Abstract

One area almost completely ignored by economic studies, and yet which has possibly the greatest potential to influence whether Brexit will ultimately be viewed as a policy success or failure, concerns the flexibility of UK policy formation. Depending upon the final form that Brexit takes, it has the potential to present policy makers with additional policy instruments which are not currently available and which have the potential to transform the national economy. Active forms of industrial and procurement policies are the most obvious examples and are examined in some detail in this chapter. Similarly, this chapter discusses macroeconomic options to reduce uncertainty and provide a solid foundation to encourage higher rates of investment and capital formation than have been the norm in the UK for decades.

Access provided by Autonomous University of Puebla. Download chapter PDF

Similar content being viewed by others

Keywords

One remarkable feature of almost all economic studies which have sought to forecast the impact of Brexit is that they have consistently ignored the role of macroeconomic policy in affecting the outcome. Presumably, this was to simplify the analysis. Yet, this omission is unrealistic for two reasons.

Firstly, one of the main claims for Brexit improving economicperformance is that UK policy makers have greater flexibility to implement initiatives designed to meet the particular circumstances and challenges facing the domestic economy. Previous chapters in this book have examined inward investment, trade policy, labour force planning and issues related to productivity. However, greater flexibility in designing macroeconomic strategy, combined with industrial and procurement policy, have arguably an even greater potential; the realisation of which depends crucially upon the type of Brexit chosen to replace EU membership, together with whether the government of the day has the insight and determination to design policy to realise potential gains. Consequently, economic studies should have placed greater weight upon the impact of economic policy measures not less.

Secondly, even assuming the predictions made by the mainstream economic studies were correct and that certain aspects of Brexit would inflict net costs upon the UK economy, it is unrealistic to expect policy makers not to react to minimise this effect. Indeed, almost immediately after the referendum result was announced, the Bank of England presented a significant stimulus package, whilst the then Chancellor of the Exchequer, Hammond, announced a partial relaxing of the former tight fiscal stance, thus restoring a measure of confidence and preventing unnecessary economic damage. It is only a pity that this immediate reaction was not carried through into the immediate reversal of austerity measures, combined with a more decisive leadership from parliament to reduce uncertainty during 2017–2019.

The omission of consideration of economic policy variables might be justifiable if study authors made it explicit that they were only concerned with examining the narrow context of what would be likely to occur if policy makers were entirely passive—that is, what might happen if no other actions were taken. However, this would have been the limit of these studies. To subsequently present their results as forecasts or predictions as to the likely prospects of the UK economy is deeply problematic. This matters because policy makers and business leaders have relied upon the accuracy of these studies to set their respective future strategies. Failure to properly consider policy actions in these studies sadly undermined their accuracy and hence weakened their utility.

This chapter seeks to rectify this apparent reluctance to include economic policy in consideration of the economic impact of Brexit.

Macroeconomic Policy

Uncertainty

One of the anticipated negative consequences resulting from the Brexit result concerned the uncertainty generated for all economic actors (HMG 2016: 21; Bank of England 2019: 38). To some extent, this was always likely to occur irrespective of the referendum result, as each and every general election results in uncertainty as to the likely result and the subsequent consequences for either continuation or a shift in economic strategy (Credit Suisse, 2016: 6; Punhani and Hill 2016: 5). Yet, the uncertainty relating to Brexit is of a different magnitude since it involves the evolution and partial replacement of a fundamental economic relationship that had formed a key part of the UK economy for more than four decades. Indeed, the Bank of England has argued that Brexit uncertainty has “only exceeded in the financial crisis” (BOE 2019: 48).

The economics literature indicates that there is likely to be a negative impact upon business investment arising from increased uncertainty (Dixit and Pindyck, 1990; Leahy and Whited 1996; Punhani and Hill 2016: 3, 7). Investment may be delayed or deferred (Bloom 2009; Bloom et al. 2014), particularly where firms have large existing fixed investment (sunk costs) (Pindyck 1988; Bank of England 2019: 39). Once uncertainty is resolved, however, there is an expectation that firms will respond to conditions of pent-up demand by unfreezing investment in new capacity and technology (Baker et al. 2016b: 1597). To the extent that investment was merely delayed, rather than cancelled or undertaken in a different jurisdiction, negative effects caused by uncertainty may be limited. Moreover, to the extent that advocates of Brexit are successful in demonstrating potential gains arising from the Brexit process—perhaps through interest expressed by non-EU nations in negotiating future trade agreements with the UK or through utilising the greater policy flexibility post-withdrawal to rejuvenate UK manufacturing industry—this might, to some extent at least, offset other negative expectations (PwC 2016: 6). However, there is no certainty that all deferred investment will, in fact, take place, and moreover, the longer the growth potential in the economy stalls, the more likely that it will have longer-term negative effects (Wren-Lewis 2019: 45). Consequently, there is an incentive for policy makers to resolve uncertainty as swiftly as possible. Keynesian demand management policies could also be helpful in this regard, by creating conditions more conducive for encouraging the realisation of investment decisions in order to take advantage of favourable levels of demand for products and services.

Uncertainty can also affect financial markets, through impacting upon the value of stocks and currencies, or via higher risk premia being charged in credit and equity markets (PwC 2016: 6, 8). In the immediate aftermath of the referendum result, UK stock market valuation fell sharply, although this immediate paper loss was recovered within a few weeks. The value of sterling did, as expected, decline significantly against the Euro (Ebell and Warren 2016; Fairbairn and Newton-Smith 2016: 16; OECD 2016: 12). The extent of this change depends upon the dates selected over which the comparison is made. Thus, if a date of January 2015 is selected as representing a pre-referendum comparator, sterling was trading at €1.28. Since the current value of sterling, in January 2020, is approximately €1.18, this represents a 7.8% fall in the value of the pound over this period. If, however, the value of sterling is taken on the morning of the European referendum itself, when speculation over the result had temporarily increased the value of sterling to €1.31, then the scale of the depreciation has been approximately 10%.Footnote 1 Interestingly, the immediate effect of the referendum result was to cause only a 6% depreciation in sterling, whereas the handling of the post-referendum process caused sterling to fall by an additional 12%,Footnote 2 before gradually recovering. This would suggest that the decision to withdraw from the EU was only one element of the uncertainty causing depreciation of the exchange rate, with the government’s handling of the Brexit process and negotiation with the EU, together with the lack of a parliamentary majority, having a larger effect.

Exchange rate depreciation can have inflationary effects, and indeed, the rate of UK inflation did rise from 0.8% in June 2016 to a peak of 2.8% in October 2018, thereby exceeding the Bank of England’s 2% target for most of 2017–2018.Footnote 3 However, this is not as significant as it might appear (Baker et al. 2016a: 115). A peak rate of 2.8% is low by historical standards and the starting point of 0.8% inflation had raised concerns that it presaged a period of economic slowdown or recession. In addition, exchange rate volatility can have a detrimental effect upon the cost of trade and trade volumes, yet this only really manifests if volatility persists for a significant period of time, given that companies typically hedge against the effects of currency variability in the short term (Pilbeam 2016). In general, the economics literature is fairly dismissive of the idea that exchange rate volatility has more than a negligible impact upon growth over the medium or longer term (Eichengreen and Boltho 2008: 27). This appears to be confirmed by the evidence relating to the trade effects of the depreciation of sterling following the referendum as the trade gap narrowed. Moreover, the decline in the value of sterling was always expected to have a positive boost to exports and reduce the trade deficit, thereby offsetting (in full or in part) other negative consequences that may arise from Brexit (Armstrong and Portes 2016: 5).

