Abstract

We use social network analysis to model the trade networks that connect each of the United States to the rest of the world in an effort to capture trade shocks and supply chain disruptions resulting from the COVID-19 pandemic and, more specifically, to capture how such disruptions propagate through those networks. The results show that disruptions will noticeably move along industry connections, spreading in specific patterns. Our results are also consistent with past work that shows that non-pharmaceutical policy interventions have had limited impact on trade flows.

Access provided by Autonomous University of Puebla. Download conference paper PDF

Similar content being viewed by others

Keywords

1 Introduction

COVID-19 has caused both significant demand and supply shocks in international trade. The latter have conceivably been caused by policy interventions that required temporarily shutting down or slowing production as well as labor shortages caused by illness, while the former have been attributable to increased demand for some goods and decreased demand for others. Moreover, shifts in consumption patterns, such as where goods are consumed, have resulted in distribution challenges, especially for foodstuffs. In this research project we propose using social network analysis to model the trade networks that connect each of the United States to the rest of the world in an effort to capture trade shocks and supply chain disruption resulting from the COVID-19 pandemic and, more specifically, to capture how such disruptions propagate through those networks. We postulate that the high levels of interconnectedness in global trade make it likely that trade shocks and disruptions of supply chains will propagate primarily along industry-level trade networks. Modeling those networks along with trade shocks and supply chain disruption as we propose here would allow us to show not only the structure of trade networks, but also how disruptions and shocks travel along them. While we have chosen to focus on the United States due to the severity of its COVID-19 outbreak in the time sample and the availability of high-quality data, we do expect that many of the findings will be generalizable for complex economies, due to the homogenization of global trade structures.

2 Theory

2.1 Industry Linkages and Disruption Propagation

Prior to the COVID-19 pandemic, most supply chain disruption discussion focused on natural disasters, geopolitical events, changes in technology, cyber-attacks, and transportation failures as threats to supply chain stability. The literature divides the causes into quadrants based on controllability and whether they are internal or external to the firm experiencing the disruption [1]. Agriculture and foodstuffs hold a prominent place in the literature due to their vulnerability to uncontrollable external disruptions, but the COVID-19 pandemic has shown that most, if not all, industries are at risk of a global disruptive event. This coincides with a general trend among firms to underestimate levels of risk to their supply chain, often leaving them unprepared to respond to disruptions as they occur [25]. Moreover, while the literature indicates that both the costs associated with such disruptions and their frequency have increased globally, the underlying assumption has long remained that they tend to be rooted locally. This has meant that the mitigation strategies developed do not account for global disruptions [21]. An important outlier has been the work of Nassim Taleb, whose assessment of vulnerabilities in global supply chains that hinge on Just-In-Time manufacturing caused him to advocate for fail-safes and backup system [20]. In this paper, we not only look at all industries, but control for interaction of disruptions at the global and local level to fill the aforementioned gap in our understanding of supply chain vulnerabilities.

There are a number of extant measures for the robustness of supply chain worldwide. For example, the Euromonitor International publishes a supply chain sensitivity index compiled on the bases of measures of sustainability, supply chain complexity, geographic dependence, and transportation network [10]. Sharma, Srinastava, Jindal, and Gupta’s comprehensive assessment of supply chain sensitivity combining 26 factors, found that having a critical part supplier, location of supplier, length of supply chain lead times, the fixing process owners, and mis-aligned incentives were the most critical factors in supply chain robustness [17]. While they both identify important aspects of supply chain vulnerability, they fail to fully account for the manner in which supply chain risk compounds as disruption spreads through industry connections. Past literature has provided theoretical grounding for this, depending largely on qualitative case studies to map out how disruption propagate through industry-based supply chain triads of suppliers, manufacturers, and consumers [16]. Zhu et al., mapping industrial linkages using the World Input-Output Database, found that on a global scale, the asymmetrical industrial linkages could see local shocks causing serious disruptions along the supply chain [2]. In this study, we extend the theoretical framework, albeit in a simplified operationalization, using quantitative analysis for a large national market and its global connections. We hypothesize that industry connections will be a significant vehicle for the spread of disruptions between US states.

