Abstract

Stock market prices are inherently volatile, and accurate forecasting is challenging. An accurate prediction of stock prices helps traders and investors to decide timely buy or sell, so an optimal investment strategy can be built, decreasing investment risks. Traditionally, linear and non-linear methods have been applied to stock market prediction. Many studies on stock market prediction have recently employed machine learning and deep learning models with the proliferation of big data and rapid development in artificial intelligence.

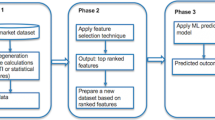

On the other hand, previous prediction studies mostly overlooked key indicators and feature engineering in the models. The feature selection can help to develop better prediction models. The stock price prediction requires a dynamic feature selection due to its time-dependent characteristics. There is no optimal set of technical indicators for stocks that perform well in all market scenarios. We propose a stock price prediction model focusing on dynamic feature selection in this study. The model uses technical, operational, and economic indicators besides price and volume data. The feature selection process has two stages. In the first stage, the importance of features for stocks is found by an ensemble learning algorithm. The final importance score is calculated by multiplying feature importance values with the next day’s model return which is the performance of the prediction method. In the second stage, a regression analysis is made daily for each feature using feature importance scores to track their performance in terms of average importance and slope (importance movement) dynamically. The proposed model enables better interpretability of features on stock price behavior and makes better stock price predictions.

Access this chapter

Tax calculation will be finalised at checkout

Purchases are for personal use only

Similar content being viewed by others

References

Yun, K.K., Yoon, S.W., Won, D.: Interpretable stock price forecasting model using genetic algorithm-machine learning regressions and best feature subset selection. Expert Syst. Appl. 213, 118803 (2023)

Kumari, B., Swarnkar, T.: Forecasting daily stock movement using a hybrid normalization based intersection feature selection and ANN. Procedia Comput. Sci. 218, 1424–1433 (2023)

Haq, A.U., Zeb, A., Lei, Z., Zhang, D.: Forecasting daily stock trend using multi-filter feature selection and deep learning. Expert Syst. Appl. 168, 114444 (2021)

Li, J., et al.: Feature selection: a data perspective. ACM Comput. Surv. (CSUR) 50(6), 1–45 (2017)

Huang, Q., Xia, T., Sun, H., Yamada, M., Chang, Y.: Unsupervised nonlinear feature selection from high-dimensional signed networks. In: Proceedings of the AAAI Conference on Artificial Intelligence, pp. 4182–4189. AAAI Press, USA (2020)

Gürcan, Ö.F., Beyca, Ö.F., Doğan, O.: A comprehensive study of machine learning methods on diabetic retinopathy classification. Int. J. Computat. Intell. Syst. 14(1), 1132–1141 (2021)

Naik, N., Mohan, B.R.: Stock price movements classification using machine and deep learning techniques-the case study of indian stock market. In: Macintyre, J., Iliadis, L., Maglogiannis, I., Jayne, C. (eds.) EANN 2019. CCIS, vol. 1000, pp. 445–452. Springer, Cham (2019). https://doi.org/10.1007/978-3-030-20257-6_38

Peng, Y., Albuquerque, P.H.M., Kimura, H., Saavedra, C.A.P.B.: Feature selection and deep neural networks for stock price direction forecasting using technical analysis indicators. Mach. Learn. Appl. 5, 100060 (2021)

Yun, K.K., Yoon, S.W., Won, D.: Prediction of stock price direction using a hybrid GA-XGBoost algorithm with a three-stage feature engineering process. Expert Syst. Appl. 186, 115716 (2021)

Ji, G., Yu, J., Hu, K., Xie, J., Ji, X.: An adaptive feature selection schema using improved technical indicators for predicting stock price movements. Expert Syst. Appl. 200, 116941 (2022)

Yan, W.L.: Stock index futures price prediction using feature selection and deep learning. North Am. J. Econ. Finance 64, 101867 (2023)

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2023 The Author(s), under exclusive license to Springer Nature Switzerland AG

About this paper

Cite this paper

Sivri, M.S., Gultekin, A.B., Ustundag, A., Beyca, O.F., Gurcan, O.F., Ari, E. (2023). A Dynamic Feature Selection Technique for the Stock Price Forecasting. In: Kahraman, C., Sari, I.U., Oztaysi, B., Cebi, S., Cevik Onar, S., Tolga, A.Ç. (eds) Intelligent and Fuzzy Systems. INFUS 2023. Lecture Notes in Networks and Systems, vol 758. Springer, Cham. https://doi.org/10.1007/978-3-031-39774-5_81

Download citation

DOI: https://doi.org/10.1007/978-3-031-39774-5_81

Published:

Publisher Name: Springer, Cham

Print ISBN: 978-3-031-39773-8

Online ISBN: 978-3-031-39774-5

eBook Packages: Intelligent Technologies and RoboticsIntelligent Technologies and Robotics (R0)