Abstract

This study presents a model in which heterogenous, risk-averse agents can use either (legal) tax optimisation or (illegal) tax evasion to reduce their tax burden and thus increase their utility. In addition to introducing individual variables like risk aversion or income, we allow agents to observe the behaviour of their neighbours. Depending on the behaviour of their peer group’s members, the agents’ utilities may increase or decrease, respectively. Simulation results show that taxpayers favour illegal evasion over legal optimisation in most cases. We find that interactions between taxpayers and their social networks have a deep impact on aggregate behaviour. Parameter changes such as increasing audit rates affect the results, often being intensified by social interactions. The effect of such changes varies depending on whether or not a fraction of agents is considered inherently honest.

Access provided by Autonomous University of Puebla. Download conference paper PDF

Similar content being viewed by others

Keywords

1 Introduction

Empirical findings suggest that taxpayers’ behaviour deviates from the predictions of analytical models (e.g., [4]). Some authors put forward psychological motives to account for the difference between theory and empirics. Erard/Feinstein, for example, consider that taxpayers experience guilt when evading taxes and shame when caught by the fiscal authorities [5]. Bernasconi suspects that taxpayers only overestimate the probability of audit [3]. Further studies propose non-psychological reasons. Conducting a laboratory experiment in which tax reports are selected for audit based on the individual deviation from the average reported amount, Alm/McKee claim that taxpayers report too honestly because they fail to coordinate on a zero-compliance Nash equilibrium [2].

In recent years, agent-based modelling has become an important area of tax evasion research, allowing for incorporating realistic assumptions concerning individuals’ heterogeneity when it comes to risk aversion, behavioural norms, social network interactions, etc. The possibility of reducing the tax burden legally has not been taken into account by this new stream of literature, however.

We therefore impose a social network that exhibits characteristics close to the small-world network, proposed by Watts/Strogatz [9]. Following Fortin/Lacroix/Villeval, we assume that agents receive (and consider in their calculus) social utility [6]. In line with recent experimental results [7] we assume that agents receive positive social utility when acting in the same way their neighbourhood does, while they receive social disutility when their behaviour differs from their environment. In Sect. 2 we develop an analytical model that captures both illegal evasion and legal optimisation. We then extend our model to incorporate network effects. In Sect. 3 we show and discuss the results of an agent-based simulation, while in Sect. 4 the paper concludes with a summary.

2 Model

2.1 Tax Law and Legal Tax Avoidance

It is possible to legally reduce one’s tax burden to some extent, either by exploiting tax loopholes or by searching for special regulations This search is associated with some cost h modelled as a fraction of pre-tax income. We assume that the government is able to control the expected tax savings by either simplifying the tax code or adopting new provisions to close tax loopholes: the higher (lower) the tax complexity, the lower (higher) the expected tax savings.

We use an exponential distribution to model legal uncertainty. Opting for legal avoidance is modelled as drawing a random number θ from a probability density function f featuring positive support over [0, ∞]. θ is interpreted as the share of the original tax liability that can be avoided due to tax optimisation. As the exponential distribution doesn’t allow for negative values of θ, tax optimisation cannot lead to a tax liability higher than the original. Values of θ > 1 are possible, meaning that sometimes tax optimisation can even cause a negative tax payment.

The probability density function of the exponential distribution is given by

γ is interpreted as a complexity parameter that can be adjusted by the government. Mean and variance of the exponential distribution are given by \(\frac {1}{\gamma }\) and \(\frac {1}{\gamma ^2}\), respectively. As explained above, a higher complexity parameter γ gives less space for tax optimisation and thus results in lower expected tax savings—the tax code is more resistant towards tax optimisation. Variance also decreases with increasing complexity, which means that the tax code is rather vague if it is simple, whereas with increasing sophistication it becomes more certain. We interpret certainty as predictability of legal decisions. If there are a large number of legal norms—i.e., if the tax code is very complex—the outcome of optimisation activities is fairly predictable. By contrast, if the tax code is worded in very abstract terms, greater optimisation is possible but uncertain. This seems plausible since we consider tax optimisation to be an option chosen by professionals whom we assume to have good legal skills. In other words, an uncertain outcome is only possible if no specific norm exists. Otherwise the professional will be bound to the law and thus produce small and predictable tax savings.