One final Brexit-related effect concerns the ability of the UK government to borrow as cheaply on international markets, as international investors might be less likely to wish to hold gilts, combined with ratings agencies downgrading the value of UK government securities (Baker et al. 2016a: 111). This problem is not as acute for the UK as for many national governments since its giltmarket is disproportionately domestic, with international investors only holding around one quarter of the total issue. Moreover, most governmentbonds are of longer than average duration, meaning that any short-term problems would take a number of years before their impact became problematic. Hence, little effect has been observed thus far. If, however, Brexit-related uncertainty was to persist into the medium term, the cost of debt financing, for businesses and governments alike, might rise (Baker et al. 2016a: 114).

A number of the economics studies, discussed in Chap. 1, sought to incorporate a variable related to uncertainty in their calculations. The problem is that uncertainty is, by definition, difficult to define and measure. Accordingly, these studies modelled uncertainty as equivalent to risk, which can be calculated based upon probabilities drawn from a well-established dataset. Assumptions were made that Brexit will reduce trade with the EU and lower business export earnings, which would in turn likely raise the cost of capital and temporarily increase the risk premium paid for borrowing to fund investment (Baker et al. 2016a: 109; PwC 2016: 6,22). It is this higher risk premia that is then utilised as a proxy for uncertainty, to produce estimates that UK gross domestic product (GDP) will grow more slowly over the medium term as a result of Brexit, albeit that these negative effects would cease to have an effect thereafter.

The problem with adopting this approach is that there is a key difference between uncertainty and risk. Uncertainty embodies both ‘risk’, where uncertainty of outcomes can be represented by a known probability distribution, and more general ‘uncertainty’, when the probability distribution itself is unknown. Former US defence secretary, Rumsfeld, sought to express something of this lack of knowledge in his oft-quoted statement:

There are known knowns; there are things we know we know. We also know there are known unknowns; that is to say we know there are some things we do not know. But there are also unknown unknowns—the ones we don’t know we don’t know.Footnote 4

The treatment of uncertainty as being equivalent to risk therefore diminishes its significance. Information remains incomplete in an ever-changing economy, and this is particularly the case with respect to Brexit-related uncertainty because this derives from a unique historical occurrence with no direct precedent. This results in market failure and economic actors responding to events through adaptive (not rational) expectations. As a result, policy makers have to resort to judgement about the probable results of actions, costs and benefits associated with various possible outcomes resulting from different policy options (Greenspan 2003). This was the essence of the writings of Keynes, in the 1930s, where the active management of the economy was prescribed as a means of creating conditions conducive for investment and employment, and thereby overcoming caution related to uncertainty about the future.

A second reason why uncertainty cannot be diminished by treating it as equivalent to risk relates to inadequacies with the data upon which risk management and the development of probability distributions are based. These are of three main forms. Transitory statistical uncertainty relates to when provisional data is revised as more information becomes available. Permanent statistical uncertainty occurs when data is incomplete or inadequate. Finally, epistemic uncertainty, arising from a lack of knowledge about current and historical data, which is expected to diminish as data is augmented over time.

There have, nevertheless, been a number of interesting attempts to seek to capture a more accurate appreciation of the comparative level of uncertainty pertaining in a given economy at any one moment in time. One of the most promising is the construction of an index of uncertainty drawn from longitudinal newspaper coverage (Baker et al. 2016a). Whilst this methodology has weaknesses, both in terms of labour intensity of data collection, the narrow range of newspapers utilised in the research and the reliance upon the researcher to identify incidents of uncertainty without unintentionally biasing the data, the approach is nevertheless rather useful in providing a means of comparing general levels of uncertainty over time and between different nations. Using this approach, indications are that uncertainty rose sharply in the period preceding, during and immediately following the 2016 European referendum in the UK, but from 2018 onwards, the level of uncertainty did not appear to be particularly marked (see Fig. 8.1). To the extent that this analysis accurately captures the essence of uncertainty, it would suggest that the most marked and therefore problematic expression of Brexit-related uncertainty was of relatively short duration, lasting perhaps 18 months, whilst what has followed has been difficult to distinguish from more general uncertainty experienced in the period preceding and following the 2008 financial crisis and economic slowdown. This interpretation is quite different from the impression garnered from other sources.

UK economic policy uncertainty, monthly index. Note: Each bar represents a month; however, due to space limitations, horizontal axis labels are only shown every six months. For example, 2019 1 means January 2019, 2019 7 means July 2019. Source: Authors’ interpretation of data available to download on the website for UK Economic Policy Uncertainty index, available via: https://www.policyuncertainty.com/uk_monthly.html

A second approach has been to use business surveys to identify an increased frequency of respondents identifying Brexit as a cause of uncertainty (Bank of England 2019: 40). Closer examination of the results suggests that it is difficult to distinguish between a general pessimism over the prospects for the global economy, with those for the UK, and a Brexit-specific element of uncertainty.Footnote 5 Moreover, it is not particularly surprising that increasing numbers of respondents mention Brexit as a factor in their investment deliberations as the topic has led most broadcast news bulletins over the past four years. The frequency of mentions, however, does not necessarily equate to action.

Notwithstanding these considerations, the Bank of England (2019: 40–3) appears sufficiently confident that investment and supply capacity have been negatively affected by Brexit-related uncertainty, and has accordingly internalised these anticipated effects in its own forecast for the future of the UK economy. There is a danger in doing so, in that this creates a self-fulfilling prophesy, as economic actors become more pessimistic precisely because of the Bank’s predictions, and their subsequent changes in behaviour are ex post facto used by the Bank in the following forecast report as evidence for the accuracy of its previous predictions. This is not simply a matter for the Bank, but also for that range of organisations whose studies were discussed in Chap. 1, where flaws inherent in model design may have inadvertently contributed towards more pessimistic expectations for Brexit than might arguably have been the case.

The difficulties in identifying a Brexit-related element in a more general measurement of uncertainty arise from the latest figures to be published as this book was being finalised. The IHS Markit’s Purchasing Managers’ Index for services, for example, has risen back to levels previously recorded in early 2018, and which would indicate the economy expanding rather than contracting.Footnote 6 Similarly, the Confederation of British Industry (CBI) Industrial Trends Survey recorded business confidence rising in the manufacturing sector.Footnote 7 This improvement in business confidence may derive from a reduction in Brexit uncertainty, as the December 2019 General Election result removed the parliamentary deadlock and provided a clearer roadmap for the evolution of the Brexit process during 2020. However, it might equally relate to the preference amongst the business community for the majority won by the Conservative Party in that election. This reduction in uncertainty and improvement in business confidence has not had time to filter through into a noticeable improvement in output and macroeconomic performance. Therefore, these remain only potential early indicators of future developments. Moreover, it is quite possible that any reduction in Brexit uncertainty might be outweighed by future unrelated developments, such as the disruption to production and supply chains caused by the COVID-19 coronavirus or the continuing trade dispute between China and the USA. The complexity of inter-related factors influencing a single forecasting indicator (business confidence) highlights the difficulty in isolating the effect of any single contributory factor (i.e. Brexit).

There are two additional points that should be considered in relation to uncertainty.

The first is that in acknowledging that change the UK’s relationship with the EU will inevitably create risks (CBI 2013: 132) and the time lags involved in implementing these changes will cause uncertainty, this would also have been true when the UK joined the then Common Market in the 1970s and would have been equally true when the CBI and others lobbied for the UK joining the ERM and the Economic and Monetary Union (EMU) in the 1990s. Moreover, risks emanating from Brexit have to be placed against risks that would occur if the UK remained within the EU. For example, it is not certain that the status quo position for the UK would have been tenable in the medium term, even had the UK remained a member of the EU, as Eurozone economies were seeking to strengthen EU economic governance as a means of creating a more supportive infrastructure necessary to sustain the single currency (Armstrong and Portes 2016: 6). In addition, as an EU member state, the UK would have been more affected by further economic contagion arising from the continued fragility of the Eurozone (Business for Britain 2015: 30).

