Abstract

We measure contagion potential and stability of banking system on a randomized version of the credit contagion model by Steinbacher M, Steinbacher M, Steinbacher M (2012) Credit contagion in financial markets: a network-based approach. Available via SSRN. http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2068716. Cited 30 Jan 2013. We introduce two estimators of the contagion potential of banks (liquidity-loss potential and α-criticality index (Steinbacher M, Steinbacher M, Steinbacher M (2012) Credit contagion in financial markets: a network-based approach. Available via SSRN. http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2068716. Cited 30 Jan 2013)) and introduce Shannon’s entropy as a stability estimator. Our approach is systemic in that it enables an overall estimation of the capacity of the banking system to provide liquidity. Mechanism developed can be employed for measuring systemic risk of banking system as a whole.

Access provided by Autonomous University of Puebla. Download chapter PDF

Similar content being viewed by others

Keywords

These keywords were added by machine and not by the authors. This process is experimental and the keywords may be updated as the learning algorithm improves.

1 Introduction

Schweitzer et al. [15] acknowledge that

We need an approach that stresses the systemic complexity […] that can be used to revise and extend established paradigms in economic theory.

It would need a special anthology to acknowledge all the authors that have contributed to the knowledge about dynamics and complexities of current financial system. Specifically, we focus on structural characteristics of banking system and on credit default contagion by the use of artificial network approach in order to build a mechanism for identifying and measuring the stability of the banking system relative to various degrees and types of mutual exposures of banks. The mechanism is tested on credit contagion model [16], who model idiosyncratic and systemic shocks and their propagation through a banking system. The model is based on credit events that spread along the banking system and subsequently influence the behavior of the system; credit events are exogenous to simulator and are spurred either by financial markets, business sector, government, or private individuals for whatever reason.

Banking system is a subsystem of a financial system. The latter resembles a network of interconnected financial and non-financial agents, whose decisions are likely to produce a rich and unprecedented structure; see [1] for a reference. Allen et al. [3] provide an extensive list of references to the research conducted on various aspects of a financial system and credit contagion, focusing basically on particular applications. Allen and Gale [2] further study banking system and its responds to contagion in various network structures based on mutual deposits of banks, which is partly similar to a setup we use.Footnote 1 Eisenberg and Noe [8] for instance develop an algorithm of a natural measure of systemic risk based on waves of defaults needed to induce failure, while Upper and Worms [17] perform a contagion test on German banking system and show that the failure of a single bank could have led to the collapse of up to 15 % of overall banking assets.Footnote 2 Some [1, 12, 15] studies show that banking system is characteristic for a few large banks that are linked with many smaller banks.

2 The Model

The model is taken from [16]. It consists of a finite set of 40 banks; 14 are big banks each having over $900 billion in assets, 17 are medium with more than $100 billion and less than $700 billion in assets, and the rest are small with less than $100 billion in assets. A cumulative initial value of assets in the network is $25,951.16 billion and it is the same for all network topologies used in simulations. Initial capital of all banks from the model is taken as of December 31, 2011 from banks’ annual reports. Mutual exposures of banks as well as their mortgage lending are distributed among banks at random and once determined remain the same in all initial periods of all banking network topologies used.

The banking system is treated as a complex system built by semi-autonomous agents that make decisions on their own behalf and follow certain generally imposed rules. Key assumptions of the model are:

-

1.

Liquidity can either be in passive or active mode;

-

2.

Connections among banks represent liquidity flows;

-

3.

Initial default risk of banks is arbitrary and bank-specific;

-

4.

Liquidity is defined in terms of a monetary unit of value.

-

5.

Banks are not allowed to change their strategies (no autonomous change in portfolios, no autonomous change in lending, no recapitalization, etc.)

-

6.

There is no lender of last resort.

-

7.

Each network exists for T time units.

2.1 Banks

The dynamics of assets of bank i can be viewed as an ordered sequence \(\{a_{i,t}\}_{t=0}^{T}\) that develops in time t as shown by (1).

