Abstract

This article focused on the international practice of financial regulation of legal relations between the jurisdiction and its resident individuals owning the assets in other jurisdictions. Special attention is given to the analysis of international tax transparency impact.

The author provides comparative analysis of legal acts of states with different economic development level. The major conclusions can be outlined as follows:

-

at the global level financial regulation of the obligations of resident individuals owning the assets abroad is influenced by two competing trends: the need for liberalization of exchange restrictions and the need to strengthen fiscal control over cross-border taxpayers’ transactions. The level of economic development of the country determines, how much is expressed the displacement of exchange restrictions by tax rules;

-

intensive development of the tax law in many countries is indicated by working-out of new measures to counter tax evasion, both domestically and at the international level; spreading of practice of providing the taxpayers, owning the properties abroad, with additional procedural obligations; application of anti-offshore measures to individuals;

-

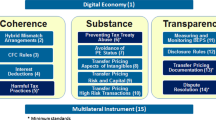

international tax transparency gives great opportunities to the state in the counteraction to tax evasion through cross-border financial transactions. But for effective use it is necessary to continue improvement of the administration of information, received during international exchange, as well as harmonization of legal rules and principles ensuring the implementation of international agreements in tax matters.

Access this chapter

Tax calculation will be finalised at checkout

Purchases are for personal use only

Similar content being viewed by others

References

Andres-Aucejo, E.: Towards an International Code for administrative cooperation in tax matter and international tax governance. Revista Derecho del Estado 40, 45–85 (2018). http://dx.doi.org/10.18601/01229893.n40.03. Accessed 27 May 2019

Avi-Yonah, R.S.: All of a piece throughout – the four ages of U.S. international taxation. Va. Tax Rev. 25(2), 313–338 (2005)

Avi-Yonah, R.S.: International tax as international law. Tax L. Rev. 57(4), 483–501 (2004)

Bogdan, M.: Concise Introduction to Comparative Law, p. 202. Europa Law Publishing, Groningen (2013)

Drake, K.D., Lusch, S.J., Stekelberg, J.: Does tax risk affect investor valuation of tax avoidance? J. Acc. Audit. Financ. 34(1), 151–176 (2019). https://doi.org/10.1177/0148558X17692674

Eden, L., Kudrle, R.T.: Tax havens: renegade states in the international tax regime? Law Policy 27(1), 100–127 (2005)

FATF: FATF Members and Observers (2019). https://www.fatf-gafi.org/about/membersandobservers/. Accessed 27 May 2019

Hilling, M.: Justifications and proportionality: an analysis of the ECJ’s assessment of national rules for the prevention of tax avoidance. Intertax 41(5), 294–307 (2013)

International Monetary Fund: World Economic Outlook Database, April 2019 Edition (2019a). https://www.imf.org/external/pubs/ft/weo/2019/01/weodata/index.aspx. Accessed 30 May 2019

International Monetary Fund: Monetary and Capital Markets Department: Annual Report on Exchange Arrangements and Exchange Restrictions 2018 (2019b). https://www.imf.org/en/Publications/Annual-Report-on-Exchange-Arrangements-and-Exchange-Restrictions/Issues/2018/08/10/Annual-Report-on-Exchange-Arrangements-and-Exchange-Restrictions-2017-44930. Accessed 30 May 2019

Joscelyne, M., Wentworth-May, M.: The UK’s New CFC Regime. Thomson Reuters Practical Law (2012). https://uk.practicallaw.thomsonreuters.com/: resource id 0-519-8741. Accessed 27 May 2019

Mara, E.R.: Determinants of tax havens. Procedia Econ. Financ. 32, 1638–1646 (2015)

Meyer, R.A.: Tax transparency. Bus. Horiz. 56, 543–549 (2013)

Morten, B., Zeume, S.: Rev. Financ. Stud. 31(4), 1221–1264 (2018). https://doi.org/10.1093/rfs/hhx122. Accessed 30 May 2019

Morris, M.: The 26 OECD Common Reporting Standard Loopholes (2017). http://www.the-best-of-both-worlds.com/support-files/oecd-crs-loopholes-report.pdf. Accessed 30 May 2019

Noked, N.: Tax evasion and incomplete tax transparency. Laws 7(3), 31 (2018a). https://doi.org/10.3390/laws7030031. Accessed 1 June 2019

Noked, N.: FATCA, CRS, and the wrong choice of who to regulate. Fla. Tax Rev. 22, forthcoming (2018b). https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3143663. Accessed 1 June 2019

OECD: Tax Transparency 2016 Report on Progress (2016). http://www.oecd.org/tax/transparency/GF-annual-report-2016.pdf. Accessed 30 May 2019

OECD: Standard for Automatic Exchange of Financial Account Information in Tax Matters, 2nd edn. (2017). https://www.oecd-ilibrary.org/taxation/standard-for-automatic-exchange-of-financial-account-information-in-tax-matters-second-edition_9789264267992-en;jsessionid=IW0_TZBRjv88sDJiI20E2i1C.ip-10-240-5-179. Accessed 30 May 2019