The second point is that Brexit-related uncertainty has not been resolved by the conclusion of the Article 50 process and the UK formally withdrawing from the EU. The transition period is scheduled to end at the end of 2020, at which time, if an agreement has not been reached and enacted, either an extension must be requested and unanimously agreed (not currently the UK government’s preference) or trade between the UK and the EU will take place according to World Trade Organization (WTO) rules. Whilst negotiations continue, so will uncertainty (Irwin 2015: 28–9; McFadden and Tarrant 2015: 60).

Has Uncertainty Reduced UK Growth?

This is a difficult question to answer convincingly. What can be noted is that the UK economy generated respectable (but not ebullient) GDP growth rates of 1.8% in 2016 and 2017, in the immediate aftermath of the referendum result, before slowing to 1.4% in 2018 and 1.2% in 2019, and is forecast to remain within the 1.4–1.6% range for the next few years (OBR 2019: 11). The immediate conclusion is that there has not been a substantial deterioration in UK growth performance, following the 2016 referendum result, whilst predictions that the UK would fall into an immediate recession have proven to be inaccurate. Nevertheless, as can be noted by Fig. 8.2, UK growth performance has been fairly modest by historical standards.

UK gross domestic product, year-on-year growth (%). Source: ONS (2020)

There are four main factors which might explain this weak performance.

-

1.

Uncertainty, related to Brexit, has resulted in a proportion of investment being deferred or cancelled, whilst more cautious behaviour by consumers might magnify this initial effect.

-

2.

External factors adversely affecting the global economy, such as the US–China trade conflict, have been estimated to have reduced global GDP in 2020 by around 0.8% (IMF 2019: xiv). This will have had a dampening effect upon UK growth performance. In this, the UK has not been alone, with Germany being badly affected, due to its dependence upon export-driven growth. Indeed, it is worthy of note that the UK’s slowdown in growth rates, over the past two years, has mirrored developments in the Eurozone (IMF 2019: 10).

-

3.

The decade since the 2008 global financial crisis has produced amongst the worst growth performance in the last century (Weldon, 2019: 15–16). Not only did output fail to recover to the pre-crisis trend, but economic growth rates also declined relative to formerly normal trends (Blanchard et al. 2015: 15; Laeven and Valencia 2018: 23–4). In other words, most advanced economies have not caught up temporarily lost output potential in a post-recession boom, but rather, growth trends have been lowered as a result of the financial crisis. This may be due to credit constraints, frustrating investment recovery or more generally the result of a reluctance to invest, due to adverse economic conditions, resulting in a shortfall of capital stock and thereby slower rates of innovation and adoption of new technology (Chen et al. 2019: 8, 10–11).

-

4.

Domestic austerity policy has constrained UK growth performance over the past decade as depressed aggregate demand caused firms to delay planned investment (Wren-Lewis 2019: 45–6).

Given that the effects of all of these factors produce impacts similar to hypothesised Brexit effects, it is difficult to distinguish between different factors which may all affect economic growth. Moreover, the small number of data points, from which to draw evidence, has led one study, conducted by the Centre for European Reform, to adopt a different methodology to try to answer the question. Their approach has been to establish a ‘doppelgänger UK’ by means of measuring how the UK performed when compared to a basket of other countries which might arguably be considered to be similar in characteristics to the UK. The countries selected were Germany (32% of the weighting), the USA (28%), Australia (17%), Iceland (9%), Greece (6%), Luxembourg (4%) and New Zealand (4%). Using this approach, Springford (2019: 2) suggests that the “cost of Brexit”, due to the uncertainty created, is around 2.9% of GDP.

There are a number of problems with this type of analysis, some of which Springford acknowledges in his report.

Firstly, this is a small data sample, whilst quarterly measures of GDP are volatile and apt to subsequent revision. Thus, small ex post facto revisions to the data can have significant effects upon the results.

Secondly, the approach depends heavily upon the validity of the original choice of the pool of countries from which the comparator countries are selected, and this choice is, to some extent, subjective (Bouttellet et al. 2018: 676). Hence, the weightings, calculated by the synthetic control method, are only as accurate as the composition of this original selection of countries. There is a question mark, for example, over the inclusion of smaller OECD in Springford’s original pool of countries, from which the sample was selected, since the challenges they face are unlikely to be similar to a larger economy such as the UK. When deconstructing growth performance across the seven country sample, it is noticeable that the three smaller economies—Iceland, Luxembourg and New Zealand—all outperformed the rest of the sample and therefore may have arguably skewed the results.

Thirdly, the time period selected is subjective and may therefore influence the results. In this case, the focus of the analysis is upon divergence following the 2016 referendum. This is barely three years or 12 data points. The small time period is particularly problematic since it is well established that the business cycles between developed nations have different degrees of correlation, with the USA, Japan and Canada tending to have similar business cycle turning points, core EU member states having a slightly different and typically later pattern, whilst the UK is not particularly closely correlated with either group (Artis et al. 1997). As a result, a three-year time period is insufficient to demonstrate whether the observed effect is simply the effect of the UK being out of step with different business cycle timelines.

Fourthly, a study of this type will always suffer from missing variable bias, in that it ascribes the culmination of a multiplicity of different impacts, each result from numerous factors, to one single event, namely the vote for Brexit in the 2016 referendum. Yet, growth is impacted by much more than a Brexit-related uncertainty effect. It will be influenced by global trade patterns, fiscal and monetary policy, and so forth. Yet, in this study, the whole of the variance between UK and the counterfactual scenario is attributed to Brexit. This is, of course, untenable. A simple example makes the point. Using the same weighted group of countries, during the period 2016–2018 inclusive, the ‘doppelgänger’ counterfactual outperformed not only the UK but also the Eurozone and OECD average. Presumably, the analysis is not suggesting that Brexit had a detrimental effect upon the whole of the OECD or the Eurozone, and therefore, it is difficult to maintain that the variance between UK and ‘doppelgänger UK’ performance is necessarily solely or even largely due to Brexit-related uncertainty.

Finally, the synthetic control approach only works well if the country of interest (i.e. the UK) is a good fit to the sample as a whole and is not an outlier. It is particularly important that there are no shocks which may contaminate the analysis (Bouttellet et al. 2018: 676). Yet, this is the whole focus for the CEPanalysis—that is, testing the impact of the Brexit ‘shock’ on the UK economy.

Limitations in terms of the short time period following the 2016 referendum and the other factors which are likely to have had significant impact upon growth rates make it difficult to draw firm conclusions regarding the likely impact of Brexit-related uncertainty upon UK economic growth. What seems reasonable to conclude is that following a period of fiscal austerity, when UK growth performance was constrained by low rates of capital formation, and during a period of slowing global growth rates, UK growth rates were underwhelming. It seems probable that uncertainty played a part in this performance; however, the nature of the limited evidence currently available means that ascribing causality to one or more factors is unsafe.

Long-Standing Investment Performance

The 1971 White Paper, which sought to explain or justify the UK’s decision to apply for membership of the EU (then the European Economic Community or EEC), raised the possibility that free access for UK exporters to the larger marketplace, comprising all EU member states, would be likely to lead to an increase in investment, production and increased efficiency through the realisation of economies of scale (HMG 1971: 11, 13–14). This is essentially the same point that critics of Brexit have been making in reverse—namely, that leaving the EU would hard investment and productivity through reducing potential scale effects. The effect of uncertainty would, as per the previous discussion, potentially further weaken investment.

