & Wollschläger, 2014; Freitag, 2016).

Internet of things

2.3.3 Autonomous Driving

Autonomous driving means driving a vehicle without interference of a person who is compulsory inside the vehicle on the driver’s seat. In contrast, there is the motion of drones and robots with exclusively external central control. A pioneer of autonomous driving is Ernst Dickmanns, former professor at the University of the Federal Armed Forces in Munich. He started in the 1980s in cooperation with Daimler-Benz AG with highly and fully automated driving tests based on Mercedes vans and S-Class vehicles (Vieweg, 2015; Dickmanns, 1998). There are five development steps to autonomous and driverless driving (CEDR, 2014):

-

Level 0: driving without any driving assistance system (not automated)

-

Level 1: driving with driving assistance systems, e.g., speed control

-

Level 2: partially automated driving, e.g., park distance control system

-

Level 3: highly automated driving, e.g., autopilot driving

-

Level 4: fully automated driving with possible interference by a driver

-

Level 5: driverless driving, which is not autonomous, but robot driving

The Continental study (2015) reveals that customers appreciate the relief of discomfort and stress by monotonous and stress-causing driving situations. These are rational buying arguments, which underline the rational characteristics of autonomous driving. Other arguments focus on safety and comfort characteristics, which are also of rational nature. But around a half of the interviewed persons in Germany and the USA doubts about the reliability of autonomous driving. Another pitfall is the cyber security issue of autonomous vehicles .

Big data and analytics as well as cloud computing are supportive elements of digitalization. The extraction of a huge amount of data and the application of data mining should lead to new knowledge about customer behavior, preferences, and needs. Volume, velocity, and the variety of data are important characteristics of big data. Winterhoff (2015a) places big data and analytics to the category of digital data together with customer relationship management (CRM) and new business models as results of insights about customer needs. Big data and the insights of its analytics are also a prerequisite of the digital customer interface, which fuels multichannel activities, marketing and sales, and new mobility services with customer-related information (Winterhoff, 2015a).

Cloud computing covers Internet-based services for (Köhler & Wollschläger, 2014):

-

Provision of computer capacities

-

Services

-

Memory capacities

Cloud computing is supportive for the other topics of digitalization and a prerequisite for the expansion of them. A pioneer of cloud computing is Salesforce (2016) specializing in “software as service,” “platform as service,” and CRM .

According to the studies of Winterhoff (2015a) and Continental (2015), customers identify the autonomous driving and the interconnectedness most interesting.

2.4 Profile of Requirements of Societal- and Customer-Focused Strategies and Measures for Electrification and Digitalization in the Automotive Industry

The trends of electrification and digitalization are technology-driven developments (technology-push) by companies from the ICT as well as automotive industry. These trends will cause tectonic shifts in the automotive industry by new competitors. They have an immense impact on the business models of the traditional automotive industry, especially OEMs, including their customer bases, customer needs, as well as political and societal impacts in the coming years.

2.4.1 Customer Requirements

On the customer side, it is interesting to anticipate the shifts in customer needs. A study of Arthur D. Little (ADL, 2009), a consulting firm, about mobility in 2020 identifies different customer types of mobility in triad markets (three developed markets of Japan, North America, and Europe) (Wittmann, 2013, pp. 118–119):

-

Greenovator (27 %) reflects/internalizes socio-ecological impacts on mobility and demands for innovative and sustainable mobility solutions.

-

Family cruiser (11 %) counts for growing demand for mobility in a rising fragmented personal environment (family, friends, peers, colleagues).

-

Silver driver (24 %) starts proactive, motivated in the third phase of life. He is experienced in mobility products and favours high quality consciousness/product awareness.

-

High-frequency commuter (24 %) is coined by high everyday mobility distances/frequencies and is focussed on mega-cities in the future.

-

Global jet setter (2 %) is dependent on global mobility needs because of his job requirements/demands and counts on exclusive premium mobility services/support.

-

Sensation seeker (4 %) considers mobility as a symbol of (personal) freedom, fun and life-style, status and prestige.

-

Low-end mobility user/consumer (8 %) has rigid mobility budgets, a need of affordable mobility solutions. He is ready to downgrade his mobility demand .