Here \(a_{i,t},h_{i,t},b_{i,t}\) and n i, t denote values of bank i total assets, mortgage loans, bonds and non-trading assets in time t, while q ij, t denotes its holdings of interbank assets with bank j at the same time. \(\mathcal{E}(i)\) is the subset of all liquidity flows from i to j; the sum operator in (1) goes over all banks j in which i holds a portion of its interbank holdings.

The value of capital of bank i develops according to its profits and losses in time (Table 1). The dynamics can be depicted as

As for the banking network a standard notation from graph theory applies. \(\mathcal{G}\) is a directed random graph that consists of the nodes of the set \(\mathcal{V}\subseteq \mathbb{Z}\) and let \(\mathcal{E}\subseteq {[\mathcal{V}]}^{2}\) include all connections in \(\mathcal{G}\); a connection is a two-element pair \((ij) \in \mathcal{E}\). Connections represent the intensity of flows passing from node i to node \(j: j\neq i\mid \{j,i\} \in \mathcal{V}\) and vice versa (\(i: i\neq j\mid \{i,j\} \in \mathcal{V}\)). Every connection is ascribed a non-negative real number k that is defined by the transformation \(f:{ [\mathcal{V}]}^{2} \rightarrow k \in \{{\mathfrak{R}}^{+} \wedge 0\}\). In our case k is expressed in monetary units and represents interbank liquidity. An overall liquidity in time t is a sum of flows over all connections in the network in time t:

By assumption banks are not allowed to recapitalize losses and in all cases they go default when the level of capital they hold in their balance sheets falls short of the obligatory Tier 1 capital in total assets (4 %). Moreover, a default of any bank from the banking system affects the whole system through mutual connections of banks with the defaulted bank.

Say, bank j is a debtor of bank i (i.e. \((ij) \in { [\mathcal{V}]}^{2}\)) and denote its debt as q ij . Now, let \(\mathcal{F}\in \mathcal{V}\) be a non-empty set of all defaulted banks from the banking system \(\mathcal{G}\) and let bank j go bankrupt (i.e. \(j \in \mathcal{F}\)) at time t. Bank j deteriorates balance sheet of i for the amount of wd i that is now under pressure to finance those write-downs. For the sake of financing those losses bank i uses capital; in this case capital acts as a protection buffer from default. Its stock of capital evolves as

Here (6) shows an immediate write-down of wd from the balance sheet of bank i after bank j went bankrupt, while rr i = (0, 1) are partial recoveries; recovery rates are exogenous and randomly distributed among banks. In principle, the stronger the exposure against any defaulted debtor and the lower the reserved capital buffer of the respective creditors, the greater the potential for credit contagion.

We have thus seen how a unit of wd i can cause further losses. This spill-over depends on the importance of bank that was hit by a liquidity shock. We will use liquidity loss-potential estimator LLP i and bank specific α-criticality index as measures of influence; see Table 2 for the definitions.

K i, T from the table is time T level of liquidity in the network after bank i went bankrupt in period t, as given by (4), while a j, T is time T level of assets in the network (1) and a i, t ∗ are assets of bank i just before it got bankrupt in time t.

Liquidity loss potential is more volatile than α-criticality index and less indicative of changes in network structure; the latter responds to actual defaults of banks, the former measures changes in liquidity that are not necessarily preceeded by defaults. Potentially useful is also a [E(A) ∕ E(LLP)] r ratio that measures a rate at which a unit of liquidity lost in banking system r leads to a subsequent loss of a unit of its assets (i.e. both are under expectations’ operator). In measuring capacity of banking system to provide liquidity we will make use of a composite influence estimator

Say, each connection of the respective system r carries BI r information about the default of certain portion of liquidity (or assets, respectively). Now, set composite influence estimator as a proxy for this influence and define BI r as

2.2 Interbank Connections and Risk

By construction every bank i is given a subset of outgoing links \(\mathcal{L}(i): \vert \mathcal{L}(i)\vert = l_{i} \vert l_{i} \sim U(0,\Vert \beta \times (\vert \mathcal{V}\vert - 1)\Vert );\beta = [0,1]\) to banks debtors from the set of all debtors \(d \in \mathcal{D}\), such that \((id) \in { [\mathcal{V}]}^{2}\).