Unfortunately, for this narrative, the evidence would seem to indicate that this anticipated acceleration in UK productive investment did not occur. Instead, the UK consistently invests an average of around 2–3% of GDP less than its major competitors (France, Germany and the USA) in fixed capital, and has ranked in the bottom quartile of OECD countries for investment in 48 of the previous 55 years (HMG 2017b: 18). Combined public and private research and development (R&D) expenditure of 1.7% of GDP is similarly insufficient since this is less than the 2.4% OECD average and significantly lower than the economies of Japan, South Korea, Denmark, Finland and Israel, who each allocate in excess of 3% of their GDP to innovation and technological investment (HMG 2017b: 26). Given that the evidence indicates that public investment in R&D tends to encourage (‘crowd-in’) additional private sector R&D expenditure, there is a clear justification for greater policy intervention to promote greater innovation and technological advances in the UK (see Fig. 8.3). Former Secretary of State for Business, Energy and Industrial Strategy, Greg Clark, made the case for rectifying the poor R&D record, when he noted that without improving this record, the UK “cannot hope to keep, let alone extend, our technological lead in key sectors” (HMG 2017b: 5).

Research and development (R&D) intensity and government support to business R&D (as % GDP), 2013. Source: OECD (2019)

EU membership did not solve this long-standing investment weakness in the UK economy. Indeed, following accession, UK gross capital formation has steadily declined, from around 26% in 1973 to 17.3% in 2015 (see Fig. 8.4).Footnote 8 Thus, the UK invests less, as a share of its national income today, than it did when it joined the EU four decades previously (Business for Britain 2015: 722–3). Given the evidence presented in the previous chapter, that investment is one of the key determinants of economic growth and productivity, this long-term failure inherent within the UK economy will have significantly limited its growth potential. Moreover, this under-performance is even more manifest when comparing the UK record on investment with other nations. For example, one comparison, based on 2013 figures from the CIA World Factbook, ranked the UK only 140 out of 153 countries in terms of its share of GDP devoted to gross fixed investment.Footnote 9

Gross capital formation as % of GDP, selected countries, 1967–2018. Source: World Bank (2020)

This dismal investment record has occurred despite a sharp increase in inequality levels within the UK. As national income has shifted from wages to capital, orthodox economic theory would have anticipated that productive investment would have risen. Yet, the evidence suggests that lowering taxes upon entrepreneurs and capital holdings has not worked for the UK, as rising inequality has depressed, rather than boosted, economic growth (Chang 2010; OECD 2014).

None of this is to suggest that EU membershipper se was to blame for this fall in investment, as this had multiple causes. Nevertheless, it does demonstrate that the anticipation of the gains to be made by joining the EU have not materialised in the way that their advocates expected. This conclusion raises questions for those seeking to forecast the likely impact of Brexit and others whose focus is upon aiming to optimise the net benefits from UK withdrawal from the EU. If UK capital formation was inadequate during the period of EU membership, then maximising market access may be one element in encouraging productive investment, but by itself, it is clearly not sufficient. This insight will be discussed in more detail a little later in this chapter.

Designing Economic Policy for an Independent UK

The long-standing weakness in investment levels and capital formation can be addressed by a more active form of economic policy. This can additionally support the creation of a more favourable economic environment conducive for economic expansion, the rebuilding of parts of the industrial base, support for the creation of new products and new markets, utilisation of procurement and other levers to capture the potential arising from the economics of place, together with management of skills and labour force resources. A balance of macroeconomic and microeconomic policy would produce the best results since thee have the potential to compliment (hence reinforce) one another if designed correctly.

Short Run—Dealing with Uncertainty

The initial challenge, facing an independent UK, is to resolve the uncertainty which has surrounded the Brexit process. The act of withdrawal from the EU will have resolved part of this uncertainty, but negotiations between the UK and the EU will be ongoing throughout the transition period (scheduled to end on 31 December 2020), and uncertainty will remain until a final resolution has been enacted.

There are, however, a number of measures that the UK government could take to mitigate against continuing uncertainty. The first is to explain, in more detail, how their preferred variant of Brexit might work. If the preference is for a simple free trade agreement (FTA) with the EU, economic actors would benefit from understanding how this is likely to affect their businesses and their working lives. Whilst not all features could be outlined until any such agreement has been agreed by all parties, there is still a lot of information that could be disseminated. For example, exporters would benefit from having the maximum amount of time to evolve their systems to address the ‘rule of origin’ requirements which will form a part of any trade settlement excepting that of a customs union.

A second element is to provide a small stimulus package, of the type introduced by the Bank of England in the immediate aftermath of the 2016 referendum result, to boost aggregate demand and thereby provide more favourable conditions for firms to invest in new plant and technology. The macroeconomic stance of the government is particularly important in creating the parameters within which firms make investment decisions. If the economy can be stimulated to grow at or above trend, firms are more likely to invest as they believe they can sell their products. Indeed, it is the expectations held by business people of future profitability that predominantly determines present investment, whilst realised profits largely finance this new investment (Kalecki 1971; Arestis 1989: 614). Hence, if macroeconomic policy focuses upon promoting growth, it is more likely that investment will be forthcoming as business people will lose out if they fail to invest in new products, processes and technology, in order to take advantage of favourable market conditions. This latter policy stance is particularly important for that proportion of investment which is not financed through borrowing from financial institutions or through equity markets, but rather financed through retained earnings.

This effort could be supplemented by the introduction of a time-limited tax allowance focused upon boosting productive investment. The time limited nature of the scheme would encourage deferred investment plans to be enacted immediately, in order to take advantage of the opportunity, and the resulting boost to the economy would encourage additional output and investment thereafter.

Medium Term—Economic Regeneration

There are three elements to a medium-term redesign of economic policy, namely

-

i.

Macroeconomic management capable of facilitating economic regeneration, promoting economic growth and full employment.

-

ii.

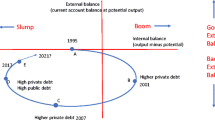

Competitive exchange rate management to offset any increase in trade costs with the EU, whilst facilitating a long-term objective of eliminating the current very large trade deficit and restoring trade balance.

-

iii.

Utilising the UK’s independent status to negotiate future trade agreements both with the EU and, perhaps more importantly in the long run, with a range of nations and/or trade blocs in the rest of the world whose rapid growth rates indicate their increasing importance in the marketplaces for UK goods and services in the future.

The rejuvenation and rebalancing of the UK economy will involve an active industrial strategy, but this will, in turn, depend upon government ensuring the maintenance of a sufficiently attractive economy in which economic activity is encouraged to take place. Unfortunately, this is where there is a weakness in much of the analysis that has been undertaken by supporters of Brexit because they tend to base their recommendations upon neo-classical foundations, thereby assuming that the economy will automatically tend towards the full employment of all resources, together with an optimistic reading of the efficient market hypothesis developed at the University of Chicago. On this basis, microeconomic interventions (such as deregulation) or fiscal incentives (such as cutting business taxation) are viewed as providing a sufficient set of incentives to economic actors to reinforce market solutions capable of achieving these goals. This is despite the fact that this approach has been tried repeatedly, over the past few decades, and it has not worked.

The alternative is to acknowledge that businesses produce and invest because they think they can sell their goods or services, rather than because labour or capital have become a little less expensive. Consequently, it is demand that drives the economy, not supply. It is the responsibility of government to management the level of aggregate demand in the economy, to ensure that there is a sufficient level to facilitate the full employment of resources, to encourage business investment and to ensure a decent level of economic growth. Aggregate demand impacts directly upon the real economy because it influences, and in turn is influenced by, the rate of investment, which changes the stock of capital and thereby affects productive capacity and employment (Rowthorn 1995, 1999; Alexiou and Pitelis 2003: 628). Moreover, a larger capital stock will permit a higher level of aggregate demand, and hence both higher output and employment, without resulting in an increase in inflation.