In BRIC (Brazil, Russia, India, China) markets other customer types of mobility are representative. These are basic, smart basic and premium customers:

-

Basic customer (48 %) demands basic mobility and needs simple and cheap mobility solutions. He focuses on local products.

-

Basic smart customer (43 %) prefers affordable mid class products, which he can individualize on his needs and requirements.

-

Premium customer (4 %) is focussed on status, reputation, prestige and comfort and intends to differentiate as a societal winner and to be considered as a successful person.

It is necessary to mirror the customer types of mobility with financial restrictions, which occur in buying decisions of products and services related to mobility. The price sensitivity and the preferences for mobility are important aspects for further analyses. The different segments of triad and BRIC markets count the following share in total (ADL, 2009) (see Table 9.2).

The customers of mobility recognize the relevance toward electric drive according to their preferences (see Table 9.3).

The trends of digitalization have different levels of relevance for the customers of mobility (see Table 9.4).

In Germany around 30 % of the purchased cars in 2015 belong to the premium segment (KBA, 2015, own calculation), which as an example can cover the customer groups: Greenovator (50 %), Silver Driver (50 %), Global Jet Setter, and Sensation Seeker. They have low price sensitivity; a focus on sustainable, individual mobility; and significant acceptance toward digital trends. These are important customer characteristics and requirements of customer-focused strategies and measures for electrification and digitalization in the automotive industry .

2.4.2 Societal and Political Requirements

Governmental initiatives like the National Platform for Electric Mobility (NPE) in Germany focus on research accelerating the development and mass introduction of electric vehicles (NPE, 2010). In parallel to governmental initiatives, like the NPE, many Western countries support the purchase of electric vehicles with financial and other incentives.

Norway is a leading example to successfully adjust to electro-mobility with incentives (Schwan, 2015). Fifty thousand electric vehicles already exist in Norway with a population of 5.2 million people. Twenty percent of newly purchased vehicles are electric vehicles. Very helpful are incentives granted by the Norwegian state, which are exemptions of vehicle and value-added taxes. Additionally, the use of toll roads, bridges, and tunnels as well as of ferries often is free of charge for electric vehicles in Norway. Critics demand to waive the incentives for premium cars like the Tesla S in Norway. According to a study of the University of Oslo (Figenbaum & Kolbenstvedt, 2015), 62 % of the electric vehicles are in the ownership of multi-vehicle households, 18 % in the ownership of single-vehicle households, and 20 % in the ownership of fleets. The sociodemographic composition of electric and conventional car owners is nearly congruent in Norway. The customer satisfaction is very high; 91 % of 7,500 interviewees are satisfied or very satisfied with their electric car. The range of the electric vehicles is not a customer problem anymore, because the average daily commuter distance is less than 60 km and within the range of fully loaded electric vehicles. Also 97 % of the electric vehicle owners have access to home charging facilities, which underlines the high relevance of multi-vehicle households and fleets as customer bases for electric vehicles in Norway.

Six other aspects cover further requirements of strategies and measures for electrical and digital disruptive innovations in the automotive industry :

-

In a research study of long-term vehicle in the 1970s, which was initiated by former Porsche CEO Ernst Fuhrmann (1918–1995) (Kortzfleisch, 1980), feasibility analyses underline that long-term vehicles with 20-year technical obsolescence or 300,000 km driving performance have despite the life-cycle enlargement a constant demand in contrast to conventional vehicles (Bellmann, 1990). The reasons why these long-term vehicles were not produced were poor customer acceptance and different buying behaviors. Wittmann (1998) forecasts that the more ecological items are relevant for customers, the more the demand of vehicles with longer model life cycles grows.

-

The goals for a long-term vehicle (Bott & Braess, 1976) are similar to goals for electric cars: preserving energy supplies, reduction of environmental burden, increase of reliability of operation, perpetuation of classical vehicle concepts, reduction of total costs, and preserving raw material supplies. Consequently electric vehicles are convenient for long-term usage.