2.2 Effectiveness of Policy Interventions

Due to the exceptional nature of pandemics on the scale of COVID-19, limited analysis exists of the economic disruption they cause and of the impact of policy measures intended to mitigate against them. The last comparable global pandemic in terms of severity and the number of economies affected was the Spanish Flu of 1918. In the limited literature available to us, policy assessments have found that public health interventions such as economic support and lockdowns did not have adverse economic effects and that these areas recovered more quickly [3]. The emerging literature assessing the efficacy of lock downs for COVID-19 show that stay at home orders did not impact trade, whereas workplace closures did negatively impact trade [6]. This suggests a limited impact for policy measures controlling adverse economic impacts on trade flows. This previous study by Hayakawa and Mukunoki was focused on country-level variation and focused on stay-at-home orders and workplace closures. We build on this work by looking at domestic propagation of disruption, while including potential policy confounders such as economic support and network confounders such as cluster effects.

3 Data and Research Design

The monthly U.S. state-level commodity import and export data used in our analysis were collected by the US Census using the U.S. Customs’ Automated Commercial System [23]. For our analysis, we use data from March 2020 to December 2020. We use this cutoff both due to availability at the time of writing and to avoid having to account for changes in the federal and local responses to the pandemic as a result of the 2020 election. The import and export data are reported in total unadjusted value, in US Dollars. All 50 states and the district of Columbia are included as nodes in the final networks.

To construct the dependent edge-level variable used in our models, we first constructed a bipartite graph with states as the first mode and exports at the four-digit level commodity code of the Harmonized System (HS-4) as the second mode. The edges in the bipartite graph are a measure of export disruptions, comparing export value of the current month to a three-month window centered on the same month of the previous year. If the value of the current month was less than 75% of the minimum value in the window for the previous year, it was coded as a one for a disruption. We then collapse the bipartite graph into a monopartite graph of US states and the edges are counts of the number of shared disruptions a state has with other states at the same HS-4 commodity level. We collapse the data primarily for methodological reasonsFootnote 1, but since our goal is to measure trade disruption spread through industry ties, this step does not lose information that we are interested in. For robustness, we repeat this process using a 50% minimum value threshold.

3.1 Covariates

In addition to using US Census data for our export disruption dependent variable, we also use the import data to control for import disruptions of inputs for the export industries. The variable is constructed as a weighted count using the 2014 World Input Output Database (WIOD) [22]. Import disruptions were first constructed in the same manner as export disruptions and then assigned weights for each HS-4 commodity. The weights were assigned using concordance tables to convert HS-4 codes to match International Standard of Industrial Classification (ISIC) codes to then calculate the commodity’s input value as a percentage of the total output value for an industry. Since the weights were percentages based on values in the WIOD and applied to counts of disruption, not trade values, no transformation was necessary to match real USD values. Last, they were collapsed to match the monopartite network.

To measure the impact of COVID-19 and COVID-19 related policies, we include hospitalizations per capita, an Economic Support Index, and a Lockdown Index. Hospitalizations per capita were calculated using monthly max hospitalization data from The Covid Tracking Project and then divided by 2019 state population estimates from the US Census Bureau. The Economic Support index and the Lockdown index are taken from the Oxford COVID-19 Government Response Tracker (OxCGRT) [4]. The Economic Support index includes measures that lessen the economic impact of COVID-19, including and weighting state level variation in measures such income support and debt relief. The Lockdown index focuses on measures intended to control people’s behavior, including measures such as mask mandates, school and gym closings, and restrictions gathering size and indoor dining.

3.2 Model and Specification: The Count ERGM

Existing models of network effect in supply chain risk management have relied on complex models based in game theory [24], firm level cluster analysis [5], Bayesian network modeling that defined edges as causes of disruption [13], and myriad others [7]. In our contribution, we are the first to our knowledge to use the count-valued Exponential Random Graph Model (ERGM) [8] to model the spread of export disruptions. This model has two key advantages for the purposes of our study. First, it allows us to model network structure without assuming the independence of observations, as is the case with the majority of generalized linear models (GLM). For example, we include transitivity, also known as the clustering coefficient, to model the linkages between shared disruptions. Moreover, this model allows us to control for deviation from the specified reference distribution, including larger variance and zero inflation. These are both critical, as we know that economic disruptions in one state will impact economic conditions in other states and that dependent variable distribution rarely follows a specific distribution perfectly.