Let each debtor be ascribed a non-negative probability p d = (0, 1) of defaulting on its debt and let p be derived from logistic function

where \(y = f(x_{1},x_{2},\ldots,x_{n})\) is a function of specific factors x i from a set of potential factors that are influencing the behavior of d. Typically p(y) would be obtained by maximum likelihood regression on the logit, the inverse of the logistic function. It is not our aim to analyze the structure of risk profiles as such. We use simple heuristics instead and assign y to each debtor d by a neutral mechanism based on Table 3. Probability to default on its obligation is then calculated from (9). Defaults of those debtors are independent and shall be drawn as random variables.

In case any debtor defaults, (1 − rr d ) share of its liquidity leaves the banking network. Creditors of defaulted debtors need to recover those losses by their capital, respectively. This capital turns liquid and becomes available for liquidity needs of the banking network. If there is sufficient capital held with banks to withstand the losses, the network will suffer no net outflow of liquidity and vice versa.

Now, let the losses of liquidity caused by the defaulted debtor d to bank i be denoted by LL id and let p(y id ) denote a probability that debtor d from risk group y defaults on its debt to creditor i. As risk profiles of banks are independent by assumption, a probability that the banking network looses at least a unit of liquidity is given as

s.t.

This loss of liquidity causes certain instability to the banking network and increases its vulnerability against further liquidity losses; in case liquidity loss is large enough it induces serious structural changes (i.e. credit contagion).

2.3 Stability of Banking System

Each unit of liquidity that is released to the interbank by creditor i to debtor d can be seen as a moving particle x i with strictly positive probability of leaving the network. Say that X i is a variable, defined on a sample space \(\mathcal{S} =\{ 0,1\}\). Say further that x = 0 means that particle stays in the network and x = 1 that it leaves. Then the probability mass function for X i is defined as

Creditor i has \(\vert \mathcal{L}(i)\vert \) debtors d. Should any debtor d default on its debts to creditor i, all of its connections cease to exist and this liquidity is lostFootnote 3 (e.g. they share the bank’s risk). Now, let \(p(x_{s} = 1) = p(y_{id})\) denote the probability that bank d goes default and let p hold probabilities p i for every bank to go default. Hence, we can apply Shannon’s information entropy (13) to p and obtain an array p ∗ of available bits of information about the defaults for all connections from the banking network.

The higher the H(X) i the higher uncertainty in predicting the default of bank i. Distribution function (13) has four turning points important to our analysis:

Based on those turning points and two rules of thumb are seven stability domains as summarized in Table 4.Footnote 4 Vector p ∗ carries liquidity-loss potentials and α-criticality of all connections from the network. Stability index of the banking system \(\mathcal{V}_{r}\) is obtained as a weighted average of all values in \(({\mathbf{p}}^{{\ast}})_{r}\).

where w is a vector of weights.

Ranks of stability and contagion potential of the banking systems are based on the following corollaries:

-

1.

The higher the stability index, the less stable the system, expected contagion potential unchanged.

-

2.

The higher the expected contagion potential, the weaker the system in terms of providing liquidity, stability unchanged.

-

3.

Banks from safe and stable domain are not contagious.

-

4.

Contagion potential and stability are independent.