-

The strong emphasis on environmental issues in the automotive industry traditionally leads to a focus on rational car features (and services) in the automotive planning and development process focusing on small- and midrange vehicles. The premium car segments in the traditional automotive industry represented by emotional items like styling, engine power, driving pleasure, sportiness, and prestige (Wittmann, 1998) do not have a focus on the introduction of electric drive, which is viewed as an environmental, rational item by the regular customers over a long time (Continental, 2015). This is an open flank for new competitors, who combine environmental items with emotional items like excellent design, sportiness, and driving pleasure, in order to charge the electric vehicle with emotions (“emotionalization ”), e.g., Tesla Motors with its Model S (Consumer Reports, 2015).

-

Another development in society on environmental issues postulates new usership concepts of the automotive industry, which concentrate on new mobility services, like car sharing, carpooling, and mobility platforms for modal transport (Canzler & Knie, 1999). This movement grounds on ideas around sustainable economic development concerning prosperity with growth fulfilling important social benefits while improving sustainability (Meadows, Randers, & Meadows, 2004), concerning prosperity without growth and innovation (Jackson, 2011; Paech, 2012), or concerning smart growth (Coble, 2013).

-

The electric drive replaces the combustion engine and its peripheral systems, like exhaust systems, in the vehicle concept. Currently, costs and weight of electric cars often are higher than of conventional cars because of the battery costs and the weight of the batteries. But in the midterm, significant cost and weight reductions are realistic, which rapidly increase the competitiveness of electric cars, especially in the price-sensitive volume segments.

-

Another aspect of electric vehicles is the strong reduction of the amount of wearing parts now just focusing on the battery, the brakes, and the tires. A long-term usage is appropriate in contrast to conventional cars. This has impacts on maintenance and running costs as well as of the resale values of the electric cars. New service, warranty, and maintenance models, based on insights of customer research methods, can compensate the higher technical obsolescence and value losses of first-generation batteries .

The framework takes the relevant aspects into account and summarizes as follows (see Fig. 9.4).

Framework for strategies and measures for “diglectrical” disruptive innovations in the automotive industry

3 Key Elements for Strategies and Measures for “Diglectrical” Disruptive Innovations in the Automotive Industry

3.1 From Open-Innovation Approaches to Discrete Innovation Approaches

The identification of customer requirements and needs for products and services is essential for designing effective strategies and measures for disruptive innovations in the automotive industry. Wittmann (2013) recommends open-innovation approaches to solve the problem of customer integration and participation, which are categorized in an open-innovation matrix based on the criteria “amount of users” and “level of integration”. The digitalization trend of “big data and analytics” enhances research methods of innovation and marketing management. In contrast to open-innovation approaches and traditional market research methods, big data analyses only require customer raw data, e.g., about individual customer behavior, from companies and organizations without direct contact to (potential) customers. Therefore the big data analyses characterize discrete innovation approaches , which enable insights toward new product and service trends and improvements as well as new business models and the identification of new customer needs. The anonymous data deliveries can range, e.g., from periodical deliveries of customer profiling (digital footprints) to real-time technical driving data of vehicles. Stahl (2016) considers big data analyses as new approaches of market research (see Table 9.5).

3.2 Concepts of Cost of Ownership and of Cost of Usership

According to Continental (2015), driving is more a question of budget than of seniority and residence. An essential prerequisite is the financial budget restriction, which influences buying decisions. In this context the concepts of cost of ownership and of cost of usership receive relevance. The concepts of cost of ownership and of usership are able to identify and to evaluate strategies and measures for electrification, digitalization, and new business models in the automotive industry:

In the cost of ownership model an ecological price premium exists when the product bears competitive advantages in ecological features in comparison to a competitor’s product. This premium can be justified by savings on fuel costs and taxes related to mobility, for example. This is also important for the owner’s view of the life cycle of the product, when significant cost, tax and fee reductions can be realized over time because of the ownership of an ecological vehicle. (Wittmann, 2013, p. 126)

The cost of usership model covers different individual and public services, offered by public and private organizations, like taxi companies, bus and railway companies, car and bike rentals, as well as by new competitors like Uber favoring on mobility on demand services (Wittmann, 2013). Equivalent to the cost of ownership model, competitive advantages like savings on fuel costs (ecological service feature) or ad hoc availability of the service (digital service feature) can justify the price premium .