OECD: Consultation Document: Preventing Abuse of Residence by Investment Schemes to Circumvent CRS (2018a). http://www.oecd.org/tax/exchange-of-tax-information/consultation-document-preventing-abuse-of-residence-by-investment-schemes.pdf. Accessed 30 May 2019

OECD: Model Mandatory Disclosure Rules for CRS Avoidance Arrangements and Opaque Offshore Structures (2018b). http://www.oecd.org/tax/exchange-of-tax-information/model-mandatory-disclosure-rules-for-crs-avoidance-arrangements-and-opaque-offshore-structures.pdf. Accessed 30 May 2019

OECD: List of CRS MCAA signatories (2019a). http://www.oecd.org/tax/automatic-exchange/international-framework-for-the-crs/MCAA-Signatories.pdf. Accessed 30 May 2019

OECD: Member countries (2019b). https://www.oecd.org/about/members-and-partners/. Accessed 30 May 2019

Owens, J.: Tax transparency and BEPS. J. Tax Adm. 1(2), 1–10 (2015)

Pistone, P.: Coordinating the actions of regional and global players during the shift from bilateralism to multilateralism in international tax law. World Tax J. 6(1), 3–9 (2014)

Pross, A.: How tax transparency went global - the new automatic exchange standard: from concept to reality. Int. Tax Rev. (2015). https://www.internationaltaxreview.com/Article/3439573/How-tax-transparency-went-global-the-new-automatic-exchange-standard-from-concept-to-reality.html?ArticleId=3439573. Accessed 02 June 2019

Rust, A.: CFC legislation and EC law. Intertax. 36(11), 492–501 (2008)

Saint-Amans, P.: Global tax and transparency: we have the tools, now we must make them work. OECD Observer (2016). https://doi.org/10.1787/15615529. Accessed 03 June 2019

Safonova, M.F., Reznichenko, D.S., Melnichuk, M.V., Karaev, A.K., Litvinova, S.F.: Taxes harmonization features in the European union countries. Int. J. Econ. Financ. Issues 6(S8), 154–159 (2016)

Ermakova, E.P., Rusakova, E.P., Sitkareva, E.V., Frolova, E.E.: Main components of protecting consumers of financial products in Asian-Oceanic (APAC) Countries. Int. J. Eng. Technol. (UAE) 7(4), 157–162 (2018)

Schmidt, P.K.: Taxation of controlled foreign companies in context of the OECD/G20 project on base erosion and profit shifting as well as the EU proposal for the anti-tax avoidance directive – an interim Nordic assessment. Nordic Tax J. 2, 87–112 (2016). https://doi.org/10.1515/ntaxj-2016-0005

Dudin, M.N., Senin, A.S., Frolova, E.E., Abashidze, A.Kh., Rusakova, E.P.: The role of the economic and mathematical modeling in the sustainable development of the foreign trade policy of modern countries. Int. J. Appl. Bus. Econ. Res. 15(8), 43–51 (2017)

Inshakova, A.O., Goncharov, A.I., Inshakova, E.I.: Innovative technologies of oil production: tasks of legal regulation of management and taxation. In: Inshakov, O.V., Inshakova, A.O., Popkova, E.G. (eds.) Energy Sector: A Systemic Analysis of Economy, Foreign Trade and Legal Regulations, pp. 79–94. Springer, Cham (2019). https://doi.org/10.1007/978-3-319-90966-0_6

Sinn, H.-W.: Tax harmonization and tax competition in Europe. Eur. Econ. Rev. 34, 489–504 (1990)

Williamson, J.: Latin American Readjustment: How Much has Happened? Peterson Institute for International Economics, Washington (1990). https://piie.com/commentary/speeches-papers/what-washington-means-policy-reform. Accessed 02 June 2019

Zelinsky, E.A.: Defining residence for income tax purposes: domicile as gap-filler, citizenship as proxy and gap-filler. Mich. J. Int. Law 38, 271 (2017). http://repository.law.umich.edu/mjil/vol38/iss2/5. Accessed 15 May 2019

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2020 Springer Nature Switzerland AG

About this paper

Cite this paper

Tsepova, E.A. (2020). Individuals’ Capital Allocation in Different Jurisdictions Within the Context of International Tax Transparency: Improving the Global Approaches to Financial Regulation. In: Popkova, E., Sergi, B. (eds) Scientific and Technical Revolution: Yesterday, Today and Tomorrow. ISC 2019. Lecture Notes in Networks and Systems, vol 129. Springer, Cham. https://doi.org/10.1007/978-3-030-47945-9_172

Download citation

DOI: https://doi.org/10.1007/978-3-030-47945-9_172

Published:

Publisher Name: Springer, Cham

Print ISBN: 978-3-030-47944-2

Online ISBN: 978-3-030-47945-9

eBook Packages: Intelligent Technologies and RoboticsIntelligent Technologies and Robotics (R0)