This approach emphasises the importance of public investment in infrastructure because of the impact this has upon the efficiency and productivity of UK firms, thereby increasing their international competitiveness. It ‘crowds in’ private investment as firms in the private sector pick up these contracts and expand their operations, thereby increasing their ability and desire to employ more workers and invest greater sums in new machinery and new technology (Aschauer 1990). The importance of infrastructural spending has been recognised by government (HM Treasury 2016). However, there is not yet a clear recognition, by HM Treasury, of the crucial role of aggregate demand as the driver of the economy. Instead, infrastructural spending is viewed rather in isolation, as a stand-alone economic instrument rather than as an integrated overall economic approach. This needs to change if the UK is to create the high growth macroeconomic framework within which firms wish to expand, entrepreneurs wish to invest and consumers wish to continue to spend. In short, macroeconomic policy requires a Keynesian foundation to be truly effective.

Secondly, over the medium term, the depreciation of sterling is likely to boost UK exports whilst reducing the level of imports and/or encouraging import substitution, thereby providing a secondary boost to domestic producers. The economics literature indicates that periods of competitive (or undervalued) exchange rates can have significant positive effects upon those industrial sectors that have significant growth potential (Rodrik 2008). Indeed, there is evidence that exchange rate undervaluation lay behind the rapid increase in the growth rates of European economies up until the 1970s, whereas subsequent revaluation and tighter macroeconomic stance has slowed this pace of development (Perraton 2014: 12). Thus, exchange rate management would appear to be an effective macroeconomic management tool. Data for 2009, drawn from OECD-WTO TiVA datasets, suggest that UK exports are price elastic, which indicates that a change in price will have a proportionately greater impact upon the quantity of that good or service demanded. In this instance, the estimate was made that a 10% change in the price of UK export prices would likely lead to a change in exports volumes of between 15% and 25% (Driver 2014: 7).

The utilisation of this policy tool is, however, circumscribed by two factors. The first is that the weakness of the UK manufacturing sector, in terms of its low international comparative ranking in per capita terms (behind Iceland and Luxembourg), suggests that it might struggle to take full advantage of an increase in international competitiveness (Chang et al. 2013). Moreover, the UK’s success in attracting foreign direct investment (FDI) and foreign ownership of a sizeable share of the industrial base may limit the effectiveness of devaluation if these owners preferred to reap increased profits rather than allow currency depreciation from reducing export prices, for fear that this would mean their UK production undercutting their other production facilities elsewhere in the world. Thus, whilst currency management is likely to play a significant role in a post-Brexit macroeconomic strategy, it is likely to be less effective in the absence of complementary measures aimed at regenerating UK manufacturing industry.

Thirdly and finally, Brexit provides the UK with the opportunity to explore alternative trade relationships with both EU member states and, more importantly in the long run, faster-growing nations elsewhere in the world. The UK will be free to negotiate its own preferential trade deals with whomever it chooses. This could be with former close trading partners in the Commonwealth and would most likely also embrace the establishment of closer economic ties with the USA. Those few studies which have sought to capture the potential for such FTAs have indicated only limited benefits. However, this analysis inevitably draws upon data relating to current trading patterns, supply chains and existing product ranges. To maximise full advantage of the trade opportunities available to an independent UK, exporters will need to be encouraged to actively seek out new opportunities outside the European regional bloc, whilst new industries, markets and product ranges will need to be developed to augment existing exports in order to reduce the UK’s trade deficit. There is no need for this process to be unduly rushed, and nor is there a requirement for the UK to capitulate in negotiations relating to the stated positions of other nations when discussing potential future FTAs. In any case, the net benefit derived from non-EU trade surpluses is likely to rise over time, as faster growth rates outside Europe lead to higher demand for UK products—the precise relationship depending upon the elasticity of the goods and services exported.

Microeconomic Policy

The macroeconomic policy framework to be set by the UK government following Brexit will be of considerable importance in determining the ultimate success or failure of the decision, taken by the British electorate, for the country to pursue independent economic development. However, microeconomic policy will be no less significant in dealing with challenges that Brexit will entail for specific sectors of the economy. Given that the UK economy has a very large trade deficit, particularly with our EU neighbours, and the economy relies too heavily upon finance and the professional services rather than manufacturing industry to restore trading balance, then industrialpolicy can play an important role in restoring greater balance to the economy. Rodrik (2006: 986) argues that “more selective, and more carefully targeted policy initiatives … can have very powerful effects on igniting economic growth in the short run”. Thus, microeconomic policy can have a significant effect upon post-Brexit economic development.

Industrial Policy

Industrial policy is intended to resolve market imperfections and thereby enhance the efficiency of the productive sector (Greenwald and Stiglitz 2012). There are two types of industrial policy. ‘Vertical’ or selective industrial policy seeks to combine planning support for industry, with state investment, infrastructural projects. Policy interventions are targeted at specific firms or sectors, to enhance their efficiency and ultimately secure international competitive advantage, and hence, this has often been characterised by critics as governments attempting to ‘pick winners’ to create ‘national champions’ (Cohen, 2007) or in ‘choosing races and placing bets’ (Hughes 2012). By contrast, ‘horizontal’ industrial policies are more general and passive in nature, focusing upon reducing constraints to the operation of market forces and the creation of a low tax, low regulation business environment. Horizontal policy could additionally include investment in education and infrastructure, as this benefits the economy in general.

There are, of course, difficulties in maintaining this distinction between vertical and horizontal forms of industrial policy, as any intervention will inevitably disproportionately benefit one firm or industry. Thus, a decision to expand technical education may form part of a horizontal skills policy, yet it will benefit engineering and IT sectors more than agriculture or large parts of the service sector. Similarly, the decision to extend the railway network in the north of England, through the so-called ‘Northern Powerhouse’ programme, will disproportionately benefit those industrial clusters which are spatially connected to this new infrastructure. Moreover, there is a further weakness with the horizontal approach, in that, because this disproportionate benefit occurs as a by-product of the intervention; rather than through its specific design, it becomes more difficult to monitor the effectiveness of the measure(s) and to prevent ‘leakages’, thereby potentially reducing the effectiveness of the intervention (Chang 2009: 13–15).

Industrial policy can be viewed narrowly or more comprehensively. For example, corporate governance and financial market structures are not typically incorporated within discussions of industrial policy, yet impatient finance and governance structures—overly concerned with short-term movements in stock market prices, takeover threats and portfolio diversification to minimise risk—tend to result in short-termism in investment decisions (Kay 2012; Crafts and Hughes 2013). Initiatives to deliver more patient forms of finance are, however, firmly within the remit of a more active form of industrial policy (HMG 2017a: 177). Similarly, the enhancement of business networks, often crucial to realise the agglomeration effects arising from clusters of specialised firms operating within a given locality, does not fit easily within the definitions of either vertical or horizontal forms of industrial policy. Nevertheless, the expectation is that networks will generate positive spillovers, whether through the creation of a labour force specialising in the skills and knowledge required by the sector in question or through innovation that emerges through a combination of collaboration and competition (Chinitz 1961; Porter 1998: 78). Consequently, the creation of networks may be categorised as a third type of industrial strategy.