3.3 Customer-Focused Strategies and Measures for “Diglectrical” Disruptive Innovations in the Automotive Industry

Christensen (1997, pp. 219–220) points out that “the electric vehicle is not only a disruptive innovation, but it involves massive architectural reconfiguration as well, a reconfiguration that must not only occur within the product itself but across the entire value chain.”

Several strategies and measures seem appropriate to guarantee the adequate reconfiguration of the automotive value chain, too. Cost of ownership and of usership concepts exemplify and visualize the financial impacts of a conventional and of an (battery) electric vehicle from a customer and OEM perspective:

-

The top-down introduction of innovations into the product program is a characteristic of premium OEMs (Wittmann, 1998), and it is also an appropriate strategy to diffuse “diglectrical” innovations, especially because of the high costs of electrical batteries. The “emotionalization ” of electric vehicles works easier in a premium vehicle positioning, where emotional items, like prestige, sportiness, and driving pleasure, dominate. The ecological price premium combines environmental aspects (CO2 free mobility) as well as emotional vehicle characteristics like driving pleasure (see Fig. 9.5).

Fig. 9.5

Cost of ownership concept: conventional vs. electric vehicle

-

A strategy of vertical integration can also support an ecological price premium. Tesla Motors, e.g., offers free charging of electric energy for specific Tesla S customers at its own charging stations (see Fig. 9.6).

Fig. 9.6

Cost of ownership concept : conventional vs. electric vehicle—vertical integration of charging stations and free charging

-

A long-term strategy, especially of electric vehicles, underlines reliability and quality, which enables an ecological price premium, too (see Fig. 9.7).

Fig. 9.7

Cost of ownership concept : conventional vs. electric vehicle—long-term effect

-

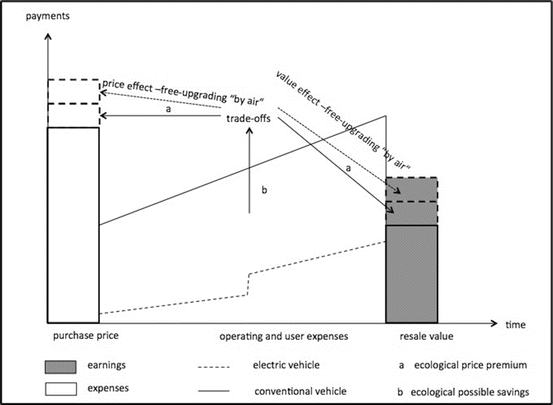

A hybrid strategy of electrification and digitalization (strategy of “diglectrification”) helps in offering a bundling of features and services to upgrade the product over the life cycle. Different pricing strategies are possible, which support an ecological price premium position as well as a higher resale value. Tesla Motors, e.g., upgrades product functions, like autopilot function, “by air” and free of charge (see Fig. 9.8).

Fig. 9.8

Cost of ownership concept : conventional vs. electric vehicle—digital upgrading “by air” and its effects

-

Last not least, mobility service strategies drive an innovative form of individual and sustainable mobility in conurbations. They probably compete with car rentals, taxi companies, and new forms of mobility on demand services, like Uber (see Fig. 9.9). An ecological price premium is arguable, when, e.g., fuel cost savings, ad hoc availability , and electric drive are service characteristics.

Fig. 9.9

Cost of usership model (Wittmann, 2013)

3.4 Societal Strategies and Measures for “Diglectrical” Disruptive Innovations in the Automotive Industry

Strategies and measures mitigating climate change focus on societal goals (NPE, 2010). The development and use of clean technologies rank first of the strategies and measures mitigating climate change (see Table 9.6). It is obvious that the disruptive innovation of electric drive changes the automotive value chain dramatically. It is the only alternative, which guarantees sustainable CO2 free automotive mobility.

The IPCC defines in 2007 key technologies, which are the bases for strategies and measures for the transport sector mitigating climate change as societal goal. The disruptive nature of the electrification in the automotive and transport industry leads to an acceleration of the development (Evannex, 2016; Vetter, 2016), where an update of technology-driven strategies and measures is necessary as follows (see Table 9.7).