The count ERGM, like all ERGMs, does not model unit level effects as GLMs do, but rather the dependent variable serves to model the entire network using an iterative estimation method (MC-MLE) in which, given starting values for the parameter estimates, a Markov Chain Monte Carlo method is used to sample networks in order to approximate a probability distribution [18]. This iterative process continues until the parameter estimates and probability distribution converge. Because the ERGM family of models allows the research to specify both network effects and covariate effects in the model, both end up being more accurate estimates [12]. While other statistical modeling approaches could be used to account for network dependence while estimating covariate effects (e.g., latent space methods [11], stochastic block modeling with covariates [19], and quadratic assignment procedure [14]), these alternative methods do not permit precise estimation and testing of specific network effects. Given that part of our research objective is to test for transitivity effects, we have adopted an ERGM-based approach, using the implementation made available in the ergm.count [9] package in the R statistical software.

Under the count ERGM, the probability of the observed \(n \times n\) network adjacency matrix \(\boldsymbol{y}\) is:

where \(\boldsymbol{g}( \boldsymbol{y} )\) is the vector of network statistics used to specify the model, \(\boldsymbol{\theta }\) is the vector of parameters that describes how those statistic values relate to the probability of observing the network, \(h(\boldsymbol{y})\) is a reference function defined on the support of \(\boldsymbol{y}\) and selected to affect the shape of the baseline distribution of dyadic data (e.g., Poisson reference measure), and \(\boldsymbol{\kappa }_{h,\boldsymbol{g}}(\boldsymbol{\theta })\) is the normalizing constant.

Our main models include a number of base level convergence related parameters, network parameters, and covariate parameters. Base level parameters include the sum of edge values, analogous to the intercept in a GLM model as well as the sum of square root values to control for dispersion in edge values. For network effects we include a transitive weight term. The transitive weight term is specified as:

This term accounts for the degree to which edge (i, j) co-occurs with pairs of large edge values with which edge (i, j) forms a transitive triad with weighted, undirected two-paths going from nodes i to k to j. Note that, because the network is undirected, cyclical and transitive triads are indistinguishable. Exogenous covariates are included by measuring the degree to which large covariate values co-occur with large edge values. Our only dyadic measure is that of shared, weighted import disruptions and is defined as:

Lastly, we specify statistics that account for node (i.e., state) level measures of COVID-19 intensity and policy measures. These parameters take the product of the node’s covariate value and a sum of the edge values in which the node is involved, defined as:

We estimate a separate model for each month for all industries and then use a time-pooled version when estimating models by industry. This allows us to see changes in general trends across time as well as changes in the impact of variables over time throughout the pandemic, as well as average effects for each industry.

4 Results

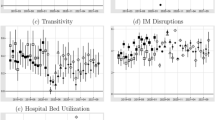

There are several important findings from our results for the overall model, shown in Fig. 1. We also remind readers that the disruptions here are not overall disruptions, but shared disruptions across states, which means that interpretations are for spread of disruptions, not overall disruption. However, there is some overlap as an increase in shared disruptions coincides with an increase in the likelihood of overall disruptions. First, we see in Panel a and b that disruptions and the overall dispersion of shared disruptions peaks in April and gradually declines across time. The second major finding is that non-pharmaceutical policy interventions (Panel f and g) had almost no impact on shared export disruptions, regardless of disruption intensity. While there are a number of sound reasons to implement lock-downs and economic support for economies in a pandemic, our results indicate that trade need not be considered as a factor in considering these measures to contain the spread of disease. Third, the transitivity coefficient (Panel c) is positive and significant for all months considered, with a small drop in the early part of the pandemic before rising again. On average, it is roughly double in effect size for more intense disruptions. This result is a strong indicator of spread through industry connections as the edges are defined as shared disruptions in the same commodity, supporting our hypothesis that export disruptions will spread through industry ties across states. Fourth, import input disruptions (Panel d) are also positive and significant, with effects growing in size for more intense disruptions. This also is indicative of the importance of supply chains and the spread of disruptions through global trade networks. Lastly, while hospitalizations (Panel e) are on average positively correlated with shared export disruptions, the relationship is volatile, even being negative at the beginning of pandemic and in late Fall indicating that immediate pandemic intensity is not the primary driver of economic disruption.