3 Results

We tested the stability of 100 independent banking systems consisting of 40 banks. As for the risk, the majority of banks belong to the safe and stable domain. Nine banks are somewhat less predictive and bank 18 is unpredictive; it carries low to moderate power to disrupt the banking system and spur contagion. On the other hand, bank 4 carries the strongest power to disrupt the banking system and cause contagion, but it is well within the safe and stable domain (i.e. tenth safest). Capacity of banking system to provide liquidity and remain stable thus depends essentially on the influence and risk profiles of the least stable group of banks.Footnote 5

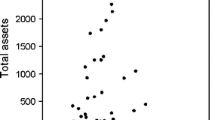

Liquidity loss potential (LLP i ) of individual banks in respective topologies. Banks are indexed on bottom axis and topologies on the left. Right axis shows expected probability of default (black dots) and Shannon’s entropy (white dots) for the banks as derived from (13)

Expected liquidity loss potential of respective banking system. A line is an ordered sequence

α-criticality of individual banks. Scaling, topologies and indexation are the same as in Fig. 1

Banking system 18 shows the lowest overall stability \((S[\mathcal{V}_{18}] = 22.756)\); 76 % of the score is due to banks from domains 3–7 and 28 % of the score is due to its 9 connections with bank 18. The system has 236 connections, making it ninth most uncertain on average. Excluding safe and stable banks from the score makes the system 52 the least stable \((S(\mathcal{V}_{52}\vert p_{i} > 0.025) = 17.38)\) and followed by system 18 \((S[\mathcal{V}_{18}\vert p_{i} > 0.025] = 17.283)\). Figures 1–6 in the sequel confirm a relatively large potential for disrupting the banking system of some banks. The last two suggest to remove banks from the safe and stabe domain when ranking banking systems’ contagion potential relative to their stability.

Expected α-criticality of respective banking system. The same scales as in Fig. 2. A line is an ordered (in descending order) sequence

A structure of stability index (columns; left axis). Black is a contribution of banks from domains 3–7; gray is the contribution of banks from domain 2 and light gray is the contribution of banks from domain 1 to the overall score. Lines present expected uncertainty per connection expressed in available bits of information about its default. Red are banks from domains 3–7; white banks from 2–7; yellow includes all banks

A structure of stability index. Ordered descending per overall score. Scaling and topologies are the same as in Fig. 7, indexation of bottom axis presents ranks of banking networks, respectively

Stability index (ascending order; left axis) and composite influence estimator (matched to stability index; right axis) of banking systems, given p i > 0. 025

Estimated contagion influence per one bit of information within the banking system (descending), given p i > 0. 025

Prime result of this paper is a distribution of information about the default of any bank from banking system as measured by BI r ; see Eq. (8). According to the BI r estimator, banking system 90 has potentially the most fragile connections (BI 90 = 0. 01616) and system 52 the least (BI 58 = 0. 00229); see Figs. 7–9 for more results).

Ranks of banking systems per their BI estimate (in descending order). Left axis shows identities of respective banking systems, bottom axis shows their ranks, accordingly

4 Concluding Remarks

We have constructed a BI estimator for detecting a default potential of each unit of interbank liability (on average) within any banking system. The estimator is based on a composite influence estimator and a stability index and it depends on the quality of information about risk profiles of banks and information about their mutual exposures. The composite influence estimator is a measure for detecting the affinity of banking system to loosing its ability for providing liquidity (i.e. it is a combination of liquidity loss potential and α-criticality), while stability index measures a level of information that is available within the banking system about the default of any of its banks. The latter is based on Shannon’s information entropy and can also serve as a tool for detecting the stability domain of banks and banking systems; we showed an example of its use in this respect and constructed seven fuzzy stability domains.

We tested the mechanism on a credit contagion model of 40 real banks connected in 100 random banking systems. Results are robust and the method can be easily employed to any banking system. Neither econometric nor statistical tests have been performed on the final results. However, there is a huge potential to devise data-based statistical methods for studying the structural characteristics of banking system and its stability as driven by the network approach.

Notes

- 1.