The rising success of electric vehicles is only possible, because digital innovations support this development and they significantly enlarge the customer and societal value of electric vehicles, e.g., through upgrading of items “by air” (Consumer Reports, 2015; Vetter, 2016).

3.5 Evaluation of Strategies and Measures: New Perspectives the Automotive Industry?

Electrification and digitalization sustainably influence the business models of traditional OEMs as well as market newcomers. In Fig. 9.10, OEM s face challenges concerning the potential of profitability and the focus on technology or customer. Traditional premium OEMs have to defend their technological leading position, which is challenged by start-up OEMs, like Tesla Motors or Google and Apple, planning autonomous, electric niche cars for conurbations. The start-up OEMs face on the one side commercial problems, like Tesla Motors, because of high investments and low volumes and sales. On the other side, future niche OEMs like Google and Apple, which belong to the ICT sector, lack technological automotive know-how and depend on external automotive support.

Potential of profitability of OEMs and of “diglectrical” measures

Technological and commercial advances in batteries, fuel cells, electric charging, and light weighting push the electric car to higher profitability, which enables the mass introduction of this vehicle type. This supports traditional OEMs in their transformation toward electrification and digitalization. Start-up OEMs get the business opportunity to establish themselves in the highly competitive automotive markets.

4 Conclusion and Outlook

Bellmann and Khare (2008) recommend the farewell from individual mobility as prerequisite for sustainable mobility, probably underestimating the disruptive nature of electrification and digitalization in the automotive industry. But they are not the only ones. Customer behavior seems to change, but not toward public or shared mobility as forms of sustainable mobility postulated by IPCC (2007), too. The technological and market revival of the electric drive makes sustainable individual mobility combined with driving pleasure possible and attractive. The technological trends of digitalization thereby accelerate the customer acceptance of electric vehicles. In the future, the societal goal of mitigating climate change and individual mobility preferred by the customers will not be a discrepancy anymore. There are new perspectives for the automotive industry.

References

ADL. (2009). Zukunft der Mobilität 2020. Arthur D. Little. Available from http://www.adlittle.de/uploads/tx_extthoughtleadership/ADL_Zukunft_der_Mobilitaet_2020_Langfassung.pdf (accessed March 18, 2012).

Bellmann, K. (1990). Langfristige Gebrauchsgüter: ökologische Optimierung der Nutzungsdauer. Wiesbaden: Deutscher Universitäts-Verlag.

Bellmann, K., & Khare, A. (2008). Response of German car manufacturers to the European Union directive on reducing CO2 emissions from passenger cars—Research report. University of Mainz.

Bott, H., & Braess, H. H. (1976). Forschungsprojekt Langzeitauto, Endbericht Phase I—Kurzfassung. Weissach: Bundesministerium für Forschung und Technologie.

Canzler, W., & Knie, A. (1999). Neue Mobilitätskonzepte: Rahmenbedingungen, Chancen und Grenzen, Veröffentlichungsreihe der Querschnittsgruppe Arbeit & Ökologie beim Präsidenten des Wissenschaftszentrum Berlin für Sozialforschung (No. P99–508). Available from http://hdl.handle.net/10419/50312 (accessed March 28, 2016).

Christensen, C. M. (1997). The innovator’s dilemma: When new technologies cause great firms to fail. Boston, MA: Harvard Business Review Press.

Coble, D. (2013). Is smart growth really so smart? In A. Khare & T. Beckman (Eds.), Mitigating climate change (pp. 3–23). Heidelberg: Springer.

Conference of European Directors of Roads (CEDR). (2014). CEDR transnational road research programme: Call 2014 (pp. 1–11). Available from http://www.bast.de/DE/BASt/Forschung/Forschungsfoerderung/Downloads/cedr_call_2014_2.pdf?__blob=publicationFile&v=2 (accessed April 27, 2016).

Consumer Reports. (2015). Tesla Model S P85D breaks consumer reports’ rating system (pp. 1–5). Available from https://consumerist.com/2015/08/27/tesla-model-s-p85d-breaks-consumer-reports-ratings-system (accessed August 28, 2015).

Continental AG. (2015). Continental mobility study 2015. Available from http://www.continental-corporation.com/www/pressportal_com_en/themes/initiatives/channel_mobility_study_en/ov_mobility_study2015_en/ (accessed March 13, 2016).