Industrial policy can be justified, in economic theory, on a number of counts. Firstly, can facilitate the efficient development of supply chains by encouraging those industries which are interdependent (hence complimentary) with other sectors of the industrial base (Rosenstein-Rodan 1943; Hidalgo and Hausmann 2009). Secondly, industrial policy may assist the slow and costly process of accumulating productive capacity (Lall 2001). The desire to protect infant industries until they have sufficiently developed these capabilities is one example of this approach. However, so is the ‘industrial commons’ argument, which notes the interdependent processes of learning and production which spill over across the industrial base, and in this way, encouraging the development of certain key sectors will strengthen the potential of others (Abramovitz 1986; Laranja et al., 2008). A third set of arguments identifies capital market failure in providing sufficient long-term funding for technologically advanced and innovative areas of production, due to their inherent uncertainty and risk profiles (Jäntti and Vartiainen 2009). Finally, industrial policy can facilitate technology transfer by enhancing the “absorptive capacity” of the economy, through skills enhancement, improving management quality and raising levels of R&D expenditure (Crafts 2018: 692).

There are a number of criticisms which are likely to be levied at the introduction of a more active industrial policy. Firstly, there is the suggestion that state investment ‘crowds out’ private investment. This is based upon the neo-classical theory of the market for money, whereby there is a finite amount of funds available, at the prevailing equilibrium rate of interest, to be borrowed to invest in productive activities as well as less productive forms of assets. If this theoretical construct is accepted, and similarly if the economy is operating at full employment, then any public sector borrowing to invest it in UK businesses will either increase demand relative to the supply of funds, thereby increasing the interest rate paid by all borrowers and thereby making investment less profitable, or else it will substitute public for private borrowing. In either case, the result would be less beneficial than adherents of industrial policy would claim. If the further assumption is added, that private investment is always superior to public investment, then it would be unlikely that state investment will produce beneficial effects that would exceed these predicted costs.

The problem with this critique is that the theory on which it is founded is fundamentally flawed. Whereas money markets might have once resembled the neo-classical characterisation in the early days of capitalism, the reality in the twenty-first century is that most investment occurs through a combination of retained earnings and bank credit (Kalecki 1971). There is not a finite amount of credit, but rather, banks can create money based (sometimes rather loosely) upon their deposits and other assets. Consequently, there is no a priori reason for crowding out to necessarily occur. Moreover, to do so, neo-classical theory requires the economy to be operating at full capacity, so there are not underutilised or unused assets that could be seamlessly employed. The theory achieves this through the simplifying assumption of ‘Say’s Law’, which holds that supply creates its own demand, which, in turn, implies that the economy will always be automatically self-correcting towards the full employment of all resources. There can, under this assumption, never be a situation where demand deficiency persists, and both capital and workers remain idle. Yet, any cursory perusal of economic history will demonstrate the fragility of this assumption. The economy is often away from its equilibrium position for long periods of time. Indeed, so much so that many have suggested that the concept of equilibrium itself is a theoretical abstraction from reality. However, the pertinent point for this discussion is that crowding out does not occur if the economy is operating at less than full employment; in circumstances of less than full employment, public investment can often ‘crowd in’ further private sector investment. Moreover, since an essential part of the intention of industrial policy is to actively shape markets, to enhance their future productive potential, then crowding-out arguments are less tenable (Mazzucato and Penna 2014: 27).

A second criticism is that by operating selective measures favouring one firm or industry over another, industrial policy weakens competition policy (Irwin 2015: 17). However, if the free operation of market forces has not been sufficient to deliver the UK sufficient industrial capacity, with future high growth potential, sufficient to eliminate its current large trade deficit, then there would appear to be an a priori justification for considering this type of intervention.

A third critique focuses upon the potential for indigenous firms to ‘capture’ rents from the UK government (Rodrik 2004: 1, 17; HOL 2018: 48). This would represent a Pareto inefficient use of resources. Of course, Pareto efficiency only really exists in a textbook and therefore trade-offs are likely to exist when seeking to achieve economic objectives. It is, for example, quite plausible to anticipate that certain strategically important firms, such as Nissan or Vauxhall, may press for government assistance to mitigate any Brexit-related disruption and ensure the viability of their longer-term operations in the UK. Whilst Crafts (2017: 318) might consider this possibility to be “unedifying”, there is a strong argument in favour of using a more active form of industrial policy to secure strategic objectives, if this creates greater benefits for the economy than the cost of any such assistance. It is often necessary, when designing economic policy interventions to deal with real-world problems, not to sacrifice a realisable second-best outcome by chasing after an unrealisable textbook optimum solution. Moreover, the threat of regulatory capture would be reduced if industrial policy measures were time-limited, to prevent the entrenchment of vested interests, together with a rigorous monitoring and policing of the various initiatives. Democratic accountability and transparency could help to prevent the abuse of policy intervention measures.

A fourth criticism is that industrial policy does not work because the state is incapable of ‘picking winners’. Presumably, those who advocate this position also hold that venture capital funds, and the financial markets more generally, are presupposed to have a monopoly of insight into future market conditions and the growth potential of each and every individual firm and productive sector (Baldwin 1969). This viewpoint is largely based upon a vague understanding of the ‘efficient market hypothesis’ (Farma 1970). Contrary to popular belief, this theory does not state that markets are always and everywhere efficient and do not exhibit excessive volatility, but rather that even if they should do so, predictions of future movements in securities prices are a random walk and hence, on average, no investor can make consistently greater returns than another. Yet, the rather limited scope of the original theory has been taken by policy makers and some economists (who perhaps should read the original texts) to imply market superiority.

The fact that industrial policy may occasionally fail in its choice of investments does not undermine the need for the state to undertake this role if the private sector is unable or unwilling to nurture these developments. Venture capitalists often fail in their investment selections, but they are judged not on individual interventions, but rather upon the balance of their entire portfolio. State investments should be similarly assessed on the same basis, so the inevitable losses sustained in certain businesses are likely to be more than offset by the successes in other ventures (Mazzucato and Penna 2014: 23–4). If governments make no mistakes when operating an active industrial policy, it implies that they are not trying sufficiently hard (Rodrik 2004: 25).

There are plenty of examples that can be given where vertical industrial policy has assisted in the development of international competitive industries—whether car production in Japan or steel in South Korea—because the state had the long-term vision often lacking in financial markets more focused upon short-term gains (Chang 2002).Footnote 10 Nations which have utilised active forms of industrial policy have included Japan, South Korea, Taiwan, Singapore, France, Finland, Norway, Austria, Germany, Italy and, more recently, China. Moreover, the UK was only the first amongst multiple nations (including Germany) which pursued what would now be described as an infant industry programme, where the development of selected industries was protected by high tariffs; the UK’s later championing of free trade allowed these same (now mature) industries to realise their competitive advantage (Chang 2009: 10).

This list could additionally include the USA since the state financed between half and two-thirds of national R&D expenditure between the 1950s and 1980s, principally in the fields of defence-aerospace and healthcare, and it is in many of these areas where the USA subsequently established a technological lead (Chang 2009: 2–8). Indeed, the USA is a good example of how government has the ability to create a direction for technological change, and by investing according to this vision, new firms and new markets will be created (McFadden and Tarrant 2015: 5). Many of the most prominent recent examples of product innovation, including pharmaceuticals, renewable energy and personal electronics such as the iPod, iPad and battery technology, depended upon foundations created by publically funded research (Mazzucato 2013). The fact that the USA funds and organises this level of innovation and technological support through a multitude of channels, rather than through a single, and hence more visible, industrial strategy, has resulted in the USA being described as a “hidden development state” (Block 2008: 2).