2.2 Taxpayers’ Optimisation Problem

We assume that taxpayers can choose between three distinct strategies:

Legal Tax Optimisation

Taxpayers can try to legally avoid taxes by exploiting tax loopholes. The intensity of searching for legal tax-saving options is denoted by tax planning effort ζ o. That is, only fraction ζ o of the original tax payment τ is subject to uncertain tax savings as described in Sect. 2.1. Choosing ζ o can also be interpreted as choosing the number (fraction) of categories of income that will be subject to tax planning. Neglecting the possibility of tax consulting fees being deductible, choosing tax planning effort ζ o results in consumption

Illegal Tax Evasion

We model illegal tax evasion as suggested by [1]. Evading taxes illegally requires no ex ante payment and reduces the tax liability by τζ eW i where ζ e is the fraction of evaded taxes. The tax authorities detect tax evasion with probability p. In case of detection, a penalty tζ eW i is due, with t ≥ τ. Illegal tax evasion delivers consumption

in case of detection (l, “lose”) or no detection (w, “win”), respectively.

“Honest” Behaviour

Finally, taxpayers can decide to refrain from any legal or illegal avoidance activities and just pay their full taxes due. Setting any effort to reduce the tax burden ζ h = 0, this results in consumption

Since we will include social effects of tax avoidance below, the direct payment effects are referred to as “private expected utility”, denoted by the vector PEU. Thus, the taxpayer’s problem can be written as

where \(\mathbf {d} = \begin {pmatrix} d_o & d_e & d_h \end {pmatrix},d_s\in \{0,1\}\forall s=o,e,h,\|\mathbf {d}\|{ }_1=1\) is a vector of binary decision variables, \(\pmb {\zeta } = \begin {pmatrix} \zeta _o & \zeta _e & \zeta _h \end {pmatrix}^T,\zeta _{s}\in \left [0,1\right ]\forall s=o,e,h\) is a vector of effort levels and PEU denotes the vector of the three strategies’ respective expected utilities, depending on the choice of effort ζ:

u[⋅] is a concave utility function that satisfies the von Neumann-Morgenstern axioms. To receive explicit solutions we impose a von Neumann-Morgenstern utility function featuring constant absolute risk aversion of degree λ: u(x) = −e −λx. The first row represents the expected utility from tax optimisation. The second row denotes the expected utility from tax evasion, whereas the third row captures the utility from neither optimising nor evading taxes. Equation (5) is solved by choosing ζ such that ∇ζd ⋅PEU = 0 and selecting the maximum element of PEU(ζ ∗). We then obtain optimal tax planning and tax evasion effort levels

2.3 Introducing Agents and Social Utility

Recent experimental studies indicate that the unethical behaviour of one group member increases the likelihood of other group members behaving unethically, too [7]. Therefore, agents receive social utility from acting in line with their environment, while they receive social disutility when differing from mainstream behaviour, which is reflected by the social utility term SU. Hence, the agents’ total expected utility consists of two parts: private expected utility PEU i as described above and social utility SU i of their respective behaviours. For reasons of notational convenience the “agent labelling” index i is dropped where possible. Thus, an agent’s problem can be written as

where SU is a vector of utility of social interaction variables [6]:

With random variables 𝜖 o, 𝜖 e, 𝜖 h capturing unobservable effects, Ω i denotes the set of members of agent i’s social network (= neighbours), m = |Ω i| denotes the number of neighbours, \(m_o=\sum _{k\in \varOmega _i}d_{o,k}\) denotes the number of optimising neighbours. s[⋅] is a concave “social utility function”; we set s[x] = −e −ρx, where ρ measures the level of interaction between an agent and his social network.

When optimising (first row), the share of optimising neighbours triggers a positive social utility whereas the share of evading neighbours causes social utility to shrink. When evading (second row), there is an inverse connection. Honest taxpayers receive negative social utility from observing both optimising and evading neighbours, not triggering any effects in turn.

3 Simulation Results

The model was set up using NetLogo 6.0.4 [10]. We impose a population with a total size of 1000 agents, with one half of them being inherently honest and the other half deciding according to the model developed above. All agents are initially connected to their 20 closest neighbours in a regular ring lattice and may as well be connected to any other agent in the network with a probability of 0.01. Each agent is endowed with an identical and constant pre-tax income W i = 25 and an individual risk aversion parameter λ i drawn from an uniform distribution over [0.47, 1]. Each period, every agent, except for those being inherently honest, reconsiders his decision considering his neighbours’ utilities. We assume that taxpayers who were found guilty of tax evasion refrain from both illegal evasion [8] and legal optimisation activities for 4 years. Links between two agents may rearrange with a certain probability. To resemble German law as closely as possible, we initially set our parameter values as follows: tax rate τ = 0.25 (doubling after period 20), complexity parameter γ = 5, low (high) audit frequency p L = 0.024 (p H = 0.063), penalty rate t = 0.8 and cost of tax optimisation h = 0.033. High social interaction parameter ρ H equals low social interaction parameter ρ L ⋅ 1000.