Consult also the studies by Freixas, Parigi and Rochet [9] about banks under uncertainty of withdrawals, where banks are connected through interbank credits, the desing of financial networks that minimize the trade-off between risk sharing and the potential for collapse presented in [14] and Dasgupta’s [6] study about banks’ crossholdings of deposits as a source of contagion. Furthermore, reader shall also consult de Vries [7] and his dependency between banks’ portfolios of assets and potential for systemic breakdown, Haldane and May’s [11] study of contagion in financial markets, Gai and Kapadia’s [10] model of contagion in financial networks, Cifuentes et al. [5] model of financial institutions that are connected via portfolio holdings, and the study of Jorion and Zhang [13], who show credit contagion via counterparty effects.

- 2.

See [4] for stress test on Austrian interbank network structure with respect to the default of a single bank.

- 3.

Recoveries are kept on creditors’ balance sheets and do not enter the interbank lending market.

- 4.

37 banks are in the 1st domain with two bordering on the 2nd; one bank is in the 6th domain and it has relatively weak liquidity loss potential and low α-criticality index.

- 5.

References

Allen F, Babus A (2008) Networks in finance. Available via SSRN. http://papers.ssrn.com/sol3/papers.cfm?abstract_id=1094883. Cited 30 Jan 2013.

Allen F, Gale D (2000) Comparing financial systems. MIT, Cambridge

Allen F, Babus A, Carletti E (2009) Financial crises: theory and evidence. Annu Rev Financ Econ 1:97–116

Boss M, Elsinger H, Summer M, Thurner S (2004) Network topology of the interbank market. Quant Financ 4(6):677–684

Cifuentes R, Ferrucci G, Shin H (2005) Liquidity risk and contagion. J Eur Econ Assoc 3:556–566

Dasgupta A (2004) Financial contagion through capital connections: a model of the origin and spread of bank panics. J Eur Econ Assoc 6:1049–1084

De Vries C (2005) The simple economics of bank fragility. J Bank Financ 29: 803–825

Eisenberg L, Noe T (2001) Systemic risk in financial systems. Manag Sci 47:236–249

Freixas X, Parigi B, Rochet J (2000) Systemic risk, interbank relations and liquidity provision by the central bank. J Money Credit Bank 32: 611–38

Gai P, Kapadia S (2010) Contagion in financial networks. Proc R Soc 466(2120):2401–2423

Haldane A, May R (2011) Systemic risk in banking ecosystems. Nature 469(7330):351–355

Iori G, De Masi G, Precup OV, Gabbi G, Caldarelli G (2008) A network analysis of the italian overnight money market. J Econ Dyn Control 32(1):259–278

Jorion P, Zhang G (2009) Credit contagion from counterparty risk. J Financ 64: 2053–2087

Leitner Y (2005) Financial networks: contagion, commitment, and private sector bailouts. J Financ 60:2925–2953

Schweitzer F, Fagiolo G, Sornette D, Vega-Redondo F, Vespignani A, White D (2009) Economic networks: the new challenges. Science 325:422–425

Steinbacher M, Steinbacher M, Steinbacher M (2012) Credit contagion in financial markets: a network-based approach. Available via SSRN. http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2068716. Cited 30 Jan 2013

Upper C, Worms A (2004) Estimating bilateral exposures in the German interbank market: is there a danger of contagion? Eur Econ Rev 4:827–849

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2014 Springer International Publishing Switzerland

About this chapter

Cite this chapter

Steinbacher, M., Steinbacher, M., Steinbacher, M. (2014). Banks and Their Contagion Potential: How Stable Is Banking System?. In: Leitner, S., Wall, F. (eds) Artificial Economics and Self Organization. Lecture Notes in Economics and Mathematical Systems, vol 669. Springer, Cham. https://doi.org/10.1007/978-3-319-00912-4_13

Download citation

DOI: https://doi.org/10.1007/978-3-319-00912-4_13

Published:

Publisher Name: Springer, Cham

Print ISBN: 978-3-319-00911-7

Online ISBN: 978-3-319-00912-4

eBook Packages: Business and EconomicsEconomics and Finance (R0)