Continental AG. (2016). Hybrid electric vehicle. Available from http://www.continental-automotive.de/www/automotive_de_de/themes/passenger_cars/powertrain/hybrid_de.html (accessed January 7, 2016).

Dickmanns, E. D. (1998). Vehicles capable of dynamic vision: a new breed of technical beings? Artificial Intelligence, 103, 49–76.

Dobbs, R., Manyika, J., & Woetzel, J. (2015). No ordinary disruption. New York: PublicAffairs.

European Alternative Fuels Observatory (EAFO). (2016). Battery electric vehicle (BEV) overview table—Europe. Available from http://www.eafo.eu/vehicle-statistics/m1 (accessed April 14, 2016).

Eck, P., & Weigel, G. (2015). IAA Spot - Internationale Automobil-Ausstellung 2015. Willmenrod: SPS Spot Press Services.

Evannex. (2016). Tesla rules battery electric vehicles vs. hydrogen fuel cells. Available from http://evannex.com/blogs/news/113215301-tesla-rules-battery-electric-vehicles-vs-hydrogen-fuel-cells-infographic (accessed March 31, 2016).

Figenbaum, E., & Kolbenstvedt, M. (2015). Competitive electric town transport (TØI report 1422/2015). Oslo: Institute of Transport Economics.

Foster, R., & Kaplan, S. (2001). Creative destruction. New York: Doubleday and Random House.

Freitag, M. (2016). Deutschlands Premiumhersteller wollen sich radikal neu erfinden. Wer die Bewegung anführt. Manager Magazin, Issue 4/2016, pp. 48–53.

Gerster, M. (2015). Tesla fordert deutsche Hersteller heraus. Available from http://www.stuttgarter-nachrichten.de/inhalt.elektro-suv-von-audi-tesla-fordert-deutsche-herstellerheraus.1aa21feb-4345-462b-a4c3-a11ed88eb65d.html (accessed August 23, 2016).

Intergovernmental Panel on Climate Change (IPCC). (2007). Working Group III, fourth assessment, summary for policymakers (pp. 1–23).

Jackson, T. (2011). Prosperity without growth. London and Washington, DC: Earthscan.

Kieler, A. (2015). Tesla CEO says summer software update could make the Model S self-driving (pp. 1–3). Available from https://consumerist.com/2015/03/20/tesla-ceo-says-summer-software-update-could-make-the-model-s-self-driving/ (accessed August 28, 2015).

Köhler, T. R., & Wollschläger, D. (2014). Die digitale Transformation des Automobils. Pattensen: Media-Manufaktur.

Kortzfleisch, G. von (1980). Vorwort. In J. Schöttner (Ed.), Ökonomische und soziale Konsequenzen einer Entwicklung zum Langzeitauto (n. p.). München: Verlag V. Florentz.

Kraftfahrt-Bundesamt (KBA). (2015). Top 50 der Modelle im Dezember 2015. Available from http://www.kba.de/DE/Statistik/Fahrzeuge/Neuzulassungen/MonatlicheNeuzulassungen/2015/201512GV1monatlich/201512_n_top50.html?nn=1129994 (accessed March 31, 2016).

McQuivey, J. (2013). Digital disruption. Las Vegas: Forrester Research and Amazon.

Meadows, D. H., Randers, J., & Meadows, D. (2004). Limits to growth. White River Junction, VT: Chelsea Green.

Nationale Plattform Elektromobilität (NPE). (2010). Available from http://nationale-plattform-elektromobilitaet.de/ (accessed March 31, 2016).

Paech, N. (2012). Nachhaltiges Wirtschaften jenseits von Innovationsorientierung und Wachstum. Marburg an der Lahn: Metropolis.

Parr, K. (2001). Porsche, Ferdinand, Neue Deutsche Biographie (No. 20, pp. 638–640). Available from http://www.deutsche-biographie.de/pnd118595881.html (accessed March 30, 2016).

Roland Berger. (2015). Automotive insights 1/2015. Available from http://newsletters.rolandberger.com/public/a_6050_lTJkh/file/data/267_Roland_Berger_Automotive_Insights_01_2015_20151008.pdf (accessed February 23, 2016).