Coefficient estimates of terms in Poisson ERGMs. Bars span 95% confidence intervals. For some models, the confidence intervals are not visible due to being small and the large range of the coefficient estimates. Circles are for models of disruptions of 75% and triangles are for 50%

Coefficient estimates of terms in time-pooled Poisson ERGMs. Bars span 95% confidence intervals. For some models, the confidence intervals are not visible due to being small and the large range of the coefficient estimates. Circles are for models of disruptions of 75% and triangles are for 50%

Variation of the coefficients across industries also leads to several interesting findings (Fig. 2). In Panel a we see that transitivity is mostly the same across industries. The exception is that industry seven (Raw Hides, Skins, Leather, and Furs) serves as an outlier for transitivity and that the clustering coefficient trends slightly larger for less processed industries (lower numbered). This trend is more pronounced for input import disruptions (Panel b). This finding is interesting as one might expect more highly processed industries to have more inputs and thus be more sensitive to disruptions in imports and across industry changes. Furthermore, while there are some similarities, these findings challenge the rankings of supply chain sensitivity in the Euromonitor’s Global Supply Chain index which ranks the least and most processed as the most sensitive and the moderately processed as the least sensitive [10]. Hospitalizations across industry (Panel c) are just as volatile across industry as it is across time, warranting deeper investigation. Lastly, we confirm that even when broken down by industry, policy variables have little to no impact on the spread of export disruption (Panel d and e).

5 Conclusion

The global pandemic that has gripped the world since early 2020 has exacted an incalculable toll in human lives, while crippling economies for much of that year. Given the impact of the pandemic as well as of policy responses intended to limit the cost in human lives, trade disruptions were to be expected throughout supply chains. Indeed, beyond policy responses, panic-buying and other behavioral oddities caused severe disruptions in very specific supply chains very early on. Given that the previous global pandemic of 1918 took place in an economic environment of much lesser economic complexity, studies examining that event could not accurately predict the manner in which modern economies and industries would be affected. Modern supply chains are, after all, significantly more spread out globally. Indeed, across the globe, new debates have emerged with regard to the perceived need to ‘re-home’ certain key industries as Just-In-Time supply chains dependent on imports from across the globe that have proven to be vulnerable to disruptions in trade over which individual governments have no control.

This pandemic, then, has presented us with a rather unique global challenge, as well as a rather unique opportunity to look at the robustness – or lack thereof – of global supply chains in our modern globalized economic environment. More than just a study into the impact of the current global pandemic on global supply chains, our study was intended to close a hole in the extant and emerging literature, which has not used network level analysis of the manner in which trade shock and disruption moves across networks. It was our hypothesis that disruptions will noticeably move along industry connections, spreading in specific patterns, and our model appears to support this hypothesis. We believe that this is an important finding that has application beyond the context of a global pandemic.

Notes and Comments. All data used are from publicly available sources. For replication code, please email the authors.

Notes

- 1.

It is common in network analysis literature to collapse bipartite graphs due to failed convergence in bipartite inferential models and for additional model features not available in bipartite models. Past work has shown that collapsing into a monopartite project still preserves important information about the network [15].

References

Agrawal, N., Pingle, S.: Mitigate supply chain vulnerability to build supply chain resilience using organisational analytical capability: a theoretical framework. Int. J. Logistics Econ. Globalisation 8(3), 272–284 (2020)

Cerina, F., Zhu, Z., Chessa, A., Riccaboni, M.: World input-output network. PloS one 10(7), e0134025 (2015)

Correia, S., Luck, S., Verner, E.: Pandemics depress the economy, public health interventions do not: evidence from the 1918 flu. SSRN (2020)

Hale, T., et al.: A global panel database of pandemic policies (Oxford COVID-19 government response tracker). Nat. Hum. Behav. 5(4), 529–538 (2021)

Hallikas, J., Puumalainen, K., Vesterinen, T., Virolainen, V.-M.: Risk-based classification of supplier relationships. J. Purch. Supply Manag. 11(2–3), 72–82 (2005)

Hayakawa, K., Mukunoki, H.: Impacts of lockdown policies on international trade. Asian Econ. Pap. 20(2), 123–141 (2021)