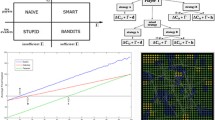

Every simulation runs for 40 periods. Performing five runs for every setting, the figures show mean values. Figure 1 contains four charts, each of them showing the evolution of the ratio of optimising (solid line), evading (dashed line) and honest (dotted line) agents simulating different scenarios. Scenario 1 shows the baseline scenario, while scenarios 2–4 each consider different settings.

Evolution of shares of optimising, evading and honest agents

Results show that taxpayers favour illegal evasion over legal optimisation in most settings. In our baseline scenario (Scen. 1), the share of evading agents rises over time. Increasing tax rate τ reinforces this effect, implicitly stating that increasing tax payments may cause taxpayers to take the risk of evading. However, increasing audit frequency (Scen. 2) causes the relation between evading and optimising agents to shrink, but tax evasion still seems to be the superior strategy. After period 20 taxpayers alternate their strategy in favour of optimising. Observing their neighbourhood’s evasion activities, taxpayers reconsider this decision after only a few periods. Increasing social pressure (Scen. 3)—i.e., taxpayers strongly consider their neighbours’ behavior—results in a lower share of evading agents; high social pressure to conform reduces propensity to tax evasion. This result is particularly interesting since by assumption, behaving honestly does not directly trigger any positive effects. Simulation of setting honest agents being not inherently honest (Scen. 4) delivers another highly surprising result. Compared to our baseline scenario, the gap between evading agents and optimising agents increases considerably. It hardly seems intuitive that taxpayers apparently tend to favour illegal actions if they don’t have to be honest by assumption. Furthermore, there is some upper boundary for the share of evaders at roughly 0.4, since detection causes an agent to refrain from illegal activities and additionally provokes his evading neighbors’ social utility to decrease.

4 Conclusion

Based on our analytical model, we use an agency-based approach to simulate the effects of introducing the option of tax optimisation into a tax evasion model. We further take into account social utility as previous research has shown significant influence. We find that taxpayers favour illegal evasion over legal optimisation in most cases. Results indicate that social interactions are highly influential for the relation between evading and optimising agents. Especially the assumption of agents being inherently honest drives our results.

References

Allingham, M.G., Sandmo, A.: Income tax evasion: a theoretical analysis. J. Pub. Econ. 1, 323–338 (1972)

Alm, J., McKee, M.: Tax compliance as a coordination game. J. Econ. Behav. Organ. 54, 297–312 (2004)

Bernasconi, M.: Tax evasion and orders of risk aversion. J. Pub. Econ. 67, 123–134 (1998)

Bloomquist, K.: Tax compliance as an evolutionary coordination game: an agent-based approach. Pub. Fin. Rev. 39, 25–49 (2011)

Erard, B., Feinstein, J.S.: Honesty and evasion in the tax compliance game. Rand J. Econ. 49(Supplement), 70–89 (1994)

Fortin, B., Lacroix, G., Villeval, M.-C.: Tax evasion and social interactions. J. Pub. Econ. 91, 2089–2112 (2007)

Gino, F., Ayal, S., Ariely, D.: Contagion and differentiation in unethical behavior. Psychol. Sci. 20, 393–398 (2009)

Hokamp, S., Pickhardt, M.: Income tax evasion in a society of heterogeneous agents – evidence from an agent-based model. Int. Econ. J. 24, 541–553 (2010)

Watts, D.J., Strogatz, S.H.: Collective dynamics of ‘small-world’ networks. Nature 393, 440–442 (1998)

Wilensky, U.: NetLogo. Center for Connected Learning and Computer-Based Modeling, Northwestern University, Evanston, IL (1999). http://ccl.northwestern.edu/netlogo/

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2020 The Editor(s) (if applicable) and The Author(s), under exclusive license to Springer Nature Switzerland AG

About this paper

Cite this paper

Diller, M., Lorenz, J., Meier, D. (2020). Tax Avoidance and Social Control. In: Neufeld, J.S., Buscher, U., Lasch, R., Möst, D., Schönberger, J. (eds) Operations Research Proceedings 2019. Operations Research Proceedings. Springer, Cham. https://doi.org/10.1007/978-3-030-48439-2_77

Download citation

DOI: https://doi.org/10.1007/978-3-030-48439-2_77

Published:

Publisher Name: Springer, Cham

Print ISBN: 978-3-030-48438-5

Online ISBN: 978-3-030-48439-2

eBook Packages: Business and ManagementBusiness and Management (R0)