Salesforce. (2016). Products. Available from http://www.salesforce.com/products/ (accessed April 27, 2016).

Schatzmann, M. (2015). Heute mehr Reichweite—übermorgen neue Batterietechnologien. Available from http://www.nzz.ch/mobilitaet/auto-mobil/e-mobilitaet/heute-mehr-reichweite--uebermorgen-neue-batterietechnologien-1.18636886#print (accessed April 14, 2016).

Schöne, R. (2013). Das vernetzte Fahrzeug. Norderstedt: GRIN Verlag.

Schwan, B. (2015). E-Autos auf dem Weg zur Normalität. Technology Review. Available from http://www.heise.de/tr/artikel/E-Autos-auf-dem-Weg-zur-Normalitaet-2632034.html? (accessed June 1, 2015).

Seiler, C. (2011). Erstes Elektroauto der Welt fährt wieder, Press Release, Stiftung Museum Autovision. Available from http://autovision-tradition.de/files/erstes-Elektroauto-der-Welt-Text.pdf (accessed March 30, 2016).

Smith, G., & Parloff, R. (2016). Hoaxwagen. Fortune, Europe Edition, 173(4), 34–48.

Stahl, F. (2016). In Diehl, N. Mit digitalen Fussabdrücken zu neuen Geschäftsmodellen. Forum, Issue 1/2016, p. 40. Available from http://www.uni-mannheim.de/ionas/uni/forum/forschung/Ausgabe%201-2016/Mit%20digitalen%20Fu%C3%9Fabdr%C3%BCcken%20zu%20neuen%20Gesch%C3%A4ftsmodellen/ (accessed April 15, 2016).

Teetor, R. R. (1950). Speed control device for resisting operation of the accelerator. Available from http://pdfpiw.uspto.gov/.piw?Docid=02519859 (accessed March 31, 2016).

Vetter, P. (2016). Mit diesem Trick will Tesla das E-Auto revolutionieren, Die Welt. Available from http://www.welt.de/wirtschaft/article153758875 (accessed March 29, 2016).

Vieweg, C. (2015). Wer hat das Roboterauto erfunden? Die Bundeswehr! Zeit Online. Available from http://www.zeit.de/mobilitaet/2015-07/autonomes-fahren-geschichte (accessed July 31, 2015).

Wimmer, E., Schneider, M. C., & Blum, P. (2010). Antrieb für die Zukunft. Stuttgart: Schäffer-Poeschel.

Winterhoff, M. (2015a). The dawn of the digital car. In Roland Berger (Ed.), Automotive insights 1/2015 (pp. 18–23). Available from http://newsletters.rolandberger.com/public/a_6050_lTJkh/file/data/267_Roland_Berger_Automotive_Insights_01_2015_20151008.pdf (accessed February 23, 2016).

Winterhoff, M. (2015b). U.S. market scenario: owners, drivers and urban traffic of the future. In Roland Berger (Ed.), Automotive insights 1/2015 (pp. 12–15). Available from http://newsletters.rolandberger.com/public/a_6050_lTJkh/file/data/267_Roland_Berger_Automotive_Insights_01_2015_20151008.pdf (accessed February 23, 2016).

Wittmann, J. (1998). Target project budgeting. Wiesbaden: Deutscher Universitätsverlag.

Wittmann, J. (2013). Mobility and mitigating climate change in urban centers. In A. Khare & T. Beckman (Eds.), Mitigating climate change (pp. 111–131). Heidelberg: Springer.

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2017 Springer International Publishing Switzerland

About this chapter

Cite this chapter

Wittmann, J. (2017). Electrification and Digitalization as Disruptive Trends: New Perspectives for the Automotive Industry?. In: Khare, A., Stewart, B., Schatz, R. (eds) Phantom Ex Machina. Springer, Cham. https://doi.org/10.1007/978-3-319-44468-0_9

Download citation

DOI: https://doi.org/10.1007/978-3-319-44468-0_9

Published:

Publisher Name: Springer, Cham

Print ISBN: 978-3-319-44467-3

Online ISBN: 978-3-319-44468-0

eBook Packages: Business and ManagementBusiness and Management (R0)