Hosseini, S., Ivanov, D., Dolgui, A.: Review of quantitative methods for supply chain resilience analysis. Transp. Res. Part E: Logistics Transp. Rev. 125, 285–307 (2019)

Krivitsky, P.N.: Exponential-family random graph models for valued networks. Electron. J. Stat. 6, 1100 (2012)

Krivitsky, P.N.: ergm.count: fit, simulate and diagnose exponential-family models for networks with count edges. The Statnet Project (2016). http://www.statnet.org. R package version 3.2.2

Julian, L.: Supply chain sensitivity index: which manufacturing industries are most vulnerable to disruption? July 2020

Matias, C., Robin, S.: Modeling heterogeneity in random graphs through latent space models: a selective review. ESAIM: Proc. Surv. 47, 55–74 (2014)

Metz, F., Leifeld, P., Ingold, K.: Interdependent policy instrument preferences: a two-mode network approach. J. Public Policy, 1–28 (2018)

Ojha, R., Ghadge, A., Tiwari, M.K., Bititci, U.S.: Bayesian network modelling for supply chain risk propagation. Int. J. Prod. Res. 56(17), 5795–5819 (2018)

Robins, G., Lewis, J.M., Wang, P.: Statistical network analysis for analyzing policy networks. Policy Stud. J. 40(3), 375–401 (2012)

Saracco, F., Straka, M.J., Di Clemente, R., Gabrielli, A., Caldarelli, G., Squartini, T.: Inferring monopartite projections of bipartite networks: an entropy-based approach. New J. Phys. 19(5), 053022 (2017)

Scheibe, K.P., Blackhurst, J.: Supply chain disruption propagation: a systemic risk and normal accident theory perspective. Int. J. Prod. Res. 56(1–2), 43–59 (2018)

Sharma, S.K., Srivastava, P.R., Kumar, A., Jindal, A., Gupta, S.: Supply chain vulnerability assessment for manufacturing industry. Ann. Oper. Res. 1–31 (2021). https://doi.org/10.1007/s10479-021-04155-4

Snijders, T.A.B.: Markov Chain Monte Carlo estimation of exponential random graph models. J. Soc. Struct. 3(2), 1–40 (2002). Kindly provide the volume number for Ref. [17], if applicable.

Sweet, T.M.: Incorporating covariates into stochastic blockmodels. J. Educ. Behav. Stat. 40(6), 635–664 (2015)

Taleb, N.N.: Antifragile: Things that Gain from Disorder, vol. 3. Random House Incorporated (2012)

Tang, C.S.: Robust strategies for mitigating supply chain disruptions. Int. J. Logistics: Res. Appl. 9(1), 33–45 (2006)

Timmer, M.P., Dietzenbacher, E., Los, B., Stehrer, R., De Vries, G.J.: An illustrated user guide to the world input-output database: the case of global automotive production. Rev. Int. Econ. 23(3), 575–605 (2015)

US Census Bureau. US import and export merchandise trade statistics. Economic Indicators Division USA Trade Online, March 2021

Wu, T., Blackhurst, J., O’grady, P.: Methodology for supply chain disruption analysis. Int. J. Prod. Res. 45(7), 1665–1682 (2007)

Zsidisin, G.A., Panelli, A., Upton, R.: Purchasing organization involvement in risk assessments, contingency plans, and risk management: an exploratory study. Supply Chain Manage. Int. J. (2000)

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2022 The Author(s), under exclusive license to Springer Nature Switzerland AG

About this paper

Cite this paper

Schoeneman, J., Brienen, M. (2022). The COVID-19 Pandemic and Export Disruptions in the United States. In: Benito, R.M., Cherifi, C., Cherifi, H., Moro, E., Rocha, L.M., Sales-Pardo, M. (eds) Complex Networks & Their Applications X. COMPLEX NETWORKS 2021. Studies in Computational Intelligence, vol 1072. Springer, Cham. https://doi.org/10.1007/978-3-030-93409-5_59

Download citation

DOI: https://doi.org/10.1007/978-3-030-93409-5_59

Published:

Publisher Name: Springer, Cham

Print ISBN: 978-3-030-93408-8

Online ISBN: 978-3-030-93409-5

eBook Packages: EngineeringEngineering (R0)