The economics literature has not, unfortunately, produced a clear consensus upon the effectiveness of different modes of industrial policy. There have, for example, been a number of studies which have concluded that vertical policy fails to deliver its intended increase in productivity (Krueger and Tuncer 1982; Lee 1996). Yet, these studies typically suffer from problems of omitted variable bias and difficulties in interpretation of causality. For example, if a study records a negative association between intervention and industrial performance, does this indicate that industrial strategy has had negative effects upon the industry or alternatively that the problems of the industry were so intractable that a more sizeable state intervention was necessitated to try and solve deep-set problems? Moreover, other econometric studies indicate that total factor productivity is higher in those nations which adopt an import-substitution form of industrial policy rather than a market-orientated alternative although, again, it is difficult to assign causality (Bosworth and Collins 2003). Hence, there is no persuasive body of evidence which can point conclusively to whether one form or another of industrial policy produces superior or inferior economic outcomes (Rodrik 2006: 9–10).

The historical record is a little clearer when considering the effectiveness of industrial strategies in aggregate as those economies which have utilised active industrial policy outperformed other large OECD economies between 1950 and 1987 (Chang 2009: 7–8). This might help to explain why there has been a significant increase of interest in a more active industrial policy proving indispensable to national economic development (Lin and Monga 2010).

Industrial Policy Within the EU

The EU initially pursued a vertical form of industrial policy, seeking to develop a set of European businesses capable of competing with US trans-national corporations (TNCs). However, during the past two decades, policy has shifted towards a horizontal approach. Indeed, to illustrate the extensiveness of this shift in approach, the former European Commissioner in charge of competition policy, Kroes, argued that concerns over retaining national control over what are regarded to be ‘strategic assets’ is “outdated—the language and the mindset are those of yesterday’s people, not of these who have the guts to look forward with ambitious realism”—a viewpoint dismissed as “contrary to the spirit and the letter of the laws underpinning the EuropeanUnion” (Kroes 2006: 3). Vertical industrial policy was, furthermore, rejected by Kroes (2006: 4,6) on the grounds that it would result in decreasing competitiveness, whilst state aid was decried as crowding out private sector investment.

The advent of the single internal market (SIM) further reinforced this shift in approach as the Commission held that national promotion of domestic industry was discriminatory and therefore not consistent with competition rules. Vertical industrial policy would, by definition, give preference to, or advantage for, domestic products vis-à-vis those produced elsewhere in the EU (Kennedy 2011: 47–8; Barnard 2016: 82–4). Whilst these restrictions upon industrial policy initially focused upon goods, a combination of the approach taken by the Commission and decisions of the European Court of Justice gradually extended these constraints to include services and issues related to tax (Reynolds and Webber 2019). This additionally includes the use of ‘buy British’, ‘buy Irish’ and even ‘buy local’ campaigns, due to concerns over unfair competition within the SIM. Yet, by doing so, this frustrates using ‘buy local’ campaigns to reduce food miles and thereby benefit the environment. Similarly, European Court rulings prevent national or regional rules requiring electricity suppliers to purchase specific quantities of renewable energy from their local region (Barnard 2016: 83), despite this frustrating the establishment of local energy generation, which many experts suggest can be produced at lower levels of energy lost through transmission grids, with resultant cost and emissions advantages (Armstrong 2015).Footnote 11

Public authorities are required to make public procurement tender details widely available across the EU and may not discriminate against any firm because it is registered or located in a different EU country.Footnote 12 The intention is to create a ‘level playing field’ for firms across the EU to bid for tenders that, in aggregate, approximate to 14% of EU GDP per annum.Footnote 13 However, this constrains the ability for public procurement to be used to establish a core market for local producers, to meet developmental or environmental objectives. It could, for example, introduce a preference for local produce to reduce food miles and raise nutritional food provision for public services (i.e. hospitals, schools, retirement homes and prisons) or to help to establish a market for local renewable energy. Similarly, it could facilitate the expansion of the UK engineering industry by ensuring that local producers receive part of the increased demand arising from the Northern Powerhouse public investment intended to renew transportation links in the north of England. In the absence of the greater industrial policy flexibility which will arise post-Brexit, comments from Sir Andrew Cook, Chairperson of William Cook Rail (a large engineering employer in South and West Yorkshire), would suggest that this opportunity is currently being squandered.Footnote 14

A third area where the EU restricts industrial policy relates to its rules relating to state aid. This may be defined as where public assistance is provided on a selective basis to a firm or group of firms either directly by public authorities or via an instrument over which the state has significant control (BIS, 2015: 4–5). This would include not only subsidies and tax credits funded through the national budget but also assistance from regional or local government, public guarantees, state holdings or all or part of a company, the provision of goods and/or services on preferential terms, and funding provided via quasi-public bodies such as the National Lottery.Footnote 15 If this assistance has any effect, it will strengthen the firm or firms targeted by the measure, and will therefore be deemed as distorting competition and fall foul of EU SIM competition laws.

There are exceptions to this rule. The first relates to the provision of very small amounts of assistance (de minimis rule), where each business receives less than €200,000 over three years; lesser sums apply in the agricultural (€15,000) and road transport (€100,000) sectors (Jozepa 2018: 4). A second set of exemptions fall under the category of ‘General Block Exemption Regulation’. These include development assistance for disadvantaged regions of the EU, infrastructure funding, environmental protection, cultural and heritage conservation, aid to facilitate recovery from natural disasters, employment and training for disabled or disadvantaged workers, provision of assistance for small and medium-sized enterprises (SMEs) and innovation funding to facilitate R&D through, for example, helping with patent costs (Jozepa 2018: 9–10).Footnote 16 Each of these categories has its own rules and ceilings placed upon the maximum amount of permitted state aid (BIS, 2015: 9). Moreover, these exemptions only apply when assistance is provided to any and all eligible firms from across the EU, irrespective of their nationality of ownership, where their headquarters are located and even, perhaps surprisingly, whether they have any current operations within the country offering the aid. It is, however, permissible to restrict assistance to those firms that have some form of operations within the national boundary of the government offering the assistance at the time that the assistance is provided (EC 2016: point 7).

It is a fair point to note that the UK has chosen not to utilise its flexibility within these exemptions to operate a more active form of industrial policy (HOL 2018: 44). For example, in 2016, the UK allocated only 0.36% of its GDP to state aid (excluding railways), compared to 0.65% in France and 1.31% in Germany (Jozepa 2018: 4). Hence, the limited forms of industrial policy that are permitted by the EU could have been pursued more vigorously (Crafts 2017: 317). Nevertheless, EU rules necessarily limit the potential for the full range of options available to a more active form of industrial policy. Instead, the EU has placed greater emphasis upon regional (EU-wide) competitiveness, utilising measures to encourage the development of SMEs and the knowledge economy (Bartlett 2014: 4–5). This was latterly extended, through provisions established in the Lisbon Treaty, to provide elements of sector-specific support (EC 2010; Uvalik 2014: 2–3). The stated goal was to support the growth of the EU’s industrial sector to approximately one-fifth of EU GDP by 2020 (Pellegrin et al. 2015: 10).

The Potential for Industrial Policy Following Brexit

Brexit offers the potential to operate a more active industrial policy unhindered by SIM competition and state aid rules. For those critical of the Brexit project, industrial strategy will be “a necessity” to prevent unnecessary harm to the UK industrial base (Jones 2016: 827). To those less antagonistic towards Brexit, industrial policy offers the opportunity to transform the fortunes of UK manufacturing and achieve a rebalancing of the economy otherwise difficult to achieve within the strictures of EU rules and regulations (Whyman 2018: 5,8,16). Whereas the current UK industrial strategy has been developed within the existing constraints imposed by EU membership, and as a result is rather limited in a number of key respects (Crafts 2017: 317, 319), the potential for industrial strategy to form a central pillar of economic strategy post-Brexit has been recognised by government and opposition parties (Conservative Party 2017: 12–13; HMG 2017a: 11, 15–16, 20, 212–3; HMG 2017b: 13, 62–4; Industrial Strategy Commission 2017: 10, 12; Labour Party 2019: 12–3, 16–18).

WTO Rules and Industrial Policy

Withdrawal from the EU does not mean that there are noconstraints remaining upon the use of industrial policy measures. The UK remains a member of the WTO and hence must follow its rules which are contained in the Agreement on Subsidies and Countervailing Measures (ASCM).Footnote 17 Crucially, however, these restrictions are not as comprehensive and “intrusive” as the EU regime (HOL 2018: 47–8, 53).

The WTO approach, for example, allows the use of public subsidies unless these are focused upon export activity or import substitution (Article 3 of the ASCM), or unless another country can prove that these measures are damaging their domestic industries and/or their trade in general (Articles 5 and 6) (Jozepa 2018: 16–17). Whereas the default EU position is to prohibit such subsidies in advance of their introduction, and businesses have to repay any aid which is found to breach EU rules, the WTO merely requires the withdrawal of any measure found to breach the ASCM, without any similar requirement for recipients to repay any assistance received prior to any judgement (HOL 2018: 47). Moreover, the WTO can accept retention of subsidies, even if found to have convened its own rules, but allow the aggrieved party to introduce a countervailing tax to offset and competitive advantage secured via the subsidy (Jozepa 2018: 17).

There are other significant differences between the EU and WTO approaches. Whereas WTO rules apply only to goods, EU rules apply to all economic activities including services (HOL 2018: 47; Jozepa 2018: 5, 17). WTO rules only apply to trade-related activities, whereas EU rules apply indiscriminately to all economic activity occurring within the UK economy, whether or not this was intended for purely domestic use and consumption or for export (HOL 2018: 48). WTO rules are reactive, depending upon a complaint being made by a signatory nation before investigation takes place, whilst EU rules are applied prospectively and do not require a formal complaint before action is taken (Jozepa 2018: 17). In addition, under the EU system, individuals and companies can lodge complaints to the Commission or through domestic courts, whereas the WTO approach is based upon dispute settlement between state actors (UKCE 2018: 8).

WTO rules generally prohibit local content requirements (Article III:4 of the GATT [General Agreement on Tariffs and Trade] 1994; Article 2.1 of the Technical Barriers to Trade Agreement; 3.1(b) of the ASCM). However, local preference is permitted in public procurement and when adopting policies aimed at avoiding environmental problems (EC 2017; Rubini 2004: 152). Similarly, subsidies can be used where they seek the protection of public health and/or public morals, the environment and the conservation of natural resources (Bohanes, 2015: 3). Non-discriminatory measures, such as labelling standards or strict hygiene requirements, would not breach WTO rules, despite their potentially having a disproportionate benefit to certain domestic industries. Industrial policy measures could be used, under WTO rules, to promote regional regeneration, the restructuring of certain industrial sectors particularly responding to changes in trade and economic policies such as presumably the impact of Brexit, encouraging R&D especially in high-techindustries, assisting the development of infant industries, introducing local preference in public procurement and when avoiding environmental problems (Rubini 2004: 152).

The degree of policy flexibility for the UK, if operating under WTO rather than EU rules, is therefore quite significant. It broadens the scope of what is a permissible use of industrial policy rather considerably which is potentially very valuable for an independent UK, seeking to rebalance its economy through rejuvenating its manufacturing industry, seeking to encourage higher rates of investment and innovation, and ensuring that any resultant economic growth is spread more evenly across the whole nation.

What Might an Active Post-Brexit Industrial Policy Look Like?

There is no reason why an industrial strategy, designed to meet the persistent weaknesses in the UK’s economic model and the particular challenges and opportunities presented by Brexit, needs to follow approaches adopted by other nations. However, there are a number of features that can be highlighted in other successful examples of industrial strategy which might inform a UK scheme.

The first element concerns the necessity for a “national vision” around which to frame the development of an industrial policy (Chang et al. 2013: 46–7). If the UK, following withdrawal from the EU, commits itself to the goal of transforming the UK economy, to deliver higher productivity and more inclusive growth, then it is much easier to achieve broad support for the principles of the industrial strategy and its policy initiatives.

A second aspect concerns the ability to coordinate activity through “thick” networks (Chang et al. 2013: 48). Certain nations utilised indicative planning to perform this function (France, Japan and Korea), whilst others adopted corporatist approaches (Finland), utilised workers councils (Germany) or specially established deliberation councils (Japan and Korea). These networks facilitate communication and coordination, which in turn both informs and facilitates the enactment of industrial policy initiatives. Coordination additionally requires the ability to coordinate across government departments, and this leadership role has been undertaken successfully by the Ministry of International Trade and Industry in Japan, the Planning Commission in France and the Economic Planning Board in Korea. The Department for Business, Energy and Industrial Strategy could perform this leadership function in the UK, but it may find the task of coordination more difficult in the absence of a well-established range of intermediate institutions or “industrial commons” (Abramovitz 1986) who are able to fully engage with the development and implementation of the industrial strategy.

The third element that typically forms a foundation of industrial policy programmes concerns the provision of affordable, patient investment finance. Japan ensured this through the Long-Term Credit Bank of Japan and the Industrial Bank of Japan, Korea through state-owned banks, whilst Finland utilised public savings, which at their peak comprised almost one-third of total domestic savings, to support productive investment (Chang et al. 2013). Given their provision of lower cost credit and financial services to businesses not adequately served by the private sector financial institutions, state investment banks have the ability to support capital development more generally and potentially enhance countercyclical macroeconomic policy in the process (Mazzucato and Penna 2014: 4–5). The current state-owned British Business Bank could develop into fulfilling this more strategic role, possibly along the lines of the German Kreditanstalt für Wiederaufbau, which both fulfils the role of a national state investment bank whilst simultaneously provides funding to regional state investment banks in Germany.Footnote 18 Previous proposals have been made along these lines in the UK (Dolphin and Nash 2012).Footnote 19 However, they have not, as yet, been implemented.

The provision of patient finance for productive investment is a necessary but not sufficient feature of industrial strategies. It is typically complemented by financial regulation aimed at rationing credit consumer credit and thereby steering resources towards the productive sector (Korea). Forced savings schemes have also been utilised as a means to generate and then steer funding towards productive investment (Singapore), whilst similar approaches have also been utilised through the development of public sector savings surpluses (Finland and Sweden).

The provision of patient capital to fund productive investment has implications for corporate governance. If this is subject to overt short-termism, the industrial policy objectives of rebuilding the UK’s industrial base will falter. In other countries, firms have been partially insulated from short-term pressures through cross-shareholding (Japan) or codetermination (Germany) (Chang et al. 2013: 50). Whatever the approach, in order to ensure that this active industrial policy is sustainable, it is important to ensure that public and private stakeholders have a “symbiotic” rather than “parasitic” relationship (Mazzucato 2013: 30). Too often state support for innovation in the private sector combines the socialisation of risk with the privatisation of gains, which is precisely the flawed balance of costs and benefits that underpinned the irrational exuberance and excessive risk taking by the financial institutions, thus precipitating the 2008 globalfinancial crisis (Mazzucato 2013: 34, 203).

A true partnership requires a means of sharing both the costs and the benefits derived from the initial public investment. This could involve the state taking a stake in the enterprise, thereby receiving a share of the rewards arising from the development of products drawing upon this publically funded invention or innovation. In addition, active industrial policy could additionally include the re-institution of a public interest test for takeovers, thereby preventing the foreign takeover of strategic industries. A variant of this approach could involve the state acquiring a ‘golden share’ in certain sectors to prevent outcomes that might prove undesirable to the economy as a whole, such as the relocation of the headquarters, or R&D functions, offshore.